- Medical Devices

- Photoacoustic Imaging Market

Photoacoustic Imaging Market Size, Share, and Growth Forecast 2026 - 2033

Photoacoustic Imaging Market by Product (Imaging Systems, Transducers, Software & Accessories), Modality (Photoacoustic Tomography, Photoacoustic Microscopy, Intravascular Photoacoustic Imaging, Others), by Application (Oncology, Cardiology, Neurology, Dermatology, Preclinical Research, Others), End-user (Hospitals & Clinics, Research & Academic Institutes, Diagnostic Imaging Centers, Pharmaceutical & Biotechnology Companies), and Regional Analysis, 2026 - 2033

Photoacoustic Imaging Market Share and Trends Analysis

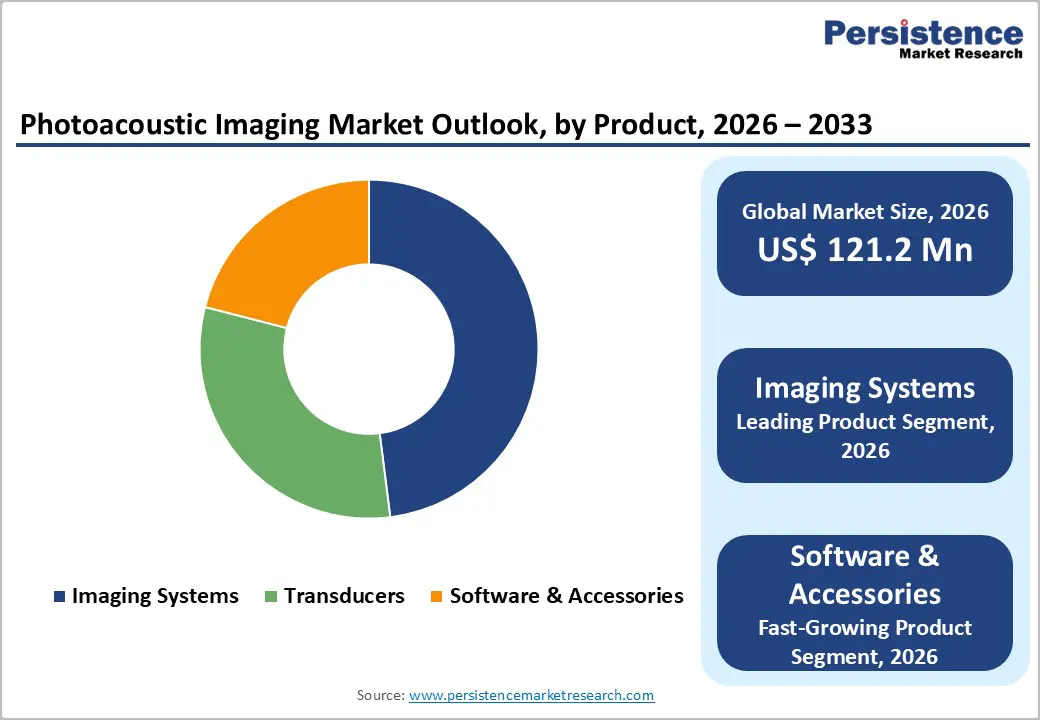

The global photoacoustic imaging market size is expected to be valued at US$ 121.2 million in 2026 and projected to reach US$ 178.2 million by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The growth is driven by the rising burden of cancer and cardiovascular diseases, growing preference for non-ionizing and hybrid imaging, and increasing use of high-resolution functional imaging in preclinical and translational research. Clinical adoption is further supported by advances in laser sources, ultrasound detection, and contrast agents, as well as growing validation of photoacoustic imaging in peer-reviewed oncology, neurology, and vascular imaging studies.

Key Industry Highlights:

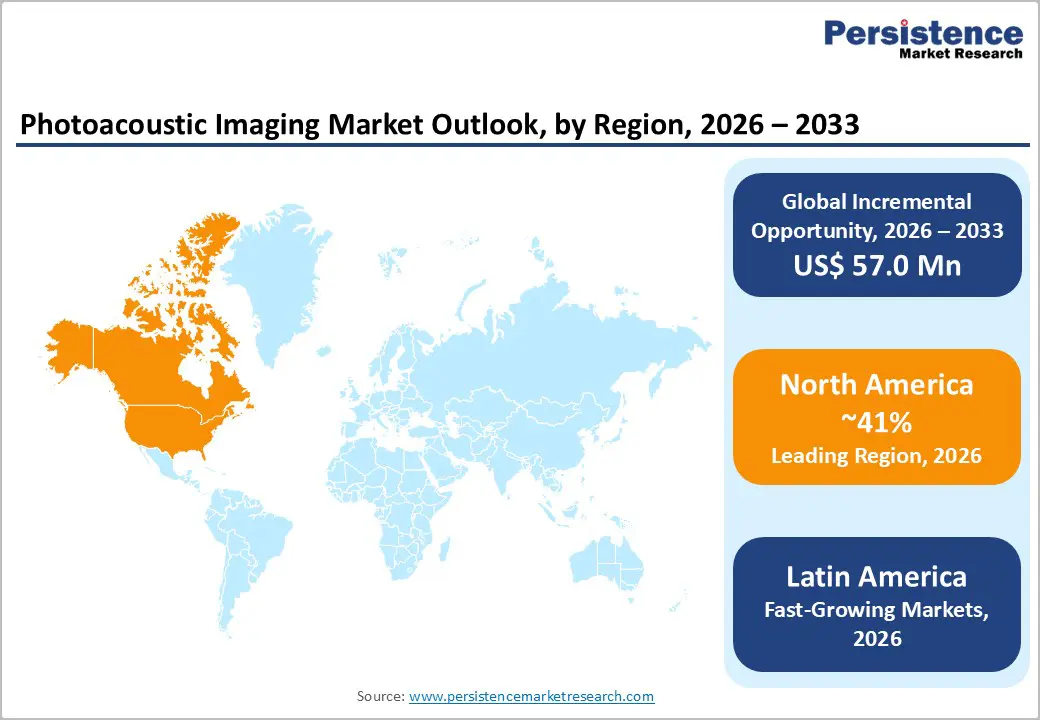

- Regional Leadership: North America is the leading region in the photoacoustic imaging market, accounting for about 41% of global revenue in 2025, supported by strong NIH-funded research, high healthcare spending, early adoption of hybrid ultrasound-photoacoustic systems, and active collaborations between device manufacturers and major academic medical centers.

- Fast-growing Region: Latin America is expected to be the fastest-growing region, as countries such as Brazil and Mexico expand oncology and cardiovascular care capacities, invest in advanced imaging technologies, and strengthen partnerships with global vendors and local distributors to modernize diagnostic infrastructure in tertiary hospitals.

- Leading Product: By product, imaging systems dominate with an estimated 48% share in 2025, as complete photoacoustic platforms incorporating lasers, transducer arrays, electronics, and software are essential for both research and early clinical deployments, typically installed at universities, cancer institutes, and specialized diagnostic centers.

- Fast-growing Product: Software & Accessories represent the fastest-growing product segment, driven by demand for advanced reconstruction, quantitative analysis, AI-assisted interpretation, and multispectral unmixing tools, as well as the recurring need for probes, fibers, and system upgrades across an expanding installed base of photoacoustic systems worldwide.

| Key Insights | Details |

|---|---|

| Photoacoustic Imaging Market Size (2026E) | US$ 121.2 million |

| Market Value Forecast (2033F) | US$ 178.2 million |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Rising cancer burden and demand for functional, non-ionizing imaging

A primary growth driver for the photoacoustic imaging market is the rising global cancer burden and the need for imaging technologies that can provide both structural and functional information without ionizing radiation. The World Health Organization (WHO) estimates that new cancer cases exceeded 19 million worldwide in 2020, with numbers projected to grow further as populations age and lifestyle risk factors persist. Functional imaging of tumor vasculature, hypoxia, and oxygen saturation is critical for early diagnosis and therapy monitoring, and photoacoustic imaging combines optical contrast with ultrasound resolution to visualize these parameters in real time. Compared with conventional optical imaging, photoacoustic techniques allow penetration depths of several centimeters while preserving high contrast based on optical absorption in hemoglobin or exogenous agents. This makes photoacoustic imaging highly attractive for breast cancer, melanoma, and other superficial or near-surface tumors, supporting broader adoption in oncology-focused research and, gradually, in clinical workflows.

Technological integration with ultrasound and advances in laser and detector design

Another key driver is the rapid technological progress in hybrid ultrasound photoacoustic platforms and system components such as tunable lasers and high-frequency transducers. Commercial systems from players such as FUJIFILM VisualSonics Inc., iThera Medical GmbH, and Seno Medical Instruments, Inc. integrate photoacoustic imaging with ultrasound to offer co-registered anatomical and functional images in a single examination, improving clinical usability. High-repetition-rate lasers, wavelength-tunable sources in the near-infrared window, and sensitive piezoelectric or capacitive micromachined ultrasonic transducers have enhanced signal-to-noise ratios and frame rates suitable for dynamic imaging. These advances enable applications such as real-time visualization of microvasculature, monitoring of oxygen saturation, and assessment of contrast-agent kinetics in preclinical research. As system performance improves and costs gradually decline, hospitals and research institutes gain stronger justification to invest in photoacoustic platforms as an extension of existing ultrasound infrastructure, which fuels incremental demand for imaging systems, transducers, and software & accessories.

Restraints - High system cost and constrained reimbursement environment

The high capital cost of photoacoustic imaging systems and the limited availability of dedicated reimbursement codes remain major barriers to widespread clinical adoption. Integrated photoacoustic-ultrasound imaging systems with tunable lasers and high-end transducer arrays can cost several hundred thousand US dollars, which is a significant investment for hospitals and diagnostic imaging centers, especially in cost-sensitive markets. In many countries, reimbursement authorities and payers have not yet established specific tariffs for photoacoustic imaging procedures, forcing providers to rely on generic ultrasound or research funding to cover costs. This mismatch between equipment investment and revenue generation potential slows the transition from research-only use to routine clinical deployment and can lengthen purchase decision cycles, especially for smaller facilities and emerging markets.

Regulatory complexity and need for robust clinical validation

Regulatory pathways for novel hybrid imaging modalities can be complex, requiring robust evidence of safety, effectiveness, and incremental clinical value over existing standards of care. Manufacturers must satisfy stringent quality and safety requirements under frameworks such as U.S. FDA device regulations and the European Union Medical Device Regulation (EU MDR). For new photoacoustic applications, particularly in oncology and cardiovascular imaging, regulators and clinicians expect prospective clinical studies demonstrating improved diagnostic accuracy, better treatment planning, or cost-effectiveness compared with conventional ultrasound, MRI, or CT. Generating such evidence is time- and resource-intensive and can delay product launches or limit labeled indications. These regulatory and evidence-generation requirements can slow innovation cycles and act as a deterrent for smaller companies seeking entry into the photoacoustic imaging space.

Opportunity - Software, AI analytics, and workflow solutions for photoacoustic image interpretation

One of the most promising opportunities lies in software & accessories, particularly advanced image reconstruction, quantification, and artificial intelligence (AI)-driven analytics. As systems generate increasingly complex multispectral and volumetric data, there is a strong demand for software that can automatically separate chromophore signatures, quantify hemoglobin oxygenation, and overlay functional information on anatomical maps in a user-friendly way. AI and machine learning algorithms can assist in lesion detection, segmentation, and classification, helping clinicians interpret photoacoustic signals more consistently and rapidly. Enhanced software capabilities are essential in modalities such as photoacoustic tomography and photoacoustic microscopy, where multi-wavelength datasets and fine spatial details are abundant. Vendors that provide robust, regulatory-compliant software ecosystems, cloud connectivity, and integration with hospital PACS and reporting systems can tap into recurring revenue through licenses, upgrades, and service contracts, supporting the high-growth profile of the software & accessories segment over the forecast period.

Expanding applications in preclinical research, neurology, and cardiovascular imaging

Another major opportunity is the expanding use of photoacoustic imaging in preclinical research and emerging clinical areas beyond oncology, notably neurology and cardiology. In preclinical settings, photoacoustic imaging enables longitudinal monitoring of small animal models to study tumor angiogenesis, brain function, stroke, and drug delivery without ionizing radiation. This is highly relevant for pharmaceutical & biotechnology companies and research & academic institutes seeking more translational imaging readouts. In neurology, research groups are exploring transcranial photoacoustic approaches and minimally invasive configurations to probe cerebral hemodynamics and oxygenation. In cardiology, intravascular photoacoustic imaging is being investigated for characterization of atherosclerotic plaques, lipid cores, and stent interactions, complementing intravascular ultrasound and optical coherence tomography. As technical challenges such as motion artifacts and access are addressed, these emerging applications can significantly widen the addressable market, particularly in specialized centers that already invest in advanced cardiovascular and neuroimaging platforms.

Category-wise Analysis

Product Insights

In the photoacoustic imaging market, Imaging Systems represent the leading product segment, accounting for approximately 48% share in 2025. This dominance reflects the fact that full systems including lasers, transducers, electronics, and integrated software, are the primary revenue generators and are essential for both research and clinical applications. Companies such as FUJIFILM VisualSonics Inc., iThera Medical GmbH, and Seno Medical Instruments, Inc. offer complete optoacoustic or photoacoustic imaging platforms that support small animal imaging, breast imaging, vascular imaging, and multimodal ultrasound integration. These systems are capital-intensive and typically installed at universities, cancer centers, and advanced research hospitals, resulting in higher per-unit revenues than standalone transducers or accessories. However, as the installed base grows, the Software & Accessories segment, covering reconstruction software, analysis modules, probes, fibers, and disposables, is expected to be the fastest-growing, driven by upgrades, license renewals, and application-specific toolkits that deepen usage within existing accounts.

Application Insights

By application, Oncology is the leading segment and is estimated to account for roughly 38% share of the photoacoustic imaging market in 2025. This leadership is grounded in the technology’s ability to visualize tumor vasculature, perfusion, and oxygenation, which are critical biomarkers for cancer detection, staging, and therapy response assessment. Breast cancer imaging, melanoma mapping, and evaluation of superficial or near-surface tumors are among the earliest clinical application areas investigated for photoacoustic techniques. Numerous preclinical and early clinical studies have demonstrated that photoacoustic imaging can detect changes in vascular density and oxygen saturation earlier than anatomical size changes, aiding treatment planning and monitoring. Beyond oncology, Preclinical Research and Neurology are emerging as high-growth segments, as investigators explore photoacoustic methods to study neurovascular coupling, stroke models, and drug distribution, bringing additional momentum to the overall application landscape.

End-user Insights

Among end users, Hospitals & Clinics currently represent the leading segment, with an estimated share of about 40% in 2025, driven by early clinical deployments of hybrid photoacoustic-ultrasound systems in oncology, breast imaging, and vascular diagnostics. Large teaching hospitals and specialty cancer centers are often first adopters, leveraging photoacoustic imaging in pilot programs and clinical research protocols while integrating it into multidisciplinary care pathways. At the same time, Research & Academic Institutes and Pharmaceutical & Biotechnology Companies collectively form a rapidly growing user base. Academic institutions adopt sophisticated systems for fundamental research, small animal imaging, and method development, while pharma and biotech organizations increasingly integrate photoacoustic imaging into preclinical efficacy and safety studies, drug delivery research, and biomarker discovery. Diagnostic imaging centers also contribute to demand, where reimbursement and clinical protocols support advanced breast and vascular imaging services.

Regional Insights

North America Photoacoustic Imaging Market Trends and Insights

North America leads the global photoacoustic imaging market with an estimated 41% share in 2025, underpinned by strong research infrastructure, high healthcare expenditure, and early adoption of hybrid imaging technologies. The United States hosts numerous academic medical centers and cancer institutes that conduct pioneering work in optoacoustic imaging, supported by funding from bodies such as the National Institutes of Health (NIH). These centers collaborate closely with industry players including FUJIFILM VisualSonics Inc., Endra Life Sciences Inc., and Seno Medical Instruments, Inc., fostering iterative system development and clinical validation. The regulatory environment, although demanding, provides clear pathways for device clearance, and early approvals of photoacoustic-ultrasound systems for breast imaging and vascular applications have helped legitimize the modality.

In addition, North America benefits from a mature ecosystem of ultrasound manufacturers, laser suppliers, and software developers that can be integrated into photoacoustic systems. Hospitals are increasingly interested in technologies that augment conventional ultrasound without adding ionizing radiation, particularly in oncology and women’s health. Growing emphasis on precision medicine and functional imaging aligns with the strengths of photoacoustic techniques, supporting gradual expansion from research only to clinical usage in selected indications.

Asia Pacific Photoacoustic Imaging Market Trends and Insights

The Asia Pacific region is emerging as a dynamic and fast-growing market for photoacoustic imaging, supported by expanding healthcare infrastructure, rising research output, and increasing investment in advanced medical technologies across China, Japan, India, and ASEAN countries. Large academic hospitals and universities in China and Japan are active in optoacoustic research, developing novel probes, contrast agents, and imaging configurations for both preclinical and clinical use. Governments across the region are promoting high-tech medical equipment manufacturing and translational research, which benefits companies involved in photoacoustic systems, lasers, and ultrasound components.

In China, the rising incidence of cancer and cardiovascular diseases, coupled with significant government funding for medical innovation, drives interest in radiation-free and functionally rich imaging modalities. Japan’s strength in precision engineering and ultrasound technologies creates natural synergies for hybrid ultrasound-photoacoustic platforms. In India and parts of ASEAN, adoption is currently concentrated in top-tier academic and research centers, but growing private healthcare investments and medical tourism could support broader uptake over the forecast horizon. Overall, Asia Pacific is expected to record the fastest growth rate globally, as local manufacturing capabilities mature and more systems are installed in research institutions and tertiary care hospitals.

Competitive Landscape

The photoacoustic imaging market is characterized by a moderately concentrated yet innovation-driven competitive landscape. Market participants compete primarily on technological differentiation, image resolution, system integration with ultrasound, and depth-penetration capabilities. Strong emphasis is placed on R&D to enhance multispectral imaging, real-time visualization, and clinical usability. Entry barriers remain high due to complex system design, regulatory requirements, and high capital investment. Strategic collaborations with research institutes and hospitals are common to validate clinical applications.

Key Developments:

- In June 2025, Verasonics, Inc., a leader in research ultrasound, announced a partnership with PhotoSound® Technologies, Inc. of Houston, Texas, to offer customers the PhotoSound Legion™ AMP for use with Vantage® and Vantage NXT Research Ultrasound Systems. The partnership expanded Vantage customers’ capabilities by integrating the Legion AMP128, enabling applications in photoacoustic imaging, thermoacoustic imaging, radiation therapy monitoring, and other advanced imaging uses.

Companies Covered in Photoacoustic Imaging Market

- FUJIFILM VisualSonics Inc

- iThera Medical GmbH

- Seno Medical Instruments Inc

- TomoWave Laboratories, Inc.

- Endra Life Sciences Inc.

- Aspectus GmbH

- InnoLas Laser GmbH

- PhotoSound Technologies Inc.

- Verasonics, Inc.

- Advantest Corporation

- Kibero GmbH

- Vibronix, Inc.

- illumiSonics Inc.

- Canon Medical Systems Corporation

- Siemens Healthineers AG

Frequently Asked Questions

The global photoacoustic imaging market is expected to reach approximately US$ 121.2 million in 2026.

Key demand drivers include the rising global burden of cancer and cardiovascular disease, growing interest in non-ionizing and hybrid imaging modalities, and the need for high-resolution functional information on oxygenation and vascularity.

North America leads the photoacoustic imaging market, with an estimated 41% share in 2025, supported by strong NIH-funded research, advanced academic medical centers, high healthcare expenditure, and early clinical adoption of hybrid ultrasound-photoacoustic systems, especially in oncology and vascular imaging applications.

A major growth opportunity lies in expanding applications in oncology, neurology, cardiology, and preclinical research through advanced software, AI-based analytics, and specialized probes. These developments will deepen the use of photoacoustic imaging for functional and molecular diagnostics, therapy monitoring, and translational research, driving demand for both imaging systems and high-margin software & accessories.

Leading companies include FUJIFILM VisualSonics Inc., iThera Medical GmbH, Seno Medical Instruments, Inc., TomoWave Laboratories, Inc., Endra Life Sciences Inc.