- Medical Devices

- Acute Care Hospital Beds and Stretchers Market

Acute Care Hospital Beds and Stretchers Market Size, Share, and Growth Forecast, 2025 - 2032

Acute Care Hospital Beds and Stretchers Market By Product Type (Beds, Stretchers), by End-user, and Regional Analysis for 2025 - 2032

Acute Care Hospital Beds and Stretchers Market Share and Trends Analysis

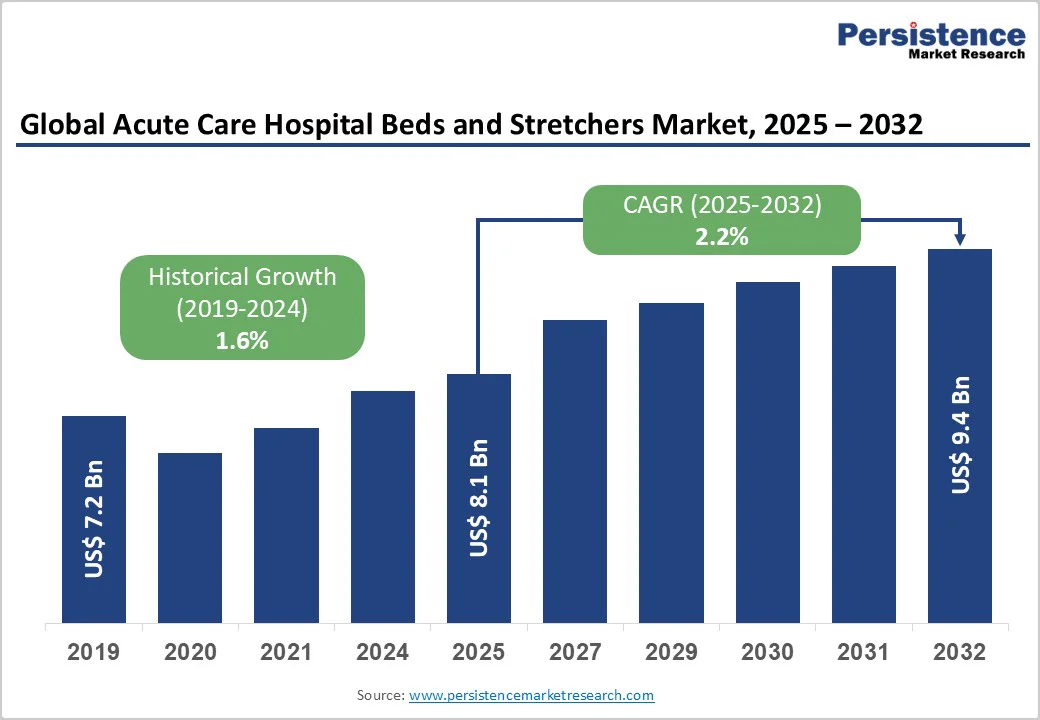

The global acute care hospital beds and stretchers market size is likely to be valued at US$8.1 billion in 2025 and is expected to reach US$9.4 billion by 2032, growing at a CAGR of 2.2% during the forecast period from 2025 to 2032, driven by the rising incidence of chronic diseases, trauma cases, and surgical procedures requiring immediate medical intervention.

Increasing hospital admissions, expanding healthcare infrastructure, and advancements in bed and stretcher designs to enhance patient comfort and safety are key market accelerators. Technological innovations such as smart, adjustable, and automated systems are improving workflow efficiency in acute care settings.

Key Industry Highlights

- Key Opportunity: Companies can invest in R&D or acquisitions in “smart bed” tech and market to hospitals, emphasizing workflow efficiency and patient safety.

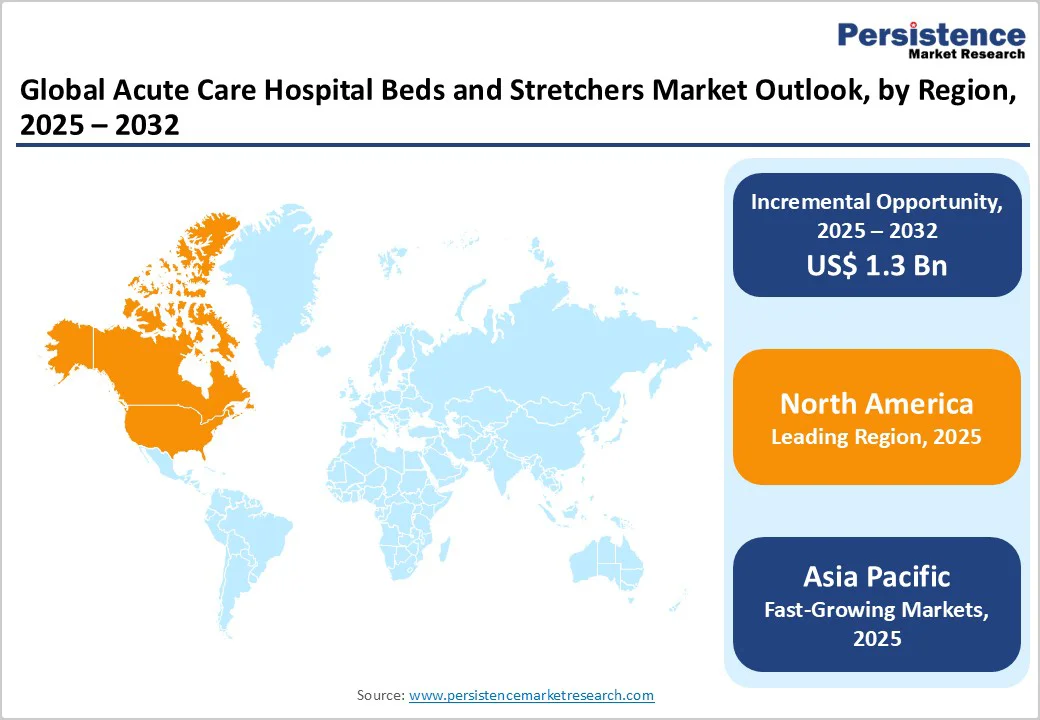

- Regional Dominance: Asia Pacific is the fastest-growing region, driven by rapid hospital infrastructure development, rising trauma and chronic disease admissions, and increasing demand for advanced ICU beds and powered stretchers across China, India, and Southeast Asia.

- Driver: The growing prevalence of chronic and acute conditions such as cardiovascular diseases, trauma, and infections drives product demand.

- Trend: Integration of IoT-enabled and automated hospital beds enhances patient monitoring and safety.

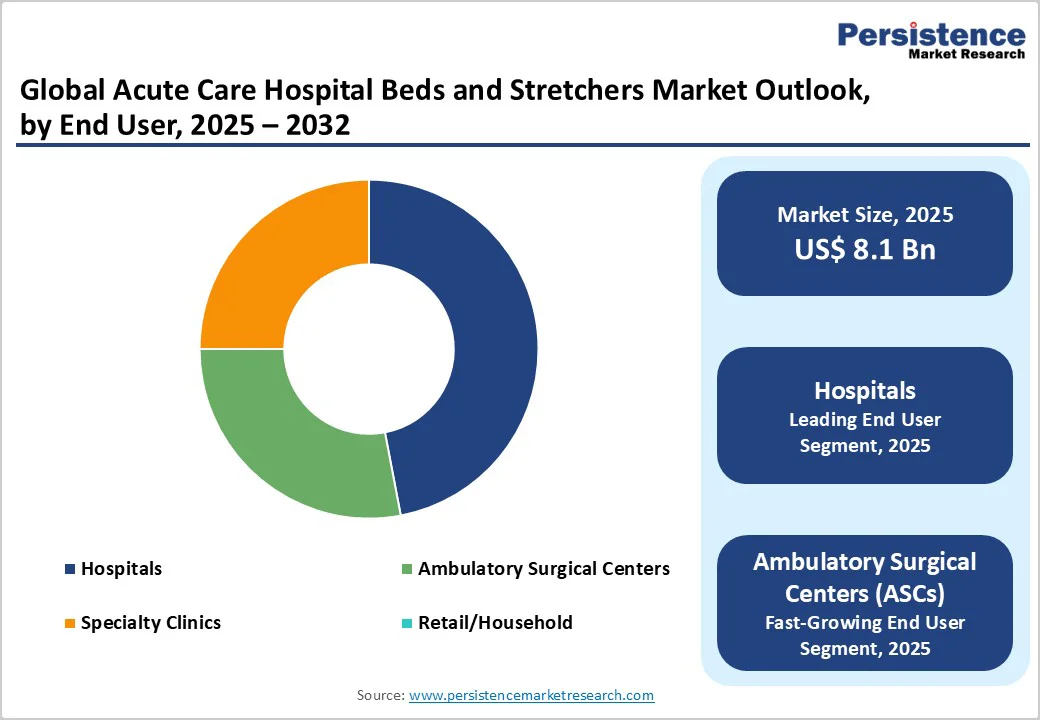

- Dominating Product Type: The beds segment holds the largest share in the acute care hospital beds and stretchers market since hospital beds are an essential and permanent part of all acute care settings, unlike stretchers, which are used temporarily for patient transport.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$8.1 Bn |

|

Market Value Forecast (2032F) |

US$9.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

2.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

1.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Post-Surgical Recovery Demand

The growing number of complex and minimally invasive surgeries worldwide has significantly increased the need for specialized post-surgical recovery infrastructure, particularly advanced adjustable hospital beds. Patients undergoing cardiac, orthopedic, and neurological surgeries often require prolonged and carefully monitored recovery periods, necessitating beds that support multiple positioning, pressure management, and enhanced comfort.

Modern acute care beds with electric adjustments, integrated monitoring systems, and anti-decubitus features help prevent complications such as bedsores and improve patient outcomes. Hospitals are increasingly prioritizing these technologically advanced beds to ensure faster rehabilitation, reduce caregiver workload, and enhance overall patient satisfaction during the critical post-operative recovery phase.

High Initial Investment Costs

The adoption of advanced electric and smart hospital beds in acute care settings is often hindered by their high initial investment costs. These beds incorporate sophisticated technologies such as motorized adjustments, integrated monitoring systems, and patient-safety features, which significantly increase their purchase price compared to traditional manual beds.

Smaller hospitals, rural clinics, and budget-constrained healthcare facilities often struggle to allocate sufficient capital for such upgrades, despite their clinical benefits. Consequently, many institutions continue using basic beds, delaying the modernization of patient care infrastructure. This cost barrier slows widespread market penetration and limits access to enhanced patient comfort and safety features.

Portable and Modular Stretchers

The rising frequency of emergencies, natural disasters, and mass casualty events has created a critical demand for portable and modular stretchers in acute care settings. Lightweight, foldable, and multifunctional designs allow rapid deployment in ambulances, field hospitals, and disaster relief zones, ensuring timely patient transport and care. These stretchers often feature adjustable height, collapsible frames, and integrated safety restraints, enabling medical personnel to handle diverse patient conditions efficiently.

Modular designs allow components to be interchanged or expanded for specialized procedures, offering versatility and durability. As hospitals and emergency responders prioritize mobility and quick response, such innovative stretchers present a significant market opportunity.

Category-wise Analysis

Product Type Insights

Hospital beds dominate the acute care market because they are fundamental to patient care, providing continuous support for recovery, monitoring, and treatment. Unlike stretchers, which are primarily used for short-term transport, beds are required for every inpatient, including ICU, post-surgical, and long-term care patients.

Modern beds offer advanced features such as electric adjustability, pressure management, built-in monitoring systems, and infection-control surfaces, making them indispensable in acute care facilities. Rising surgical volumes, an aging population, and the expansion of multi-specialty hospitals further reinforce their demand. Beds consistently generate higher sales and maintain the largest market share.

End-user Insights

Hospitals lead the acute care beds and stretchers market due to their high patient volumes, diverse treatment requirements, and 24/7 operational demands. They house multiple departments, ICUs, emergency rooms, surgical units, and long-term care wards, each requiring dedicated beds with advanced adjustability, monitoring systems, and safety features.

Stretchers are also essential for rapid patient transport within these large facilities. Unlike ambulatory surgical centers or specialty clinics, which primarily handle outpatient or short-duration procedures, hospitals manage critical and complex cases that necessitate continuous patient support. This extensive, multi-departmental need makes hospitals the largest and most consistent consumer in the market.

Regional Insights

North America Acute Care Hospital Beds and Stretchers Trends

North America, particularly the U.S., is a dominant region in the acute care hospital beds and stretchers market due to advanced healthcare infrastructure, high healthcare expenditure, and a growing prevalence of chronic and acute illnesses.

Hospitals increasingly adopt smart beds with IoT-enabled monitoring, pressure-relief mattresses, and electric adjustability to enhance patient outcomes. Rising surgical volumes, an aging population, and stringent regulatory standards drive demand for both beds and modular stretchers. Emergency preparedness and trauma care initiatives in the U.S. also encourage investments in portable, multifunctional stretchers. Strong government support and private hospital expansions reinforce North America’s leading market position.

Asia Pacific Acute Care Hospital Beds and Stretchers Market Trends

The Asia Pacific region is emerging rapidly in the acute care hospital beds and stretchers market due to expanding healthcare infrastructure, rising hospital admissions, and increasing government investments in modern medical facilities.

Countries, including China, India, Japan, and Australia, are witnessing a surge in chronic disease prevalence and surgical procedures, driving demand for advanced beds with adjustable, smart, and infection-control features. Growing emergency care services and disaster preparedness programs are boosting the adoption of portable and modular stretchers. Rising healthcare awareness, urbanization, and private hospital expansions further accelerate market growth, positioning Asia Pacific as a key emerging region in the sector.

Europe Acute Care Hospital Beds and Stretchers Market Trends

Europe’s acute care hospital beds and stretchers market is shifting toward fully digital, interoperable critical-care beds integrated with nurse-call platforms, EMR connectivity, and automated fall-prevention systems. Hospitals across Germany, the U.K., France, and the Nordic countries are prioritizing ergonomic, low-height beds and powered stretchers to reduce caregiver injuries and comply with stringent EU safety mandates.

Sustainability has become a major purchasing criterion, driving demand for recyclable frames, energy-efficient motors, and long-life-cycle designs. Additionally, aging infrastructure replacement cycles, growing ICU admissions from geriatric populations, and standardization toward pressure ulcer-prevention surfaces are accelerating premium product uptake across Europe.

Competitive Landscape

The global acute care hospital beds and stretchers market is highly competitive, driven by continuous innovation, technological advancements, and the need for differentiated patient care solutions. Market players focus on developing smart beds, ergonomic stretchers, and IoT-enabled systems to enhance patient safety, comfort, and caregiver efficiency. Strategic partnerships, mergers, and acquisitions are common to expand geographic reach and product portfolios. Emphasis on cost-effective, modular, and multifunctional designs allows companies to cater to diverse healthcare settings, from large hospitals to emergency response units.

Key Industry Developments:

- In June 2025, Agiliti, a leading manufacturer and provider of medical device solutions to the U.S. healthcare industry, launched NP Line™ of stretcher support surfaces, which were clinically engineered to deliver safer patient care.

- In March 2025, China developed an advanced smart transfer bed that transferred patients who had undergone major surgeries from one bed to another without causing any stress or pain.

Companies Covered in Acute Care Hospital Beds and Stretchers Market

- Invacare Corporation

- Hill-Rom Holdings Inc.

- Stryker Corporation

- LINET

- Getinge AB (ArjoHuntleigh)

- PARAMOUNT BED CO., LTD.

- Midmark Corp

- Howard Wright Limited

Frequently Asked Questions

The acute care hospital beds and stretchers market is projected to be valued at US$8.1 Billion in 2025.

The key drivers include an increasing number of surgeries, chronic disease cases, and emergency admissions that require advanced beds and stretchers.

The acute care hospital beds and stretchers market is poised to witness a CAGR of 2.2% between 2025 and 2032.

The key opportunities include IoT-enabled beds for real-time monitoring and remote patient management.

The key players include Invacare Corporation, Hill-Rom Holdings Inc., Stryker Corporation, and LINET.