- Nutraceuticals & Functional Foods

- Oryzanol Market

Oryzanol Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Oryzanol Market by Product Type (Gamma Oryzanol, Ferulic Acid Esters, and Others), by Source (Rice Bran Oil, Wheat Bran, Fruits & Vegetables, and Others), by Application (Pharmaceuticals, Nutraceuticals & Dietary Supplements, Food & Beverages, Cosmetics & Personal Care, and Animal Feed) End-user, and Regional Analysis from 2026 - 2033

Oryzanol Market Share and Trend Analysis

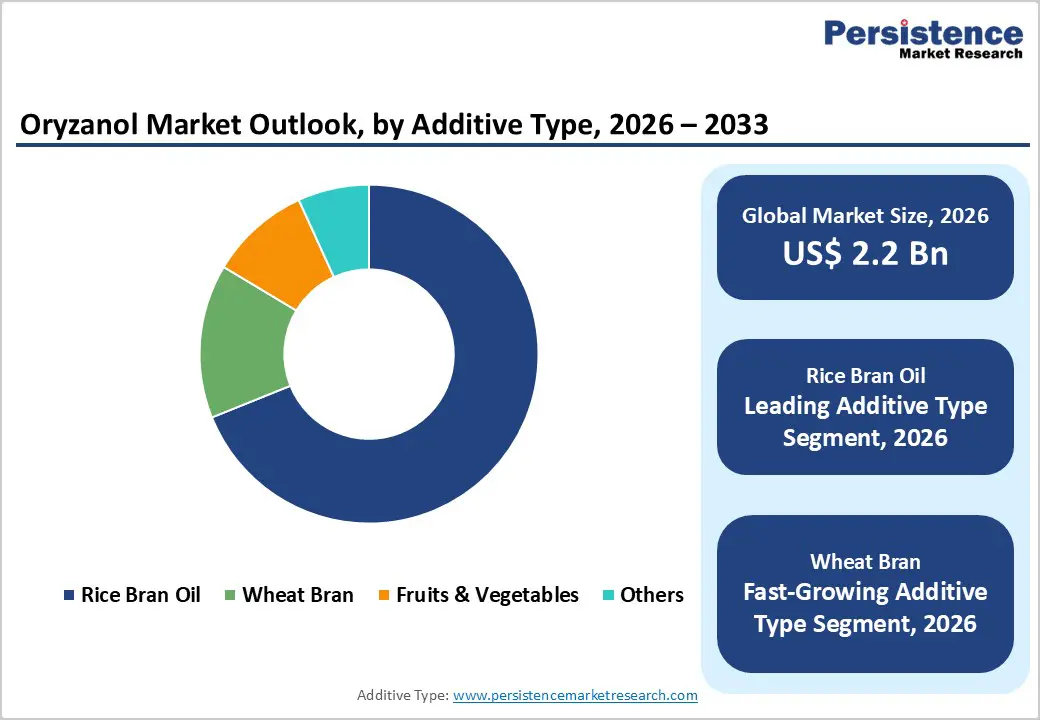

The global oryzanol market size is estimated to grow from US$ 2.2 billion in 2026 to US$ 3.6 billion by 2033 and is projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033. Shifting consumer focus toward plant-based bioactives and scientifically backed wellness ingredients is significantly boosting the adoption of oryzanol across global markets.

Derived primarily from rice bran oil, oryzanol is increasingly used for its cholesterol-lowering, antioxidant, and anti-inflammatory properties. Manufacturers are integrating this compound into nutraceuticals, functional foods, and personal care products to enhance product efficacy while maintaining a natural positioning. Its role in supporting cardiovascular health and metabolic balance has strengthened its appeal among health-conscious consumers.

Rising awareness regarding preventive healthcare, coupled with growing demand for clean and sustainable ingredients, is encouraging companies to expand their portfolios with oryzanol-based formulations. Additionally, improvements in extraction and purification technologies are enabling higher potency and better bioavailability, making it more effective across applications. The increasing penetration of dietary supplements and fortified products, especially in developing economies, continues to reinforce their market relevance.

Key Industry Highlights:

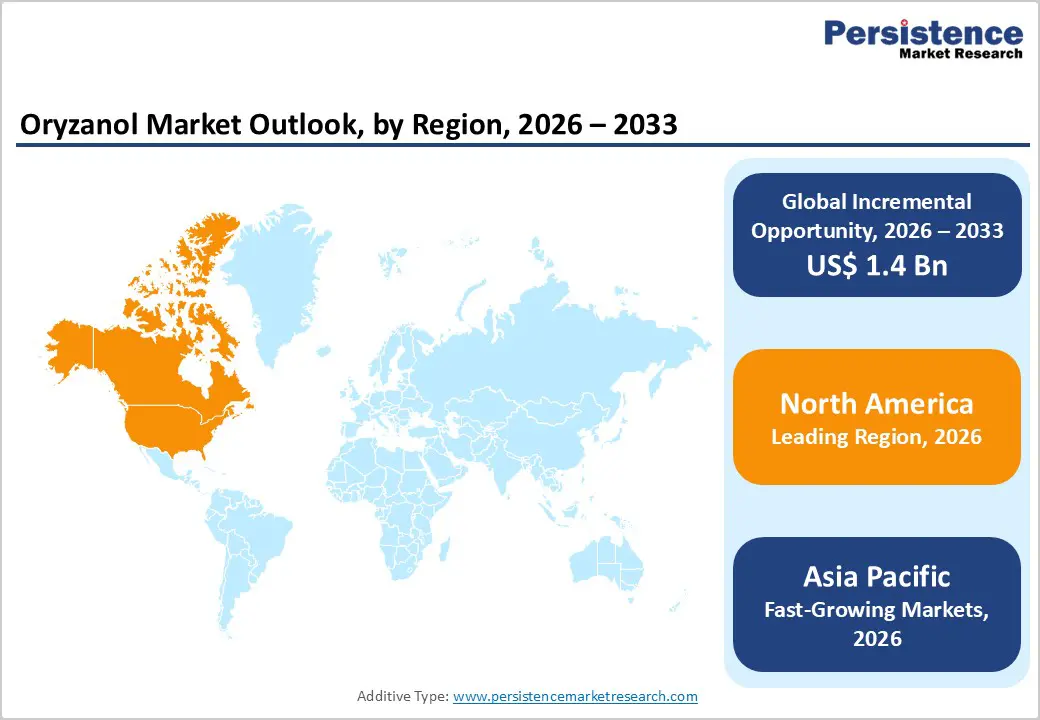

- Leading Region: North America accounts for 46.7% of the market, supported by a well-established nutraceutical sector, high consumer awareness, and strong demand for plant-derived functional ingredients.

- Fastest-Growing Region: Asia Pacific is expanding rapidly, driven by abundant rice bran availability, rising health awareness, and increasing adoption of dietary supplements in emerging economies.

- Leading Product Type Segment: Gamma oryzanol dominates due to its high purity, proven health benefits, and widespread use across nutraceutical and pharmaceutical applications. Fastest-Growing Product Type Segment: Ferulic acid esters are gaining momentum as demand for advanced antioxidant compounds with enhanced functional properties increases.

- Leading Application Segment: Nutraceuticals & Dietary Supplements (41.8%) – driven by strong demand for preventive healthcare, cholesterol management, and plant-based bioactive supplementation.

- Fastest-Growing Application Segment: Pharmaceuticals are witnessing steady growth, driven by increasing clinical adoption in cholesterol management, rising prevalence of cardiovascular disorders, and growing demand for plant-derived bioactive compounds in therapeutic formulations.

| Key Insights | Details |

|---|---|

|

Oryzanol Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 3.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1 % |

Market Dynamics

Driver - Increasing Adoption of Plant-Derived Bioactives and Preventive Healthcare Trends

A key force driving growth is the rising consumer shift toward plant-based bioactive compounds that support long-term health and wellness. Oryzanol, primarily extracted from rice bran oil, has gained considerable traction due to its clinically supported benefits in cholesterol reduction, antioxidant activity, and hormonal balance. Growing prevalence of lifestyle-related disorders, including cardiovascular diseases and metabolic syndromes, has encouraged consumers to adopt preventive healthcare approaches, significantly boosting demand for functional ingredients in daily nutrition. Additionally, the expanding nutraceutical and dietary supplement industry is accelerating product incorporation, as manufacturers seek ingredients with both therapeutic potential and natural origin. Consumers are increasingly scrutinizing product compositions, favoring supplements with scientifically backed, plant-derived constituents over synthetic alternatives.

Furthermore, advancements in extraction technologies have enabled the production of high-purity oryzanol with improved bioavailability, further enhancing its commercial viability. Regulatory support for nutraceutical ingredients in key markets has also contributed to widespread acceptance. With increasing investments in clinical research and product innovation, manufacturers are actively positioning oryzanol as a multifunctional ingredient across supplements, fortified foods, and personal care products. These combined factors are reinforcing its role as a preferred bioactive compound in health-focused applications globally.

Restraints - High Production Costs and Limited Functional Awareness Across End Users

Despite favorable growth trends, certain constraints continue to limit broader market penetration. One of the primary challenges lies in the relatively high production cost associated with oryzanol extraction and purification. The process requires advanced technologies to isolate and stabilize the compound from rice bran oil, resulting in higher operational expenses than for other functional ingredients. This cost factor often restricts adoption, particularly among small and mid-scale manufacturers with limited R&D budgets. Another significant barrier is the limited awareness of oryzanol’s benefits across certain consumer segments and industrial end users. While it is well-recognized in niche nutraceutical and pharmaceutical applications, its utilization in mainstream food and beverage formulations remains comparatively low. This gap is further compounded by competition from alternative bioactive ingredients such as phytosterols and omega fatty acids, which are more widely marketed and understood.

Additionally, variability in raw material quality and supply chain inefficiencies can impact product consistency and pricing. Regulatory differences across regions regarding health claims and ingredient classification also create complexities for global manufacturers. These challenges collectively hinder large-scale adoption, requiring focused efforts in cost optimization, consumer education, and standardized regulatory frameworks to unlock full market potential.

Opportunity - Expanding Scope in Functional Foods, Cosmetics, and Emerging Economies

A significant growth avenue lies in the increasing integration of bioactive compounds into functional foods and personal care formulations. Oryzanol is gaining prominence as a multifunctional ingredient in fortified food products, beverages, and skincare applications due to its antioxidant and anti-aging properties. In the cosmetics sector, it is widely used for UV protection, skin conditioning, and anti-inflammatory benefits, making it an attractive component in premium formulations.

Emerging economies present substantial untapped potential, driven by rising disposable incomes, urbanization, and growing health awareness. Consumers in these regions are gradually shifting toward value-added products that offer both nutritional and functional benefits. This transition is encouraging manufacturers to introduce innovative offerings incorporating oryzanol across diverse applications. Technological advancements in extraction and formulation are further enhancing product efficiency, enabling the development of more stable and bioavailable variants.

Moreover, the growing emphasis on sustainable sourcing, particularly from rice bran a byproduct of rice milling supports circular economy practices and strengthens the ingredient’s environmental appeal. Strategic collaborations, expanding distribution networks, and targeted marketing initiatives are expected to further accelerate adoption, positioning oryzanol as a high-potential ingredient across multiple high-growth industries.

Category-wise Analysis

By Product Type Insights

Gamma oryzanol is expected to retain its leading position in the global oryzanol market in 2026, capturing 72.6% of total revenue. Its dominance is attributed to its well-documented bioactive profile, particularly its antioxidant, cholesterol-lowering, and anti-inflammatory effects. Derived primarily from rice bran oil, gamma oryzanol offers high purity and consistent efficacy, making it a preferred choice across nutraceutical and pharmaceutical formulations. Increasing consumer inclination toward plant-derived functional compounds has further strengthened its adoption. Additionally, its stability under varying processing conditions enhances its usability in food applications. Compared to other derivatives, gamma oryzanol benefits from stronger clinical backing and broader regulatory acceptance, supporting its extensive commercialization. As demand for preventive healthcare solutions rises globally, this segment continues to gain traction due to its alignment with health-focused product innovation and natural ingredient positioning.

By Application Insights

The nutraceuticals and dietary supplements segment is projected to hold the largest share in 2026, contributing 41.8% of total revenue. This leadership is driven by increasing consumer awareness regarding cardiovascular health, cholesterol management, and overall wellness. Oryzanol is widely incorporated into supplements due to its proven efficacy in reducing LDL cholesterol and supporting metabolic health. The shift toward preventive healthcare, especially among aging populations, has significantly boosted demand for bioactive compounds like oryzanol.

Additionally, the rise of fitness-oriented lifestyles and plant-based supplementation trends has further accelerated adoption. Compared to pharmaceuticals, nutraceutical applications benefit from fewer regulatory constraints and faster product commercialization cycles. Manufacturers are increasingly introducing innovative delivery formats such as capsules, softgels, and fortified foods to enhance consumer accessibility. This expanding application scope continues to reinforce the segment’s dominant position in the global market.

By End-user Insights

Nutraceutical manufacturers are anticipated to account for 24.2% of total market revenue in 2026, establishing them as the leading end-user segment. Their prominence is supported by the rapid expansion of functional food and dietary supplement portfolios targeting heart health, immunity, and metabolic wellness. These manufacturers actively utilize oryzanol as a key ingredient due to its multifunctional benefits and compatibility with plant-based formulations.

Growing consumer demand for scientifically backed natural ingredients has encouraged companies to invest in product innovation and clinical validation. Furthermore, the segment benefits from high-volume production and widespread distribution networks across developed and emerging markets. Compared to other end users, nutraceutical companies demonstrate greater agility in responding to evolving consumer trends. Continuous investment in branding, clean-label positioning, and premium product offerings is expected to further strengthen their market leadership over the forecast period.

Regional Insights

North America Oryzanol Market Trends

North America is projected to account for 46.7% of the global oryzanol market value in 2026, with the U.S. serving as the primary growth engine. The region’s leadership is supported by a mature food processing industry that places strong emphasis on ingredient transparency and product labeling. Consumers increasingly demand recognizable, non-GMO, and minimally processed ingredients, prompting manufacturers to shift toward clean label starch solutions. Regulatory oversight by authorities such as the FDA has further reinforced the need for clear labeling practices, accelerating product reformulation initiatives.

In addition, large food corporations are investing heavily in R&D to develop starches that maintain performance under varying processing conditions while meeting clean label standards. The growing popularity of organic and plant-based foods has also contributed to increased utilization of native and specialty starches. Retailers and private label brands are playing a pivotal role by promoting clean ingredient positioning. Furthermore, advancements in supply chain traceability and sourcing transparency are strengthening consumer trust, ensuring sustained demand across multiple food categories in the region.

Europe Oryzanol Market Trends

Europe represents a highly regulated and quality-focused market, characterized by strong consumer awareness regarding food ingredients and sustainability. Key countries including Germany, France, the Netherlands, Spain, and the United Kingdom are major contributors, supported by well-established food manufacturing sectors. The region has been at the forefront of clean label adoption, driven by strict regulations governing food additives and labeling practices. As a result, manufacturers are increasingly replacing chemically modified starches with natural alternatives to comply with evolving standards.

Consumer preference for organic, non-GMO, and sustainably sourced products continues to shape market dynamics, encouraging the use of plant-based starches derived from sources such as potato and wheat. Additionally, the European food industry emphasizes environmental responsibility, prompting investments in sustainable sourcing and production techniques. Collaboration between ingredient suppliers and food manufacturers has accelerated innovation in functional clean label solutions. Ongoing efforts to reduce carbon footprint and improve supply chain efficiency further support market expansion, positioning Europe as a key hub for clean label ingredient development.

Asia Pacific Oryzanol Market Trends

Asia Pacific is expected to be the fastest-growing region, expanding at a CAGR of approximately 7.3% between 2026 and 2033. Growth is fueled by rapid urbanization, rising disposable incomes, and increasing consumption of processed and convenience foods. Countries such as China and India are at the forefront, supported by expanding food processing industries and evolving dietary preferences. As awareness regarding food safety and ingredient quality increases, consumers are gradually shifting toward products with simplified and natural ingredient lists.

The region is witnessing significant investments in domestic manufacturing capabilities, enabling large-scale production of clean label starch from diverse raw materials such as tapioca and rice. Additionally, multinational companies are expanding their presence to tap into the growing demand for premium and health-oriented food products. Government initiatives aimed at improving food quality standards and encouraging local production further support market growth. The rising influence of western dietary patterns, combined with increasing demand for packaged foods, continues to accelerate adoption, making Asia Pacific a high-potential market for clean label starch.

Competitive Landscape

The global oryzanol market is highly competitive, with strong participation from Fengchen Group Co., Ltd., NutriScience Innovations, LLC., Merck KGaA, Ricela Health Foods Ltd., Oryza Oil & Fat Chemical Co., Ltd., and Tano Biotech. These companies leverage advanced extraction technologies, functional ingredient expertise, and integrated supply chains to strengthen their market presence while enhancing product efficacy, bioavailability, and stability across nutraceutical, pharmaceutical, and food applications. Rising demand for plant-based antioxidants is accelerating innovation, with manufacturers expanding production capacities, ensuring regulatory compliance, and investing in R&D to develop high-purity oryzanol solutions for diverse industrial and health-focused applications globally.

Key Industry Developments:

- In March 2026, researchers at the University of Arkansas at Pine Bluff (UAPB) identified that a rice bran–derived compound, delivered using nanotechnology, may enhance cellular protection against age-related damage, indicating a promising strategy to improve the bioavailability and efficacy of food-based bioactives.

- In July 2025, KRBL, the parent company of India Gate Basmati Rice, entered the edible oil segment with the launch of India Gate Uplife, a health-focused brand targeting digestive wellness. The initial portfolio features two blended oil variants Uplife Weight Watchers and Uplife Gut Pro reflecting the company’s strategic move to diversify into a multi-category, multi-brand FMCG business.

Companies Covered in Oryzanol Market

- Fengchen Group Co., Ltd.

- NutriScience Innovations, LLC

- Merck KGaA

- Ricela Health Foods Ltd.

- Oryza Oil & Fat Chemical Co., Ltd.

- Tano Biotech

- Tokyo Chemical Industry Co., Ltd.

- Kangcare Bioindustry Co., Ltd.

- Source Naturals, Inc.

- Swanson Health Products, Inc.

- FUJIFILM Wako Pure Chemical Corporation

- Xi'an Gaoyuan Bio-Chem Co., Ltd.

- Shaanxi Pioneer Biotech Co., Ltd.

- Puyer Group

- Sure Chemicals Co., Ltd.

- Others

Frequently Asked Questions

The global oryzanol market is projected to be valued at US$ 49.8 Bn in 2026.

Rising consumer demand for natural, clean-label, and additive-free food ingredients along with stringent labeling regulations and growing health consciousness are driving market growth.

The global oryzanol market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Expansion into plant-based foods, emerging markets, and non-food applications (pharma, cosmetics) along with technological innovations in starch processing creates significant growth opportunities.

Fengchen Group Co., Ltd., NutriScience Innovations, LLC., Merck KGaA, Ricela Health Foods Ltd., Oryza Oil & Fat Chemical Co., Ltd., and Tano Biotech some of the key players in the oryzanol market.