- Semiconductor Materials & Components

- RF Predistortion ICs Market

RF Predistortion ICs Market Size, Share, and Growth Forecast, 2026 - 2033

RF Predistortion ICs Market by Product Type (Digital RF Predistortion ICs, Others), Technology (GaAs Technology, Others), Application (Telecommunications, Broadcasting, Others), End-user (Telecom Service Providers, Others), and Regional Analysis for 2026 - 2033

RF Predistortion ICs Market Size and Trends Analysis

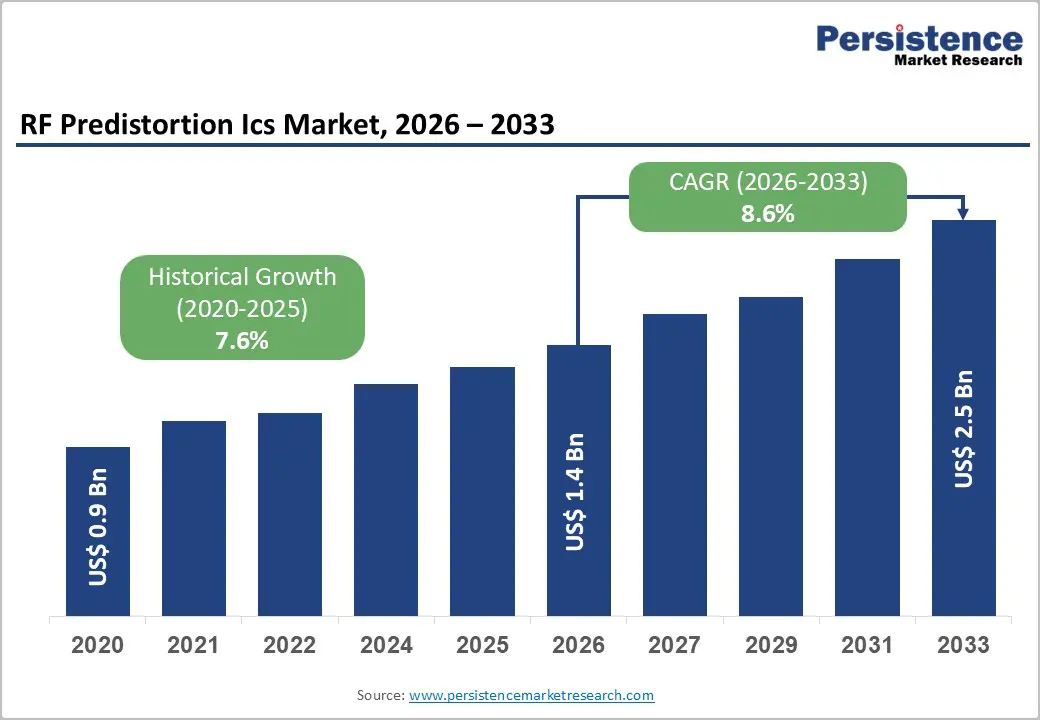

The global RF predistortion ICs market size is likely to be valued at US$1.4 billion in 2026, and is expected to reach US$2.5 billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of 5G network deployments, rising demand for linear power amplifiers in telecommunications, and advancements in digital RF predistortion ICs.

Growing demand for efficient, high-linearity RF predistortion ICs, especially in GaN and mixed-signal technologies, is accelerating adoption across applications. Advances in digital and GaN-based designs are further boosting uptake by offering superior distortion correction and power efficiency. The increasing recognition of RF predistortion ICs as critical to spectral efficiency in emerging wireless markets remains a major driver of market growth.

Key Industry Highlights:

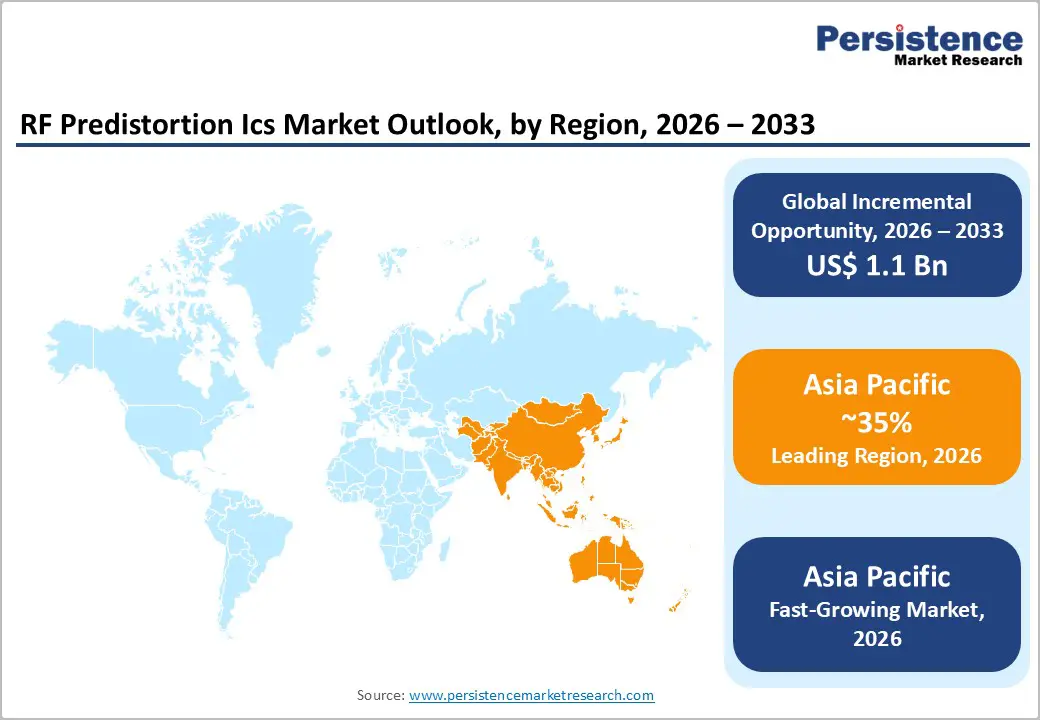

- Leading Region: Asia Pacific, anticipated to account for a 35% market share in 2026, driven by massive 5G rollout, high base station production, and strong demand in China and South Korea.

- Fastest-growing Region: Asia Pacific, fueled by telecom expansion, automotive radar growth, and growing investments in defense electronics.

- Dominant Product Type: Digital RF predistortion ICs, to hold approximately 55% of the revenue, as they provide adaptive correction for complex signals.

- Leading Technology: GaN technology is expected to account for over 40% of market revenue in 2026, thanks to its high power-handling and efficiency.

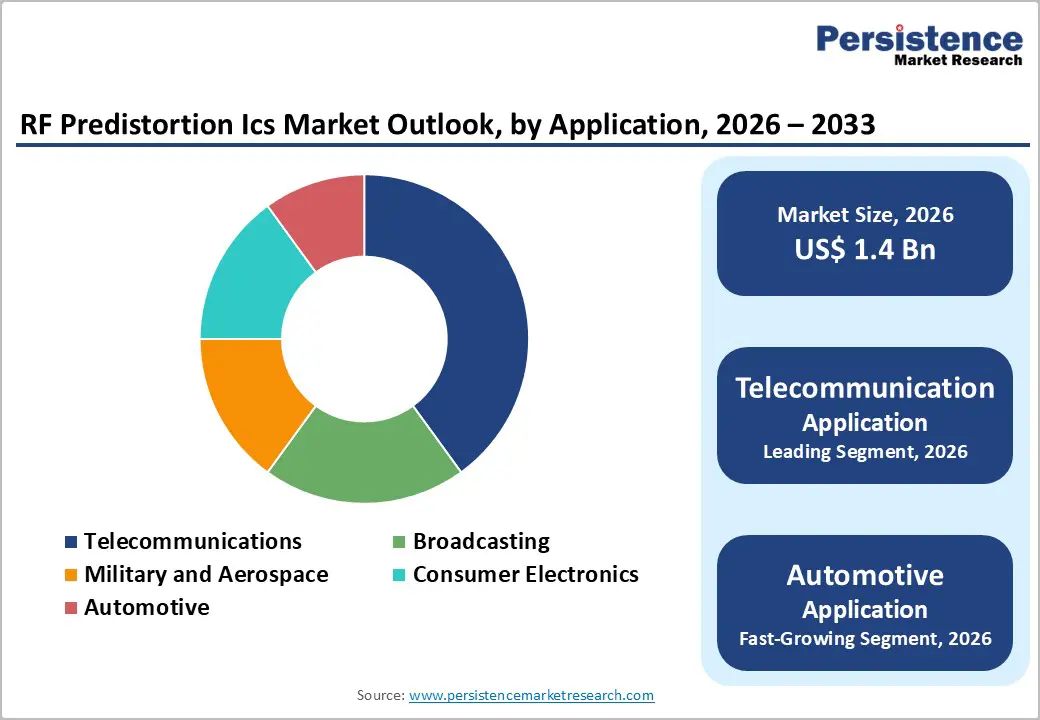

- Leading Application: Telecommunications, accounting for nearly 50% of market revenue due to 5G base station requirements.

- Leading End-user: Telecom service providers, to account for 45% revenue share in 2026, due to network upgrade needs.

| Key Insights | Details |

|---|---|

|

RF Predistortion ICs Market Size (2026E) |

US$1.4 Bn |

|

Market Value Forecast (2033F) |

US$2.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for5G Network Deployments

The increasing demand for 5G network deployment is driven by the need for faster data speeds, lower latency, and more reliable connectivity across diverse industries. As data consumption continues to surge, driven by video streaming, cloud computing, and the proliferation of connected devices, existing network infrastructure is approaching its performance limits. 5G technology addresses these challenges by delivering substantially higher bandwidth and supporting massive device connectivity, making it a cornerstone for next-generation digital ecosystems.

Sectors such as manufacturing, healthcare, automotive, and smart cities are accelerating 5G adoption to enable real-time applications, automation, and mission-critical communications. Advanced use cases, including autonomous vehicles, remote surgery, industrial robotics, and augmented reality, require ultra-low latency and stable connectivity, capabilities that only 5G networks can provide at scale. The growth of the Internet of Things is also driving demand for networks that can efficiently manage billions of connected sensors and devices. To meet this demand, telecom operators are heavily investing in infrastructure upgrades, including small cells, fiber backhaul, and other advanced network technologies.

Integration Challenges with Legacy Systems

Integration with legacy systems presents a major challenge, particularly in technology markets that depend on long-established infrastructure. Many existing systems are built on older architectures, interfaces, and processing standards, making them difficult to align with modern, high-performance solutions. Introducing new technologies often requires significant modifications at both the hardware and software levels, adding complexity and extending implementation timelines.

Legacy systems typically lack the flexibility to support advanced capabilities such as real-time optimization, adaptive control, or digital signal processing. Integrating new solutions may necessitate additional interface modules, custom firmware, or extensive re-engineering of system workflows. This not only increases integration costs but also raises the risk of performance issues or system instability. Operational downtime is another critical concern, as many legacy deployments support mission-critical services, making it challenging to schedule upgrades without disrupting ongoing operations.

Innovations in Digital and GaN-Based Delivery Platforms

Innovations in digital and GaN-based RF predistortion ICs delivery platforms are transforming the global amplification landscape by addressing two major challenges: linearity barriers and power efficiency. Digital platforms are engineered to achieve adaptive correction, reducing reliance on analog and enabling real-time distortion compensation in 5G systems. Innovations, such as CFR/DPD algorithms, machine-learning adaptation, wideband support, and integrated DACs, significantly improve ACPR and reduce back-off, thereby lowering operational costs for telecom and broadcasting campaigns.

Progress in GaN-based platforms, including high-voltage transistors, integrated predistortion, rugged packaging, and thermal management, supports more powerful amplification by minimizing heat, the IC’s first line of defense against failure. These formats eliminate efficiency trade-offs, enhance bandwidth, and allow versatile use without cooling overdesign, making them highly suitable for mass-scale base-station programs. New technologies such as bio-adhesive heatsinks, VLP-based monitoring, and quantum-inspired algorithms further enhance reliability and response.

Category-wise Analysis

Product Type Insights

Digital RF Predistortion ICs are anticipated to dominate the market, accounting for approximately 55% of revenue share in 2026. Its dominance is driven by adaptive algorithms, wideband support, and scalability, making it preferred for 5G applications. Digital RF Predistortion ICs provide real-time correction, ensure linearity, and contribute to efficiency, making them suitable for large-scale telecom campaigns. Analog Devices, Inc. has developed advanced digital predistortion (DPD) technology as part of its RF front-end solutions to improve power amplifier linearity and energy efficiency in 5G base stations and small cells. ADI’s digital predistortion techniques enable real-time adaptive compensation that maintains signal fidelity while allowing power amplifiers to operate more efficiently, a key requirement for high-bandwidth, wideband 5G deployments.

Mixed-signal RF predistortion ICs are likely to be the fastest-growing segment, driven by hybrid integration and expanding use in multi-standard systems. Its combined profile makes it ideal for targeted flexibility, overcoming the limitations of pure digital. Continuous innovations in integration are further strengthening its appeal, driving rapid adoption across North America and Europe, where demand for versatile RF is accelerating. MaxLinear’s Sierra single-chip radio SoC integrates RF, digital, and mixed-signal functions tailored for 5G Open RAN macro-cell radio units, enabling flexible support for multiple 5G bands and signal standards within a single platform. This integration reduces design complexity and supports diverse telecom equipment needs across North America and Europe, reflecting why mixed-signal RF predistortion ICs are gaining traction for versatile RF applications.

Technology Insights

GaN technology is expected to lead the market, accounting for approximately 40% of revenue in 2026, driven by high power density, large amplifier programs, and strong global demand for efficient RF. Their dominance continues as networks expand capacity. Rising adoption of silicon and expanded SiGe campaigns highlight the growing focus on cost alternatives. Qorvo, Inc. is a key example of how GaN technology leads the RF market by enabling high-power, high-efficiency RF amplifiers used in 5G telecommunications infrastructure. Qorvo’s GaN-on-SiC RF power amplifier modules are widely deployed in 5G base stations to deliver the superior power density and thermal performance required for wideband signals and high-capacity networks.

Silicon technology is likely to be the fastest-growing segment, due to strong momentum in cost reduction and expanding inclusion in consumer devices. The growing shift toward economical platforms, along with better integration, accelerates the adoption. Advancements in CMOS and continued progress of SoC blends entering production trials drive market growth. Socionext Inc. demonstrates how silicon technology drives rapid growth by leveraging RF-CMOS custom SoCs that integrate RF and digital functionality on a cost-effective silicon platform. Socionext’s RF-CMOS solutions combine analog RF circuits and baseband processing on a single silicon chip, reducing component count and manufacturing costs while addressing the needs of consumer electronics, IoT devices, and wireless communication systems.

Application Insights

The telecommunications segment is expected to dominate the market, contributing nearly 50% of revenue in 2026, due to remaining the primary hub for 5G linearization, large base-station programs, and the management of high-frequency signals that require distortion control. Their strong integration, trained engineers, and ability to handle high-volume or wideband blends drive higher consumption. Telecommunications sectors are leading digital rollouts and administering emerging mixed-signal trials. Ericsson’s 5G Radio System portfolio, which includes advanced base-station hardware for massive MIMO, beamforming, and wideband RF performance, has been deployed extensively by operators worldwide to support large-scale 5G network rollouts.

The automotive segment is likely to be the fastest-growing segment, driven by its strong radar presence and expanding role in ADAS. They offer convenient, quick, and accessible sensing, attracting OEMs who prefer reliable, low-distortion settings. Increased outreach programs, EV focus, and wider availability of routine and premium ICs further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. Infineon Technologies AG is a leading supplier of automotive radar ICs that power Advanced Driver Assistance Systems (ADAS) and safety features in modern vehicles. Infineon’s 76-81 GHz radar chips and highly integrated radar-on-chip solutions are widely used by global OEMs to support adaptive cruise control, collision avoidance, and autonomous emergency braking functionalities critical to EVs and semi-autonomous driving platforms.

End-user Insights

Telecom service providers are likely to dominate the market, with approximately 45% share in 2026, driven by the high volume of network upgrades and the strong global emphasis on 5G deployment. Regular rollout schedules, coverage requirements, and widespread access to GaN ICs drive consistent demand. Rising focus on defense and broadcasting further strengthens telecom leadership. Vodafone Idea Limited, one of India’s major telecom service providers, has actively rolled out 5G services across Delhi NCR and other priority circles through partnerships with network equipment vendors such as Ericsson, deploying high-performance 5G radio solutions designed to handle wideband signals and high-capacity data traffic. This deployment supports enhanced connectivity and network efficiency, reflecting how telecom operators are driving large-scale 5G infrastructure upgrades that require advanced RF components and GaN technology to manage high-frequency signals and distortion control in modern networks.

Defense contractors are expected to be the fastest-growing segment, driven by increasing demand for secure communications, vulnerability mitigation against jamming, and the expanding adoption of electronic warfare (EW) technologies. Enhanced system resilience, specialized performance grades, and robust integration for mission-critical applications are the key factors supporting rapid adoption. The rising use of aerospace, consumer electronics, and other high-tech sectors is further fueling market growth. Honeywell Aerospace is a leading defense contractor that develops advanced EW and secure communications RF solutions for military platforms, including the F-35, F-22, and MQ-9 Reaper. Their electronic warfare systems feature mission-specific RF and microwave components, subsystems, and secure signal processing modules designed to detect, deter, and counter evolving threats across land, sea, air, and space domains.

Regional Insights

North America RF Predistortion ICs Market Trends

North America’s growth is expected to be driven by its advanced 5G infrastructure, strong research and development capabilities, and high public awareness of the efficiency benefits. Systems in the U.S. and Canada provide extensive support for integrated circuit (IC) programs, ensuring broad accessibility of RF predistortion ICs across telecommunications, automotive, and military sectors. Rising demand for digital, convenient, and easily integrated solutions is further accelerating adoption, as these formats enhance linearity and reduce challenges associated with legacy amplifiers.

Technological innovation in RF predistortion ICs, including stable GaN integration, enhanced mixed-signal performance, and targeted wideband improvements, is attracting substantial investment from both public and private sectors. Government initiatives and FCC campaigns continue to drive adoption by addressing spectrum limitations, power costs, and emerging 6G challenges, sustaining market demand. The increasing emphasis on defense-grade and specialized applications, particularly in aerospace and related industries, is expanding the range of use cases for RF predistortion ICs.

Europe RF Predistortion ICs Market Trends

Europe’s growth is being driven by increasing awareness of spectral efficiency, robust telecommunications infrastructure, and government-led connectivity initiatives. Countries such as Germany, France, and the U.K. have established frameworks that support routine linearization and encourage the adoption of innovative IC solutions, including RF predistortion ICs. These high-performance technologies are particularly attractive to telecom operators, regulation-conscious industries, and automotive users, enhancing both efficiency and coverage.

Advancements in RF predistortion IC development, such as improved digital adaptation, application-specific delivery, and enhanced GaN grades, are further expanding market potential. European authorities are actively supporting research and pilot programs to address both standard and specialized IC requirements, reinforcing market confidence. Increasing emphasis on convenient, low-power solutions aligns with the region’s goals of optimizing spectrum use and reducing energy consumption. Public awareness campaigns and promotional efforts are broadening adoption across urban and rural areas, while suppliers are investing in integration and innovative variants to enhance overall performance.

Asia Pacific RF Predistortion ICs Market Trends

The Asia Pacific region is expected to lead the market for RF predistortion ICs in 2026, accounting for approximately 35% of the global share, and is also projected to be the fastest-growing region. This growth is driven by increasing awareness of 5G technology, supportive government initiatives, and the expansion of application programs across the region. Countries such as India, China, Japan, and various Southeast Asian nations are actively promoting the deployment of ICs to support network expansion and emerging automotive requirements. RF predistortion ICs are particularly appealing in these markets due to their efficient performance, scalability, and suitability for large-scale base station implementations in both urban and rural areas.

Advancements in technology are enabling the production of stable, high-performance, and easily deployable RF predistortion ICs that can operate effectively under challenging bandwidth conditions while minimizing distortion. These innovations are essential for reaching remote locations and enhancing overall signal coverage. The growing demand from telecommunications, automotive, and defense sectors is further driving market growth. Public-private partnerships, increased investments in connectivity, and rising spending on semiconductor research and manufacturing capacity are accelerating expansion. The ease of IC deployment, coupled with improved linearity and reduced interference risk, makes RF predistortion ICs a preferred solution in the region.

Competitive Landscape

The global RF predistortion ICs market features competition between established semiconductor leaders and emerging specialty providers. In North America and Europe, Analog Devices and Texas Instruments lead through strong R&D, distribution networks, and industry ties, bolstered by innovative digital and GaN programs. In the Asia Pacific, NXP Semiconductors advances with localized solutions, enhancing accessibility. Digital delivery boosts adaptation, cuts distortion risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. GaN formulations address power issues, enabling penetration into high-frequency applications.

Key Industry Developments:

- In March 2025, Murata Manufacturing launched the world’s first Digital Envelope Tracking (Digital ET) technology. This cutting-edge innovation is expected to significantly reduce power consumption in advanced RF circuits for 5G and future 6G devices, promoting greater energy efficiency across a range of applications. Collaborating with Rohde & Schwarz, Murata has leveraged their combined expertise to create an advanced RF measurement setup that showcases the capabilities of this pioneering Digital ET technology.

- In February 2024, MaxLinear, Inc., a leader in wireless infrastructure silicon solutions, announced it had launched the MXL17xxx family of devices (Sierra), a highly integrated SoC optimized for 4G/5G Open Radio Access Network (RAN) radio units (RU). Sierra is an innovative single-chip platform that flexibly supports major RU applications, including traditional macro, massive MIMO, picocell, and all-in-one small cells.

Companies Covered in RF Predistortion ICs Market

- Analog DevicesTexas Instruments

- Infineon Technologies AG

- NXP Semiconductors

- Macom

- Qorvo Inc.

- Wolfspeed

- Xilinx

- Inspower

- Microwaves & RF

Frequently Asked Questions

The global RF predistortion ICs market is projected to reach US$1.4 billion in 2026.

Key drivers include 5G infrastructure growth, network automation, and the need for low-power, high-efficiency circuits, supported by investments in telecom and advancements in GaN technology.

The RF predistortion ICs market is poised to witness a CAGR of 8.6% from 2026 to 2033.

Opportunities lie in 5G and IoT expansions, price reductions through scale, and integration in military/aerospace, potentially adding significant revenue via network automation and emerging tech.

Analog Devices, Texas Instruments, Infineon Technologies AG, NXP Semiconductors, and Qorvo Inc. are the key players.