- Healthcare Services

- Weight Loss Services Market

Weight Loss Services Market Size, Share, Trends, Growth, Regional Forecasts, 2026 - 2033

Weight Loss Services Market by Function (Fitness Centers, Slimming Centers, Consultation Services, Digital Programs, Surgical Services), Payment Model (Out-of-Pocket Payment, Government Programs, Private Insurance Coverage), End-User (Individual Consumers, Corporate Programs, Healthcare Institutions), and Regional Analysis for 2026 - 2033

Weight Loss Services Market Share and Trends Analysis

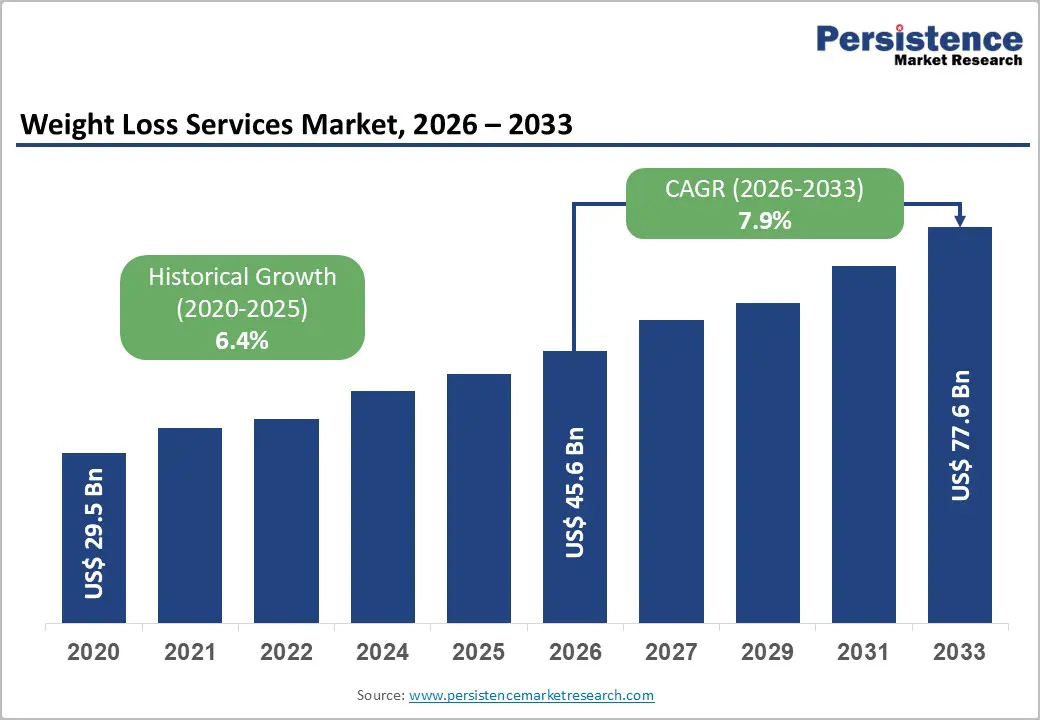

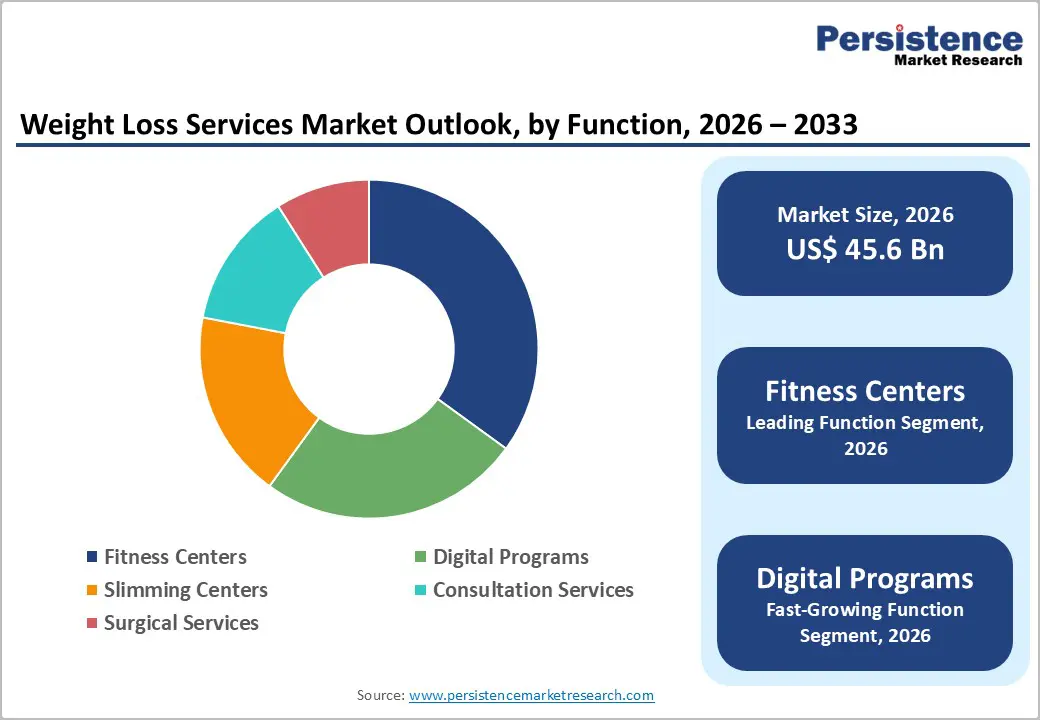

The global weight loss services market size is likely to be valued at US$ 45.6 billion in 2026, and is project to reach US$ 77.6 billion by 2033, growing at a CAGR of 7.9% during the forecast period 2026−2033. Market growth is driven by rising prevalence of overweight and obesity, increasing demand for structured weight management services. Greater awareness of clinical efficacy and safety has boosted adoption among individual consumers and institutional clients.

Integration of digital platforms, telehealth, and personalized mobile applications enhances service delivery, adherence, and operational efficiency. Urbanization, higher disposable income, and changing lifestyles fuel demand for professional fitness, dietary, and surgical services. Expanded healthcare infrastructure, including certified fitness centers, specialized clinics, and advanced surgical facilities, supports scalable provision. Regulatory recognition of structured programs has facilitated market penetration through insurance coverage and reimbursement pathways.

Key Industry Highlights

- Leading Function: Fitness centers are projected to hold the largest revenue share at about 35% in 2026, driven by accessibility, clinical acceptance, and subscription-based models.

- Fastest-Growing Function: Digital programs are expected to grow the fastest during 2026–2033, supported by mobile apps, telehealth, and AI-driven personalization.

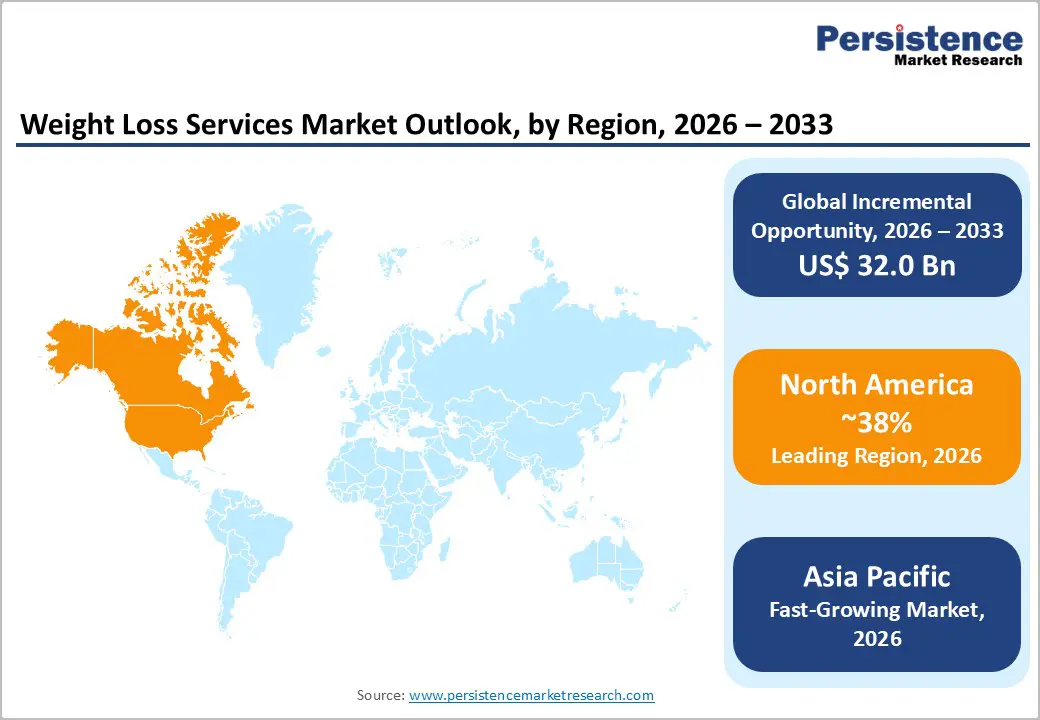

- Regional Leadership: North America is poised to lead in 2026 with an estimated 38% of the market share in 2026, supported by strong infrastructure and digital adoption

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing regional market through 2033, powered by large-scale urbanization and widening health awareness.

- Competitive Environment: The market is moderately consolidated with leading global chains and regional providers focusing on hybrid models, technology integration, and corporate partnerships.

- March 2026: Indian pharma companies launched low-cost generic semaglutide to boost access to diabetes and weight-loss treatments.

| Key Insights | Details |

|---|---|

|

Weight Loss Services Market Size (2026E) |

US$ 45.6 Bn |

|

Market Value Forecast (2033F) |

US$ 77.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.4% |

DRO Analysis

Rising Prevalence of Overweight and Obesity

Rapid growth in overweight and obesity increases demand for intervention services. In 2022, about 43% of adults worldwide were overweight and 16% were living with obesity, showing widespread need for professional solutions. Higher prevalence raises healthcare concerns related to chronic diseases that are costly to manage. Consumers seek structured support to reduce health risks and improve quality of life. Growing numbers of individuals and families require access to services that offer measurable outcomes. Providers are responding with comprehensive programs covering diet, exercise, clinical monitoring and behavioral guidance to meet the rising treatment demand.

Persistent increases in overweight and obesity strain healthcare infrastructures and public health systems. Governments and insurers face higher long-term costs linked to related illnesses. Greater prevalence motivates policy makers and employers to invest in preventive and therapeutic services. Health systems expand capacity for certified professionals and accredited programs to address this burden. Wider public awareness of risk factors drives individual engagement with professional support. Service providers are scaling offerings to include personalized plans and technology-supported interventions to respond to rising demand from diverse patient groups.

Integration of Digital Health and Technological Platforms

Government resources show that remote healthcare tools such as telehealth, mobile apps, and digital tracking are recommended to manage chronic disease risk factors including obesity and related conditions. Telehealth interventions support improved self-management of diet and physical activity and can reach patients who face barriers attending in-person services, such as rural populations or those with limited mobility. These tools allow ongoing monitoring of patient progress and provide frequent touchpoints with healthcare professionals through video, text, and mobile interfaces. Evidence shows that digital health tools extend access to care and support behavior change in ways that traditional services cannot given time and resource constraints.

Digital platforms are increasingly adopted because they deliver personalized experiences at scale and lower operational costs. Mobile applications, wearable devices, and electronic communication enable real-time self-monitoring of weight, activity, and nutrition, improving engagement and adherence to structured plans. Government telehealth recommendations highlight that interactive digital functions such as goal-setting, reminders, and remote data sharing improve dietary outcomes and support sustained behavior changes without requiring face-to-face visits. The U.S. Community Preventive Services Task Force supports telehealth interventions for chronic disease risk management, including obesity, indicating public health confidence in digital care models.

High Operational and Treatment Costs

Establishing certified fitness centers, specialized clinics, and advanced surgical facilities requires substantial capital investment. High-cost medical devices, fitness equipment, and technology-intensive systems contribute to elevated operational expenses. Recruiting skilled professionals, including nutritionists, personal trainers, and clinical staff, demands competitive compensation, increasing service pricing. Continuous procurement of dietary supplements, consumables, and maintenance of equipment adds recurring costs. Personalized weight management programs, structured fitness regimens, and surgical interventions require extensive monitoring and resource allocation.

Complex treatment protocols and follow-up consultations increase operational time and resource utilization. Compliance with clinical regulations, safety standards, and certification requirements necessitates ongoing investment in quality control and administrative oversight. Limited insurance coverage in several regions shifts financial responsibility to end users, affecting adoption rates. High operational expenditures reduce profitability for smaller providers and create challenges in sustaining service quality. Market participants must manage staffing, equipment maintenance, and patient support simultaneously, intensifying cost structures.

Regulatory and Clinical Acceptance Challenges

Regulatory frameworks governing weight loss services are often fragmented and inconsistent across regions, creating complexity for service providers seeking market entry. Strict compliance requirements for clinical validation, certifications, and safety standards increase operational costs and extend time-to-market for new programs and technologies. Insurance coverage and reimbursement approvals remain limited, restricting access for a wider consumer base and slowing adoption rates. Approval delays for novel digital or surgical interventions reduce competitive advantage for early movers, while uncertainty in regulatory interpretations creates risk for investors and institutional clients considering partnerships or service expansions.

Clinical acceptance remains cautious due to variability in efficacy evidence for diverse weight management interventions. Healthcare professionals prioritize treatments supported by peer-reviewed research and long-term outcomes, creating barriers for emerging digital, dietary, or fitness programs lacking rigorous trials. Skepticism from clinicians limits referrals and endorsement, reducing consumer confidence and affecting program enrollment. Service providers must invest in structured clinical studies and outcome tracking to gain credibility. Inconsistent clinical guidelines across countries further challenge standardization of treatment protocols, complicating scalability and operational integration for multi-regional service providers.

Introduction of Innovative, Personalized Dietary and Fitness Solution

Rising clinical evidence and personalization enable more effective dietary and fitness solutions that align with individual health profiles. Tailored programs use data from assessments to specify nutrient targets, caloric needs, and behavioral patterns. Such customization improves participant engagement and measurable outcomes compared with generic plans. With US adult obesity still high at around 40.3% of the population in 2024 according to the Centers for Disease Control and Prevention (CDC), demand for targeted approaches increases as individuals seek interventions suited to their unique risk factors and goals.

Service providers can deliver differentiated offerings leveraging wearables, mobile tracking, and clinician oversight. Personalized solutions support integration of physical activity data and dietary adherence metrics. Insurers and employers see value in measurable, data-backed plans that may reduce long-term health costs. Employers increasingly partner with providers to improve workforce health. Public health agencies emphasize lifestyle interventions as critical complements to medical care for chronic conditions linked to overweight.

Partnerships with Corporate Wellness Programs

Workplace health initiatives reach large employee populations and offer structured environments for preventive care and behavior change. U.S. government health resources note that worksite nutrition and physical activity programs are designed to improve health-related behaviors and outcomes among employees by increasing access to healthy choices and promoting physical activity and dietary education at work. These programs operate where adults spend most of their awake hours, creating repeated touchpoints for weight management engagement and support for lifestyle improvements without competing with personal time outside work.

Offering wellness benefits aligns employer interests with workforce health metrics such as reduced absenteeism, lower chronic disease risk and improved productivity. Public data from the U.S. Bureau of Labor Statistics shows that in March 2025, about 60 % of private-industry workers had access to wellness programs in establishments with 500 or more workers, indicating widespread organizational adoption of health-focused benefits. These programs strengthen employer-employee partnerships and can lead to improved weight outcomes by embedding supportive interventions within daily work routines.

Category-wise Analysis

Function Insights

Fitness centers are anticipated to secure around 35% of the weight loss services market revenue share in 2026, reflecting widespread accessibility, established brand presence, and integration of structured exercise regimens. These centers benefit from high clinical acceptance of exercise-based weight management as preventive and therapeutic interventions. Providers utilize certified trainers, evidence-based protocols, and group programs to enhance adherence and measurable outcomes. Urban penetration, retail visibility, AI-guided workouts, wearable integration, and performance tracking improve personalization and efficiency. Fitness centers offer scalable, cost-effective solutions for individual consumers, corporate clients, and healthcare institutions.

Digital programs are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by increasing adoption of mobile applications, telehealth consultations, and virtual coaching. Digital platforms provide personalized diet, exercise, and behavioral interventions, expanding access to remote and underserved populations. Integration of wearable devices, Artificial Intelligence (AI) analytics, and teleconsultation enhances engagement, adherence, and long-term retention. Flexible, on-demand solutions, corporate wellness collaborations, and subscription-based models support rapid adoption while combining clinical credibility with technology-enabled convenience.

End-User Insights

Individual consumers are likely to be the leading segment with a projected 55% of the weight loss services market share in 2026 due to widespread demand for personalized and flexible weight management solutions. Structured programs, including exercise, dietary, and digital interventions, drive adoption among health-conscious individuals. Expert consultations, provider referrals, and evidence-based protocols enhance trust and adherence. Mobile platforms and digital tools improve accessibility, monitoring, and engagement. Cost-effective, subscription-based non-surgical interventions, urbanization, rising income, and lifestyle awareness further support sustained growth and scalability.

Corporate programs are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by increasing employer investment in employee wellness initiatives. Organizations adopt structured weight management programs to improve productivity, reduce healthcare costs, and enhance workforce satisfaction. Digital platforms, telehealth, and on-site facilities enable scalable delivery across locations. Cost-effective, outcome-driven interventions with corporate incentives and insurance alignment encourage participation. Provider partnerships allow program customization, performance tracking, and technology-enabled engagement, with urban and industrial adoption accelerating recurring revenue and operational scalability.

Regional Insights

North America Weight Loss Services Market Trends and Insights

North America is expected to lead with an estimated 38% of the weight loss services market value in 2026, supported by advanced healthcare infrastructure and well-established service networks. High adoption of structured fitness centers, clinical programs, and digital weight management platforms ensures widespread consumer engagement. Strong presence of certified trainers, nutrition specialists, and outcome-driven protocols drives program credibility. Corporate wellness initiatives and insurance coverage for structured interventions further increase accessibility. Consumer demand for personalized, evidence-based solutions encourages continuous innovation. Integration of wearable devices, AI analytics, and mobile applications improves adherence and operational efficiency across both individual and institutional segments.

Robust investment in research and technology strengthens market dominance. Strategic partnerships between providers and healthcare institutions enable service standardization and expansion. Urban population density, high disposable income, and lifestyle-related health concerns accelerate demand for professional weight management. Data-driven program monitoring, subscription models, and telehealth consultations facilitate scalable service delivery. Regulatory recognition of clinical programs ensures legitimacy, while performance-tracking systems enhance measurable outcomes. Consumer preference for flexible, non-surgical interventions reinforces growth. Established brand presence and diversified service offerings secure revenue streams across multiple service channels, sustaining competitive advantage in the market.

Europe Weight Loss Services Market Trends and Insights

Europe demonstrates a mature weight loss services market with steady growth driven by rising health awareness and preventive healthcare adoption. Fitness centers, dietary clinics, and digital platforms provide structured weight management solutions. Consumers increasingly seek evidence-based exercise, nutritional, and behavioral interventions through certified professionals and technology-enabled platforms. Corporate wellness programs and insurance-aligned services drive adoption among employed populations. Telehealth consultations and mobile applications expand reach to semi-urban and remote populations, supporting scalable delivery. Urban lifestyle changes and rising disposable income further boost enrollment.

Investment in technology-driven programs strengthens market evolution. AI-guided exercise, wearable integration, and digital dietary tracking improve engagement and outcomes. Partnerships with healthcare institutions enable standardization, outcome validation, and recurring revenue streams. Non-surgical interventions, subscription models, and group-based fitness programs maintain cost efficiency and accessibility. Aging populations and lifestyle-related health risks increase demand for preventive services. Mobile platforms, corporate collaborations, and outcome-focused programs encourage adoption, allowing providers to capture new segments and optimize scalability.

Asia Pacific Weight Loss Services Market Trends and Insights

Asia Pacific is forecasted to be the fastest-growing market for weight loss services between 2026 and 2033, stimulated by rapid urbanization and rising prevalence of overweight and obesity. China sees strong adoption of mobile-based weight management platforms, AI coaching, and digital monitoring in cities. India demonstrates growing demand for structured corporate wellness programs, telehealth consultations, and subscription-based dietary and fitness services. Japan experiences growth from aging populations seeking preventive interventions. South Korea shows increasing uptake of personalized diet, exercise, and wearable-integrated programs among health-conscious individuals. Rising income and lifestyle changes accelerate market expansion.

Investment in digital infrastructure and teleconsultation platforms drives accessibility and scalable service delivery. AI-powered applications, wearable devices, and performance-tracking tools enhance engagement, adherence, and measurable outcomes. Fitness centers, certified trainers, and evidence-based diet programs improve credibility and trust. Corporate partnerships and healthcare collaborations enable standardized delivery and recurring revenue streams. Subscription models, insurance-aligned services, and urban penetration boost adoption. Data-driven insights optimize efficiency and retention, positioning providers to capitalize on emerging opportunities in health-conscious markets across urban and semi-urban regional markets.

Competitive Landscape

The global weight loss services market demonstrates a moderately consolidated structure, with major players capturing a significant revenue share while regional and niche providers operate in fragmented segments. Key companies such as Weight Watchers, Jenny Craig, Slimming World, Nutrisystem, LA Fitness International, and Orangetheory Fitness exert substantial influence through brand recognition, extensive networks, and diversified offerings. Market concentration is higher in North America and Europe due to established chains and regulatory oversight, supporting structured program adoption.

Competitive positioning focuses on differentiation through clinical credibility, integration of digital platforms, and hybrid service delivery. Providers leverage evidence-based programs, subscription models, and corporate wellness partnerships to enhance engagement and operational efficiency. Emphasis on measurable outcomes, personalized coaching, and technology-enabled solutions strengthens market presence. Fragmented regions present opportunities for growth, while strategic barriers created by leading players maintain competitive advantage and challenge new entrants seeking scale and brand visibility.

Key Industry Developments

- In January 2026, Medicover hospital launched a dedicated obesity clinic in Navi Mumbai offering medically supervised weight-management care, personalized nutrition, activity guidance, and behavioral support to address rising lifestyle-related weight challenges and long-term health outcomes.

- In November 2025, Novo Nordisk launched Wegovy in Hong Kong, making the once-weekly semaglutide treatment available for long-term weight-management care through clinics and select pharmacies.

- In May 2025, Evernorth introduced a first-of-its-kind pharmacy benefit capping monthly co-pays for weight-loss drugs such as Wegovy and Zepbound at US$ 200 to expand access and affordability for patients while streamlining prior authorization and reducing net prescription costs.

Companies Covered in Weight Loss Services Market

- Weight Watchers International, Inc.

- Jenny Craig, Inc.

- Slimming World Ltd.

- Nutrisystem, Inc.

- LA Fitness International LLC

- Orangetheory Fitness

- Gold’s Gym International, Inc.

- Anytime Fitness, LLC

- Life Time Fitness, Inc.

- Mediterranean Diet Centers

- F45 Training Pty Ltd.

- Planet Fitness, Inc.

Frequently Asked Questions

The global weight loss services market is projected to reach US$ 45.6 billion in 2026.

Rising prevalence of overweight and obesity, growing health awareness, and widening adoption of personalized, technology-enabled weight management programs are driving the market.

The market is poised to witness a CAGR of 7.9% from 2026 to 2033.

Expansion of digital platforms, telehealth services, corporate wellness programs, and affordable, evidence-based interventions is unlocking attractive market opportunities.

Some of the key market players include Weight Watchers, Jenny Craig, Slimming World, Nutrisystem, LA Fitness International, and Orangetheory Fitness.