- Medical Devices

- Teledentistry Market

Teledentistry Market Size, Share, and Growth Forecast 2026 - 2033

Teledentistry Market by Component (Software & Services, Hardware), by Delivery Mode (Cloud-Based Platforms, Web-Based / On-Premise Platforms), by Application (Tele-Consultation, Remote Patient Monitoring, Education & Training), and Regional Analysis, 2026 - 2033

Teledentistry Market Share and Trends Analysis

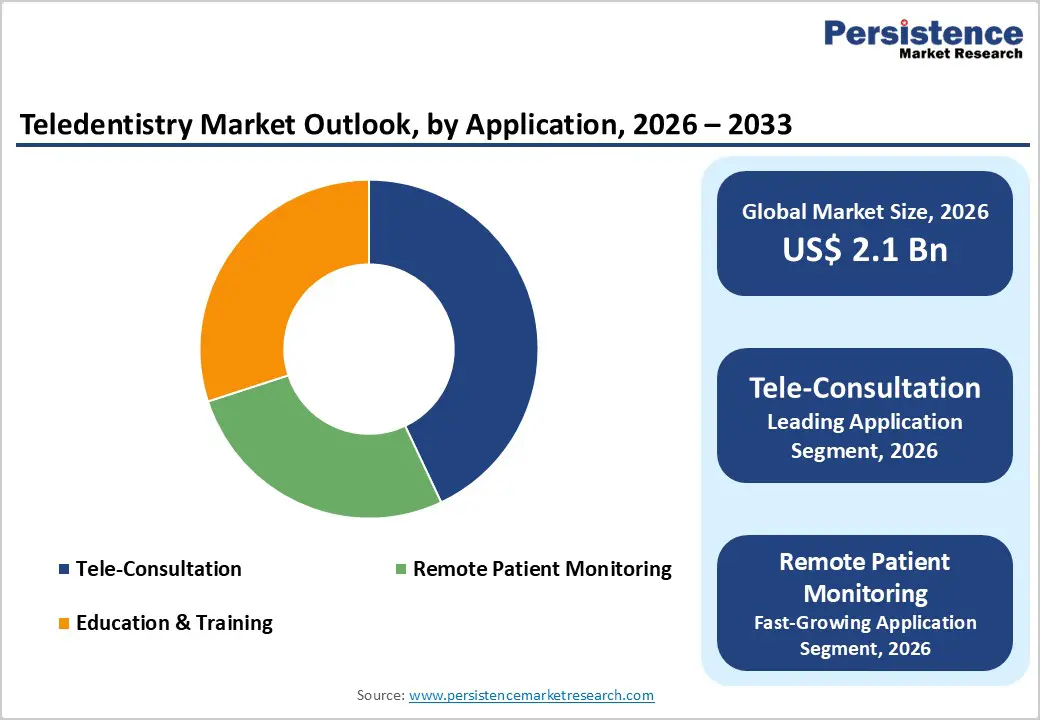

The global teledentistry market size is expected to be valued at US$ 2.1 billion in 2026 and projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

This robust growth reflects accelerating digital transformation in dental care, sustained post-pandemic adoption of virtual consultation models, and supportive telehealth policy frameworks across major markets. Rising awareness of oral health disparities, combined with the need to extend dental services to rural and underserved communities, is encouraging payers, providers, and regulators to normalize teledentistry as a core access channel. The American Dental Association (ADA) recognizes teledentistry as an effective tool to expand the reach of the dental home, while studies published on PubMed Central (PMC) show that virtual dental consultations significantly improve access, triage efficiency, and continuity of care, especially during public health emergencies such as COVID-19.

Key Industry Highlights:

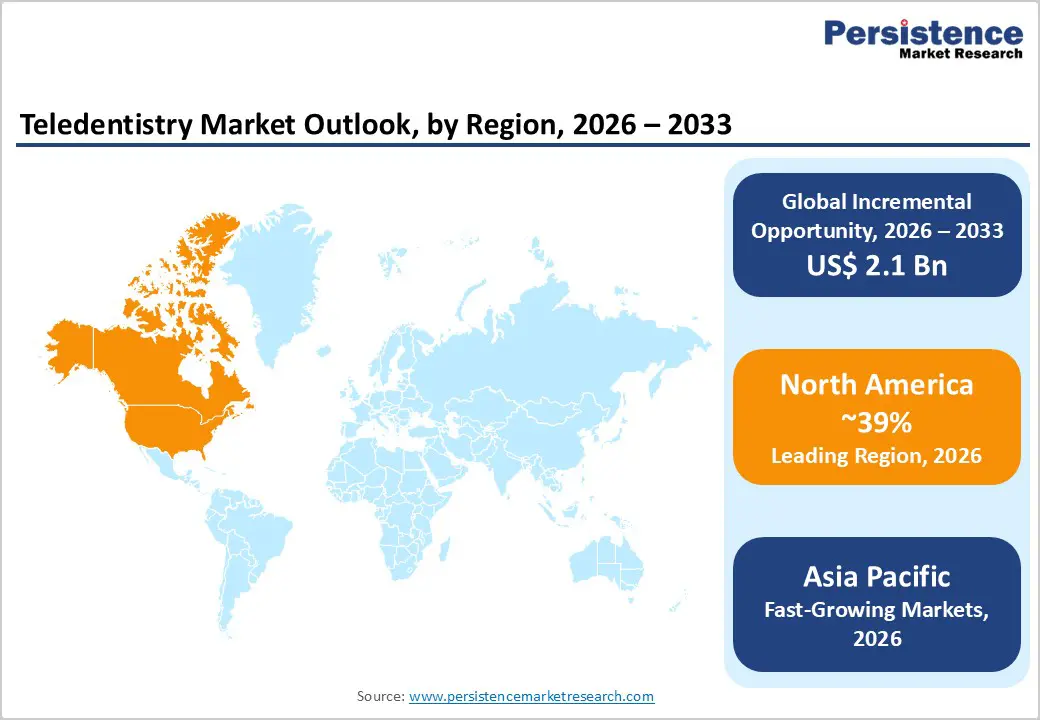

- North America remains the leading teledentistry region, holding about 39% share in 2025, supported by mature telehealth infrastructure, strong professional backing from organizations like the ADA, robust payer reimbursement for virtual dental codes in many states, and high penetration of digital tools among dental service organizations and private practices.

- The Asia Pacific region is the fastest-growing teledentistry market, driven by rapid smartphone adoption, government telemedicine initiatives in China, India, and ASEAN, and emerging synchronous consultation platforms that extend specialist dental care to underserved communities, underpinning double-digit CAGR prospects through 2033.

- By component, software & services account as the dominant segment with an estimated 72% share in 2025, as cloud-based platforms, practice portals, and patient apps from vendors like MouthWatch LLC, Dentulu Inc., and Teledentix underpin virtually all tele-consultation and remote monitoring workflows in the teledentistry ecosystem.

- Within applications, remote patient monitoring is the fastest-growing segment, fueled by orthodontic and aligner programs using tools such as Invisalign® Virtual Care from Align Technology, Inc. and similar solutions, enabling frequent assessment of treatment progress via patient submitted images and reducing in-office visit burden for both providers and patients.

- A key market opportunity centers on integrating teledentistry into broader digital health and value-based care strategies, where virtual consultations, remote monitoring, and education & training can help payers and health systems improve oral health outcomes, reduce emergency visits, and manage high-risk populations more efficiently using data-driven, preventive care pathways.

| Key Insights | Details |

|---|---|

| Teledentistry Market Size (2026E) | US$ 2.1 billion |

| Market Value Forecast (2033F) | US$ 4.2 billion |

| Projected Growth CAGR (2026 - 2033) | 10.3% |

| Historical Market Growth (2020 - 2025) | 8.6% |

Market Dynamics

Drivers - Expansion of Telehealth Frameworks and Pandemic-Driven Digital Adoption

The rapid expansion of telehealth frameworks and the experience of the COVID-19 pandemic have been pivotal in accelerating teledentistry adoption worldwide. During lockdowns, many dental clinics suspended routine care and relied on teledentistry for triage, remote consultation, and follow-up, using synchronous and asynchronous modalities through secure platforms or widely used tools such as video applications.

A scoping review published on PMC found that teledentistry reduced in-person visits, supported emergency triage, and enabled continuity of non-procedural care when face-to-face services were restricted. The ADA has formalized policy supporting teledentistry as a means to expand the dental home, emphasizing that virtual services should meet the same standard of care and be reimbursed equivalently when clinically appropriate. As many payers and health systems have kept telehealth reimbursement provisions beyond the acute pandemic phase, dental practices increasingly integrate teledentistry into routine workflows for pre-visit screening, post-operative review, orthodontic monitoring, and urgent care triage, structurally lifting long-term demand for teledentistry platforms and services.

Need to Address Oral Health Inequities and Rural Access Gaps

Growing recognition of oral health inequities is also driving teledentistry market growth. The World Health Organization (WHO) notes that oral diseases affect over 3.5 billion people globally, with underserved and rural communities facing disproportionate barriers to care. Teledentistry offers a scalable way to extend specialist expertise to remote locations through hub-and-spoke models linking centralized dentists with community clinics, hygienists, or mobile units. Research on teledentistry implementation indicates that virtual dental services improve access in areas lacking dentists and help optimize limited chairtime by pre-assessing cases remotely. In the United States, analyses of claims data showed that more than 78,000 teledentistry encounters in one study period relied on synchronous audio or video, indicating meaningful uptake among Medicaid and safety-net populations. Policymakers and professional bodies such as the American Academy of Pediatric Dentistry (AAPD) have issued checklists and guidance to safely use teledentistry for pediatric populations, further legitimizing remote models. As governments and payers seek cost-effective strategies to close access gaps without proportionally increasing physical infrastructure, teledentistry platforms are positioned as critical enablers, strengthening the long-term demand outlook.

Restraints - Regulatory Fragmentation and Reimbursement Uncertainty

Despite progress, regulatory fragmentation and reimbursement uncertainty remain key barriers to teledentistry expansion. In the U.S., a compilation by the American Dental Education Association (ADEA) shows wide variation among states in teledentistry laws, Medicaid policies, and dental board directives, ranging from explicit statutes to limited guidance or pilot-focused rules. Requirements around licensing (dentist must be licensed in the patient’s state), supervision models, allowable modalities, and HIPAA-compliant technology can be complex, especially for multi-state dental service organizations. While the ADA advocates parity in reimbursement for clinically equivalent virtual services, payer policies still differ significantly, with some plans restricting codes or reimbursing at lower rates. This variability increases administrative burden for providers and technology vendors, slows adoption in smaller practices, and may discourage investment in sophisticated platforms where revenue visibility is limited.

Digital Divide, Infrastructure Limitations, and Data Security Concerns

The digital divide and infrastructure constraints also restrain the teledentistry market, particularly in low-resource settings. Effective teledentistry requires reliable broadband, appropriate hardware (cameras, intraoral imaging devices), and digital literacy on both the patient and provider sides. Studies of teledentistry utilization highlight challenges, including inadequate technology infrastructure, clinician and patient acceptance, reimbursement issues, and privacy and security concerns. For example, a review observed that while virtual care improved access, concerns about secure data transmission and use of non-HIPAA-compliant consumer applications were prominent. In rural and low-income communities, limited internet access and lower smartphone penetration can constrain the reach of real-time video consultations, forcing reliance on audio-only or store-and-forward approaches. Dental providers may also be hesitant to invest in cameras or integrated teledentistry systems without a clear return on investment, particularly when in-person demand is strong, slowing modernization of parts of the provider base.

Opportunities

Growth of Cloud-Based Platforms and Remote Patient Monitoring Models

One of the strongest opportunities lies in cloud-based teledentistry platforms integrated with remote patient monitoring, particularly for orthodontics and chronic disease management. Solutions such as Invisalign® Virtual Care and Invisalign® Virtual Appointment from Align Technology, Inc. allow orthodontists to remotely track aligner therapy progress via patient-submitted images and secure messaging in the My Invisalign app, reducing in-office visits while maintaining control over treatment. During the COVID-19, these tools were scaled rapidly to maintain continuity of care; their sustained use demonstrates the value of hybrid care models combining digital and physical touchpoints. Similar remote monitoring concepts are being adopted for post-operative checks, periodontal maintenance, and monitoring of high-risk patients, creating demand for platforms that combine video visits, asynchronous image review, automated reminders, and integrated documentation. As reimbursement frameworks for remote patient monitoring evolve across telehealth, vendors capable of offering scalable, cloud-hosted, interoperable software with analytics and integration into practice management systems will be well-positioned for double-digit growth.

Integration of Teledentistry into Broader Digital Health and Value-Based Care

A second major opportunity is the integration of teledentistry into wider digital health and value-based care ecosystems. Health systems and payers increasingly recognize oral health’s connection with chronic conditions such as diabetes and cardiovascular disease, creating incentives to align dental and medical care. Teledentistry can function as the “front door” for preventive interventions, early triage of infections, and education & training for high-risk groups, thereby reducing emergency department visits and advanced disease treatment costs. Large dental service organizations and integrated delivery networks are exploring business models that combine teledentistry with population health management, where virtual check-ins, educational content, and remote assessments are used to monitor oral health metrics in defined populations. As governments and private payers move toward bundled payments and quality-based incentives, platforms that generate measurable improvements in access, adherence, and clinical outcomes supported by robust data reporting can capture growing budgets within digital health transformation programs.

Category-wise Analysis

Component Insights

Within the component category, software & services are expected to be the leading segment, accounting for an estimated around 72% share of the teledentistry market in 2025. This dominance reflects the central role of cloud-based practice portals, patient apps, video communication tools, triage workflows, and billing integrations in enabling virtual dental care. Platforms from companies such as MouthWatch LLC, Dentulu Inc., Denteractive Solutions Inc., Teledentix (Virtual Dental Care), and The TeleDentists focus on delivering end-to-end software solutions that support synchronous video consultations, asynchronous case review, secure messaging, and electronic documentation. The shift towards subscription-based software-as-a-service (SaaS) models reduces upfront costs for dental practices and allows frequent feature updates, including AI-assisted image assessment and automated reminders. Services such as implementation support, training, and clinical workflow design further expand the revenue base. As regulations stress HIPAA-compliant and secure teledentistry workflows, demand will continue to concentrate on scalable, compliant software ecosystems rather than standalone hardware.

Delivery Mode Analysis

Among delivery modes, cloud-based platforms are projected to hold the leading share, estimated at about 65% of the teledentistry market in 2025, and to represent the fastest-growing deployment model. Cloud-based architectures enable anytime, anywhere access for providers and patients, facilitate integration with electronic health records and practice management systems, and support centralized updates and security patches. During the COVID-19 pandemic, cloud-hosted telehealth solutions scaled rapidly as providers sought to launch virtual clinics with minimal on-premise setup, a trend mirrored in dentistry. Cloud platforms also support multi-site dental organizations, mobile clinics, and outreach programs by allowing decentralized staff to log into the same system with appropriate role-based access. In contrast, traditional web-based/on-premise deployments require local server maintenance, VPN access, and higher capital expenditure, which many smaller practices are seeking to avoid. With ongoing advances in cybersecurity, encryption, and compliance frameworks, cloud-based teledentistry offerings are likely to remain the default choice for new deployments.

Regional Insights

North America Teledentistry Market Trends and Insights

North America has emerged as the dominant region in the global teledentistry market, fueled by advanced healthcare infrastructure, high digital literacy, and supportive telehealth regulations. In 2024, the region captured the largest market share, with the United States leading and Canada making significant progress in providing teledentistry services to rural and underserved areas.

Key trends driving growth include the widespread adoption of cloud-based platforms, AI-powered diagnostic tools, and mobile health applications, which enhance remote consultations and patient engagement. High smartphone penetration and reliable internet connectivity have further accelerated usage among dental providers and patients alike. Moreover, favorable reimbursement policies and increasing awareness of teledentistry’s cost-effectiveness are motivating clinics and hospitals to integrate virtual dental services into their regular practice.

With continuous technological innovation, policy support, and patient-focused solutions, North America maintains its leadership in teledentistry, setting a benchmark for other regions seeking to expand virtual dental care services.

Asia Pacific Teledentistry Market Trends and Insights

The Asia Pacific region is the fastest-growing teledentistry market, driven by rapid digitization, large populations, and increasing awareness of telehealth solutions. Countries such as China, Japan, South Korea, Australia, and India are at different stages of adoption but share common trends: rising smartphone penetration, expanding broadband coverage, and government support for telemedicine to bridge access gaps. In markets like Japan and South Korea, advanced health systems and high digital literacy support early adoption of virtual dental consultations and remote orthodontic monitoring. In India and parts of ASEAN, telehealth platforms increasingly partner with dentists to provide remote consultations that extend services into rural and semi-urban regions, as highlighted by case examples of telehealth providers enabling video-based dental visits.

The Asia Pacific synchronous teledentistry space is evolving quickly, with real-time video consultations used for emergency triage, follow-up reviews, and cross-border specialist opinions. Private dental chains and start-ups are experimenting with app-based virtual dental services and AI-supported image assessment to increase scalability and standardization. Regulatory frameworks vary widely, but many countries have issued telemedicine guidelines since COVID-19, which often include or imply dental services, creating a more permissive environment than before the pandemic. Manufacturing advantages in hardware-such as low-cost intraoral cameras and imaging accessories produced in China and India-also reduce barriers to equipping clinics for tele-exams. Collectively, these factors position Asia Pacific for sustained double-digit teledentistry growth over the forecast period.

Competitive Landscape

The global teledentistry market is highly competitive, characterized by rapid technological innovation and the adoption of digital solutions across dental care providers. Key players focus on developing cloud-based platforms, AI-assisted diagnostics, and mobile consultation tools to enhance patient engagement and streamline workflow efficiency. Market competition is also driven by pricing strategies, service quality, and integration capabilities with existing healthcare systems. New entrants are leveraging remote monitoring and virtual consultation technologies to capture niche segments, while established providers invest in research, partnerships, and software upgrades to maintain market share.

Key Developments:

- In January 2026, OrisDX and Teledentistry.com entered into a strategic partnership to expand access to early oral cancer detection by integrating OrisDX’s non-invasive salivary rinse test into the Teledentistry.com virtual care platform. Under the agreement, Teledentistry.com’s network of licensed dentists would be able to prescribe and facilitate the high-accuracy oral cancer diagnostic test during virtual consultations, allowing patients, including those in high-risk or underserved areas to receive advanced screening remotely.

- In April 2025, DentalMonitoring unveiled a suite of AI-powered tools and strategic platform partnerships, highlighting its most extensive product showcase to date. The company introduced DentalMonitoring+, featuring dynamic 3D visualization for improved clinical assessment, and launched AIDA Auto Replies, an AI tool to streamline communication within the platform. It also announced an Integration Partnership Program to expand collaborations with aligner manufacturers, patient management systems, scanners, and referral platforms, strengthening remote monitoring and workflow capabilities for orthodontic practices.

Companies Covered in Teledentistry Market

- Align Technology, Inc.

- Koninklijke Philips N.V.

- MouthWatch LLC

- Dentulu Inc.

- Denteractive Solutions Inc.

- Toothpic, Virtudent, Inc.

- Straight Teeth Direct

- Teledentix (Virtual Dental Care)

- The TeleDentists

- Live Dentist Inc.

- Henry Schein, Inc.

- SmileDirectClub, Inc.

- Colgate-Palmolive Company

Frequently Asked Questions

The global teledentistry market is expected to reach US$ 2.1 billion in 2026, supported by sustained post-pandemic demand for virtual dental consultations, expanding telehealth reimbursement, and growing integration of digital tools into routine dental workflows across major regions.

Major demand drivers include the need to expand access to dental care in rural and underserved areas, telehealth policy evolution following COVID-19, high burden of oral diseases affecting over 3.5 billion people, and growing use of cloud-based platforms for teleconsultation and remote patient monitoring in orthodontics and general dentistry.

North America is the leading region, with about 39% share in 2025, driven by advanced digital health infrastructure, supportive professional policies from organizations such as the ADA, significant telehealth reimbursement across many payers, and the presence of leading teledentistry innovators and dental service organizations.

The most attractive opportunity lies in integrating teledentistry with remote patient monitoring and value-based care models, where cloud-based platforms, AI-augmented image analysis, and app-based patient engagement can help payers and providers improve outcomes, reduce emergency utilization, and manage high-risk populations more efficiently.

Key market participants include Align Technology, Inc., Koninklijke Philips N.V., MouthWatch LLC, Dentulu Inc., Denteractive Solutions Inc., Toothpic, Virtudent, Inc., Straight Teeth Direct, Teledentix (Virtual Dental Care), The TeleDentists, Live Dentist Inc., and Henry Schein, Inc., among others providing platforms, services, and integrated virtual care solutions.