- Hardware & Software IT Services

- Thermal Inkjet Printheads Market

Thermal Inkjet Printheads Market Size, Share, and Growth Forecast, 2026 - 2033

Thermal Inkjet Printheads Market by Ink Type (Aqueous-Based, UV-Curable, Others), Resolution (601-1200 dpi, ≥1201 dpi, Others), Application, End-user Industry, and Regional Analysis for 2026 - 2033

Thermal Inkjet Printheads Market Size and Trends Analysis

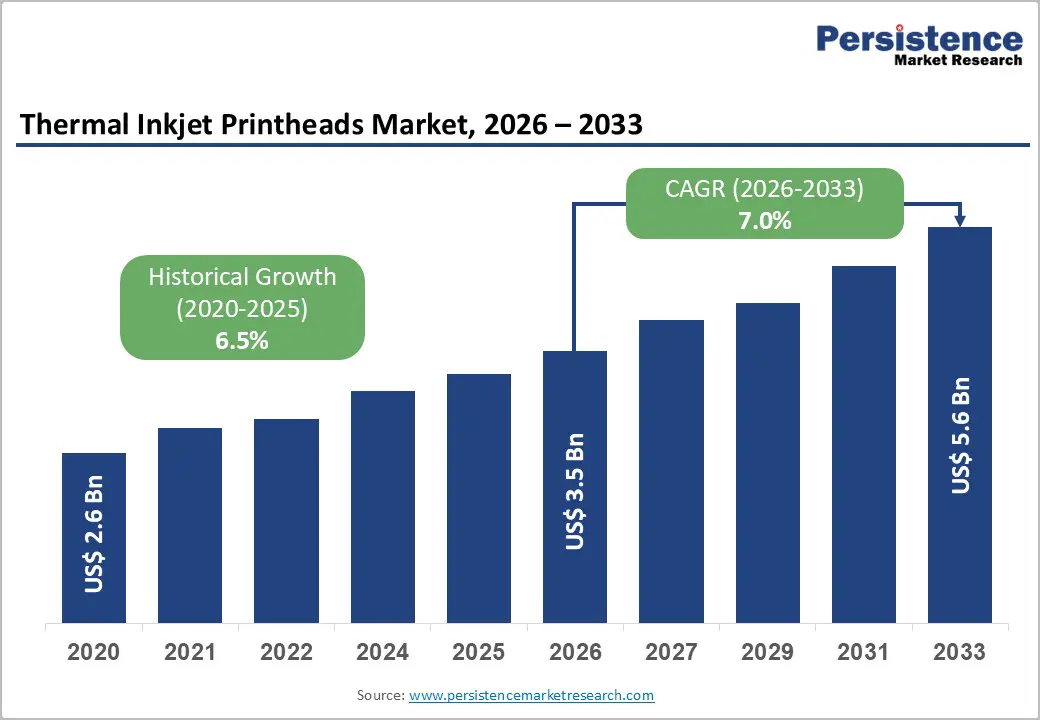

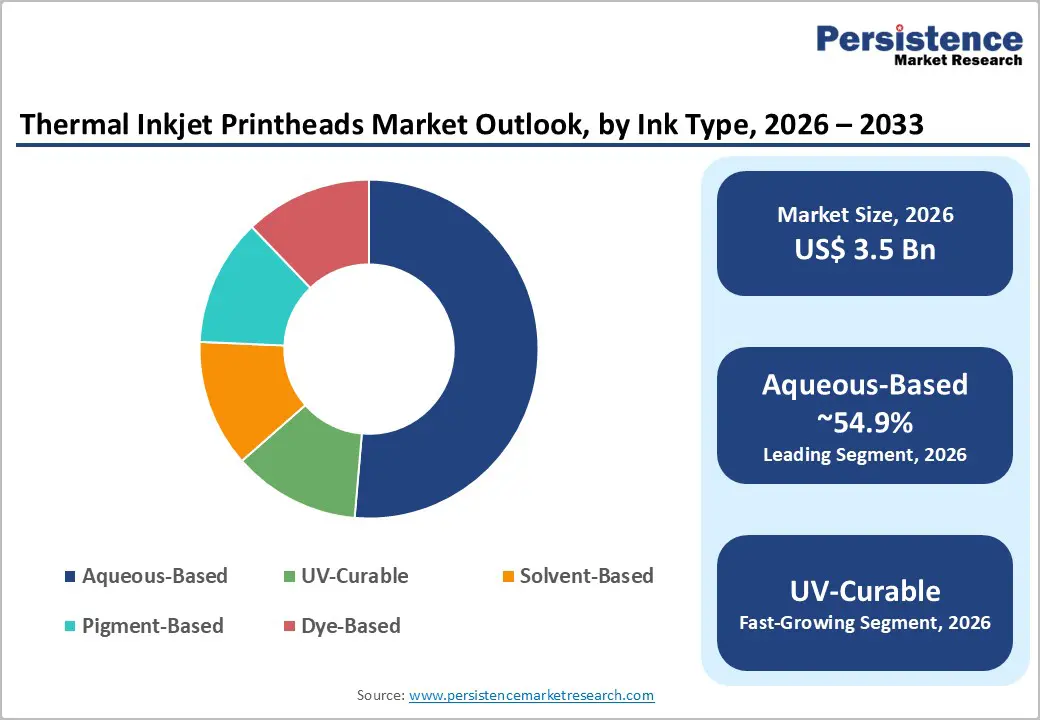

The global thermal inkjet printheads market size is likely to be valued at US$ 3.5 billion in 2026 and is expected to reach US$5.6 billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033, driven by the rising adoption of digital printing technologies in packaging, labeling, and industrial coding applications.

Expansion of e-commerce supply chains and stricter product traceability regulations are increasing demand for high-resolution variable data printing. Improvements in thermal printhead durability, ink compatibility, and modular single-pass printing architectures are further expanding industrial applications. As packaging manufacturers increasingly adopt automated digital printing systems, thermal inkjet printheads are becoming a core component in modern production lines.

Key Industry Highlights:

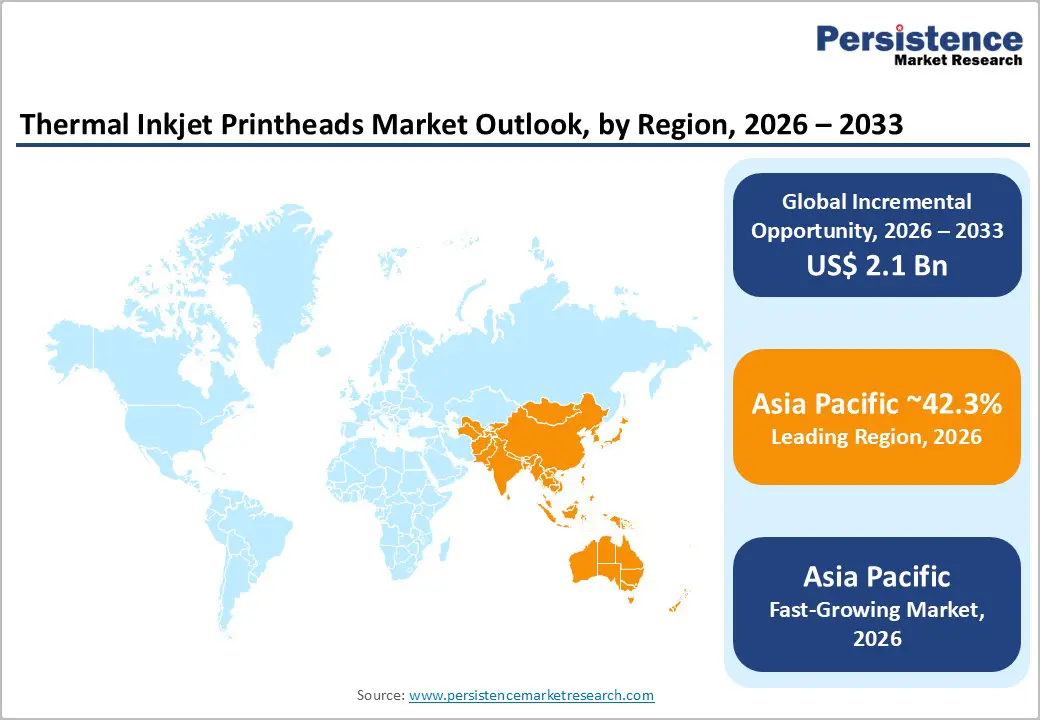

- Leading Region: Asia Pacific is projected to lead the market with a 42.3% market share, supported by strong manufacturing capacity in China, Japan, and Southeast Asia, along with large-scale packaging and consumer goods production that requires high-volume digital printing solutions.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing regional market, driven by the rapid expansion of e-commerce logistics networks, increasing packaging automation, and continued investment in industrial digital printing technologies across China, India, Vietnam, and Indonesia.

- Investment Plans: Printing technology companies, including HP Inc., Canon Inc., and Domino Printing Sciences, are expanding research and development investments in advanced printhead architecture, UV-curable ink compatibility, and high-resolution printing systems to support evolving industrial packaging and labeling applications.

- Dominant Ink Type: Aqueous-based inks are anticipated to dominate the ink type segment with a 54.9% market share, widely used in packaging labels, coding and marking, and commercial graphic printing due to strong compatibility with thermal inkjet technology and lower volatile organic compound emissions.

- Leading Resolution: The 601-1200 dpi resolution is estimated to lead the market with a 40.9% share, offering an optimal balance between print clarity and operational speed, which is critical for industrial packaging, barcode printing, and logistics labeling applications.

| Key Insights | Details |

|---|---|

| Thermal Inkjet Printheads Market Size (2026E) | US$3.5 Bn |

| Market Value Forecast (2033F) | US$5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Digital Packaging and Traceability Requirements

Digital transformation across packaging and labeling operations is a major growth driver for thermal inkjet printheads. Consumer goods manufacturers are increasingly adopting digital printing to support variable data printing, serialization, and product traceability. Food safety regulations and pharmaceutical compliance standards require clear coding for batch numbers, expiration dates, and anti-counterfeiting measures. Thermal inkjet printheads are widely used in coding and marking systems due to their cost efficiency, high print resolution, and integration flexibility. The rapid growth of global e-commerce logistics has intensified demand for dynamic labeling and barcode printing. Packaging lines now require printing technologies capable of producing unique codes and short-run designs at high speed. Thermal inkjet printheads meet these requirements while maintaining low maintenance costs and easy integration into automated packaging systems. As supply chains increasingly rely on real-time tracking and digital identifiers, adoption of TIJ technology continues to expand across logistics and consumer goods manufacturing.

Technological Advancements in Printhead Design and Ink Chemistry

Advancements in thermal printhead engineering have significantly improved reliability, droplet precision, and operating lifespan. Modern nozzle architectures use advanced microfabrication techniques that enhance drop placement accuracy and improve thermal efficiency. These improvements allow printheads to operate at higher speeds while maintaining consistent image quality. Ink chemistry innovation has also expanded the application range of thermal inkjet technology. Improved pigment formulations and enhanced aqueous ink systems allow printing on a wider range of substrates, including coated packaging films, plastics, and specialty papers. Development of compatible UV-curable inks further enables durable printing for industrial packaging and decorative applications. As printhead manufacturers continue to improve thermal control systems and nozzle density, the technology is becoming increasingly competitive with piezoelectric alternatives in industrial digital printing environments.

Growth of Short-Run and Customized Printing

Demand for short-run printing and customized product packaging is increasing across multiple industries. Brand owners are adopting limited-edition packaging, regional marketing campaigns, and personalized product labeling to enhance customer engagement. Traditional printing technologies struggle to accommodate these requirements due to high setup costs and long production cycles. Thermal inkjet printheads offer flexible digital printing capabilities that allow manufacturers to rapidly switch designs without costly plate changes. This flexibility enables efficient production of smaller batches while maintaining consistent print quality. Packaging converters and commercial printing providers are therefore integrating TIJ modules into digital presses and inline printing systems to support these evolving production requirements.

Barrier Analysis - Operational Limitations Compared with Piezoelectric Printheads

Thermal inkjet technology faces competition from piezoelectric printhead systems, which are often preferred for high-volume industrial printing applications. Piezoelectric heads typically offer longer operational lifespans and broader compatibility with high-viscosity inks. In continuous heavy-duty printing environments, thermal printheads may require more frequent replacement or maintenance. These lifecycle considerations can influence purchasing decisions among large industrial printers that prioritize durability and operational efficiency. As a result, some high-precision printing segments continue to favor alternative technologies.

Compatibility Constraints for Certain Industrial Ink Types

Thermal inkjet printheads rely on controlled heating mechanisms to eject droplets, which limits compatibility with certain solvent-based or high-viscosity ink formulations. Applications involving specialized coatings, conductive materials, or ceramics may require ink chemistries that exceed the thermal tolerance of standard TIJ systems. These technical limitations restrict adoption in certain niche industrial markets. Expanding compatibility through joint development between printhead manufacturers and ink formulators remains an ongoing challenge for the industry.

Opportunity Analysis - Integration of Single-Pass Printing Architectures

Single-pass printing systems represent a significant opportunity for thermal inkjet printhead manufacturers. These systems use wide printhead arrays to complete printing in a single pass rather than multiple scanning cycles. The approach dramatically increases printing speed while maintaining high resolution. Packaging converters and industrial printers are increasingly investing in single-pass digital presses to improve throughput and production efficiency. As thermal inkjet modules become wider and more reliable, they are being integrated into next-generation packaging and label printing systems. This shift toward high-speed digital printing infrastructure creates strong demand for advanced TIJ printhead arrays.

Growth of Aftermarket and Service-Based Revenue Models

Thermal inkjet printheads function as replaceable components within printing systems, creating recurring demand for replacement units and maintenance services. Companies that provide predictive maintenance, technical support, and subscription-based replacement programs can capture long-term revenue streams. Industrial customers increasingly prefer service contracts that guarantee operational uptime and technical support. Vendors that integrate remote monitoring and diagnostic tools into their printing systems can offer proactive maintenance services, improving reliability while strengthening customer relationships.

Expansion of Digital Printing in Emerging Markets

Emerging economies are experiencing rapid industrialization and growing demand for modern packaging solutions. Manufacturers in Asia, Latin America, and parts of the Middle East are investing in automated packaging equipment to meet international export standards. Digital printing technologies, including thermal inkjet systems, allow these manufacturers to upgrade production capabilities without the capital expenditure required for large conventional presses. As a result, adoption of TIJ printheads in emerging markets is expected to increase steadily over the forecast period.

Category-wise Analysis

Ink Type Insights

Aqueous-based inks are anticipated to account for 54.9% market share in the thermal inkjet printheads market, making them the dominant ink chemistry used with thermal ejection technologies. Their formulation, primarily water combined with dyes or pigments, provides optimal viscosity and surface tension properties that enable stable droplet formation during heating cycles. This compatibility reduces nozzle clogging risk and ensures consistent print performance across high-volume industrial printing systems. These inks are widely used in packaging labels, coding and marking, and commercial graphic printing, particularly in porous substrates such as paperboard, corrugated packaging, and label stock. For example, industrial packaging printers from companies such as HP Inc. and Domino Printing Sciences frequently rely on aqueous-based ink systems for high-speed carton coding and product labeling applications. Environmental compliance further strengthens adoption because aqueous inks typically contain lower levels of volatile organic compounds (VOCs) compared with solvent formulations. The combination of cost efficiency, substrate compatibility, and regulatory alignment supports the continued leadership of aqueous-based ink systems within the thermal inkjet ecosystem.

UV-curable inks are anticipated to expand at the fastest rate during the forecast period. These inks cure instantly when exposed to ultraviolet light, eliminating drying time and enabling faster production throughput in digital printing environments. Their rapid polymerization also creates highly durable prints with strong adhesion and abrasion resistance. Manufacturers are increasingly adopting UV-curable inks for flexible packaging, plastic films, industrial labels, and rigid substrates where conventional aqueous inks struggle to adhere. Industrial printers produced by companies such as Xaar plc and Fujifilm Holdings Corporation support UV-curable ink systems for decorative packaging and industrial marking applications. The ability of UV inks to deliver high color density, chemical resistance, and scratch durability makes them particularly suitable for premium packaging and product branding. As printhead manufacturers continue improving nozzle coatings and ink compatibility, UV-curable systems are expected to gain wider adoption across industrial printing workflows.

Resolution Insights

The 601-1200 dpi resolution segment is anticipated to hold 40.9% share of the thermal inkjet printheads market, making it the leading resolution category used in industrial digital printing systems. This resolution range delivers a practical balance between print quality and operational speed, which is essential for high-throughput manufacturing environments. Printheads operating within this range provide sufficient clarity for barcodes, QR codes, product information text, and packaging graphics while maintaining reliable performance on automated production lines. Most packaging and coding applications require machine-readable barcodes and clear text output rather than ultra-high image resolution, which explains the widespread adoption of 600-1200 dpi printheads. For example, industrial coding systems from companies such as Videojet Technologies and Markem-Imaje commonly operate in this resolution range for carton labeling and pharmaceutical packaging serialization. The ability to combine readable graphics with high printing speeds makes this resolution segment particularly attractive for large-scale packaging, logistics, labeling, and product traceability applications.

The ≥1201 dpi resolution segment is anticipated to grow at the fastest rate, registering a CAGR of 6.81% as demand for high-definition digital printing increases across premium product packaging and design-oriented applications. Ultra-high resolution printing enables sharper graphics, improved gradient transitions, and more precise color reproduction, which are essential for brand-focused packaging and marketing materials. Advancements in micro-nozzle architecture, droplet control electronics, and ink chemistry are allowing thermal inkjet printheads to achieve extremely fine droplet placement at higher resolutions. Companies such as Canon Inc. and HP Inc. have developed high-density printhead arrays capable of delivering high-resolution output for digital presses and specialty printing systems. Demand is particularly increasing in luxury packaging, decorative printing, and high-end graphic applications, where visual quality significantly influences consumer perception. As brand owners continue prioritizing visual differentiation and short-run customization, adoption of ≥1200 dpi thermal inkjet technologies is expected to accelerate.

Regional Insights

North America Thermal Inkjet Printheads Market Trends - E-commerce Logistics and Regulatory Labeling Driving Industrial TIJ Adoption

North America represents a technologically advanced market for thermal inkjet printheads, supported by strong adoption in industrial packaging, labeling, and commercial printing applications. The U.S. accounts for the largest share of the regional market, supported by a large base of packaging converters, digital printing equipment manufacturers, and logistics companies that rely heavily on variable data printing. Large-scale packaging production across industries such as food processing, pharmaceuticals, and consumer goods continues to generate demand for reliable coding and labeling technologies that can operate continuously on high-speed production lines.

The rapid expansion of e-commerce and omnichannel retail distribution has significantly increased the need for variable data printing on shipping cartons, product labels, and warehouse packaging. Major logistics operators such as Amazon and UPS rely on barcode labeling and real-time package identification systems that require consistent and high-resolution printing. Thermal inkjet printheads are commonly integrated into automated packaging lines used by fulfillment centers, enabling high-speed printing of product information, batch numbers, and QR codes that support inventory management and shipment tracking.

Regulatory compliance also plays a major role in driving technology adoption in North America. Agencies such as the U.S. Food and Drug Administration enforce strict labeling requirements for pharmaceuticals, food products, and medical devices. Regulations related to product traceability, serialization, and batch identification require manufacturers to print accurate and legible product information on primary and secondary packaging. Thermal inkjet printing systems are widely used in pharmaceutical packaging lines because they offer precise droplet control and high resolution, enabling manufacturers to meet serialization standards while maintaining production efficiency. Innovation also remains a defining characteristic of the North American market.

The region hosts several leading digital printing technology developers that continuously invest in printhead engineering, ink chemistry, and workflow automation. For example, HP Inc. continues to expand its Thermal Inkjet (TIJ) technology platform, supplying printheads used in industrial coding systems and commercial digital presses. Similarly, Memjet has advanced high-speed page-wide printhead technologies that support packaging and label printing applications. These research and development initiatives strengthen the regional innovation ecosystem and contribute to the ongoing performance improvement of thermal inkjet printing systems.

Europe Thermal Inkjet Printheads Market Trends - Sustainable Packaging and Digital Printing Integration Accelerating TIJ Deployment

Europe represents a mature yet technologically sophisticated market for thermal inkjet printheads, supported by strong industrial printing adoption across packaging, labeling, and graphic printing applications. Countries such as Germany, the U.K., France, and Spain play major roles in regional demand because they host large manufacturing sectors and highly developed packaging industries. Many European packaging converters are adopting digital printing systems to improve production flexibility, reduce setup time, and enable short-run packaging production for customized consumer products. Germany plays a particularly important role in the regional market due to its leadership in industrial automation and printing equipment manufacturing.

German manufacturing companies are increasingly incorporating digital printing solutions into packaging lines to support rapid product customization and improved traceability. Companies such as Koenig & Bauer AG and Heidelberger Druckmaschinen AG have invested in digital printing platforms that integrate advanced printhead technologies for industrial printing applications. These developments are encouraging packaging manufacturers to transition from traditional analog printing processes to more flexible digital production systems.

Sustainability considerations are also shaping printing technology adoption across Europe. Environmental regulations issued by institutions such as the European Commission promote the use of low-emission inks, recyclable packaging materials, and energy-efficient printing technologies. As a result, aqueous-based thermal inkjet inks have gained strong traction because they contain lower levels of volatile organic compounds compared with solvent-based alternatives. Packaging companies across the region are adopting thermal inkjet systems to align with these sustainability requirements while maintaining efficient production processes. Recent collaborations between printing technology developers and packaging companies are further accelerating innovation. Digital press technologies integrating advanced inkjet printheads are enabling faster production of labels and flexible packaging materials while minimizing material waste. These developments strengthen Europe’s position as a key innovation hub in the global digital printing industry and support continued adoption of thermal inkjet printhead technologies across industrial and commercial printing applications.

Asia Pacific Thermal Inkjet Printheads Market Trends-Manufacturing Expansion and E-commerce Growth Boosting High-Volume TIJ Demand

Asia Pacific represents the largest and fastest-growing regional market for thermal inkjet printheads, accounting for 42.3% of the market share. Rapid industrialization, expanding packaging manufacturing capacity, and the rapid growth of e-commerce platforms are major contributors to regional demand. China represents the largest market within the Asia Pacific region, supported by its extensive manufacturing sector and high production volumes of consumer goods. The country’s packaging industry is undergoing rapid modernization as manufacturers adopt digital printing technologies to improve operational efficiency and meet export labeling requirements.

Companies such as Han's Laser Technology Industry Group and Shanghai Yuchang Industrial are expanding digital printing equipment production to meet domestic demand for high-speed packaging printing systems. The continued expansion of e-commerce platforms such as Alibaba Group is also increasing demand for shipping labels and variable data printing, further supporting the adoption of thermal inkjet printing technologies. India is emerging as a rapidly expanding market for thermal inkjet printing technologies, driven by the growth of organized retail, pharmaceutical manufacturing, and food processing industries. The expansion of logistics networks and modern packaging facilities is increasing demand for automated coding and labeling technologies.

Companies such as Domino Printing Sciences and Videojet Technologies have expanded their presence in India to supply thermal inkjet printing solutions for packaging manufacturers and pharmaceutical companies. Government initiatives supporting domestic manufacturing are also encouraging companies to adopt advanced production technologies, including digital printing systems.

Competitive Landscape

The global thermal inkjet printheads market is characterized by a moderately consolidated competitive structure. A group of global technology companies dominates high-value industrial printing solutions, while smaller specialized suppliers provide components and aftermarket services. Leading companies maintain competitive advantages through proprietary printhead technologies, integrated ink ecosystems, and extensive research and development capabilities. Firms that combine printhead manufacturing with digital printing equipment production typically capture larger market shares due to stronger system integration capabilities and established distribution networks.

Market leaders prioritize technological innovation, integrated printing ecosystems, and global expansion strategies. Companies are investing in improved nozzle architecture, wider printhead arrays, and advanced ink compatibility. Service-based revenue models and strategic partnerships with equipment manufacturers are also becoming increasingly important competitive differentiators.

Key Industry Developments:

- In March 2025, HP Inc. introduced the next-generation HP ThermaCore thermal inkjet technology, designed for high-speed coding and marking applications. The platform offers up to 3× longer throw distance and 2× higher print swath and speed, enabling manufacturers to improve efficiency and integrate thermal inkjet systems into fast packaging lines across food, beverage, and pharmaceutical industries.

- In June 2025, Domino Printing Sciences expanded its product portfolio for the life sciences sector, highlighting Gx-Series thermal inkjet printers for coding on flexible films, cartons, and pharmaceutical packaging as part of integrated product-to-pallet traceability solutions.

Companies Covered in Thermal Inkjet Printheads Market

- HP Inc.

- Seiko Epson Corporation

- Canon Inc.

- Ricoh Company, Ltd.

- Konica Minolta, Inc.

- Kyocera Corporation

- Fujifilm Holdings Corporation

- Fujifilm Dimatix

- Xaar plc

- Domino Printing Sciences

- Toshiba Tec Corporation

- Seiko Instruments Inc.

- Brother Industries, Ltd.

- Durst Group

- Agfa-Gevaert Group

- Xerox Holdings Corporation

- Videojet Technologies

Frequently Asked Questions

The thermal inkjet printheads market is estimated to be valued at US$ 3.5 billion in 2026.

The thermal inkjet printheads market is projected to reach US$ 5.6 billion by 2033.

Key trends include the growing adoption of digital printing in packaging and labeling, increasing use of high-resolution printheads for premium graphics, expansion of UV-curable ink compatibility, and integration of thermal inkjet systems into automated smart manufacturing environments.

The aqueous-based ink segment leads the market with a 54.9% share, driven by strong compatibility with thermal inkjet technology and widespread use in packaging, labeling, and commercial graphic printing.

The thermal inkjet printheads market is projected to grow at a CAGR of 7.0% between 2026 and 2033.

Major companies with strong product portfolios include HP Inc., Seiko Epson Corporation, Canon Inc., Ricoh Company, Ltd., and Domino Printing Sciences.