- Agrochemicals

- Rodent Control Pesticides Market

Rodent Control Pesticides Market Size, Share, and Growth Forecast 2026 - 2033

Rodent Control Pesticides Market by Product Type (Anticoagulant Rodenticides, First-generation anticoagulants, Second-generation Anticoagulants, Non-Anticoagulant Rodenticides), Rodent Type (Rats, Mice, Chipmunks, Hamsters, Others), Formulation (Pellet, Powder, Spray, Others), Distribution Channel (Offline Channels, Online Channels), and Regional Analysis, 2026 - 2033

Rodent Control Pesticides Market Size and Trend Analysis

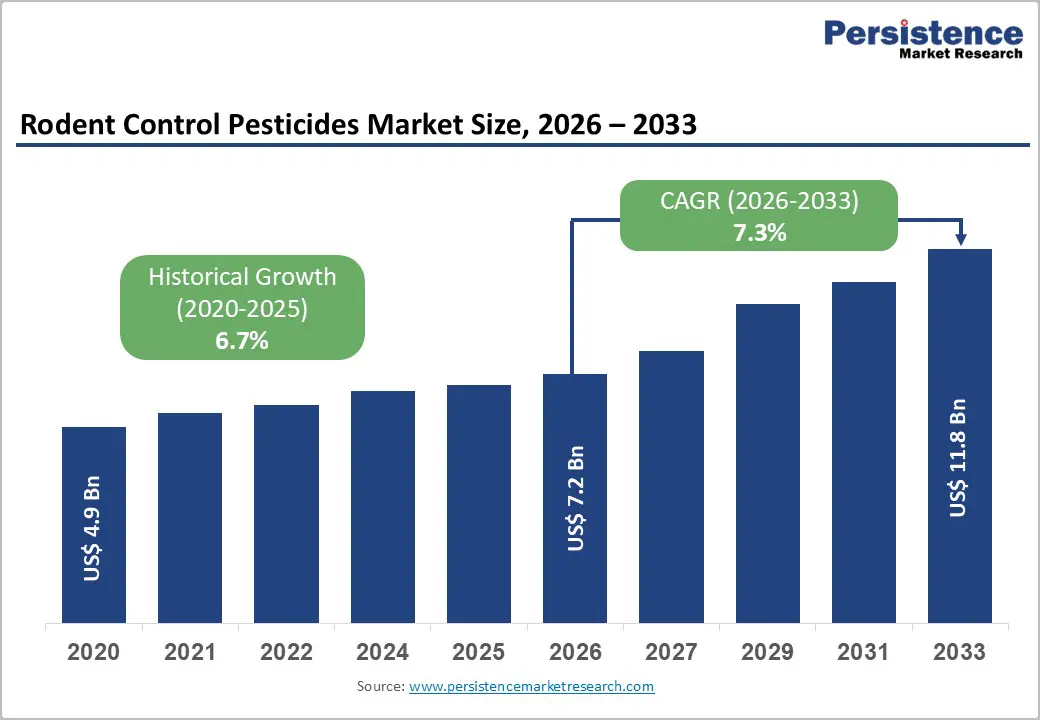

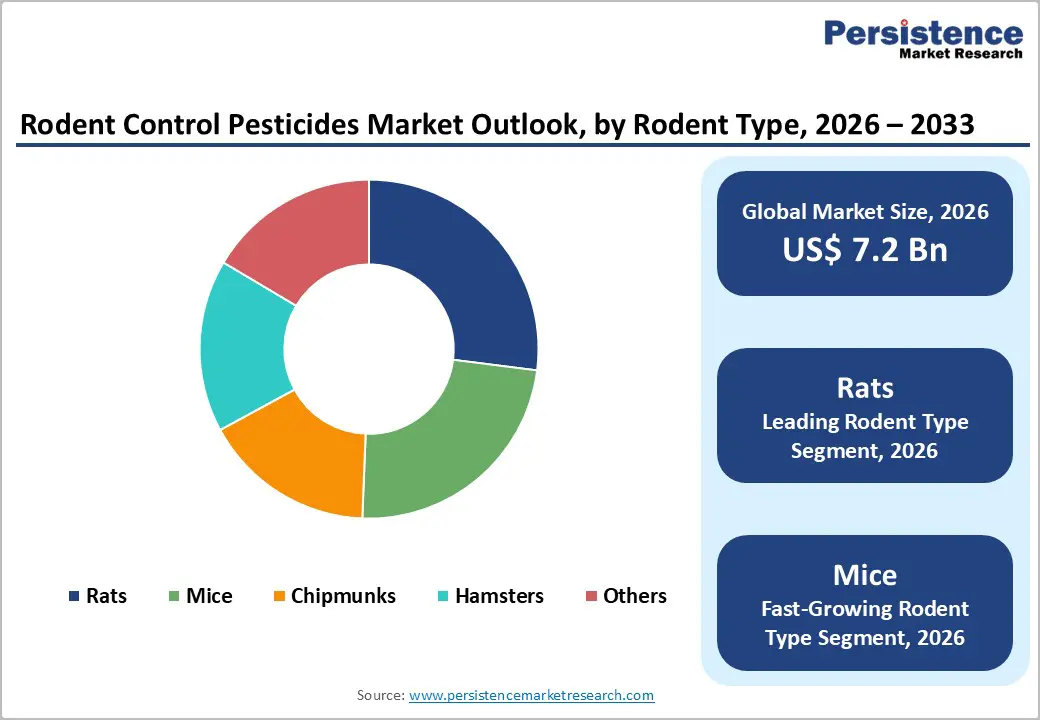

The global rodent control pesticides market size is expected to be valued at US$ 7.2 billion in 2026 and projected to reach US$ 11.8 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

Rising urbanization, intensifying agriculture, and greater public health awareness are key demand drivers. Rodents cause significant food losses globally, prompting strong adoption across farming and storage sectors. Urban infestations are also increasing due to dense populations, gaps in waste management, and climate shifts. Additionally, regulatory emphasis on safe pesticide usage to control zoonotic diseases is accelerating adoption across residential, commercial, and municipal applications worldwide.

Key Industry Highlights:

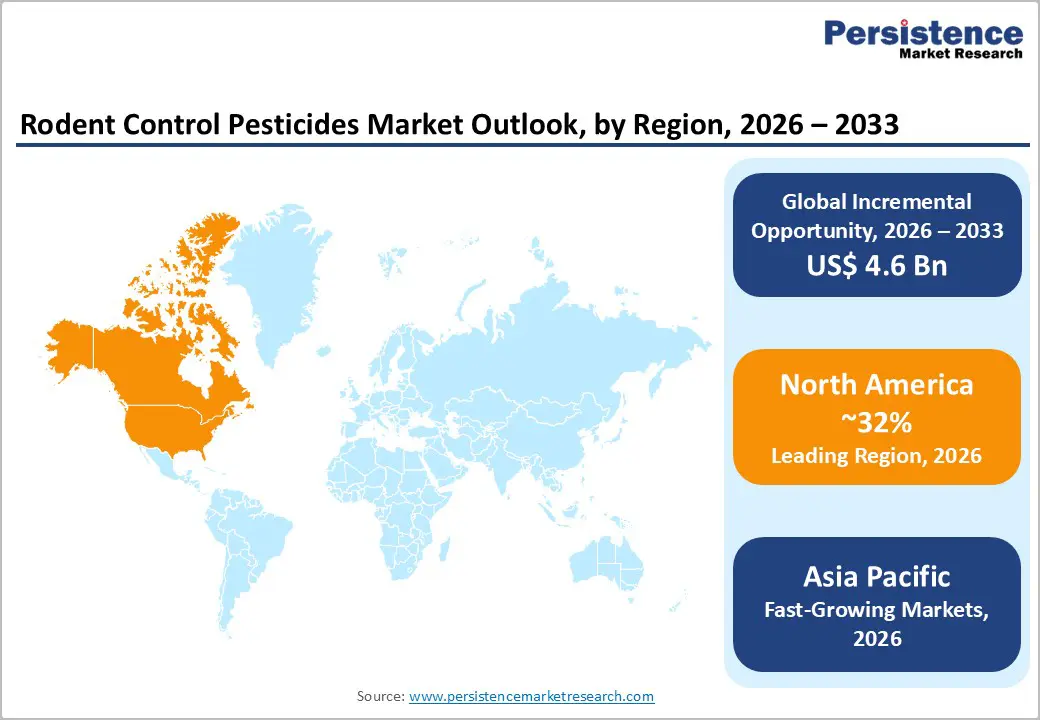

- Leading Region: North America dominates with 32% share (2025), driven by strict regulations, high infestation rates, and strong pest control infrastructure.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by rapid urbanization, agricultural expansion, and rising food safety concerns.

- Leading Category Product Type: Second-generation anticoagulants lead with 55% share (2025) due to superior efficacy and effectiveness against resistant rodent populations.

- Fastest-Growing Category Distribution Channel: Online channels are the fastest-growing, driven by expanding e-commerce access and increasing digital adoption.

- Key Opportunity: Expansion of IPM-based solutions offers strong potential, reducing pesticide use while improving long-term rodent control efficiency.

Market Dynamics

Drivers - Urbanization and Agricultural Expansion Driving Rodenticide Demand

Rapid urbanization and agricultural expansion are significantly driving demand for rodent control pesticides by creating dense human and food ecosystems favorable for rodent proliferation. Increasing urban populations lead to higher waste generation and crowded housing conditions, escalating infestations in residential and commercial spaces. In agriculture, rodent damage to crops and stored grains results in substantial economic losses, compelling farmers and authorities to adopt effective chemical control solutions.

Rodent damage in food systems can reach up to 20% of global production, making it a critical food security concern. In developing regions, particularly Asia, large-scale agricultural dependency and inadequate storage infrastructure further intensify losses. Governments and cooperatives increasingly integrate rodenticide-based pest control into agricultural protection programs, ensuring consistent demand for effective and scalable rodent control pesticides across rural and urban applications.

Public Health Regulations Accelerating Market Adoption

Stringent public health and food safety regulations are strongly supporting the adoption of rodent control pesticides worldwide. Rodents are known carriers of diseases such as leptospirosis and hantavirus, prompting governments to enforce stricter sanitation and pest control standards. Regulatory agencies mandate safe and controlled use of rodenticides, encouraging adoption of approved and standardized products across residential, commercial, and municipal environments.

In major regions, compliance frameworks require safer formulations, proper labeling, and controlled distribution channels, reducing reliance on unregulated alternatives. These rules push end users, such as food processors, hospitals, and municipal bodies, toward certified solutions despite the higher costs. As a result, regulatory pressure not only improves safety outcomes but also ensures steady, long-term demand for compliant rodent control pesticide products globally.

Restraints - Regulatory Pressure Limiting Chemical Rodenticide Use

The rodent control pesticides market is increasingly constrained by stringent regulatory restrictions on chemically active ingredients, especially second-generation anticoagulants. Environmental agencies have raised concerns about secondary poisoning of non-target wildlife through food-chain accumulation, leading to tighter use rules. In Europe, several rodenticide formulations have been restricted in sensitive zones, while regulators promote safer, integrated pest management approaches over broad chemical application.

In the United States, the EPA enforces strict guidelines, including tamper-resistant bait stations, restricted outdoor use, and enhanced labeling requirements, thereby increasing compliance costs for end users. These measures make the application more difficult for residential and small-scale users. Additionally, re-registration requirements under evolving safety frameworks raise costs for manufacturers, reducing product availability and slowing innovation, thereby restraining overall market expansion.

Rodent Resistance Reducing Product Effectiveness

A major restraint for the rodent control pesticides market is the increasing development of resistance in rodent populations, particularly against widely used first-generation anticoagulants. Studies indicate that resistance has become widespread in urban rat populations, significantly reducing the effectiveness of conventional rodenticides. This leads to repeated infestations, higher treatment frequency, and reduced confidence among end users in traditional chemical solutions.

To manage resistance, users are shifting toward stronger second-generation anticoagulants or non-anticoagulant alternatives, which are costlier and more tightly regulated. In many urban regions, resistant rodents can tolerate significantly higher doses of older compounds, complicating control programs. This growing resistance trend increases operational costs, increases the R&D burden for manufacturers, and highlights the need for integrated pest management strategies that combine chemical and non-chemical approaches for long-term effectiveness.

Opportunities - Eco-Friendly Rodenticides Driving Next-Gen Solutions

A key opportunity in the rodent control pesticides market is the rapid development of eco-friendly, low-toxicity, and targeted rodenticide formulations. Increasing environmental concerns and regulatory pressure in developed regions are pushing demand for non-persistent chemicals that reduce ecological impact. Non-anticoagulant options such as zinc phosphide, bromethalin, and cholecalciferol are gaining traction due to improved safety profiles and strong efficacy in controlled field conditions.

These formulations are especially preferred in urban parks, peri-urban farms, and ecologically sensitive areas where traditional anticoagulants are restricted. Additionally, advancements in precision pest control technologies, such as smart bait stations and AI-enabled monitoring systems, are improving product efficiency. This shift aligns with sustainability goals and supports higher-value demand from municipal bodies, large farms, and food processing industries seeking safer and more efficient rodent control solutions.

Expansion of Integrated Pest Management Services

The expansion of Integrated Pest Management (IPM) services presents a significant growth opportunity for the Rodent Control Pesticides market. Governments and agricultural bodies are increasingly promoting IPM practices that combine chemical, biological, and mechanical pest control methods to reduce overall pesticide usage. These programs encourage the controlled and optimized use of rodenticides, improving effectiveness while minimizing environmental impact and the development of resistance.

This shift is driving strong demand for service-based pest management models that bundle rodenticides with monitoring, inspection, and digital reporting services. Companies are increasingly offering subscription-based pest control contracts, particularly in warehouses, food processing facilities, and logistics hubs. As pest risks rise in urban and post-pandemic supply chains, IPM-driven service ecosystems are transforming rodenticide demand from standalone products into integrated long-term pest management solutions.

Category-wise Analysis

Product Type Insights

Anticoagulant rodenticides dominate the rodent control pesticides market, with second-generation anticoagulants accounting for around 55% of the global share in 2025. Their high efficacy against resistant rodent populations and single-dose lethality make them widely preferred in urban and agricultural applications. Active compounds such as brodifacoum and bromadiolone deliver strong performance in high-infestation environments, such as grain storage and dense urban centers.

Non-anticoagulant rodenticides are emerging as the fastest-growing category due to rising resistance issues and tightening environmental regulations. Products such as zinc phosphide and bromethalin are gaining acceptance for their rapid action and lower ecological persistence. These solutions are increasingly used in sensitive ecological zones and peri-urban farms, where reduced secondary poisoning risk and faster degradation are critical for sustainable pest management practices.

Rodent Type Insights

Rats remain the leading rodent type segment, accounting for about 48% of the global market in 2025. Their dominance is driven by severe economic losses, high adaptability, and widespread presence in urban infrastructure, agriculture, and storage facilities. Species such as Norway rats and black rats contribute significantly to contamination and structural damage, making them a primary target for rodent control programs worldwide.

Mice are the fastest-growing segment due to rising indoor infestations in residential, commercial, and food-processing environments. Their ability to enter small spaces and contaminate stored products has increased demand for specialized bait formulations and compact control systems. Growing urban density and climate-driven migration into buildings further strengthen the need for targeted and efficient mouse-specific rodenticide solutions.

Formulation Insights

Pellet formulations dominate the market, accounting for around 52% share in 2025, owing to their durability, weather resistance, and high palatability. They are widely used in agricultural fields, grain storage facilities, and outdoor baiting systems where long-lasting effectiveness is essential. Their ease of handling and strong field performance make them the preferred choice for both large-scale and small-scale rodent control operations.

Spray-based formulations are the fastest-growing segment due to rising demand for precision pest management in urban and institutional environments. They enable targeted application in hard-to-reach areas such as cracks, baseboards, and confined indoor spaces. Increasing adoption of IPM practices in hospitals, food processing units, and commercial facilities is further accelerating their use as part of integrated rodent control strategies.

Distribution Channel Insights

Offline channels lead the Rodent Control Pesticides market with around 65% share in 2025, supported by strong reliance on agro-retail stores, distributors, and pest control suppliers. These channels remain preferred due to expert guidance, immediate availability, and established trust among farmers and professional pest control operators. In many developing regions, physical retail continues to dominate pesticide procurement.

Online channels are the fastest-growing segment, driven by expanding e-commerce platforms and improving digital accessibility. Farmers, households, and commercial users increasingly prefer online purchasing for convenience, wider product selection, and transparent pricing. Growth in digital agriculture initiatives and the expansion of logistics infrastructure is further enabling remote areas to access rodent control products efficiently, transforming traditional distribution models.

Regional Insights

North America Rodent Control Pesticides Market Trends and Insights

North America leads the rodent control pesticides market, accounting for about 32% of the global share in 2025. The region benefits from a mature regulatory framework under the EPA, high pest control spending, and strong adoption of professional rodent management services. Rising urban rodent complaints and strict compliance requirements for bait stations and application practices further drive demand for advanced and regulated rodenticides across residential, commercial, and municipal applications.

The region is witnessing strong innovation-led growth, supported by major agrochemical and pest control companies developing smart bait stations and data-driven monitoring systems. The integration of AI-enabled pest-tracking and IPM-based solutions is improving efficiency and reducing chemical use. Additionally, government-backed research on rodent-borne diseases and food safety continues to strengthen the adoption of premium rodent control solutions across urban infrastructure and food processing industries.

Europe Rodent Control Pesticides Market Trends and Insights

Europe accounts for a significant share of the rodent control pesticides market and is characterized by strict regulatory oversight and sustainability-driven pest management practices. Frameworks such as the Biocidal Products Regulation and Sustainable Use Directive emphasize reduced environmental impact, encouraging the use of safer, targeted, and IPM-compatible rodenticides. Rising infestations in warehouses and industrial facilities have further increased demand for compliant pest control solutions.

The region is expected to grow at a CAGR of approximately 5.9% during the forecast period, driven by regulatory modernization and the increasing adoption of eco-friendly formulations. A strong focus on resistance management and secondary poisoning risks is reshaping product portfolios across major markets such as Germany, France, and the UK. Additionally, EU sustainability initiatives are pushing manufacturers toward low-toxicity and precision-based rodent control solutions integrated with advanced monitoring systems.

Asia Pacific Rodent Control Pesticides Market Trends and Insights

Asia Pacific accounted for around 30% of the global rodent control pesticides market share in 2025, driven by rapid urbanization, agricultural expansion, and increasing food security concerns. Countries such as China, India, and Japan face significant rodent-related crop losses and storage contamination, encouraging government-backed pest control initiatives. Rising population density and expanding logistics infrastructure further intensify rodent infestations in urban and peri-urban areas.

The region is experiencing rapid growth, driven by strong agricultural demand, regulatory improvements in food safety, and large-scale infrastructure development. Increasing adoption of modern rodent control practices, including pellet formulations and IPM-based strategies, is boosting effectiveness. Additionally, strong agrochemical manufacturing capabilities and expanding export networks are reinforcing Asia Pacific’s role as a key global supply and demand hub for rodent control pesticides.

Competitive Landscape

The rodent control pesticides market is moderately consolidated, with a mix of global leaders and numerous regional players competing across product categories. Large companies benefit from strong research capabilities, extensive distribution networks, and established brand presence, while smaller manufacturers focus on cost-effective generic formulations and niche applications, maintaining competitive intensity at the local and mid-tier levels.

Competition is increasingly driven by innovation, regulatory compliance, and integrated solutions rather than pricing alone. Companies are investing in eco-friendly formulations, resistance management, and IPM-compatible technologies to capture premium segments. Additionally, expansion into emerging markets through partnerships and localized strategies, along with the rise of service-based models and digital monitoring platforms, is reshaping competitive dynamics.

Key Developments:

- In March 2025, BASF SE launched an eco-friendly second-generation anticoagulant rodenticide with reduced environmental persistence while maintaining efficacy. The formulation received conditional EPA approval for controlled urban and industrial use, aligning with sustainability-driven regulatory trends.

- In July 2024, Syngenta AG initiated a pilot for AI-enabled bait stations across major U.S. cities, integrating sensors and cloud analytics. The system reduced repeat infestations significantly, highlighting the growing role of data-driven technologies in improving rodent control efficiency.

- In November 2023, Corteva Agriscience expanded zinc phosphide rodenticide production capacity in India to address rising demand in Asian markets. The move supports increasing adoption of non-anticoagulant solutions in regions facing resistance and environmental sensitivity challenges.

Rodent Control Pesticides Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.9 Bn |

| Current Market Value (2026) | US$ 7.2 Bn |

| Projected Market Value (2033) | US$ 11.8 Bn |

| CAGR (2026-2033) | 7.3% |

| Leading Region | North America, 32% share |

| Dominant Formulation | Pellet, 52% share |

| Top-ranking Product | Anticoagulant Rodenticides, 55% |

| Incremental Opportunity | US$ 4.6 Bn |

Companies Covered in Rodent Control Pesticides Market

- BASF SE

- Bayer AG

- Syngenta AG

- UPL Limited

- Rentokil Initial plc

- Liphatech, Inc.

- Bell Laboratories Inc.

- Neogen Corporation

- Ecolab Inc.

- SenesTech, Inc.

- Rollins, Inc.

- JT Eaton & Co., Inc.

- PelGar International

- Abell Pest Control

Impex Europa S.L.

Frequently Asked Questions

The market is projected to reach US$ 7.2 billion in 2026, driven by urbanization, agricultural demand, and rising food safety concerns.

Key drivers include urbanization, agricultural expansion, and food safety regulations, with rodents causing up to 20% global food losses.

North America leads with 32% share (2025), supported by strong regulations and advanced pest control infrastructure.

Asia Pacific is the fastest growing region, driven by urban growth, agricultural losses, and improving food safety standards.

Expansion of IPM solutions offers strong potential by combining monitoring and control to reduce pesticide use while maintaining effectiveness.

Leading players include BASF SE, Syngenta AG, Cortev Agriscience, Bayer AG, Rentokil Initial plc, Rollins Inc., Ecolab Inc., and Neogen Corporation.