- Specialty & Fine Chemicals

- Polyfluoroalkyl Substances (PFAS) Waste Management Market

Polyfluoroalkyl Substances (PFAS) Waste Management Market Size, Share, and Growth Forecast 2026 - 2033

Polyfluoroalkyl Substances (PFAS) Waste Management Market by Waste Type (PFAS-Contaminated Water, PFAS-Contaminated Soil, PFAS-Contaminated Sludge/Biosolids, Landfill Leachate, Firefighting Foam Residues, Industrial Process Waste), by Treatment Technology, by End-User, by Regional Analysis, 2026 - 2033

Polyfluoroalkyl Substances (PFAS) Waste Management Market Size and Trend Analysis

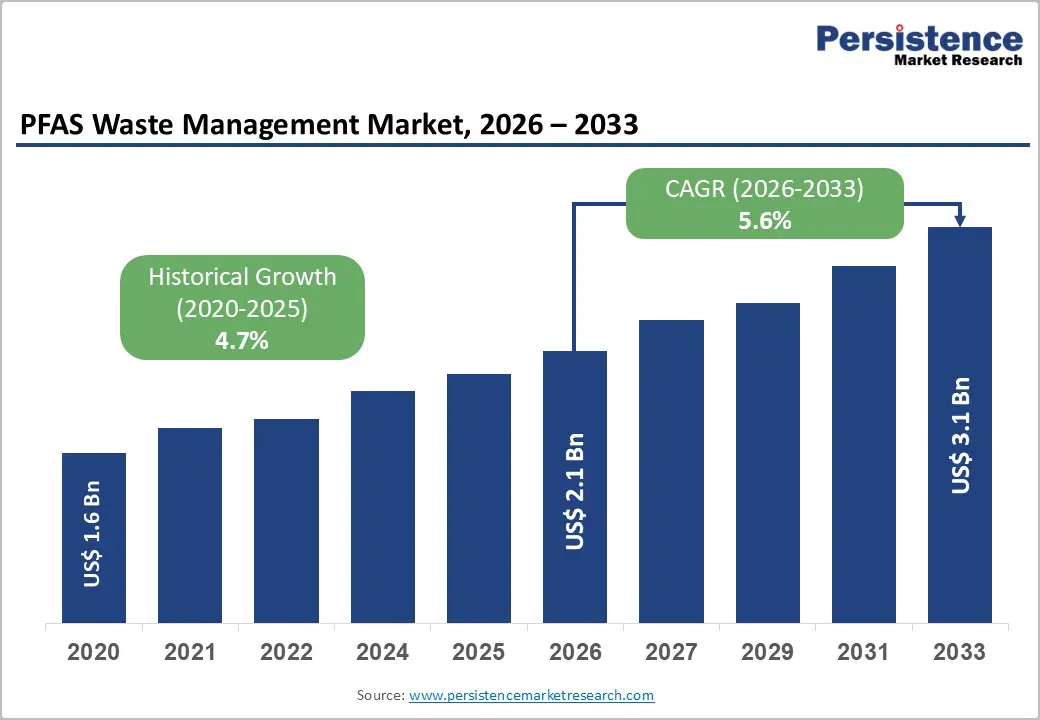

The global polyfluoroalkyl substances (PFAS) waste management market size is likely to be valued at US$ 2.1 Billion in 2026 and is expected to reach US$ 3.1 Billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033. The rise in regulatory mandates from governments and environmental agencies worldwide, combined with the accelerating discovery of widespread PFAS contamination across drinking water supplies, soil, and industrial waste streams, are the primary forces driving sustained demand.

Key Industry Highlights:

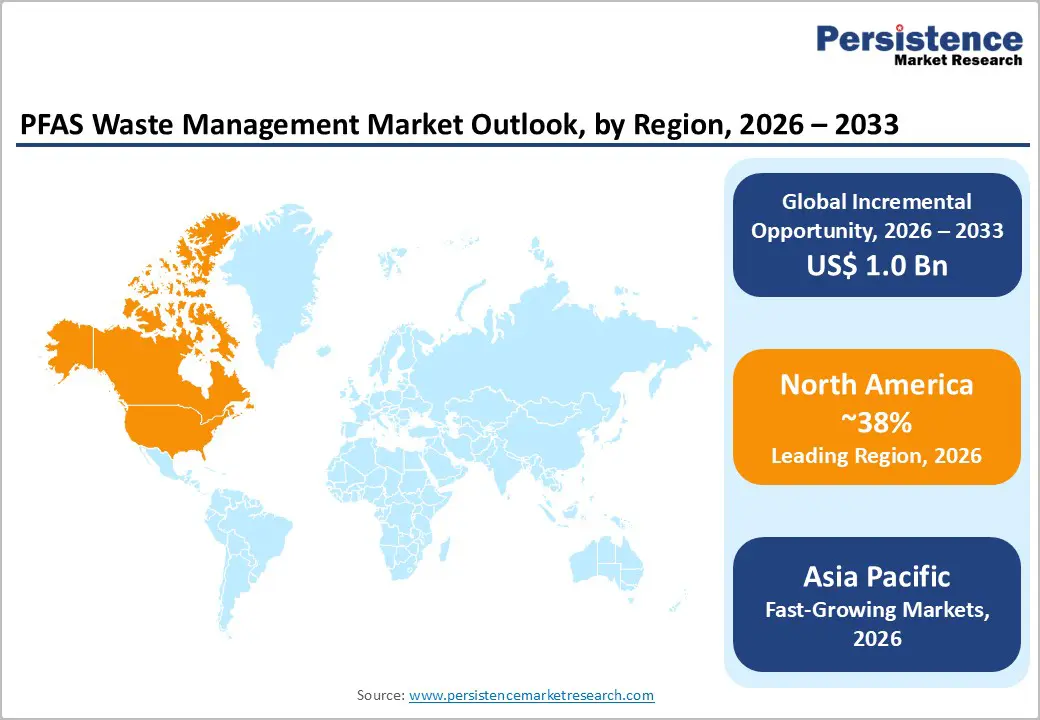

- Leading Region: North America leads the global PFAS Waste Management market holding 38% share, underpinned by the U.S. EPA's enforceable 4 ppt drinking water limits, CERCLA hazardous substance designations, and the U.S. government's $10 Billion remediation allocation in 2024.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 7.2%, driven by China's position as the world's largest fluorochemical manufacturer, documented PFAS contamination hotspots, escalating regulatory frameworks in Japan and India, and growing ASEAN multinational supply chain compliance pressure.

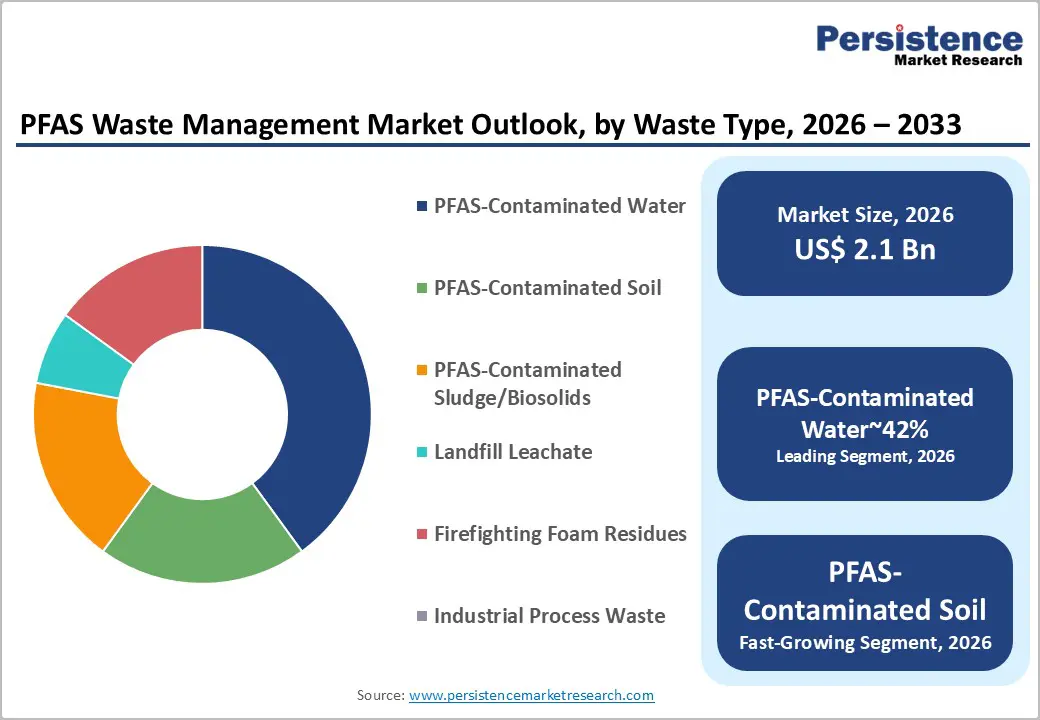

- Leading Segment: PFAS-Contaminated Water dominates the By Waste Type category with approximately 40% market share, driven by enforceable EPA and EU drinking water regulations, an estimated 70 million Americans with PFAS in drinking water, and the global breadth of contamination confirmed in 45,000+ water samples.

- Fastest-Growing Segment: Thermal Destruction Technologies represent the fastest-growing treatment segment, as regulatory mandates for >99.9% destruction efficiency, demonstrated by Veolia at Port Arthur, Texas in 2025, shift institutional preference from adsorption-based containment toward permanent mineralization solutions.

- Key Opportunity: AFFF firefighting foam remediation represents the single largest near-term market opportunity, anchored by the $13.5 Billion combined 3M and DuPont settlement fund, U.S. DoD multi-year cleanup programs at contaminated military installations, and expanding international AFFF remediation mandates in Germany, UK, and Australia.

| Key Insights | Details |

|---|---|

| PFAS Waste Management Market Size (2026E) | US$ 2.1 Billion |

| Market Value Forecast (2033F) | US$ 3.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.7% |

Market Dynamics

Drivers - Stringent Regulatory Frameworks and Hazardous Substance Designations

The tightening regulatory landscape around PFAS is currently the strongest growth driver for the global PFAS Waste Management market. In April 2024, the U.S. Environmental Protection Agency (EPA) finalized the first enforceable National Primary Drinking Water Regulation for PFAS, setting an extremely low maximum contaminant level of 4 parts per trillion (ppt) for both PFOA and PFOS. These limits are among the strictest anywhere in the world. At the same time, the EPA released its Updated Interim Guidance on PFAS Destruction and Disposal (2024), which provides clear direction on high-efficiency destruction technologies.

In Europe, regulatory pressure is also increasing. The European Chemicals Agency (ECHA) revised its REACH restriction proposal, covering more than 10,000 PFAS chemicals. Once implemented, these regulations will require extensive remediation efforts across EU member states. As a result, municipalities, industrial facilities, and defense organizations are increasingly required to invest in PFAS waste treatment solutions, creating a rapidly expanding pipeline of mandatory remediation projects worldwide.

Escalating Scope of PFAS Contamination in Drinking Water and Groundwater

The growing scale of PFAS contamination across global water systems is creating strong and consistent demand for PFAS waste management solutions. A peer-reviewed study published in Nature Geoscience in 2024 analyzed more than 45,000 water samples worldwide and found that 31% of groundwater samples exceeded proposed U.S. EPA threshold limits, even in areas without known pollution sources. In the United States alone, the EPA estimates that nearly 70 million people have detectable levels of PFAS in their drinking water.

A 2023 study revealed that PFAS compounds were present in at least 45% of drinking water samples taken from both private wells and public tap water systems. Further research by the U.S. Geological Survey found measurable PFAS contamination in 76% of rivers and streams tested in Pennsylvania. This widespread contamination across municipal water systems, industrial sites, military installations, and landfills is generating a large and long-term demand for remediation services and treatment infrastructure globally.

Restraints - High Cost and Technical Complexity of PFAS Destruction

One of the main challenges in the PFAS Waste Management market is the high cost and technical complexity involved in effectively destroying PFAS compounds. To meet regulatory requirements in several regions, destruction technologies must achieve more than 99.9% efficiency, which requires highly advanced treatment methods. Thermal destruction processes, such as high-temperature incineration above 1,100°C, are currently considered one of the most reliable solutions. However, these systems require significant capital investment and specialized infrastructure.

Clean Harbors invested heavily in a PFAS incineration facility in Kimball, Nebraska, which was commissioned in December 2024. Analysts expect the facility to take approximately 12 to 18 months before reaching full operational profitability. Such large investments create financial barriers, especially for smaller municipalities and industrial operators that may struggle to fund advanced treatment systems. As a result, the high cost of implementing and maintaining effective PFAS destruction technologies continues to slow broader adoption and limits the pace of overall market growth.

Uncertainty Over Long-Term Regulatory Implementation

Although regulatory pressure on PFAS is increasing globally, differences in implementation timelines and regulatory definitions create uncertainty for companies operating in the PFAS waste management sector. In Europe, the proposed REACH restriction includes transition periods ranging from five to twelve years for different industrial applications. These long timelines allow industries additional time to adapt, but also delay immediate remediation requirements in several sectors. In the United States, regulators are still considering proposals to classify additional PFAS compounds as hazardous waste under the Resource Conservation and Recovery Act (RCRA).

The waste management companies face uncertainty about the future scope of regulated waste streams owing to indecisiveness. This lack of regulatory clarity makes long-term planning difficult for service providers and investors. Companies may hesitate to expand treatment capacity or invest in specialized infrastructure until clearer regulatory frameworks are established, which ultimately slows the scaling of PFAS treatment facilities and workforce development.

Opportunities - Thermal Destruction Technologies as a High-Growth Commercial Frontier

Thermal destruction technologies represent one of the most promising opportunities in the PFAS Waste Management market. These technologies are capable of breaking down PFAS molecules completely, eliminating the long-term environmental risk associated with these “forever chemicals.” Unlike adsorption-based methods that only capture PFAS temporarily, thermal destruction can permanently mineralize the compounds. Recognizing this capability, the U.S. Environmental Protection Agency’s 2024 Updated Interim Guidance identified thermal destruction as one of the few technologies capable of handling large volumes of PFAS waste at scale.

The commercial potential of this approach was highlighted in 2025 when Veolia Environnement published extensive testing results from its Port Arthur, Texas facility. The tests demonstrated destruction efficiencies exceeding 99.9% for Aqueous Film-Forming Foam (AFFF) waste while processing over 143,550 gallons annually. In addition, the U.S. government allocated approximately US$10 billion in 2024 for environmental remediation programs. As global regulators increasingly favor permanent destruction over containment strategies, companies providing advanced thermal treatment technologies are well positioned to secure high-value, long-term remediation contracts.

Firefighting Foam Residue Remediation as a Large-Scale Liability-Driven Opportunity

The cleanup of Aqueous Film-Forming Foam (AFFF) residues represents one of the largest remediation opportunities within the PFAS Waste Management market. AFFF has historically been used extensively at military bases, airports, and industrial fire-training facilities, making it a major source of PFAS contamination in soil and groundwater. In response to growing environmental concerns and legal pressure, major chemical manufacturers have reached significant settlement agreements. In 2023, 3M agreed to pay at least US$10.3 billion to resolve lawsuits related to PFAS contamination of public drinking water systems caused by AFFF products.

When combined with settlements involving DuPont and its spin-off Chemours, the total financial commitment reached approximately US$13.5 billion to support municipal remediation efforts. In addition, the U.S. Department of Defense has identified hundreds of military installations with PFAS contamination from legacy firefighting foam use and is implementing large-scale cleanup programs. Similar remediation obligations are emerging in the United Kingdom, Australia, and Germany, creating long-term demand for PFAS treatment services worldwide.

Category-wise Analysis

Waste Type Insights

Among all waste type segments, PFAS-Contaminated Water is the dominant category, accounting for approximately 40% of total market revenue. Water contamination from PFAS is the most widespread and heavily litigated form of PFAS pollution worldwide. This situation is mainly driven by decades of AFFF firefighting foam usage, industrial discharges, and the gradual atmospheric deposition of PFAS into both surface water and groundwater systems. Regulatory enforcement is also accelerating demand for remediation solutions.

The U.S. EPA established maximum contaminant levels of 4 ppt for PFOA and PFOS in public drinking water, which has compelled thousands of utilities to invest in large-scale water treatment infrastructure upgrades. A Nature Geoscience (2024) study further highlighted the scale of the problem by reporting that 31% of global groundwater samples exceeded the proposed EPA safety thresholds. Due to its universal occurrence in water systems, strict regulatory limits, and growing legal liabilities, PFAS-contaminated water continues to generate the highest demand for treatment and remediation services worldwide.

By Treatment Technology Analysis

Activated carbon adsorption is the leading treatment technology segment, representing approximately 35% of the total technology market share. Both Granular Activated Carbon (GAC) and Powdered Activated Carbon (PAC) systems are widely used in municipal water treatment facilities because they are technically mature, commercially scalable, and widely accepted by regulators. Another key advantage is their compatibility with existing water treatment infrastructure, allowing utilities to upgrade treatment processes without completely redesigning facilities.

A 441-day pilot-scale study published in a peer-reviewed environmental science journal demonstrated that GAC systems can effectively retain PFAS mass, accumulating around 85 μg of PFAS per gram of adsorbent. These systems are particularly effective in removing long-chain perfluorosulfonic acids (PFSA). Because of this proven performance, the U.S. EPA and many major water utilities recognize GAC as a primary point-of-entry treatment technology for PFAS compliance. In addition, the availability of raw materials, well-established operating procedures, and compatibility with hybrid treatment systems further strengthen activated carbon’s dominant position in large-scale PFAS water management projects.

End-User Insights

The Municipal Water & Wastewater Utilities segment leads the end-user category, accounting for approximately 38% of the total market share. Municipal utilities play a critical role as the primary organizations responsible for implementing PFAS drinking water regulations. They are legally required to comply with enforceable contaminant limits established by regulatory authorities such as the U.S. EPA under the Safe Drinking Water Act, as well as similar regulations within the European Union’s revised Water Framework Directive.

The scale of the challenge is substantial. The U.S. EPA estimates that about 70 million Americans receive drinking water from systems where PFAS has been detected, and many utilities serving populations of 10,000 or more must install compliant treatment systems by 2029. In Europe, the EU Water Framework Directive’s September 2025 provisional agreement to include PFAS, including trifluoroacetic acid (TFA), as priority pollutants requires strict monitoring and treatment. These regulatory obligations, combined with the responsibility to protect public health, ensure steady and predictable procurement of PFAS treatment technologies by municipal utilities worldwide.

Regional Insights

North America PFAS Waste Management Trends

The United States Environmental Protection Agency (EPA) is a major driver of PFAS waste management activity in North America, making the United States the dominant market globally due to its comprehensive and rapidly evolving regulatory framework. In April 2024, the EPA finalized the first enforceable National Primary Drinking Water Regulation for PFOA and PFOS, setting a maximum contamination limit of 4 ppt. This rule requires thousands of public water systems to upgrade treatment infrastructure by 2029. Additionally, the designation of PFOA and PFOS as hazardous substances under Comprehensive Environmental Response, Compensation, and Liability Act has expanded liability to generators, transporters, and disposal companies handling PFAS waste.

The demand for professional remediation services has grown significantly. The U.S. government’s $10 billion environmental remediation funding allocation in 2024 further strengthens cleanup initiatives. Canada is emerging as a secondary market, where Health Canada has established some of the strictest PFAS drinking water guidelines. A 2024 groundwater study found that about 69% of Canadian samples exceeded national PFAS limits, increasing regulatory attention. Provincial authorities now require PFAS assessments at industrial and military sites, while research programs led by Environment and Climate Change Canada continue building a national contamination inventory.

Europe PFAS Waste Management Market Trends

Europe is moving quickly toward becoming the world’s most tightly regulated region for PFAS management. The European Chemicals Agency updated its landmark universal PFAS restriction proposal under REACH Regulation in August 2025 after reviewing more than 5,600 consultation responses. The initiative was originally proposed by Germany, the Netherlands, Denmark, Norway, and Sweden, which continue to drive stronger PFAS legislation across the European Union. Additional regulatory measures include the EU POPs Regulation (EU) 2025/718, which aligns PFOS limits with PFOA at ≤0.025 mg/kg starting December 2025.

The new Packaging and Packaging Waste Regulation introduces PFAS limits for food-contact packaging beginning in August 2026. These layered rules are pushing chemical, textile, and electronics manufacturers in Germany, France, and Spain to invest quickly in PFAS waste treatment solutions. The United Kingdom is developing its own PFAS strategy through the Environment Agency after Brexit. Meanwhile, the European Commission plans to launch a continent-wide PFAS monitoring framework by 2026 to create a comprehensive contamination database.

Asia Pacific PFAS Waste Management Market Trends

Asia Pacific is expected to be the fastest-growing market for PFAS waste management due to its large manufacturing base, rapid industrial expansion, and strengthening environmental regulations. China, the world’s leading producer of fluorochemicals and PFAS precursors, represents the region’s largest contamination source. Significant PFAS discharges have been reported near fluorochemical manufacturing hubs in Jiangsu and Zhejiang provinces. A 2024 study published in Nature Geoscience identified China, along with Australia, Europe, and North America, as a global PFAS contamination hotspot.

In response, Chinese regulators are gradually incorporating PFAS into national water quality and hazardous waste management policies, supporting the development of commercial PFAS treatment services. Japan has also introduced PFAS drinking water guidelines through the Ministry of the Environment Japan and continues to investigate contamination near U.S. military base sites. India is at an earlier regulatory stage but is seeing rising awareness in sectors such as electronics manufacturing, textile finishing, and leather processing. Across ASEAN countries, including Vietnam, Thailand, and Indonesia, multinational supply chain standards and export regulations are encouraging early adoption of PFAS treatment solutions.

Competitive Landscape

The global PFAS Waste Management market shows a moderately fragmented competitive structure, with both large multinational environmental service providers and specialized technology companies competing across treatment, remediation, and destruction services. Veolia Environnement currently holds a leading position through its BeyondPFAS initiative, which offers an integrated solution covering sampling, water treatment, soil remediation, and high-efficiency incineration. The company has already processed around 24 billion gallons of PFAS-contaminated water globally. Another key player, Clean Harbors, differentiates itself through its “Total PFAS Solution,” a vertically integrated service model that includes laboratory analysis, filtration, remediation, and final destruction.

The company commissioned a dedicated PFAS incineration facility in Kimball, Nebraska, strengthening its treatment capacity. Across the market, companies compete based on factors such as thermal destruction capability, regulatory compliance expertise, geographic reach, and access to licensed disposal facilities. Emerging service models, including remediation-as-a-service (RaaS) and performance-based contracts tied to regulatory targets, are also shaping future competitive strategies.

Key Developments:

- In May 2025, Veolia Environnement released results from extensive PFAS incineration testing at its Port Arthur, Texas, hazardous waste facility. The study confirmed that high-temperature thermal treatment can destroy more than 99.9% of PFAS compounds in AFFF firefighting foam and contaminated waste streams.

- In December 2024, Clean Harbors commissioned a new incinerator at its Kimball, Nebraska facility, expanding hazardous waste destruction capacity. The project supports the company’s integrated “Total PFAS Solution,” providing end-to-end services including sampling, transportation, treatment, and disposal of complex PFAS waste streams.

- In April 2024, The United States Environmental Protection Agency finalized the National Primary Drinking Water Regulation for PFAS, setting enforceable limits of 4 parts per trillion for PFOA and PFOS. The rule requires public water systems to monitor contamination and implement treatment solutions by 2029.

Companies Covered in Polyfluoroalkyl Substances (PFAS) Waste Management Market

- Chemours

- Asahi Glass

- Kuraray Co., Ltd.

- Arkema S.A.

- BASF SE

- Shandong Chengxin Chemical Co., Ltd.

- DIC Corporation

- 3M Company

- Daikin Industries, Ltd.

- Huntsman Corporation

- Solvay S.A.

- AGC Chemicals

- Haike Chemicals Group

- Clean Harbors, Inc.

- Veolia Environnement S.A.

- AECOM

- Xylem Inc.

- Evoqua Water Technologies

- Stericycle, Inc.

- US Ecology

Frequently Asked Questions

The global PFAS Waste Management market is estimated at US$ 2.1 Billion in 2026 and is projected to reach US$ 3.1 Billion by 2033, advancing at a CAGR of 5.6% through the forecast period, driven by mandatory regulatory compliance obligations and the widening scale of confirmed PFAS contamination across drinking water, soil, and industrial waste streams globally.

The most critical growth driver is the escalating global regulatory framework for PFAS. The U.S. EPA's April 2024 rule designating PFOA and PFOS as hazardous substances under CERCLA, establishing enforceable drinking water limits at 4 ppt, and the EU's REACH universal PFAS restriction proposal covering over 10,000 substances are collectively generating large-scale, legally mandated remediation demand.

PFAS-Contaminated Water is the leading waste type segment, accounting for approximately 40% of market share. It is the most extensively regulated and litigated PFAS contamination medium, with the U.S. EPA estimating 70 million Americans currently exposed to PFAS through drinking water, a contamination scale confirmed by a peer-reviewed Nature Geoscience (2024) study of over 45,000 global water samples.

North America holds the leading regional position, anchored by the United States' comprehensive regulatory ecosystem, including the EPA's National Primary Drinking Water Regulation, CERCLA hazardous substance designations, and the $10 Billion government remediation allocation in 2024, which collectively generate the world's largest and most legally defined PFAS waste treatment procurement pipeline.

AFFF firefighting foam remediation is the most immediate large-scale commercial opportunity. The combined $13.5 Billion settlement by 3M and DuPont, multi-year U.S. Department of Defense cleanup programs at contaminated military installations, and expanding international AFFF remediation mandates in Germany, Australia, and the U.K. represent a mandated, legally funded demand stream of exceptional scale.

Key market participants include Veolia Environnement (with its BeyondPFAS end-to-end remediation platform), Clean Harbors (with its "Total PFAS Solution" and Kimball, Nebraska incineration facility), Chemours, 3M, BASF SE, Daikin Industries, Solvay S.A., Arkema, AGC Chemicals, Kuraray, Huntsman Corporation, AECOM, Xylem, and Stericycle, among others.