- Metalworking & Fabrication

- Powder Coating Equipment Market

Powder Coating Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Powder Coating Equipment Market by Powder Coating Equipment (Powder Coat Guns, Ovens & Curing Systems, Powder Coating Booths & Systems, Auxiliary & Ancillary Equipment, Misc.), Industry (Automotive & Transportation, Appliances & Consumer Electronics, Architectural & Construction, General Industrial / Machinery, Furniture & Home Décor, Misc.), and Regional Analysis for 2026 - 2033

Powder Coating Equipment Market Size and Trends Analysis

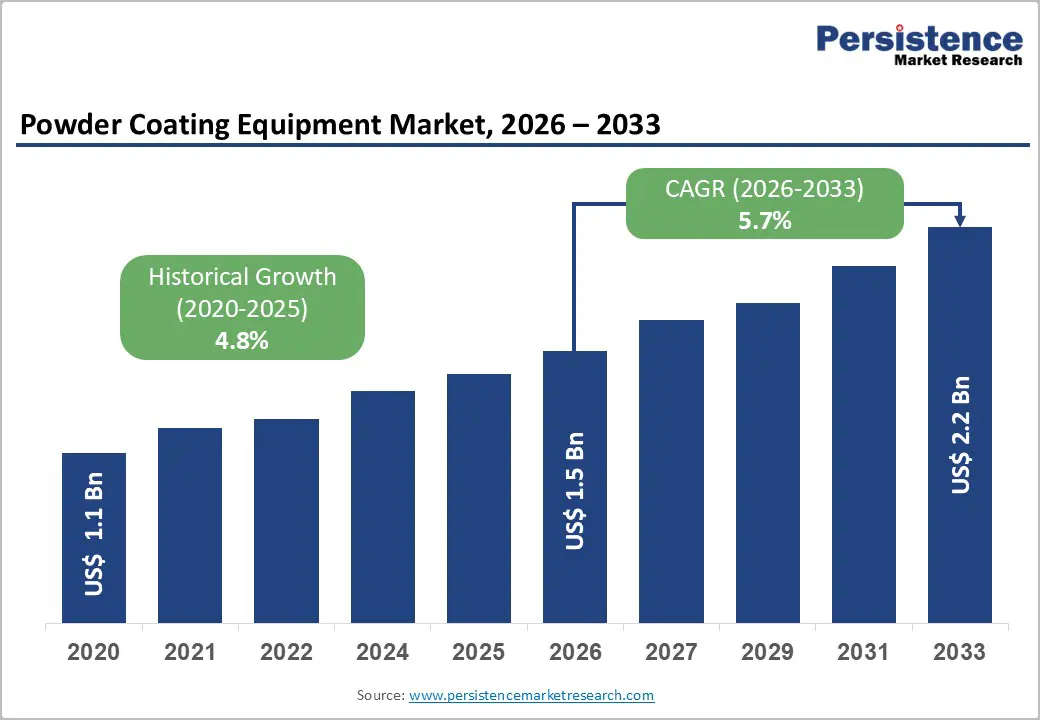

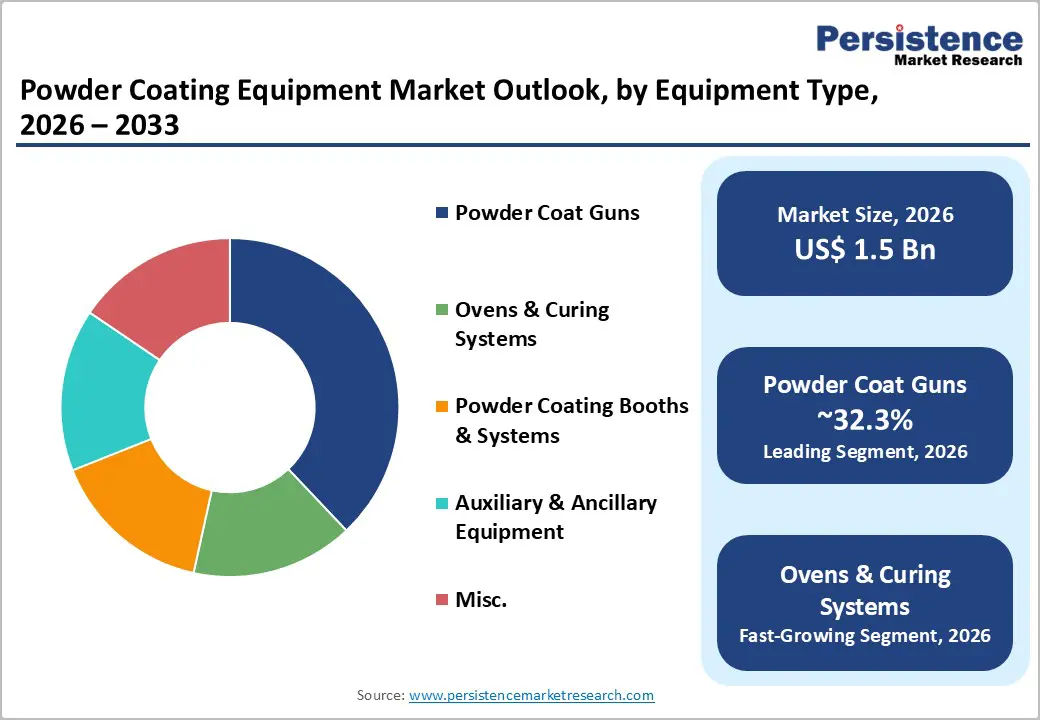

The global powder coating equipment market size is likely to be valued at US$ 1.5 billion in 2026 and is projected to reach US$ 2.2 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

This expansion reflects fundamental structural demand from automotive electrification trends, accelerating electronics manufacturing capacity in emerging markets, and regulatory imperatives favouring volatile organic compound (VOC) reduction that position powder coating as a preferred technology across industrial finishing applications.

The market growth trajectory balances maturation in developed economies with rapid industrialisation and infrastructure expansion in the Asia-Pacific and emerging markets, combined with technological convergence toward Industry 4.0 integration, including Internet of Things sensor networks, predictive maintenance capabilities, and data-driven process optimisation driving equipment adoption across automotive, appliances, construction, and general industrial sectors.

Key Industry?Highlights:

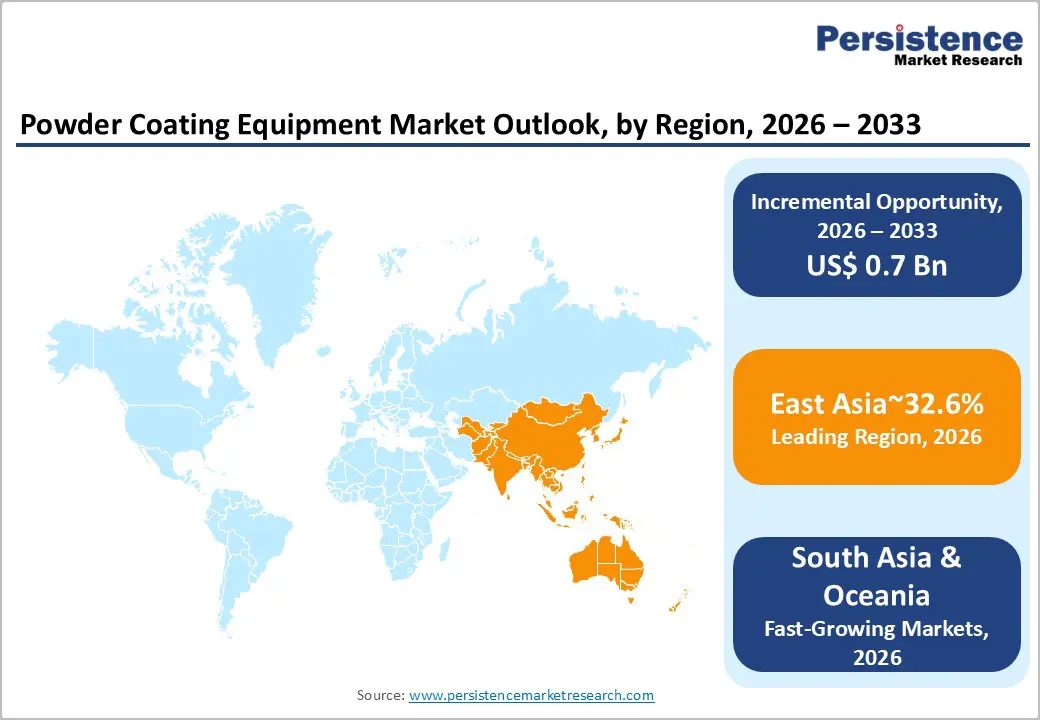

- Leading Region: East Asia leads the global powder coating equipment market with 32.6% share, supported by large-scale manufacturing bases, appliance production, and export-oriented electronics growth.

- Fastest-Growing Region: South Asia & Oceania emerges as the fastest-growing regional cluster, driven by India’s rapidly expanding electronics ecosystem and rising appliance and consumer-goods production.

- Leading Equipment Category: Powder Coated Guns dominate with 32.3% market share, reflecting their core role across manual operations, automated lines, and robotic spray systems.

- Fastest-Growing Equipment Category: Ovens & Curing Systems represent the fastest-growing segment, fueled by infrared, UV, and hybrid curing innovations that reduce cycle times and energy consumption.

- Leading End-user: Automotive & Transportation holds the largest end-use share at 30.6%, supported by corrosion-resistant component finishing and rising EV-related coating requirements.

- Fastest-Growing End-user: Appliances & Consumer Electronics is the fastest-growing application, boosted by India’s electronics manufacturing expansion and global demand for durable, premium finishes.

| Key Insights | Details |

|---|---|

| Powder Coating Equipment Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Drivers - Regulatory Transition Toward Volatile Organic Compound Reduction and Environmental Compliance

Environmental regulatory frameworks that prioritise VOC emissions reduction drive the expansion of the powder coating equipment market, as equipment specifications support compliance with increasingly stringent standards. The European Union REACH regulation establishes ≤35 grams per cubic meter VOC limits for industrial coatings, effective July 2024, while China's GB 37824 standard mandates ≤50 grams per cubic meter for automotive coatings, enforced January 2024, thereby establishing mandatory equipment specifications supporting low-VOC formulation application.

The U.S. Environmental Protection Agency's greenhouse gas reporting protocol requires mandatory emissions quantification for facilities exceeding 25,000 tonnes CO2-equivalent thresholds, creating operational incentives for powder coating adoption over solvent-based alternatives, generating superior compliance documentation and reducing reporting burden. Clean Air Act Title V permitting requirements for particulate matter emissions drive equipment manufacturers to innovate filtration systems, spray booth design optimisation, and recovery mechanism advancement, thereby enhancing operational compliance and reducing facility permitting complexity.

Regulatory pressure extends beyond equipment compliance to manufacturing process sustainability: facilities operating under the Resource Conservation and Recovery Act hazardous waste management requirements benefit from powder coating's characterization as non-hazardous under most jurisdictional frameworks, thereby reducing waste disposal costs and administrative burden relative to solvent-based coating systems.

The growth of the powder coating equipment market reflects this regulatory transition, as manufacturers upgrade coating systems from legacy liquid-spray infrastructure to compliant powder systems, enabling facility-wide emissions reductions and simplified environmental permitting trajectories.

Electronics Manufacturing Expansion and Appliance Production Intensification

Accelerating electronics and appliance manufacturing capacity in emerging markets is a critical driver of the powder coating equipment market, particularly India's electronics industry expansion from US$ 29 billion in FY15 to US$ 101 billion in FY23, which accounts for 3.4 percent of GDP. India's electronics manufacturing sector projects expansion from US$ 75 billion in FY21 to US$ 300 billion by FY26, supported by US$ 17 billion in Production Linked Incentive scheme allocations across semiconductors, smartphones, IT hardware, and components, thereby generating substantial new manufacturing facility construction and equipment capital expenditure demand.

Mobile phone production expanded 21-fold to reach US$49.3 billion over the past decade, positioning India as the second-largest global manufacturer after China. Electronics exports reached US$29.12 billion in FY24, a 23.6% year-over-year increase, with the largest share directed to South Asia, Africa, and the Middle East.

The appliances and consumer electronics segment, representing the fastest-growing equipment category, demonstrates equipment demand intensity as manufacturers prioritise aesthetic finishes, corrosion protection, and thermal durability, supporting export market competitiveness and premium product positioning.

Specialised coating requirements for heat-sensitive electronic components drive demand for advanced curing ovens with precise thermal control, resulting in the fastest-growing equipment category within the powder coating equipment market. Consumer demand for durable, aesthetically superior appliances mandates equipment capable of delivering consistent, high-quality finishes across high-volume production environments.

Restraint - High Capital Investment Requirements and Complex Installation Protocols

Powder coating equipment systems require substantial capital investment, with complete turnkey systems potentially exceeding US$500,000 for high-volume automated installations, creating barriers, particularly for small and medium-sized manufacturers in emerging markets operating under capital constraints.

Installation complexity encompasses spray booth design optimization, ventilation system integration, waste-recovery mechanism installation, and curing-oven thermal profiling, which require specialized engineering expertise and extended commissioning timelines, particularly in manufacturing environments and during the retrofitting of legacy facilities. This complexity restricts equipment adoption among manufacturers that lack technical infrastructure for equipment maintenance, process optimization, and operator training, creating adoption friction in price-sensitive developing markets where liquid spray systems remain economically preferred despite higher lifecycle operational costs and environmental compliance burdens.

Opportunities - Advanced Curing Oven Technology and Thermal Process Innovation

Thermal management innovation within powder coating curing systems represents high-growth opportunity as manufacturers develop infrared, ultraviolet, and hybrid curing technologies enabling accelerated production cycles, reduced energy consumption, and expanded substrate material compatibility. Ovens & Curing Systems are the fastest-growing equipment category, driven by technological advancements that enable faster curing protocols, reduce production cycle time, enhance throughput efficiency, and provide competitive advantages in high-volume manufacturing environments.

Innovation pathways include infrared radiation curing, reducing cycle times by 30-50 percent compared to conventional convection ovens, ultraviolet polymerisation enabling room-temperature curing of specialised powder formulations supporting temperature-sensitive substrates, and hybrid systems optimising energy efficiency through strategic heating method combination.

The market expansion of advanced curing technology addresses manufacturers' requirements for accelerating production cycles, supporting just-in-time manufacturing protocols, reducing inventory carrying costs, and improving operational capital efficiency.

Emerging thermal management technologies, combined with Industry 4.0 integration that enables predictive maintenance, real-time temperature monitoring, and automated process optimisation, position advanced curing systems as strategic investment opportunities for manufacturers prioritising operational excellence and cost-structure optimisation in high-volume production environments.

Automation Integration and Robotic Spray System Deployment

Roboticized powder-coating application systems represent an emerging category of opportunity as manufacturers prioritize labor efficiency, improved coating consistency, and management of geometric complexity through automated spray positioning, precision gun control, and advanced coating-parameter optimisation.

Automation integration reduces operational labour requirements by 40-60 percent in high-volume production environments while simultaneously enhancing coating quality, reducing material waste through optimized powder deposition, and improving worker safety by eliminating hazardous spray environment exposure.

The Market opportunity encompasses specialized robotic integration platforms supporting modular deployment across existing manufacturing infrastructure, collaborative robot systems enabling human-equipment interaction in flexible production environments, and advanced vision systems enabling real-time coating quality assurance and process parameter adjustment.

Industry 4.0 convergence enables integrated manufacturing execution systems coordinating spray automation with material handling, quality control inspection, and production scheduling, creating systemic efficiency advantages justifying capital investment in automated coating systems across appliances, automotive, and consumer electronics manufacturing.

Robot integration, particularly in the appliance and consumer electronics segments, addresses requirements for aesthetic finish quality and coating consistency, supporting premium market positioning and export competitiveness, and positions automation as a strategic platform for manufacturers targeting high-growth Asian and emerging markets that require scale and precision within cost-constrained manufacturing environments.

Category-wise Analysis

Equipment Type Insights

Powder-coated guns maintain market leadership at 32.3% share in 2026, reflecting a foundational role in coating application and ongoing design innovation addressing precision requirements, user interface improvement, and operational efficiency enhancement across manual and automated systems. Spray gun design evolution emphasises electrostatic charging optimization improving powder particles transfer efficiency to substrates, reducing material waste through enhanced deposition precision, and minimising powder cloud formation within spray booth environments.

Advanced gun designs, including variable voltage control, adjustable fan patterns, and ergonomic weight distribution, enhance operator productivity in manual coating applications while reducing fatigue-related quality variance.

WAGNER's April 2024 launch of the Sprint 2 manual powder coating unit featuring Digital Surface Optimiser and Air Flow Control technology exemplifies product innovation trajectory, delivering homogeneous high-quality finishes on complex geometries while reducing overcharge effects and streamlining rapid colour changes through Quick-Link injectors. PPG's October 2025 introduction of ENVIROCRON® Extreme Protection Edge Plus patent-pending one-coat solution enhances edge coverage and corrosion resistance through reduced powder retraction and orange-peel texture minimisation, demonstrating continued innovation within gun technology, addressing industry-specific performance requirements.

Ovens and curing systems are the fastest-growing equipment category, driven by advances in thermal management technology, improvements in energy efficiency, and requirements to accelerate production cycles. Nordson's Dynamic Contouring Movers system, integrated with HDLV soft spray technology and the Nordson PowderPilot™ HD controller, exemplifies advanced curing-system sophistication, enabling automatic coverage of complex product geometries and precise thermal process control.

Specialised curing technologies, including infrared radiation systems that enable 30-50 percent reduction in cycle time, ultraviolet polymerisation to support temperature-sensitive substrate compatibility, and hybrid thermal systems that optimise energy consumption, drive equipment adoption as manufacturers prioritise production acceleration and operational cost reduction.

Industry Insights

Automotive and transportation applications command 30.6 percent of market share in 2026, reflecting the industry's critical requirement for durable, corrosion-resistant finishes protecting vehicle components across diverse environmental and operational stresses.

Electric vehicle component coating requirements, including battery housings, thermal management systems, and power electronics enclosures, drive demand for specialised equipment to optimise thermal profiles and ensure precise coating conformity, supporting component performance specifications. Global car production reached 75.5 million units in 2024, with China contributing 46 million units, underscoring continued manufacturing intensity and the need for consistent, high-quality coating systems to support production targets and export market competitiveness.

The automotive segment reflects capital-intensive equipment deployment, particularly roboticized systems addressing the geometric complexity of modern vehicle components and aesthetic finish requirements supporting premium market positioning.

Equipment manufacturers prioritise automotive sector development through specialised gun-coating designs, thermal management systems that meet the requirements of sensitive components, and automation integration to address the high-volume production demands characteristic of global automotive supply chains. North America's automotive equipment investment, coupled with continued German, Italian, and Spanish manufacturing activity, sustains steady demand for powder coating systems, supporting OEM production targets and supplier network expansion for coating outsourcing.

Appliances and consumer electronics are the fastest-growing end-use category, driven by India's electronics manufacturing expansion to US$ 300 billion by FY26, alongside global consumer preferences for aesthetic durability and sustainable product finishes.

Specialized coating requirements for heat-sensitive components, aesthetic surface requirements that support premium positioning, and export market compliance with international corrosion resistance standards drive equipment adoption among appliance manufacturers and consumer electronics component suppliers.

Regional Insights and Trends

North America Powder Coating Equipment Market Trends

North America represents the largest powder coating equipment market, accounting for 27% of global value, characterised by established automotive and aerospace manufacturing infrastructure, sophisticated equipment specifications, and strong environmental compliance emphasis.

The United States dominates regional activity with a dominant automotive sector presence, including Tesla, General Motors, Ford, and Stellantis operations, supported by 3.8 percent automotive production growth in 2024, creating sustained demand for coating equipment supporting OEM production targets and supplier network requirements.

U.S. construction sector spending reached $2.2 trillion in 2024, representing 4.5 percent of GDP, supporting 8.2 million workers across 3.7 million construction businesses, driving architectural and construction coating equipment demand for structural steel protection, architectural metalwork finishes, and construction component durability.

Federal government initiatives prioritising energy-efficient manufacturing through Department of Energy programs and EPA emphasis on VOC-free coating solutions reinforce market preference for powder coating adoption, supporting equipment manufacturer expansion.

The region demonstrates the highest sophistication of contractors, advanced digital system integration capability, and a strong preference for Industry 4.0-enabled equipment featuring predictive maintenance, real-time process monitoring, and data analytics integration supporting operational excellence and competitive manufacturing positioning.

East Asia Powder Coating Equipment Market Trends

East Asia accounts for 32.6% of the global powder coating equipment market value, driven by China's dominant manufacturing position and India's rapid expansion of the electronics and appliances sector. China's industrial base encompasses automotive manufacturing, electronics component production, appliance fabrication, and infrastructure development, supporting sustained equipment demand. Government initiatives that promote environmental compliance and sustainable manufacturing practices accelerate the adoption of powder coating over solvent-based alternatives.

India's electronics industry is projected to expand to US$101 billion in FY23, and the manufacturing sector's projected to reach US$300 billion by FY26, creating substantial new equipment capital expenditure demand as facilities establish coating infrastructure to support production targets. Mobile phone manufacturing, IT hardware production, and consumer electronics assembly drive equipment adoption across tier-one and tier-two manufacturers, supporting export market participation and domestic consumption growth. Government support through Production Linked Incentive schemes allocating US$17 billion across semiconductors, smartphones, IT hardware, and components creates policy incentives for capital investment in modern manufacturing infrastructure, including powder-coating systems.

Europe Powder Coating Equipment Market

Europe is likely to account for a considerable share in 2026, characterised by strong environmental compliance requirements, sophisticated equipment specifications, and automotive manufacturing concentration among premium brands, including BMW, Mercedes-Benz, Volkswagen, and Stellantis. European automotive manufacturers prioritise the adoption of powder coating for electric-vehicle component protection and aesthetic finishes that support premium brand positioning, thereby driving demand for specialised equipment for thermal management, precise application, and quality assurance.

The EU regulatory framework, emphasising VOC reduction and environmental compliance, including REACH regulations establishing ≤35 g/m³ industrial coating limits effective July 2024, drives equipment specifications that support the application of low-emission formulations. The European construction sector, despite modest growth, maintains steady equipment demand driven by architectural metalwork, structural steel protection, and building component durability requirements, thereby supporting the construction industry supply chain. Strategic corporate developments, including Gema's August 2024 relocation to the new Gossau facility, which features expanded production capacity, four state-of-the-art coating lines, and enhanced R&D capabilities, and underscore regional manufacturers' commitment to technological leadership and to capacity expansion supporting continued market growth.

Competitive Landscape

The global powder coating equipment market is moderately consolidated, dominated by a few major players, while smaller regional manufacturers serve niche markets. Leading companies such as Nordson Corporation, Gema Switzerland GmbH, Wagner Group, PPG Industries, ECKART GmbH, and Eastwood Company hold significant market share through advanced technology, automation solutions, and robust after-sales services.

The market is driven by innovations in robotic systems, digital controllers, and energy-efficient equipment, catering to automotive, industrial, and architectural applications. While top players secure large OEM and industrial contracts, regional players focus on cost-effective, customizable solutions for SMEs. Strategic expansions, R&D investments, and partnerships help market leaders maintain technological leadership and global reach.

Key Developments:

- In January 2026, ECKART launched STANDART PCS HD, a new non-leafing aluminium pigment specifically designed for powder coating applications. The product provides high metallic brilliance, improved coverage, and up to 30% pigment savings, thereby enhancing efficiency and visual quality in industrial powder coating processes. It supports diverse applications such as furniture and household appliances and is compatible with existing powder coating equipment, reflecting the market’s shift toward high-performance, cost-efficient, and visually superior coating solutions.

- In October 2025, PPG launched the PPG ENVIROCRON® Extreme Protection Edge Plus powder coating, a patent-pending one-coat solution designed to enhance edge coverage and corrosion resistance. The innovation reduces powder retraction and orange-peel texture, providing smoother finishes on complex metal parts. It is compatible with both manual and automated powder coating systems, reflecting growing demand for advanced coatings that optimise performance, efficiency, and durability in industrial and heavy-duty applications.

Companies Covered in Powder Coating Equipment Market

- Nordson Corporation

- Gema Switzerland GmbH

- WAGNER

- ANEST IWATA Corporation

- Carlisle

- Hangzhou Color Powder Coating Equipment Co., Ltd.

- Mitsuba Systems Pvt. Ltd.

- Statfield Equipment Pvt. Ltd.

- SAMES KREMLIN

- Eastwood Company

- Parker Ionics

- Red Line Industries Ltd

- Reliant Finishing Systems

- Pittsburgh Spray Equipment Co.

Frequently Asked Questions

The global powder coating equipment market is projected to be valued at US$ 1.5 Bn in 2026.

The powder coating equipment market is expected to witness a CAGR of 5.7% from 2026 to 2033.

The powder coat guns is expected to account for approximately 32.3% of the global market.

The powder coating equipment market growth is driven by tightening global VOC and environmental compliance regulations alongside accelerating electronics and appliance manufacturing expansion that boosts demand for compliant, high-performance coating systems.