- Rail

- Railcar Leasing Market

Railcar Leasing Market Size, Share, and Growth Forecast 2026 - 2033

Railcar Leasing Market by Railcar Type (Tank Cars, Freight Cars, Intermodal Cars, Refrigerated Cars, Specialized Railcars), Lease Type (Operating Lease, Finance Lease, Full-Service Lease, Net Lease), Cargo Type (Liquid Bulk, Dry Bulk, Containerized Cargo, Automotive Cargo, Industrial Goods), End-user, and Regional Analysis, 2026 - 2033

Railcar Leasing Market Size and Trend Analysis

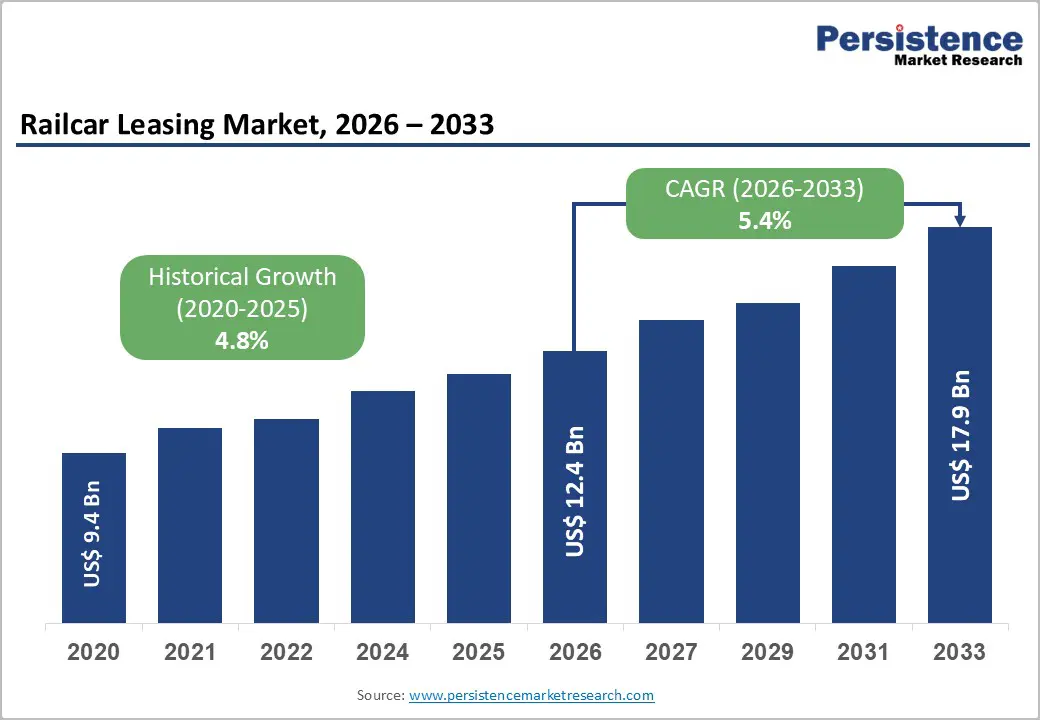

The global railcar leasing market size is likely to be valued at US$ 12.4 Billion in 2026 and is expected to reach US$ 17.9 Billion by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033.

Sustained growth in freight rail demand, capital optimization strategies among industrial operators, and accelerating infrastructure investment across both mature and emerging rail economies are the foundational pillars driving this market expansion.

Key Industry Highlights:

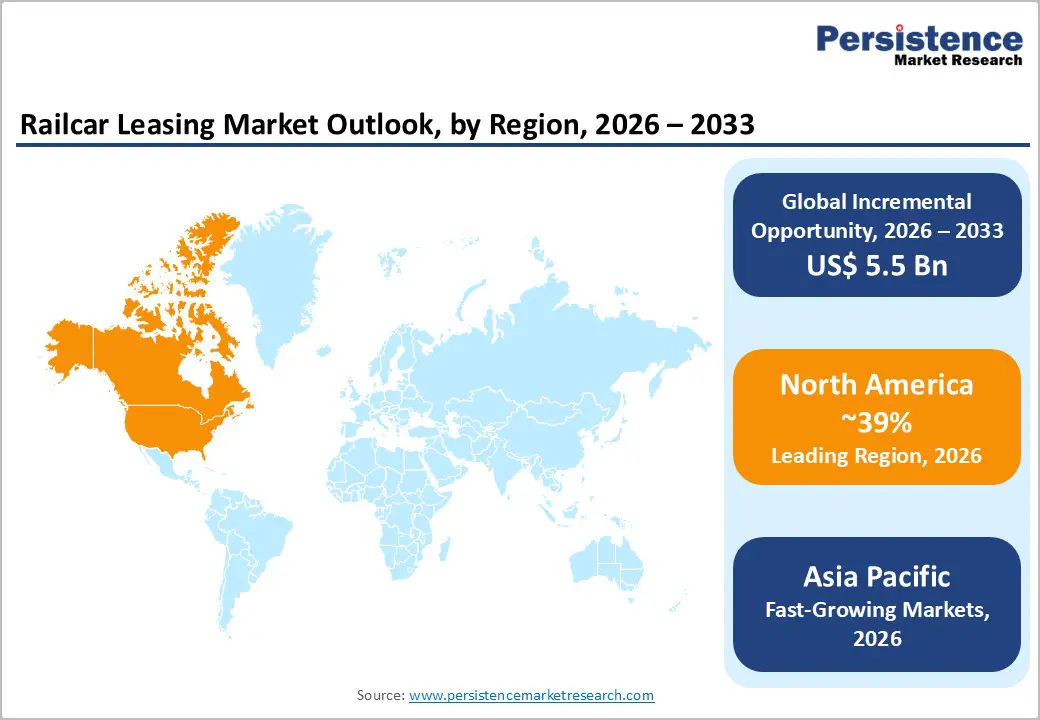

- Leading Region: North America leads the global Railcar Leasing market holding 39% share, underpinned by the world's largest private freight rail network spanning over 140,000 route miles, advanced leasing infrastructure, and the U.S. Bipartisan Infrastructure Law's US$ 66 billion rail investment commitment driving capacity expansion.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 6.1%, propelled by India's Dedicated Freight Corridor program, China's continued freight rail capacity investment under Five-Year Plans, and progressive adoption of leasing models across industrial freight operators in emerging manufacturing economies.

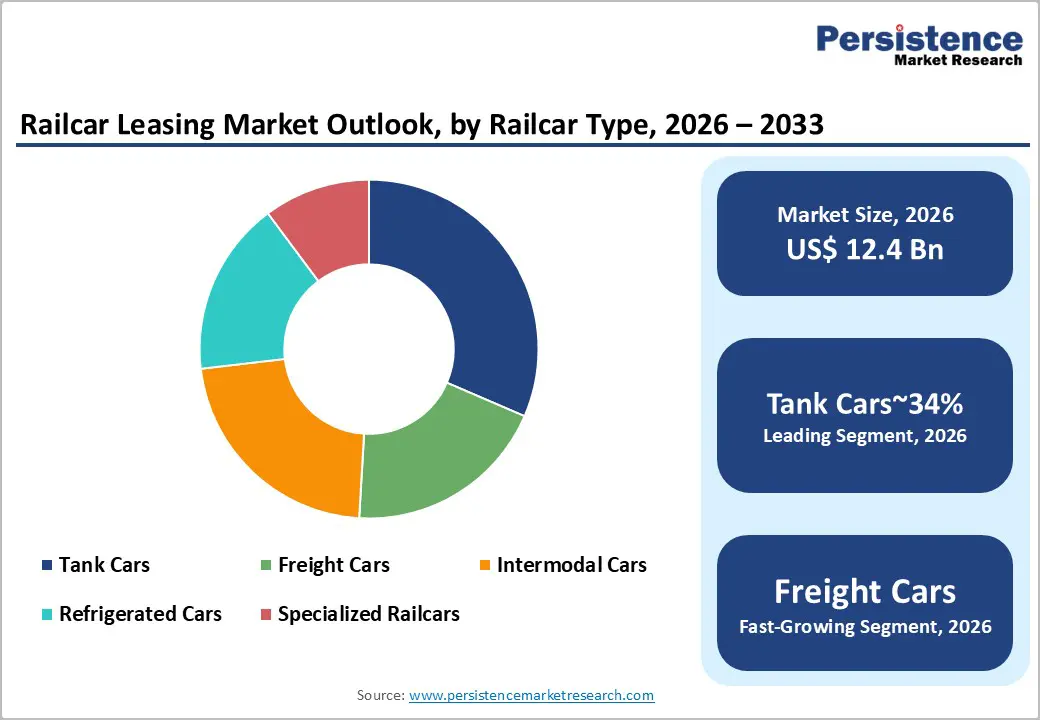

- Leading Segment: Tank Cars dominate the Railcar Type category with approximately 34% market share, driven by sustained demand from oil and gas, chemicals, and petrochemicals industries for compliant, specialized liquid bulk transportation solutions requiring long-term, full-service lease arrangements.

- Fastest-Growing Segment: Operating Lease is the fastest-growing and dominant lease structure, preferred by industrial shippers for its financial flexibility, off-balance-sheet characteristics, and ability to refresh fleet technology without capital commitment, particularly relevant amid evolving PHMSA and ERA safety compliance requirements.

- Key Opportunity: AFFF-site-equivalent chemical sector expansion, with the American Chemistry Council tracking over US$ 200 billion in announced U.S. chemical investment since 2010, creates a sustained, long-horizon opportunity for tank car lessors offering full-service, compliance-integrated fleet management to Tier 1 chemical producers globally.

| Key Insights | Details |

|---|---|

| Railcar Leasing Market Size (2026E) | US$ 12.4 Billion |

| Market Value Forecast (2033F) | US$ 17.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Rising Freight Rail Volumes and Shipper Preference for Capital-Efficient Fleet Access

The steady rise in freight rail activity across major industrial economies is driving consistent demand for leased railcar fleets. Industry data shows that freight volumes remain strong, with millions of carloads and additional intermodal units transported annually. Industrial shippers, including chemical manufacturers, agricultural exporters, and energy companies, are increasingly choosing leasing over ownership. This shift is primarily driven by the need for capital efficiency and operational flexibility.

Purchasing railcars requires significant upfront investment, typically ranging from US$ 80,000 to over US$ 200,000 per unit, depending on specifications. Leasing allows companies to avoid these large capital expenses while optimizing working capital and adapting quickly to fluctuating commodity cycles. As a result, leasing enables better financial discipline and scalability. These combined factors are creating a stable and long-term demand outlook for railcar leasing services across global markets.

Government Infrastructure Investment and Rail Modal Shift Policies Stimulating Fleet Demand

Government investments and policy initiatives aimed at strengthening rail infrastructure are creating strong growth momentum for the railcar leasing market. Large-scale funding programs are improving freight capacity, efficiency, and network reliability. For example, significant investments in rail infrastructure are supporting expansion projects and modernization efforts, directly boosting freight movement capabilities. In parallel, policy frameworks encouraging a shift from road to rail transport are gaining traction, especially in regions focused on reducing carbon emissions and improving logistics efficiency. These initiatives are pushing freight operators to expand their rail usage, increasing the need for additional rolling stock. In emerging markets, national rail expansion plans are further accelerating this transition by targeting higher freight modal share. As a result, leasing companies are benefiting from long-term contracts and predictable demand cycles, making government-backed infrastructure and policy support a key structural driver of market growth.

Restraints

Growing Railcar Manufacturing Costs and Extended Delivery Lead Times

Rising manufacturing costs are becoming a significant challenge for the railcar leasing market. The primary driver behind this increase is the volatility in steel prices, which accounts for a substantial portion of total production costs. In addition, supply chain disruptions have further intensified cost pressures and slowed down manufacturing processes. These challenges are reflected in rising industry price indices for rail equipment.

At the same time, extended delivery timelines from manufacturers are limiting the ability of leasing companies to quickly expand their fleets in response to rising demand. This creates a mismatch between supply and demand, especially during peak freight cycles. For new entrants, these barriers make it difficult to establish competitive fleet sizes. Overall, higher costs and delayed deliveries are restricting market expansion and reducing the agility of lessors in meeting customer requirements.

Regulatory Compliance and Safety Retrofit Mandates Increasing Operational Cost Burden

Strict safety and environmental regulations are adding to the operational cost burden for railcar lessors. Compliance requirements often involve upgrading or replacing older railcars to meet updated safety standards, particularly for transporting hazardous materials. These retrofit programs can be expensive, with costs per unit reaching significant levels depending on the type of upgrade required. Additionally, ongoing inspections, maintenance, and certification processes further increase lifecycle costs.

Regulatory bodies across different regions continue to introduce new standards, requiring continuous investment from fleet owners. These compliance activities can also temporarily reduce fleet availability, as railcars must be taken out of service for upgrades or inspections. As a result, lessors face both higher capital expenditure and operational challenges. This ongoing regulatory pressure makes fleet management more complex and impacts overall profitability within the leasing market.

Opportunities - Intermodal Freight Expansion and E-Commerce-Driven Containerized Cargo Growth

The rapid expansion of intermodal freight presents a major growth opportunity for the railcar leasing market. This trend is largely driven by the rise of e-commerce, evolving supply chain strategies, and ongoing shortages in long-haul trucking capacity. Intermodal transport, especially for distances exceeding 500 miles, is increasingly preferred due to its cost efficiency and reliability. As companies look for faster and more sustainable logistics solutions, rail is emerging as a strong alternative to road transport. At the same time, infrastructure investments in intermodal terminals are improving efficiency and capacity, further supporting this shift. The growing need for specialized equipment such as flatcars and double-stack platforms is creating new leasing opportunities. As demand continues to rise, leasing companies that focus on intermodal solutions are well-positioned to capture above-average growth and build long-term customer relationships.

Chemical and Petrochemical Sector Expansion Driving Long-Term Tank Car Lease Demand

The global expansion of the chemical and petrochemical industries is creating sustained demand for specialized tank car leasing. Major investments in production capacity, particularly in key industrial regions, are driving increased transportation needs for liquid bulk commodities. Each new facility or expansion project typically requires dedicated tank cars designed for specific chemical properties, including specialized coatings and pressure configurations.

These requirements make leasing a more practical option compared to ownership, especially for companies seeking flexibility and compliance support. Leasing providers that offer integrated services such as maintenance, regulatory compliance, and fleet management are gaining a competitive advantage. Additionally, long-term contracts associated with chemical transportation provide stable and predictable revenue streams. As global trade in chemicals continues to grow, tank car leasing is expected to remain a high-value and reliable segment within the broader market.

Category-wise Analysis

By Railcar Type Insights

Tank cars continue to lead the railcar leasing market, accounting for the largest share due to their critical role in transporting liquid commodities. Industries such as oil and gas, chemicals, and agriculture rely heavily on these railcars for both hazardous and non-hazardous materials. Tank cars are designed with specialized features to ensure safe handling, including pressure resistance and regulatory compliance standards.

Their widespread use across multiple industries makes them a core component of leasing portfolios. Additionally, tank cars typically command higher lease rates and are often leased under long-term agreements, ensuring stable revenue for lessors. The complexity involved in manufacturing and maintaining these railcars further discourages ownership, strengthening the preference for leasing. These factors collectively reinforce the dominance of tank cars as the most valuable and strategically important segment in the market.

By Lease Type Insights

Operating leases dominate the railcar leasing market as they provide flexibility and financial efficiency for customers. Under this model, companies can use railcars without taking ownership or bearing residual value risks. This is particularly beneficial for industries that experience fluctuating demand, such as energy, agriculture, and chemicals. Operating leases allow businesses to scale their fleet size based on market conditions and upgrade to newer equipment when needed.

Although accounting standards have evolved, the fundamental advantages of reduced capital commitment and operational flexibility remain strong. Lessors also benefit by retaining ownership and managing asset utilization across multiple lease cycles. This arrangement creates a win-win situation for both parties. As a result, operating leases continue to be the preferred structure, supporting their leading position in the market.

By Cargo Type Insights

Liquid bulk remains the largest cargo segment in the railcar leasing market due to its extensive use across energy and chemical industries. Commodities such as crude oil, refined fuels, ethanol, and industrial chemicals require specialized tank cars for safe and efficient transportation. In many regions, rail plays a crucial role in moving these products, especially where pipeline infrastructure is limited. The consistent demand for these commodities ensures steady utilization of tank car fleets.

Additionally, regulatory requirements for transporting hazardous liquids further encourage companies to rely on leased equipment. Higher lease rates and specialized design requirements make liquid bulk transportation a high-revenue segment. With ongoing industrial activity and energy demand, this segment is expected to maintain its leading position in the market.

By End-user Insights

The oil and gas sector is the largest end-user in the railcar leasing market, driven by its continuous need for transporting crude oil, natural gas liquids, and refined products. Rail transport becomes especially important in regions where pipeline capacity is insufficient or unavailable. This creates strong demand for tank cars, particularly during periods of high production.

In addition, the movement of chemicals and materials used in oilfield operations further increases leasing requirements. The sector’s cyclical nature also makes leasing a more attractive option, as it allows companies to adjust capacity based on market conditions. These factors make oil and gas a key contributor to overall leasing demand. Its reliance on flexible and scalable logistics solutions ensures its continued dominance in the market.

Regional Insights

North America Railcar Leasing Market Trends

North America remains the leading region in the railcar leasing market, supported by a well-established freight rail network and a mature leasing ecosystem. The region benefits from strong private sector participation, with major leasing companies managing large and diverse fleets. Continuous infrastructure investments are improving rail capacity and efficiency, supporting higher freight volumes.

Regulatory frameworks also play a significant role in shaping leasing demand, particularly through safety standards and compliance requirements. Cross-border trade between the U.S., Canada, and Mexico further strengthens the market, with integrated rail networks supporting seamless logistics. Additionally, nearshoring trends are increasing manufacturing activity in Mexico, driving demand for leased railcars. These combined factors position North America as a stable and dominant market with long-term growth potential.

Europe Railcar Leasing Market Trends

Europe represents the second-largest market, driven by strong regulatory support for rail freight expansion. Policies focused on sustainability and emission reduction are encouraging a shift from road to rail transport. This is increasing demand for leased railcars across the region. Harmonization of rail standards is also improving cross-border operations, making it easier for leasing companies to operate efficiently.

Major economies continue to invest in rail infrastructure, supporting freight growth. At the same time, environmental regulations are enhancing rail’s competitiveness compared to trucking. The combination of policy support, infrastructure development, and sustainability goals is creating a favorable environment for leasing companies. As a result, Europe continues to offer strong growth opportunities for market participants.

Asia Pacific Railcar Leasing Market Trends

Asia Pacific is the fastest-growing region in the railcar leasing market, driven by rapid industrialization and large-scale rail investments. Governments are actively expanding rail networks to improve freight efficiency and reduce logistics costs. In several countries, there is a gradual shift from ownership to leasing models, creating new opportunities for market growth.

Major economies are investing heavily in freight corridors and infrastructure upgrades, supporting higher capacity and faster operations. Additionally, growing manufacturing activity and export demand are increasing the need for efficient rail transport solutions. Emerging markets are also gaining attention as potential growth hubs. These factors collectively position Asia Pacific as a high-growth region with strong long-term potential for railcar leasing.

Competitive Landscape

The global railcar leasing market shows moderate consolidation in developed regions, while remaining more fragmented in emerging markets. Leading companies compete based on fleet size, service capabilities, and geographic reach. Many players are expanding their offerings by integrating maintenance, compliance, and fleet management services into their leasing models. Strategic initiatives such as acquisitions, partnerships, and vertical integration are shaping the competitive landscape.

Additionally, digital technologies are being adopted to improve fleet utilization and operational efficiency. New business models focusing on flexible leasing options and data-driven decision-making are gaining traction. Sustainability is also becoming an important factor, with companies exploring environmentally friendly leasing solutions. These evolving strategies are helping market leaders strengthen their position while creating opportunities for innovation and differentiation.

Key Developments:

- In January 2025: GATX Corporation reported a record lease pricing environment, with renewal rates exceeding expiring contracts across multiple railcar categories. This reflects tight fleet availability and strong industrial demand, highlighting favorable market conditions for lessors.

- In September 2024: The Greenbrier Companies secured multi-year manufacturing and leasing agreements covering over 4,500 railcars with major North American railroads and shippers, strengthening its vertically integrated model and reinforcing its competitive positioning in fleet expansion.

- In March 2023: VTG AG, backed by Morgan Stanley Infrastructure Partners, announced a strategic fleet expansion focused on chemical and liquid bulk tank wagons in Europe, aligning growth with EU rail freight policies and increasing demand for sustainable transport solutions.

Companies Covered in Railcar Leasing Market

- GATX Corporation

- TrinityRail

- Wells Fargo Rail

- SMBC Rail Services

- Union Tank Car Company

- The Greenbrier Companies

- VTG AG

- Ermewa Group

- Touax Rail

- Mitsui Rail Capital

- CIT Rail

- Chicago Freight Car Leasing Company

- Progress Rail Leasing

- Andersons Rail Group

- Wascosa AG

- TTX Company

- RAIL Management Corp.

- Infinity Rail

- First Wagon Leasing

- Nacco

Frequently Asked Questions

The global Railcar Leasing market is estimated to be valued at US$ 12.4 Billion in 2026 and is projected to reach US$ 17.9 Billion by 2033, expanding at a compound annual growth rate (CAGR) of 5.4% during the forecast period. The historical CAGR for the period 2020-2025 stood at 4.8%, reflecting sustained demand from industrial freight shippers and energy sector operators.

The primary demand drivers include the U.S. Bipartisan Infrastructure Law's US$ 66 billion rail investment commitment, the European Commission's target of a 50% increase in rail freight by 2030, and the capital-efficiency advantages of leasing over ownership, particularly relevant as new railcar acquisition costs range from US$ 80,000 to over US$ 200,000 per unit, compelling industrial operators in oil and gas, chemicals, and agriculture to prefer leased fleet access over direct capital investment.

Tank Cars represent the leading Railcar Type segment, holding approximately 34% of total market share. Their dominance is driven by sustained demand from the oil and gas, chemicals, and petrochemicals sectors for specialized liquid bulk transportation, supported by stringent PHMSA and AAR regulatory standards that make long-term full-service leasing the preferred fleet access model over outright ownership for most industrial shippers.

North America is the dominant regional market, led by the United States, which hosts the world's largest private freight rail network exceeding 140,000 route miles according to the Association of American Railroads (AAR). The region benefits from a mature private railcar leasing ecosystem, strong regulatory frameworks enforced by the Surface Transportation Board (STB) and PHMSA, and accelerating federal rail infrastructure investment under the Bipartisan Infrastructure Law of 2021.

The most compelling opportunity lies in the intersection of intermodal freight expansion and chemical sector fleet growth. The chronic truck driver shortage, estimated at over 60,000 drivers by the American Trucking Associations (ATA), is accelerating modal shift to intermodal rail, while the American Chemistry Council's tracking of over US$ 200 billion in announced U.S. chemical investment is generating long-term, high-value tank car lease demand from Tier 1 chemical producers requiring full-service, compliance-integrated fleet management solutions.

The global railcar leasing market is served by prominent players including GATX Corporation, TrinityRail, Wells Fargo Rail, SMBC Rail Services, Union Tank Car Company, The Greenbrier Companies, VTG AG, Ermewa Group, Touax Rail, Mitsui Rail Capital, CIT Rail, Chicago Freight Car Leasing Company, Progress Rail Leasing, Andersons Rail Group, and Wascosa AG, among other regional and specialist leasing operators.