- Industrial Goods & Service

- Underground Mining Equipment Market

Underground Mining Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Underground Mining Equipment Market by Equipment Type (Load-Haul-Dump (LHD) Loaders & Haulers, Underground Mining Trucks, Drilling Equipment, Bolters & Rock Support Equipment, Continuous Miners, Mining Shearers, Excavators & Scalers, Ventilation & Air Handling Systems), Mining Method (Room & Pillar Mining, Longwall Mining, Drill & Blast /Conventional Mining, Sublevel Caving / Block Caving Mining.), Mining Type and Regional Analysis for 2026 - 2033

Underground Mining Equipment Market Size and Trends Analysis

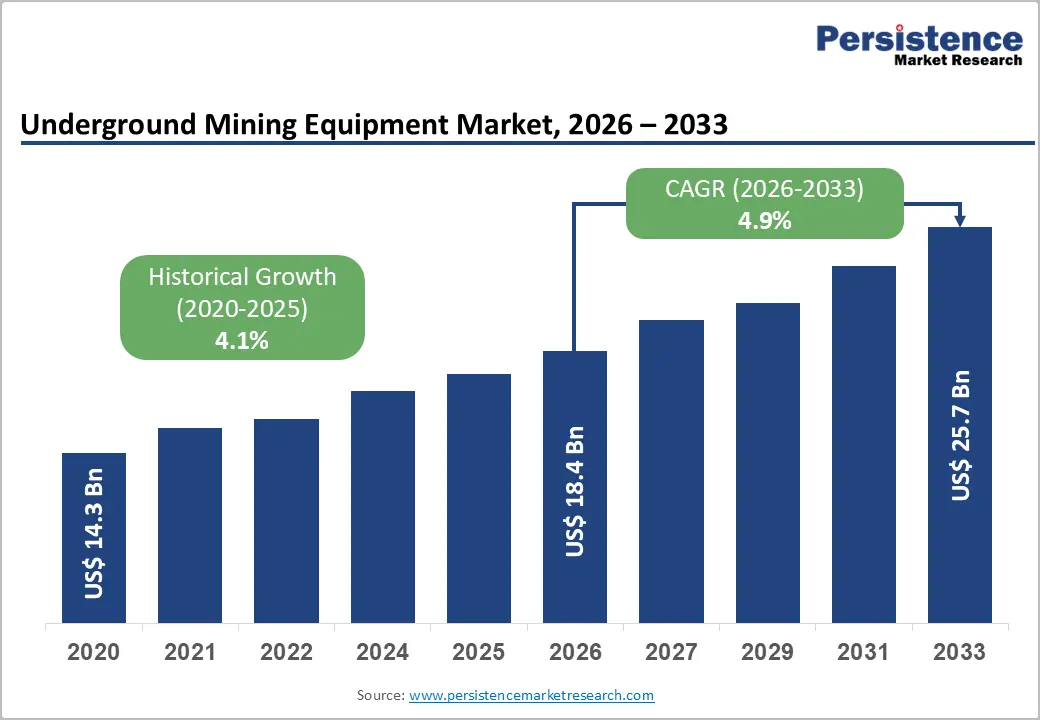

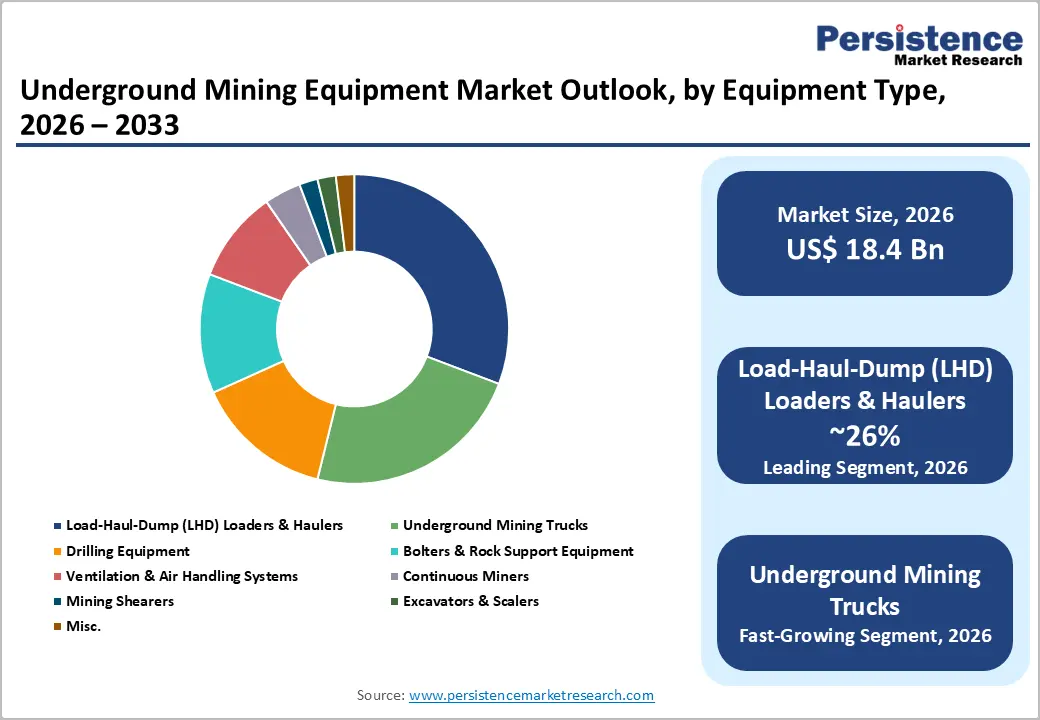

The global underground mining equipment market size is likely to be valued at US$ 18.4 billion in 2026 and is projected to reach US$ 25.7 billion by 2033, growing at a CAGR of 4.9 percent between 2026 and 2033.

This trajectory is underpinned by accelerating global mineral extraction activity, widespread fleet electrification programs, and intensifying investment in autonomous underground mining systems. According to global industry data, total world mining production reached 19.2 billion metric tons in 2023, nearly double the 9.6 billion metric tons recorded in 1985, a long-term volume surge that generates a sustained demand for purpose-built underground equipment.

Key Industry Highlights:

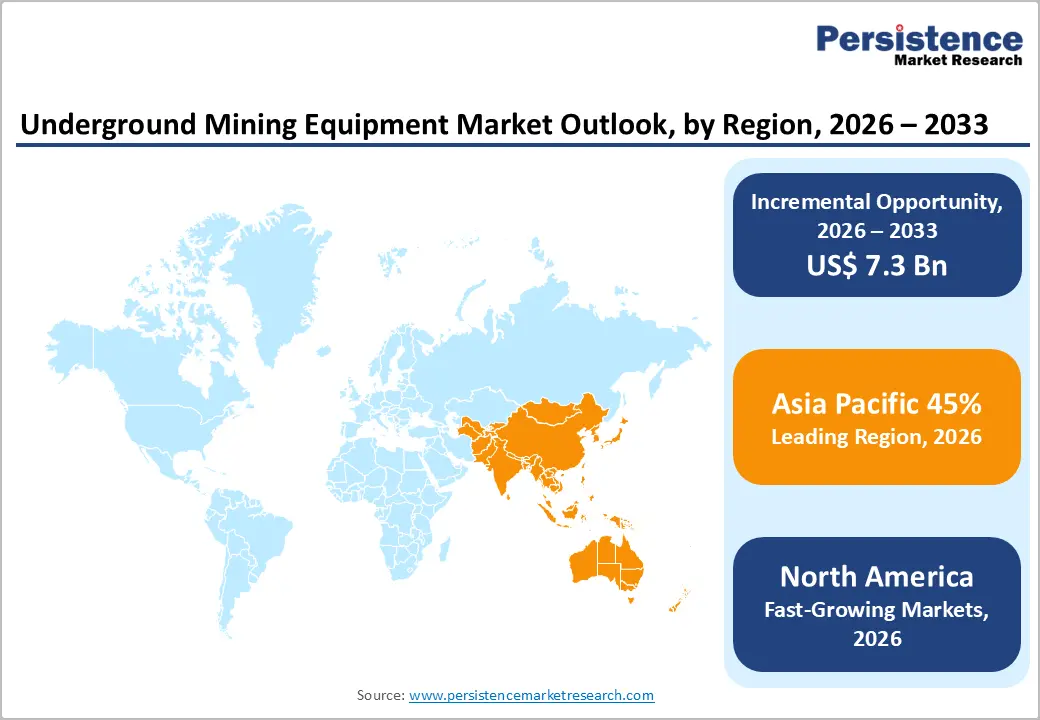

- Dominant Region: Asia Pacific leads the underground mining equipment market with an approximately 45% share, supported by its 62.3% share of global mining output and large-scale underground coal and metal extraction across China, India, and Australia.

- Metal Mining Leading Segment: Metal mining accounts for nearly 38% of total market share, driven by sustained underground extraction of copper, gold, nickel, cobalt, and other energy-transition metals.

- Leading Equipment Type: Load-Haul-Dump (LHD) loaders and hauliers hold around 26% share, remaining the backbone of underground production cycles due to their universal deployment across mining methods and commodities.

- Fastest-Growing Equipment: Underground mining trucks are the fastest-growing equipment segment, driven by deeper mine development, longer haulage distances, and battery-electric innovations commercialised by Caterpillar Inc. and Epiroc AB.

- Electrification & Automation Transformation: Battery-electric and autonomous platforms are transitioning from pilot stages to mainstream procurement, with integrated digital solutions increasingly bundled by OEMs such as Sandvik AB to enhance productivity and reduce underground emissions.

- Fast-Growing Region: North America captures roughly 20% market share, strengthened by critical mineral funding programs and streamlined permitting frameworks, accelerating underground mine development in the United States and Canada.

| Key Insights | Details |

|---|---|

| Underground Mining Equipment Market Size (2026E) | US$ 18.4 Bn |

| Market Value Forecast (2033F) | US$ 25.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Drivers - Electrification and Automation Technologies Transforming Underground Fleet Procurement

The accelerating transition toward battery-electric vehicles and autonomous systems represents a technological inflexion point for the underground mining equipment market, fundamentally altering procurement priorities and capital expenditure patterns. Electrification is advancing more quickly in underground operations than in open-pit environments, driven by the dual imperative of reducing diesel particulate emissions in enclosed spaces and meeting corporate sustainability commitments.

Caterpillar Inc. successfully demonstrated its first battery-electric prototype underground mining truck at its Tasmania proving ground in collaboration with Newmont Corporation, advancing a complete, fully electric load-and-haul solution. Epiroc AB secured an order worth approximately MSEK 350 from Eurasian Resources Group for battery-electric and automation-ready loaders, trucks, and drill rigs equipped with collision-avoidance systems for a chromium mine expansion in Kazakhstan.

These developments illustrate that electrified and tele-remote equipment is transitioning from pilot programs to mainstream procurement cycles, directly stimulating demand for next-generation underground equipment globally.

Global Mineral Demand Driving Mechanisation and Fleet Expansion

As surface-level ore deposits become progressively depleted, mining operators are extending operations deeper underground, necessitating high-capacity, technologically advanced equipment capable of functioning in confined and hazardous environments. This structural shift is one of the most decisive drivers of demand for the underground mining equipment market.

World mining production reached 19.2 billion metric tons in 2023, compared to 11.3 billion metric tons in 2000, a nearly 70 percent volumetric expansion over two decades, driven by rapid urbanization, infrastructure construction, and intensifying demand for energy-transition metals such as copper, lithium, nickel, and cobalt.

Asia alone accounts for 62.3 percent of global mining output, followed by North America at 15.5 percent and Oceania at 6.3 percent. The broad-based scale of extraction activity across multiple geographies and commodity types creates parallel demand streams for drilling equipment, loaders, haulage systems, and ventilation units, reinforcing a stable, multi-decade procurement outlook.

Government Policy Frameworks and Critical Minerals Programs Catalyzing Investment

National policy frameworks targeting domestic mineral security and underground coal extraction are creating powerful demand tailwinds for equipment suppliers in the underground mining equipment market. India's Ministry of Coal introduced a landmark incentive package that reduced the floor revenue share for underground coal mines from 4% to 2% and completely waived upfront payment requirements for underground mining ventures with an existing 50% rebate on performance security for underground coal blocks, further lowering entry barriers. In the United States, the Department of Defence executed a US$400 million equity investment in domestic rare-earth projects, while the Department of Energy announced nearly US$1 billion in funding opportunities across critical mineral supply chains.

The U.S. Geological Survey simultaneously updated its 2025 Critical Minerals List, expanding the strategic scope of domestic extraction. These coordinated government interventions are accelerating mine development timelines, expanding underground exploration, and directly stimulating procurement of underground mining equipment across key mineral-producing nations.

Restraint - High Capital Expenditure and Complex Underground Infrastructure Requirements

Underground mining operations demand substantially higher capital investment than open-pit alternatives, primarily due to the need for specialised shaft infrastructure, ventilation systems, and safety architecture. For operators transitioning to battery-electric and autonomous equipment, the requirement to retrofit underground electrical charging infrastructure adds high upfront costs.

Research from the Perenti Group highlights that underground electrification studies must comprehensively account for the technical requirements of shaft hoisting integration, power distribution networks, and mine-wide charging systems, which can substantially elevate total project costs and lengthen return-on-investment timelines, particularly for mid-tier operators with constrained capital budgets. Metso Outotec specifically engineered its SUPERIOR MKIII 6275UG crusher to reduce CAPEX by up to 20 percent by addressing underground space constraints, acknowledging cost complexity as a defining operational challenge.

Opportunity - Autonomous and Digitally Integrated Equipment Platforms Redefining Competitive Advantage

The convergence of robotics, sensor networks, artificial intelligence, and real-time data analytics is creating a transformative opportunity for manufacturers in the underground mining equipment market who can deliver fully integrated autonomous mining solutions. Automation technologies are no longer experimental; they are being adopted to address structural challenges, including ore depletion at greater depths, labour shortages in remote mining regions, and the demand for continuous production processes in hazardous environments.

Hitachi Construction Machinery launched the LANDCROS Connect Insight digital platform to deliver near real-time operational data analytics across global mining sites, directly supporting productivity, cost reduction, and sustainability goals. Sandvik AB secured an order worth approximately SEK 430 million from La Cantera Desarrollos Mineros in Mexico, covering underground loaders, drill rigs, and rock bolters, along with integrated digital solutions and aftermarket services, demonstrating that bundled digital-physical equipment solutions are becoming a primary competitive differentiator.

The global underground mining automation segment is projected to expand through 2035, according to industry analysis, confirming robust structural demand for automation-ready platforms. Equipment manufacturers who develop open, interoperable digital ecosystems will capture significant long-term value in this evolving competitive landscape.

Strategic Expansion in Emerging Markets Supported by State-Backed Mining Programs

Emerging economies represent a compelling and largely underpenetrated growth frontier for participants in the underground mining equipment market, particularly across South and Southeast Asia, Latin America, and Africa, where large undeveloped mineral reserves are increasingly being brought into production under government-backed development mandates.

India is a structurally important market, where the Ministry of Coal's incentive package, including a floor revenue share reduction and a full waiver of upfront payments, is designed to accelerate private-sector participation in underground coal mining while promoting advanced mechanisation technologies, including continuous miners, longwall systems, and AI-based safety mechanisms.

The government has explicitly targeted the adoption of remote sensing tools and specialised equipment tailored to India's geological conditions. In Latin America, Sandvik AB's SEK 430 million equipment order in Mexico, covering loaders, drill rigs, and rock bolters, with deliveries extending through 2028, reflects deepening commercial engagement with the region's expanding underground mining programs. These policies and commercial developments together establish a coherent demand pathway across multiple emerging markets for the forecast period.

Category-wise Analysis

Equipment Type Insights

Load-Haul-Dump (LHD) loaders and hauliers are dominant, accounting for approximately 26% of the total share. Their primacy is rooted in the indispensable role that load-and-haul operations play in underground production cycles connecting the extraction face directly to ore passes and haulage drives with minimal operational interruption. LHD loaders are deployed across virtually every underground mining commodity and methodology, from hard rock metal mining to coal development headings, making them the highest-volume equipment category by procurement value. Advanced automation features, including tele-remote control, collision avoidance, and autonomous cycle operation, are driving demand for fleet replacement beyond standard maintenance cycles.

Komatsu Ltd. demonstrated this segment's technological evolution at MINExpo INTERNATIONAL 2024 in Las Vegas, where it showcased the WX04B 4-tonne battery-powered LHD featuring a ground-level battery swap system and a 150kW charger designed to minimise underground infrastructure needs, alongside the rebranded WX15 LHD following its acquisition of GHH Group GmbH.

Underground mining trucks represent the fastest-growing sub-segment, fueled by escalating haulage distances in deeper mines, the adoption of battery-electric drivetrain options demonstrated by Caterpillar Inc. in collaboration with Newmont Corporation, and strong OEM order pipelines from major mining contractors

Mining Type Insights

Metal Mining holds the dominant position in the mining type category, accounting for approximately 38% of the underground mining equipment share in 2026. This leadership reflects the critical economic and strategic importance of metals, including copper, gold, nickel, cobalt, zinc, and chromite, whose extraction is overwhelmingly conducted through underground methods as surface orebodies are exhausted. The accelerating global energy transition has intensified demand for battery metals, directly driving mine development and equipment procurement in underground hard-rock environments. In Kazakhstan, Epiroc AB secured an approximately MSEK 350 order for the ShDNK-2 chromium mine expansion, including battery-electric loaders, trucks, and drill rigs with collision avoidance systems, illustrating active capital investment in underground metal mining infrastructure.

Coal mining is the fastest-growing segment within the mining type category, propelled by strong energy demand across Asia and targeted government policy interventions. India's Ministry of Coal formally introduced a comprehensive incentive structure for underground coal operations, including halving the floor revenue share to 2 percent and waiving upfront payment requirements, aimed at driving private-sector investment and mechanisation. Epiroc AB's order from Hindustan Zinc Limited for underground mine trucks and face drilling rigs in Rajasthan, supported by a 6 to 8-year service contract, further underscores active capital deployment in South Asian underground mining programs.

Regional Insights and Trends

Asia Pacific Underground Mining Equipment Market Trends

Asia Pacific commands the largest share of the global underground mining equipment market, representing approximately 45% of total demand, anchored by China's dominant position as the world's largest coal and mineral producer. Asia accounts for 62.3 percent of global mining production by volume as of 2023, a regional concentration that directly translates into the highest equipment procurement volumes of any geography. China's coal-heavy energy mix and extensive underground metal mining operations, particularly in copper, zinc, and iron ore, sustain a large, recurring capital equipment replacement cycle.

India is the fastest-growing sub-market within the region. Epiroc AB secured an approximately MSEK 280 order from Hindustan Zinc Limited for underground mine trucks and drilling rigs in Rajasthan, with a 6- to 8-year aftermarket contract, confirming active mine expansion and fleet deployment. India's Ministry of Coal has formally waived upfront payment requirements and reduced revenue-share obligations for underground coal mining operators, thereby directly stimulating equipment procurement under the Defence Acquisition Procedure 2020 indigenisation framework. Australia remains a high-value market, as evidenced by Sandvik AB's SEK 420 million equipment order for Evolution Mining's Cowal Gold Operations, covering underground trucks, loaders, and drill rigs to be delivered from mid-2026 through 2027.

North America Underground Mining Equipment Market Trends

North America holds approximately 20% of the global underground mining equipment market, driven by the United States' aggressive critical minerals policy agenda and Canada's large-scale underground metal mining sector. The U.S. Department of Energy announced nearly US$ 1 billion in funding opportunities for critical mineral supply chains, including US$ 500 million for processing and battery manufacturing and US$ 135 million for rare earth supply chain enhancement. The U.S. Geological Survey's updated 2025 Critical Minerals List expanded the strategic designation of domestically extractable resources, accelerating mine permitting and equipment procurement across copper, lithium, and rare earth programs.

Technologically, North America is at the vanguard of battery-electric and autonomous underground equipment adoption. Caterpillar Inc. unveiled its first battery-electric underground mining truck prototype developed in collaboration with Newmont Corporation at its Tasmania proving ground, with the system designed to pair with the R1700 XE battery-electric loader to deliver a fully autonomous, zero-carbon load-and-haul circuit. The Trump administration's "Unleashing American Energy" executive order, effective in January 2025, streamlined permitting timelines for domestic mining projects, creating a policy tailwind expected to accelerate underground mine development and equipment deployment across the U.S. and Canada.

Europe Underground Mining Equipment Market Trends

Europe accounts for approximately 18% of the global underground mining equipment market, supported by a long-established mining tradition and active mine modernisation programs across Germany, Sweden, Poland, and Finland. The EU mining and quarrying sector employed approximately 371,000 people across around 17,000 enterprises in 2022, generating €173.6 billion in net turnover, a 70 percent year-on-year increase driven by post-pandemic commodity demand and geopolitical supply disruptions. Although turnover was corrected to approximately €126.5 billion in 2023, sectoral activity remains substantially above pre-2021 levels, sustaining equipment procurement.

Metal ore mining contributed 9.6 percent of total EU sectoral turnover, with Poland specialising in coal and lignite extraction and Bulgaria concentrated in metal ore mining, both representing active equipment procurement markets. European operators are accelerating the adoption of battery-electric loaders and low-ventilation underground fleets in compliance with EU Green Deal environmental mandates and product sustainability regulations.

Competitive Landscape

The global underground mining equipment market is largely oligopolistic, dominated by a few global heavy equipment giants that hold significant market share due to their extensive product portfolios and strong service networks. Leading players such as Sandvik AB, Epiroc AB, Caterpillar Inc., Komatsu Ltd., Atlas Copco, and Mindrill offer comprehensive solutions, including LHDs, drill rigs, bolters, and ventilation systems, often integrating advanced automation and battery-electric technologies to improve productivity and safety.

Players like Liebherr Group, SANY Group, and Boart Longyear compete in specialised segments or regional markets, focusing on drilling attachments, consumables, and support equipment. The market is highly technology-driven, with top companies investing heavily in digital solutions, tele-remote operations, and fleet management systems. Barriers to entry are high due to capital intensity, technical expertise, and the need for reliable after-sales support, which consolidates the power of leading OEMs. Emerging players from Asia Pacific and Latin America add localised competition, but the established global brands continue to dominate.

Key Developments

- In January 2026, Sandvik AB secured a major underground mining equipment order worth approximately SEK 420 million from The Redpath Group for deployment at Evolution Mining’s Cowal Gold Operations in Australia. The contract includes underground trucks, loaders, and drill rigs, with deliveries scheduled from mid-2026 through 2027. In addition to equipment supply, Sandvik will provide digital solutions, rock tools, consumables, and aftermarket services, strengthening its position in integrated underground mining solutions.

- In April 2025, Epiroc AB secured a major underground mining equipment order valued at approximately MSEK 280 from Hindustan Zinc Limited for its mining operations in Rajasthan, India. Booked in Q1 2025, the order includes underground mine trucks and face and production drilling rigs, supported by a 6-8-year service and maintenance contract, with deliveries scheduled from Q3 to end-2025. This development underscores rising demand for automation-ready underground equipment and long-term aftermarket support in the global underground equipment market.

Companies Covered in Underground Mining Equipment Market

- Sandvik AB

- Epiroc AB

- Atlas Copco

- Mindrill

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery

- Liebherr Group

- SANY Group

- Terex Corporation

- Metso Corporation

- Schmidt, Kranz & Co

- Smt Scharf

- Boart Longyear

- XCMG Group

- Schmidt

Frequently Asked Questions

The global Underground Mining Equipment Market is projected to be valued at US$ 18.4 Bn in 2026.

The Load-Haul-Dump (LHD) Loaders & Haulers segment is expected to account for approximately 26% of the Global Underground Mining Equipment Market by Equipment type in 2026.

The market is expected to witness a CAGR of 4.9% from 2026 to 2033.

The Underground Mining Equipment Market growth is driven by rapid electrification and automation of underground fleets led by innovations from Caterpillar Inc. and Epiroc AB, rising global mineral production reaching 19.2 billion metric tons with Asia contributing 62.3% of output, deeper ore extraction requiring advanced mechanised equipment, and strong government-backed critical mineral and underground coal incentive programs in India and the United States that are accelerating mine development and capital equipment procurement.

Key market opportunities in the Underground Mining Equipment Market lie in the expansion of fully autonomous and digitally integrated equipment platforms leveraging AI, real-time analytics, and robotics commercialized by companies such as Hitachi Construction Machinery and Sandvik AB, along with strategic growth in emerging markets across Asia and Latin America where state-backed mining incentives and large undeveloped reserves are accelerating underground mechanisation and long-term equipment procurement.

Key players in the Underground Mining Equipment Market include Sandvik AB, Epiroc AB, Caterpillar Inc., Komatsu Ltd., Atlas Copco, and Mindrill.