- Pharmaceuticals

- Pneumonia Diagnostics Market

Pneumonia Diagnostics Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Pneumonia Diagnostics Market by Product (Kits and Reagents, and Instruments), Pathogen (Bacterial Pneumonia, Atypical Pneumonia, Viral Pneumonia, and Others), Setting of Acquisition (Community-Acquired Pneumonia (CAP), Hospital-Acquired Pneumonia (HAP), and Ventilator-Associated Pneumonia (VAP)), End-user (Hospitals, Diagnostic Centers, and Specialty Clinics) and Regional Analysis from 2026 - 2033

Pneumonia Diagnostics Market Share and Trends Analysis

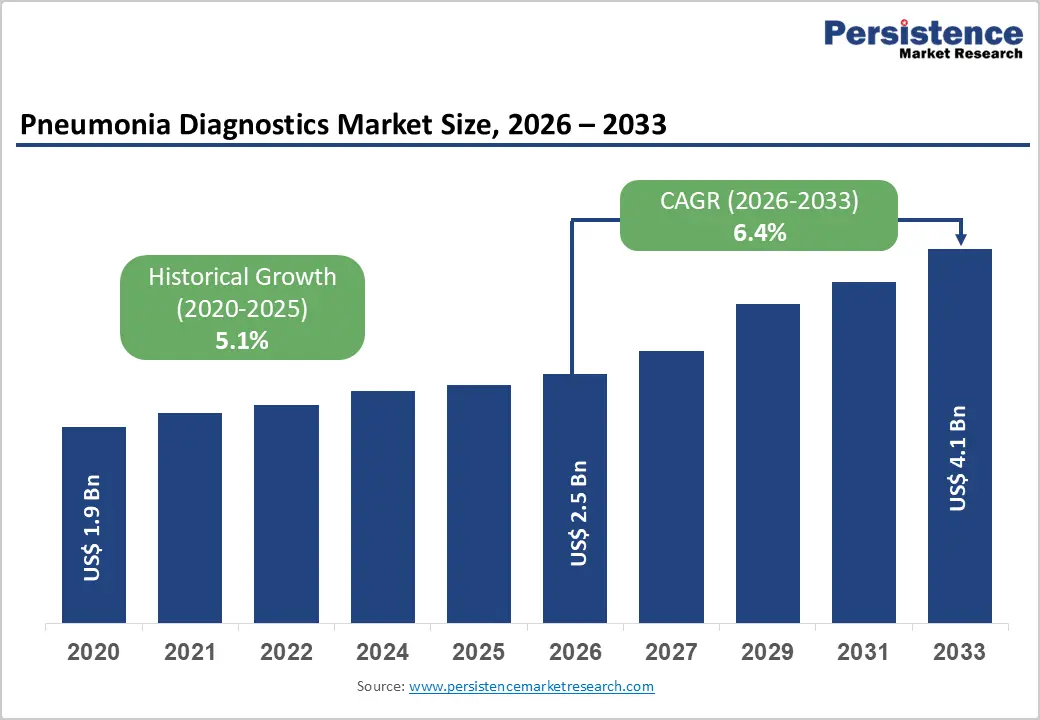

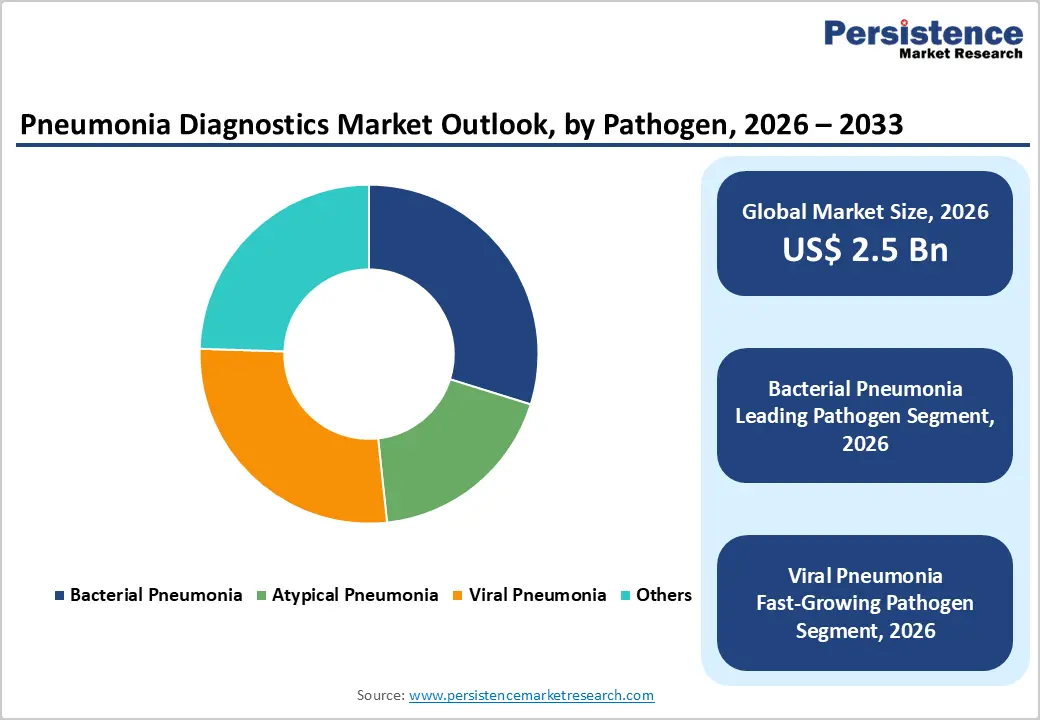

The global pneumonia diagnostics market is expected to reach US$ 2.5 billion in 2026 and US$ 4.1 billion by 2033, growing at a CAGR of 6.4% over the forecast period from 2026 to 2033.

The global demand for pneumonia diagnostics is steadily increasing, driven by the rising burden of respiratory infections, growing hospitalization rates, and increasing emphasis on early and accurate disease detection. Higher incidence of community-acquired and hospital-acquired pneumonia, particularly among elderly and immunocompromised populations, is supporting sustained diagnostic volumes worldwide. The use of rapid molecular diagnostics, antigen-based tests, and syndromic respiratory panels is improving clinical decision-making and accelerating test adoption across care settings. Increased healthcare spending, heightened awareness of antimicrobial resistance, and the need for timely differentiation between bacterial and viral pneumonia are further strengthening market growth.

Key Industry Highlights:

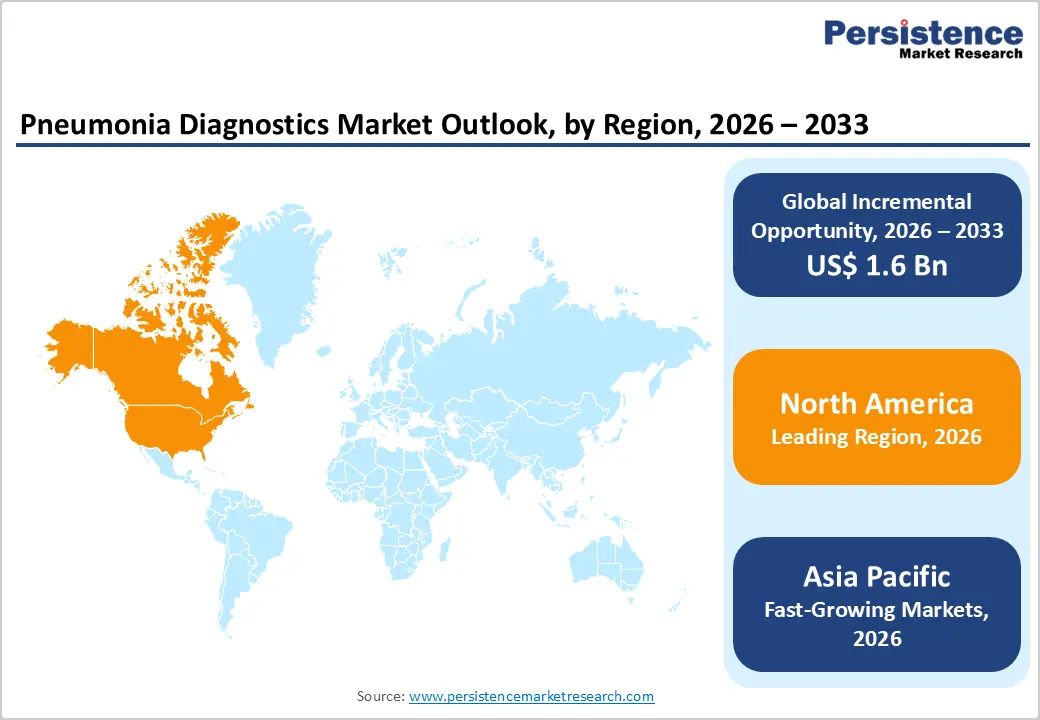

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high diagnostic testing rates, strong reimbursement frameworks, early adoption of molecular diagnostics, and the strong presence of leading diagnostic manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large patient base, rising incidence of respiratory infections, improving access to healthcare services, rapid expansion of diagnostic laboratories, and increasing government investments in infectious disease surveillance.

- Leading Product Segment: Kits and reagents dominate the market due to their recurring use across molecular, immunodiagnostic, and antigen-based pneumonia testing, as well as their critical role in routine and high-throughput diagnostic workflows.

- Fastest-Growing Product Segment: Instruments are expanding rapidly as hospitals and laboratories invest in automated analyzers, multiplex PCR platforms, and advanced diagnostic systems to improve efficiency and turnaround time.

- Leading Setting of Acquisition Segment: Community-acquired pneumonia (CAP) remains the top application, driven by high diagnostic volumes in outpatient clinics, emergency departments, and hospitals managing routine pneumonia cases.

- Fastest-Growing Setting of Acquisition Segment: Hospital-acquired pneumonia (HAP) is scaling quickly due to increasing ICU admissions, ventilator use, and the growing need for rapid and precise diagnostics to manage complex inpatient infections.

| Key Insights | Details |

|---|---|

|

Pneumonia Diagnostics Market Size (2026E) |

US$ 2.5 Bn |

|

Market Value Forecast (2033F) |

US$ 4.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.1% |

Market Dynamics

Driver - Rising Disease Burden and Increased Hospitalization Rates Driving Diagnostic Demand

The global burden of pneumonia and other respiratory infections continues to rise, particularly among vulnerable populations such as the elderly, pediatric patients, and individuals with compromised immune systems. Aging populations in developed and emerging economies are more susceptible to community-acquired pneumonia due to weakened immune responses and higher prevalence of chronic conditions such as diabetes, cardiovascular disease, and chronic obstructive pulmonary disease. Similarly, children under five years of age remain at high risk in low- and middle-income countries, where access to early diagnosis is often limited.

For instance, in 2023, according to the Global Burden of Disease (GBD 2023) estimates, pneumonia accounted for approximately 2.5 million deaths worldwide, highlighting its significant global health impact. This included around 610,000 deaths among children under five years of age and an additional 79,000 deaths among children aged 5–14 years, highlighting the disproportionate burden of the disease on pediatric populations, particularly in low- and middle-income countries These epidemiological trends are driving sustained demand for pneumonia diagnostics, as early and accurate detection is critical to reducing mortality, preventing complications, and optimizing treatment decisions across care settings.

Increasing hospitalization rates for severe respiratory infections are significantly amplifying diagnostic requirements, particularly in intensive care units. The rising incidence of hospital-acquired pneumonia and ventilator-associated pneumonia has heightened the need for rapid, high-sensitivity diagnostic tests capable of identifying causative pathogens in critically ill patients. ICU environments demand fast turnaround times to guide timely antimicrobial therapy and infection-control measures. As hospitals face growing patient loads and higher clinical complexity, adoption of advanced molecular and multiplex diagnostic platforms is accelerating, reinforcing the central role of pneumonia diagnostics in inpatient and critical care pathways.

Restraints - High Cost and Limited Diagnostic Infrastructure Restricting Market Penetration

The high cost of advanced molecular diagnostic platforms remains a significant restraint on the pneumonia diagnostics market, particularly in low- and middle-income countries. Technologies such as multiplex PCR systems, automated nucleic acid extractors, and syndromic respiratory panels require substantial upfront capital investment, along with recurring expenses for reagents, maintenance, and quality control. These costs often exceed the budgetary capacities of public hospitals and smaller laboratories in resource-constrained settings. In addition, limited reimbursement coverage for advanced diagnostics in many developing regions further discourages adoption. As a result, healthcare providers may continue to rely on slower, less sensitive conventional methods, delaying accurate diagnosis and appropriate treatment.

Limited access to diagnostic infrastructure in rural and underdeveloped healthcare settings further compounds this challenge. Many primary and secondary care facilities lack adequately equipped laboratories, stable electricity supply, cold-chain logistics, and trained personnel required to operate advanced diagnostic systems. Geographic barriers, workforce shortages, and fragmented referral networks often result in delayed or missed pneumonia diagnoses, particularly among vulnerable populations. These infrastructure gaps restrict the reach of modern diagnostic solutions and contribute to persistent disparities in pneumonia outcomes. Until affordable, decentralized, and easy-to-use diagnostic technologies become more widely available, infrastructure limitations will continue to constrain broader market expansion.

Opportunity - Expansion of Rapid and Syndromic Diagnostics Creating New Growth Opportunities

The expansion of point-of-care (POC) and rapid diagnostic tests represents a major opportunity for the pneumonia diagnostics market, particularly by enabling decentralized testing in outpatient, emergency, and resource-limited settings. POC diagnostics allow clinicians to obtain results within minutes to hours, facilitating faster clinical decision-making, earlier treatment initiation, and reduced reliance on centralized laboratories. This is especially valuable in primary care clinics, emergency departments, and rural healthcare facilities where access to advanced laboratory infrastructure is limited. Growing demand for near-patient testing, coupled with efforts to reduce hospital congestion and improve care accessibility, is accelerating the adoption of compact, user-friendly diagnostic platforms. These solutions also support timely triage, reduce unnecessary hospital admissions, and improve patient outcomes.

Furthermore, demand for syndromic respiratory panels is increasing due to the clinical challenge of distinguishing pneumonia caused by bacterial, viral, or atypical pathogens solely on symptoms. Overlapping clinical presentations often lead to empirical treatment and inappropriate antibiotic use. Syndromic panels address this gap by simultaneously detecting multiple respiratory pathogens from a single sample, improving diagnostic accuracy and supporting antimicrobial stewardship initiatives. Hospitals and diagnostic laboratories are increasingly adopting multiplex panels to streamline workflows, shorten turnaround times, and enhance infection control. As respiratory surveillance programs expand and clinicians seek comprehensive diagnostic insights, syndromic testing is expected to play a pivotal role in market growth.

Category-wise Insights

By Product, Kits and Reagents Dominate Globally Due to High Testing Volumes and Recurring Diagnostic Demand

The kits and reagents segment is projected to dominate the global pneumonia diagnostics market in 2026, accounting for 53.6% of revenue. This dominance is primarily attributed to their recurring use across all pneumonia diagnostic workflows, including molecular assays, immunodiagnostics, and antigen-based testing. Kits and reagents are consumed with each test, making them indispensable in hospitals, diagnostic laboratories, and specialty clinics. The growing adoption of multiplex PCR panels for rapid differentiation between bacterial, viral, and atypical pneumonia is significantly increasing reagent consumption.

Additionally, rising pneumonia incidence, seasonal respiratory outbreaks, and post-pandemic respiratory surveillance programs continue to drive sustained test volumes. Continuous innovation in assay sensitivity, specificity, and turnaround time has improved clinical confidence and expanded routine testing. Expanding antimicrobial stewardship initiatives and increased reliance on early pathogen identification further reinforce the sustained dominance of kits and reagents in the global pneumonia diagnostics market.

By Pathogen, Bacterial Pneumonia Leads the Market Due to High Disease Burden and Routine Diagnostic Testing

The bacterial pneumonia segment is projected to dominate the global pneumonia diagnostics market in 2026, accounting for 29.8% of revenue. This leadership is driven by the high global burden of bacterial pneumonia, particularly infections caused by Streptococcus pneumoniae and other common bacterial pathogens. Bacterial pneumonia diagnostics remain central to clinical decision-making, as timely identification directly influences antibiotic selection and patient outcomes. Hospitals and laboratories routinely perform bacterial testing using cultures, antigen detection, and molecular assays, resulting in consistent diagnostic demand.

Rising concerns over antimicrobial resistance have further increased the need for accurate bacterial identification to support targeted therapy. Aging populations, higher hospitalization rates, and increasing prevalence of comorbid conditions continue to elevate bacterial pneumonia risk worldwide. Advances in rapid molecular diagnostics and syndromic panels are further strengthening adoption and sustaining the segment’s leading position.

By End-user, Hospitals Dominate Globally Due to High Case Severity and Advanced Diagnostic Infrastructure

The hospitals segment is projected to dominate the global pneumonia diagnostics market in 2026, accounting for 48.2% of revenue. This dominance is driven by the high volume of pneumonia cases managed in hospital settings, including severe community-acquired, hospital-acquired, and ventilator-associated pneumonia. Hospitals are equipped with advanced laboratory infrastructure and intensive care units, enabling comprehensive diagnostic testing using molecular, immunoassay, and culture-based methods.

Higher patient acuity, frequent ICU admissions, and the need for rapid diagnostic turnaround significantly increase test utilization in hospitals. In addition, hospitals are early adopters of advanced multiplex panels and automated platforms to support infection control and antimicrobial stewardship programs. Strong reimbursement coverage, standardized clinical protocols, and integration of diagnostics into inpatient care pathways further reinforce hospital-led dominance in the global pneumonia diagnostics market.

Region-wise Insights

North America Pneumonia Diagnostics Market Trends

North America is expected to dominate the global pneumonia diagnostics market, with a 47.5% share in 2026, led primarily by the United States. Market leadership is underpinned by a high burden of respiratory infections, advanced healthcare infrastructure, and widespread access to diagnostic testing across hospital and outpatient settings. Early adoption of molecular diagnostics, including multiplex PCR panels and rapid antigen tests, has significantly improved turnaround times and clinical decision-making.

The region benefits from strong reimbursement frameworks, high healthcare spending, and the presence of leading diagnostic manufacturers with extensive distribution networks. Increasing ICU admissions, aging populations, and heightened focus on antimicrobial stewardship programs further support demand for accurate pathogen identification. In addition, strong regulatory oversight, continuous product approvals, and integration of diagnostics into hospital infection-control protocols accelerate technology uptake.

High awareness among clinicians, routine use of advanced diagnostic algorithms, and growing emphasis on early differentiation between bacterial and viral pneumonia continue to reinforce North America’s dominant position in the global market.

Europe Pneumonia Diagnostics Market Trends

The European pneumonia diagnostics market is expected to grow steadily, supported by rising pneumonia incidence among the elderly, expanding healthcare coverage, and greater emphasis on early and accurate diagnosis. Key markets such as Germany, the U.K., France, Italy, and the Nordic countries demonstrate strong adoption of molecular and immunodiagnostic testing, driven by well-developed laboratory infrastructure and standardized clinical guidelines. Public healthcare systems across Europe are increasingly prioritizing rapid diagnostics to reduce inappropriate antibiotic use and hospital length of stay. Growing investments in laboratory automation, syndromic respiratory panels, and hospital-based testing capabilities are enhancing diagnostic efficiency.

Regulatory harmonization under the EU framework and strong emphasis on quality and clinical validation support sustained adoption of advanced diagnostics. Additionally, rising seasonal viral outbreaks and post-pandemic respiratory surveillance programs are increasing testing volumes. Collaboration between public health agencies, hospitals, and diagnostic manufacturers continues to strengthen long-term market growth across the region.

Asia Pacific Pneumonia Diagnostics Market Trends

Asia Pacific pneumonia diagnostics market is expected to register a relatively higher CAGR of around 8.4% between 2026 and 2033, driven by large patient populations, rising incidence of respiratory infections, and improving access to healthcare services. Countries such as China, India, Japan, and South Korea are witnessing a rapid expansion of diagnostic capacity, supported by government investments in healthcare infrastructure and infectious disease surveillance. Increasing awareness of early pneumonia diagnosis, growing hospital admissions, and rising adoption of molecular and rapid diagnostic tests are key growth drivers. Cost-effective diagnostic solutions and local manufacturing are improving affordability in price-sensitive markets, particularly in emerging economies.

The expansion of private diagnostic laboratories, urbanization, and the increasing penetration of point-of-care testing are further boosting demand. In addition, national health programs focused on respiratory disease management and antimicrobial resistance are encouraging wider use of advanced pneumonia diagnostics across both urban and semi-urban healthcare settings.

Competitive Landscape

The global pneumonia diagnostics market is highly competitive, with strong participation from companies such as Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., BIOMÉRIEUX, Eisai Co., Ltd., Xiamen Wiz Biotech Co., Ltd., and F. Hoffmann-La Roche Ltd. These players leverage extensive distributor networks, strong brand recognition, and continuous innovation in molecular assays, immunodiagnostics, and automated platforms to address diverse clinical needs across community-acquired, hospital-acquired, and ventilator-associated pneumonia settings.

Rising demand for rapid and accurate pathogen identification, early differentiation between bacterial and viral pneumonia, and support for antimicrobial stewardship is accelerating adoption across hospitals, diagnostic laboratories, and specialty clinics. Manufacturers are increasingly focused on multiplex PCR panels, point-of-care testing solutions, faster turnaround times, and improved sensitivity and specificity. Strategic priorities include portfolio expansion, regulatory approvals, clinician and laboratory staff training, and geographic expansion to strengthen market positioning and drive sustained growth.

Key Industry Developments:

- In December 2025, Detect-ION LLC partnered with the Infectious Diseases Division at Mayo Clinic Florida to develop a non-invasive, breath-based diagnostic test for detecting Pseudomonas aeruginosa using miniaturized gas chromatography–mass spectrometry technology. Funded by the Mayo Clinic Advanced Innovation Research program, the collaboration aims to improve early detection of this high-risk pathogen, a major cause of hospital-acquired and ventilator-associated pneumonia, particularly in lung transplant and structurally compromised lung patients.

- In August 2025, In August 2025, EDX Medical developed a diagnostic test to detect and characterize early signs of pneumonia in critically ill hospitalized patients. The company partnered with the intensive care unit at Cambridge University Hospitals NHS Foundation Trust to advance development, with the test originating from a public–private collaboration involving the University of Cambridge, the UK Health Security Agency, and Cambridge Enterprise.

Companies Covered in Pneumonia Diagnostics Market

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories, Inc.

- BIOMÉRIEUX

- Eisai Co., Ltd.

- Xiamen Wiz Biotech Co., Ltd

- F. Hoffmann-La Roche Ltd

- AdvaCare Pharma®

- Jiangsu BioPerfectus Technologies Co., Ltd

- Jiangsu Macro & Micro-Test Med-Tech Co., Ltd.

- WELLS BIO INC.

- Avecon Healthcare

- Angstrom Biotech Pvt. Ltd.

- Alpine Biomedicals Pvt Ltd.

- Revvity

- Others

Frequently Asked Questions

The global pneumonia diagnostics market is projected to be valued at US$ 2.5 Bn in 2026.

The global pneumonia diagnostics market is driven by the high burden of respiratory infections, rising hospitalizations and ICU admissions, increasing antimicrobial resistance, and growing adoption of rapid molecular and multiplex diagnostic technologies.

The global pneumonia diagnostics market is poised to witness a CAGR of 6.4% between 2026 and 2033.

Major opportunities lie in the expansion of syndromic PCR panels, point-of-care and decentralized testing, emerging market penetration, and integration of diagnostics with antimicrobial stewardship programs.

Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., BIOMÉRIEUX, Eisai Co., Ltd., Xiamen Wiz Biotech Co., Ltd, and F. Hoffmann-La Roche Ltd are some of the key players in the pneumonia diagnostics market.