- Automation & Robotics

- Smart Pigs Market

Smart Pigs Market Size, Share, and Growth Forecast 2026–2033

Smart Pigs Market by Technology (Magnetic Flux Leakage, Ultrasonic, Caliper), Pipeline Type (Liquid, Gas), Service (Inspection, Cleaning, Maintenance), End-user Industry (Oil & Gas, Chemical Industry, Water & Wastewater), and Regional Analysis 2026 – 2033

Smart Pigs Market Share and Trends Analysis

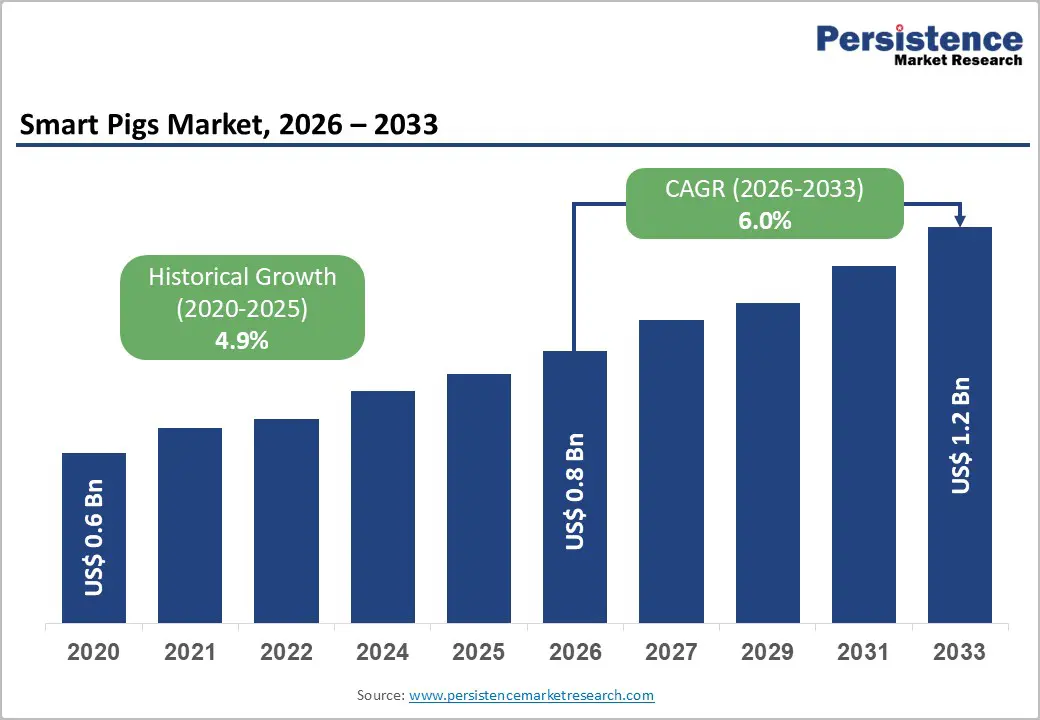

The global smart pigs market size is likely to be valued at US$0.8 billion in 2026 and is projected to reach US$1.2 billion by 2033, growing at a CAGR of 6.0% between the forecast period 2026-2033, driven by the integration of artificial intelligence (AI) in data interpretation and the rising demand for high-resolution inspection tools in the gas and chemical sectors.

Smart pig technology, enabled by magnetic flux leakage (MFL), ultrasonic (UT), and caliper-based sensors, has become indispensable for pipeline operators seeking to extend asset lifecycles while managing regulatory obligations in an increasingly stringent compliance environment.

Key Industry Highlights:

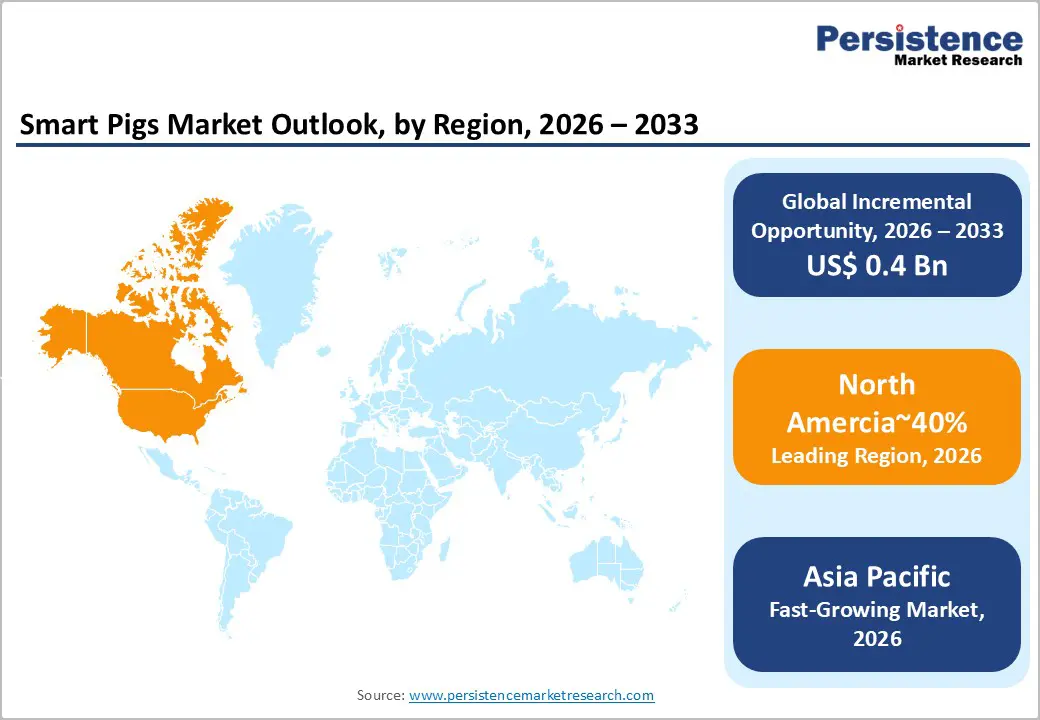

- Leading Region: North America is expected to lead the smart pigs market, accounting for 40% of the share, supported by strict pipeline safety regulations, extensive aging pipeline networks, and sustained inspection demand across oil and gas transmission infrastructure.

- Fastest-growing Region: Asia-Pacific is projected to be the fastest-growing region, driven by large-scale pipeline infrastructure expansion, energy security investments, and the increasing adoption of advanced inspection technologies across emerging economies.

- Leading Technology Type: Magnetic flux leakage technology is likely to be the leading segment, with about 57% adoption in 2026, owing to reliable metal loss detection, cost-effectiveness, high run-speed capability, and compatibility with long-distance ferrous pipelines.

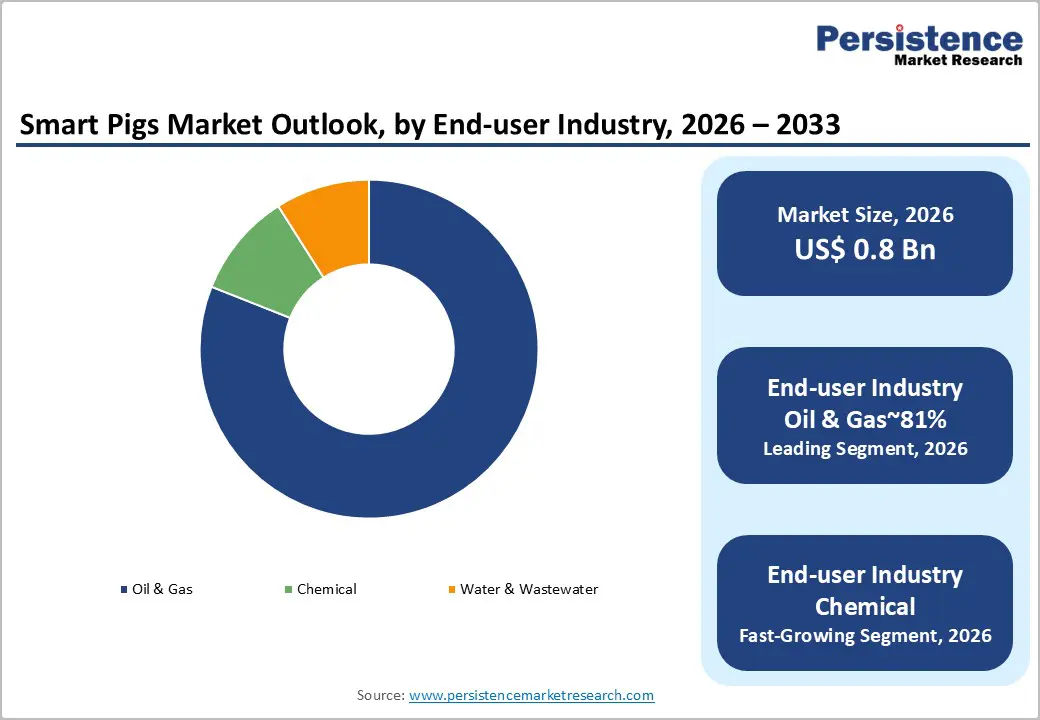

- Leading End-user Industry: The oil & gas segment remains the leading end-user segment with about 81% market share, supported by extensive pipeline assets, strict regulatory oversight, ESG compliance requirements, and capital-intensive integrity programs.

| Key Insights | Details |

|---|---|

| Smart Pigs Market Size (2026E) | US$0.8 Bn |

| Market Value Forecast (2033F) | US$1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Dynamics – Driver, Barrier, and Opportunity Analysis

Technological Evolution in Data Analytics and Sensor Fusion

The smart pigs market is undergoing a significant transformation due to the integration of artificial intelligence, real-time analytics, and predictive maintenance systems. Hybrid multi-technology tools that combine MFL, UT, and EMAT sensors in a single inspection run are reducing operational downtime and greatly enhancing defect classification accuracy.

When paired with industrial IoT platforms and digital twin environments, these tools convert inspection data into quantified risk scores and automated intervention prioritization. Recent deployments, such as AI-powered anomaly classification systems and large-diameter ultrasonic tools for subsea pipelines, demonstrate how sophisticated sensors can reduce decision-making cycles from weeks to hours while improving safety and compliance outcomes.

Advancements in data analytics and sensor fusion are reshaping the commercial value of in-line inspections. Smart pigs are no longer just data collection devices but have evolved into decision support systems, backed by machine learning-driven diagnostic engines that can automatically size defects and assess their severity. This shift is reducing interpretation times and reducing unnecessary excavation, thereby improving the efficiency of maintenance capital. Adoption remains uneven due to challenges, including regulatory scrutiny, data governance issues, and the complexity of integrating these technologies into legacy pipeline networks.

High Initial Capital Expenditure and Operational Costs Complexity

High initial capital expenditure and operational complexity remain persistent restraints on the adoption of smart pigging in the pipeline inspection market. Advanced ultrasonic and EMAT-based tools require substantial upfront investment and are further constrained by the need for compatible launchers, receivers, and controlled flow conditions during deployment. Inspection campaigns often introduce operational disruptions, elevating indirect costs for operators managing throughput-sensitive assets. For smaller regional and non-regulated pipeline owners, high per-kilometer inspection expenses continue to delay inspection cycles, particularly where regulatory enforcement remains uneven, reinforcing a bifurcation between compliance-driven and discretionary adoption.

Operational economics create additional challenges for penetration in price-sensitive regions. Smart pig programs require certified personnel, tailored tool configurations for different pipeline sizes and materials, and a strong data management system to process high-resolution inspection results. Although lifecycle economics increasingly favor intelligent inspection over manual methods, the high upfront costs and execution complexity limit short-term adoption by budget-conscious operators. These barriers slow market growth, even though the long-term safety and integrity benefits are clear.

Integration of Hydrogen-Ready Inspection Solutions

The transition to hydrogen transportation presents a clear opportunity in the smart pigs market, but the underlying technical rationale must be explicit. Hydrogen molecules are significantly smaller than methane and interact differently with steel pipelines, increasing susceptibility to micro-cracking, fatigue acceleration, and hydrogen-induced embrittlement.

As a result, conventional inspection tools designed for natural gas service lack the sensitivity required to validate pipeline integrity for hydrogen blending or full conversion. This shift is elevating inspection requirements from routine compliance to a prerequisite for asset repurposing, particularly under emerging hydrogen safety and certification frameworks.

Hydrogen-ready smart pigs address this gap through advanced sensing technologies, including ultrasonic and electromagnetic acoustic systems that can detect early-stage cracks and subtle material degradation without direct contact with the pipe wall. These tools are engineered to operate reliably under high-pressure hydrogen conditions, enabling higher diagnostic confidence. The specialized nature of these inspections supports premium pricing and margin expansion, although adoption remains gated by regulatory clarity, pilot-scale hydrogen deployments, and capital allocation discipline among pipeline operators.

Category–wise Analysis

Technology Insights

Magnetic flux leakage (MFL) is projected to lead, accounting for roughly 57% of global technology adoption, positioning it as the leading inspection modality in intelligent pigging. Its dominance stems from dependable detection of metal loss and corrosion in ferrous pipelines without the need for liquid couplants. This advantage makes MFL well-suited for long-distance inspection programs where uninterrupted operations and ease of deployment are essential. Its cost effectiveness, ability to operate at high run speeds, and compatibility with a wide range of pipeline diameters further cement its status as the default baseline technology.

As regulatory frameworks increasingly emphasize corrosion control, MFL remains central to inspection strategies and provides a consistent revenue foundation. AI-driven diagnostics, real-time IoT data streaming, and hybrid MFL-UT tools further reinforce MFL’s role as the industry workhorse while improving predictive maintenance and operational efficiency.

The Automated ultrasonic Testing (UT) segment is likely to be the fastest-growing segment, propelled by its ability to provide millimeter-accurate measurements of wall thickness and detect axial and circumferential cracks. Growth is driven by stricter safety regulations, the expansion of the gas sector, and demand for high-consequence pipeline inspection. Leading trends include hybrid MFL-UT tools, live-streaming smart pigs, and compact mini-pig systems for small-diameter or previously “unpiggable” pipelines.

Companies such as T.D. Williamson, NDT Global, and Intero Integrity are driving innovation, with live-streaming UT pigs that detect micro-cracks in real time and cloud-based visualization suites that enable remote data analysis. Additional industrial developments include M&A activity, such as Baker Hughes’ acquisition of Quest Integrity, and the tracking of innovations, such as CDI’s Qube GPS-enabled pig locator.

End-user Industry Insights

The oil & gas segment is expected to remain the leading end user, accounting for 81% of total market revenue, reflecting its extensive pipeline networks and the critical need for integrity management across upstream, midstream, and downstream operations. High-consequence failure risk, strict regulatory oversight, and ESG-driven compliance elevate intelligent pigging from discretionary maintenance to mandatory inspection programs. Capital availability and technical maturity enable frequent deployment of advanced inspection technologies, ensuring recurring demand, premium service utilization, and long-term revenue stability.

A defining industry trend is the shift toward predictive maintenance, where operators use smart pig data to build digital twins of pipelines and forecast failure risks well ahead of inspection cycles. Major service providers, including Baker Hughes, ROSEN Group, and T.D. Williamson is strengthening digital diagnostics, AI-enabled analytics, and offshore-capable smart PIG platforms to support long-term midstream reliability.

The chemical Industry is likely to be the fastest-growing application segment as manufacturers prioritize leak prevention, product purity, and compliance with stricter environmental regulations. Unlike long-haul oil and gas pipelines, chemical networks feature complex geometries, smaller diameters, and aggressive media, driving demand for miniaturized, bend-tolerant inspection tools and chemically resistant sensor housings.

A key trend is the adoption of 4-inch mini-pigs, smart foam tools, and tethered robotic systems for lines lacking traditional launchers. Increasing transport of acids, alkalis, and specialty chemicals has also expanded the use of UT and EMAT-based solutions for non-ferrous and lined pipes. Companies such as Intero Integrity and NDT Global are actively commercializing compact inspection platforms and cloud-based data visualization tailored to chemical plants, positioning this segment as a high-growth, technology-intensive extension of the smart pigs market.

Regional Insights

North America Smart Pigs Market Trends

North America is projected to remain the largest regional market, accounting for 40% of the total share, driven by the concentration of high-risk pipeline infrastructure and the large scale of U.S. oil and gas networks. The region’s vast onshore and offshore pipeline systems, with a median asset age of over 40 years, create a consistent demand for recurring inspections. Regulatory requirements, such as the expanded PHMSA mandates on transmission line inspections, stress-corrosion cracking evaluations, and methane detection, further ensure a steady flow of capital directed toward intelligent pigging services.

Backlogs of deferred maintenance and uninspected pipelines also create immediate opportunities for deployment. The high service costs and complex technical demands support investments in hybrid multi-technology pigs, while ample capital availability sustains premium pricing and long-term revenue growth.

Regulatory expansion, aging infrastructure, and stringent compliance enforcement are the key factors shaping the market in North America, solidifying its position as both a dominant and high-value region. The intensity of inspections, driven by mandatory integrity programs, guarantees steady demand for service providers and fosters the adoption of high-end services.

Capital-heavy deployments remain focused on areas with the highest-risk pipelines, enabling concentrated revenue generation. The market is influenced by regulatory alignment, technological advancement, and scale-driven efficiency, creating a predictable, compliance-driven growth environment for intelligent pigging solutions.

Europe Smart Pigs Market Trends

Europe is expected to experience robust growth, driven by advanced pipeline infrastructure and regulatory-driven adoption across major economies. Countries such as Germany, the U.K., France, and Spain are at the forefront of implementing sophisticated inspection programs, whereas Eastern European networks face challenges posed by outdated assets and limited budgets. Regulatory frameworks, such as the EU SEVESO III Directive and national regulations, require integrity management and environmental protection, thereby creating sustained demand for intelligent pigging services.

The shift toward natural gas and the early development of hydrogen infrastructure further heighten inspection needs, while premium service offerings ensure stable revenue streams in Western Europe.

The accelerated modernization and expansion of assets in Central and Eastern Europe are positioning these regions as the fastest-growing areas on the continent. The increasing demand from emerging water utility networks, where reducing non-revenue water and monitoring quality align with inspection needs, adds further pressure. Compliance-driven budgets, environmental priorities, and technology adoption shape the market dynamics. Mature Western economies generate steady revenue through recurring integrity programs, while developing networks present new growth opportunities, reinforcing the critical role of inspection and maintenance services across Europe.

Asia Pacific Smart Pigs Market Trends

Asia-Pacific is expected to remain the fastest-growing regional market, driven by the rapid expansion of pipeline infrastructure and the increasing adoption of intelligent pigging technologies. The development of greenfield pipelines across India, China, Indonesia, Vietnam, and other ASEAN nations is a key driver of demand, while the gradual implementation of inspection programs on existing networks is supported by maturing regulatory frameworks and the growth of local service capabilities.

Concerns over energy security, LNG terminal expansions, and industrialization are further accelerating capital investments in pipeline integrity programs. The cost advantages in manufacturing also help emerging regional providers become more competitive, boosting adoption while preserving demand for high-quality, advanced inspection tools.

China and India are the main growth drivers in the region, thanks to large-scale transmission projects and the expansion of national gas grids. Alignment with international standards such as API and ISO has led to more frequent, compliance-driven inspections, while both state-owned and private operators are investing in advanced technologies to manage both aging and new pipelines. Japan contributes a steady demand, with its mature infrastructure requiring periodic re-inspection. The region’s market dynamics are shaped by infrastructure scale, regulatory requirements, technology adoption, and cost-efficient service delivery, collectively positioning Asia-Pacific as the world’s fastest-growing market for smart pigging services.

Competitive Analysis

The global smart pigs market is moderately consolidated, with the top five players ROSEN Group, Baker Hughes, T.D. Williamson, NDT Global, and Xylem (Pure Technologies) collectively account for approximately 60% of the total market share. The remaining 40% comprises specialized regional service providers and niche technology firms, sustaining a fragmented competitive landscape across lower-complexity and inland pipeline segments.

Market concentration is particularly high in high-resolution ultrasonic and offshore inspection applications, driven by substantial technical expertise, precision engineering, and extensive R&D investment requirements. Competitive positioning is increasingly determined by proprietary sensor technologies, data analytics integration, and service reliability, while smaller players differentiate through cost-effective localized services. The market is expected to evolve with the adoption of digital twin frameworks, automated defect analysis, and enhanced inspection accuracy, reinforcing the dominance of leading global firms while enabling targeted growth opportunities for specialized entrants.

Key Industry Developments

- In December 2025, Baker Hughes secured a significant multiyear Artificial Lift and Surveillance contract with Kuwait Oil Company. The agreement involves integrating intelligent production drives (FusionPro™) with automated field solutions to improve the reliability of large-scale extraction and pipeline feeding systems.

- In July 2024, T.D. Williamson (TDW) developed the 22-inch MDS™ Inline Inspection System to address complex anomalies. This new 22-inch platform provides multi-diameter flexibility and advanced analytics, allowing it to detect interacting anomalies that traditional pigs typically overlook.

- In April 2024, ROSEN Group launched the next-generation RoCorr + EMAT Ultra for high-resolution crack detection. This system is specifically designed to identify subcritical stress-corrosion cracking (SCC) at higher spatial resolution, thereby enhancing safety for aging gas pipelines.

- In November 2023, ROSEN Group reported record revenue growth following the acquisition of a controlling stake. The 2024 acquisition by Partners Group provided the capital required for large-scale R&D, particularly in EMAT technology and AI-powered image processing, to accelerate data interpretation.

Companies Covered in Smart Pigs Market

- Baker Hughes

- ROSEN Group

- T.D. Williamson

- NDT Global

- Enduro Pipeline Services

- Xylem (Pure Technologies)

- Enbridge Inc.

- Applus+ RTD

- Intertek Group plc

- Dacon Inspection

- MISTRAS Group

- Weatherford Houston

- Quest Integrity Group

Frequently Asked Questions

The global smart pigs market is projected to be valued at US$0.8 billion in 2026 and is expected to reach US$1.2 billion by 2033, driven by increasing pipeline integrity inspection requirements worldwide.

The adoption of smart pigging solutions is growing due to stricter pipeline safety regulations, the aging of oil and gas infrastructure, and the increasing need for precise inline inspections to detect issues such as corrosion, cracks, and metal loss, all while reducing operational risks.

The smart pigs market is expected to grow at a CAGR of 6.0% between 2026 and 2033, supported by technological advances in ultrasonic, MFL, and data analytics-enabled inspection tools.

The fastest growth opportunities in the smart pigs market are emerging in the Asia Pacific region, fueled by extensive pipeline infrastructure expansion, investments in energy security, and the growing adoption of advanced inspection technologies in developing economies.

Key players include Baker Hughes, ROSEN Group, and T.D. Williamson, NDT Global, Quest Integrity Group, Weatherford, SGS SA, Bureau Veritas, Applus+ RTD, Intertek Group plc, MISTRAS Group, and Dacon Inspection.