- Specialty & Fine Chemicals

- Oil & Gas Security and Service Market

Oil & Gas Security and Service Market Size, Share, and Growth Forecast 2026 - 2033

Oil & Gas Security and Service Market by Component (Risk Assessment & Consulting, Surveillance & Monitoring Services, Manned Guarding Services, Emergency Response & Crisis Management, Cybersecurity Services, Asset Integrity & Infrastructure Protection, Logistics & Escort Services, Training & Security Management), Security Type (Physical Security, Cybersecurity, Operational Security, Environmental & Safety Security), Sector (Upstream, Midstream, Downstream), Application (Exploring and Drilling, Transportation, Pipelines, Distribution and Retail Services, Others), by Regional Analysis, 2026 - 2033

Oil & Gas Security and Service Market Size and Trend Analysis

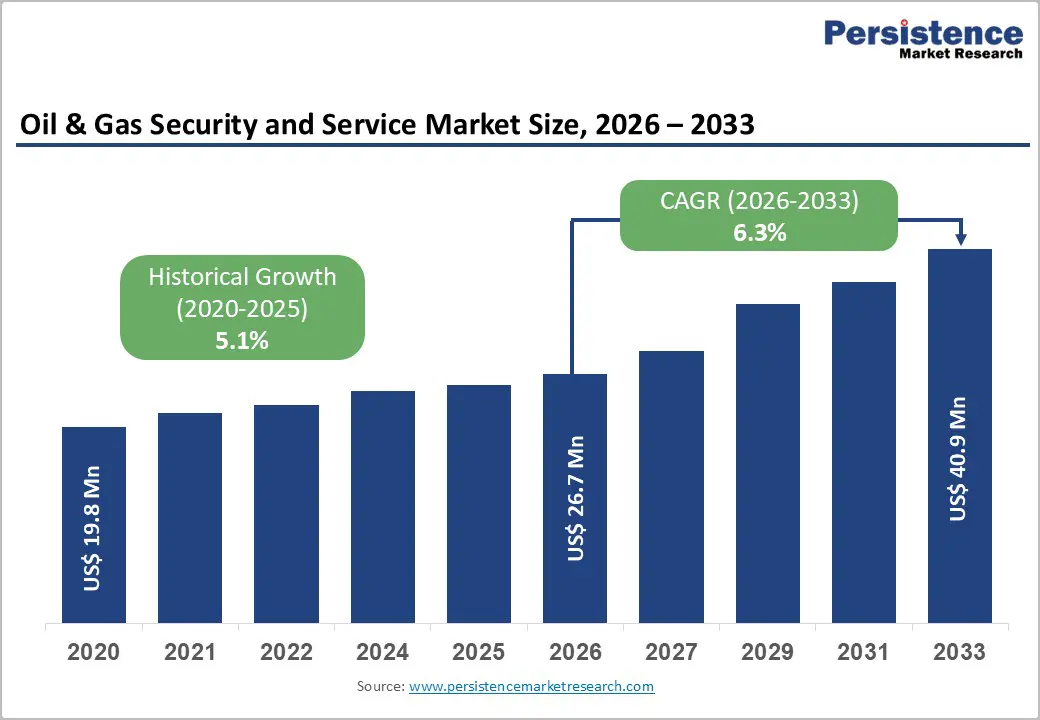

The global Oil & Gas Security and Service market size is expected to be valued at US$ 26.7 Billion in 2026 and projected to reach US$ 40.9 Billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. The rise in geopolitical tensions, rising frequency of cyberattacks on critical energy infrastructure, and expanding offshore and onshore oil and gas exploration activities are the principal forces driving consistent security services market growth.

The increasing digitalization of oil and gas operations, encompassing Industrial IoT (IIoT), SCADA systems, and cloud-connected operational technology (OT) environments, has dramatically expanded the attack surface for both physical and cyber threats, compelling operators to invest in integrated, multi-layered security solutions. According to the U.S. Cybersecurity and Infrastructure Security Agency (CISA), the energy sector remains among the most targeted critical infrastructure categories globally, with oil and gas pipelines, refineries, and LNG terminals facing an average of over 1,000 cyberattack attempts per week. Simultaneously, expanding production activity in the Middle East, West Africa, and deepwater Gulf of Mexico is generating sustained demand for manned guarding, surveillance, and emergency response services in operationally challenging environments.

Key Industry Highlights:

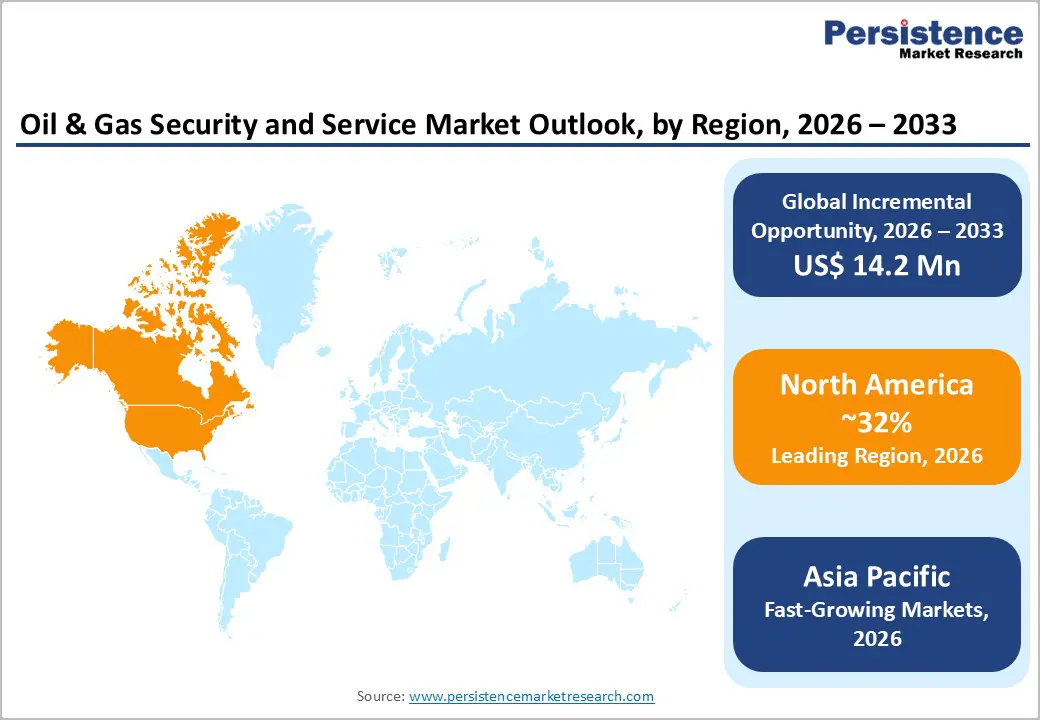

- Leading Region: North America commands approximately 32% of global Oil & Gas Security and Service market revenue in 2025, underpinned by the U.S.'s position as the world's largest oil producer and mandatory security frameworks under TSA Security Directives and CISA critical infrastructure protection mandates.

- Fastest Growing Region: Asia Pacific is projected to grow at a CAGR of 7.8% during 2026–2033, driven by expanding LNG import infrastructure, offshore production growth in the South China Sea, and new cybersecurity mandates from Japan's METI and India's NCIIPC frameworks.

- Dominant Segment: The Upstream sector leads with approximately 45% of global market share in 2025, driven by IEA-reported US$ 570 billion in global upstream investment in 2023, requiring comprehensive physical, cyber, and emergency response security across remote and high-risk production environments.

- Fastest Growing Segment: Cybersecurity Services is the fastest growing component, driven by TSA pipeline cybersecurity directives, EU NIS2 compliance requirements, and Dragos Inc. reporting 17 active threat groups targeting oil and gas OT/ICS systems globally.

- Key Opportunity: The IEA's projected 200+ MTPA of new LNG export capacity by 2030, combined with AI-driven security operations center (SOC) solutions delivering million-event-per-second threat monitoring, creates a multi-billion-dollar, long-duration security services opportunity for integrated technology providers.

| Key Insights | Details |

|---|---|

|

Oil & Gas Security and Service Market Size (2026E) |

US$ 26.7 Billion |

|

Market Value Forecast (2033F) |

US$ 40.9 Billion |

|

Projected Growth CAGR (2026–2033) |

6.3% |

|

Historical Market Growth (2020–2025) |

5.1% CAGR |

Market Dynamics

Drivers - Surging OT/ICS Cybersecurity Threats Targeting Oil and Gas Critical Infrastructure

The convergence of Information Technology (IT) and Operational Technology (OT) in modern oil and gas facilities has created unprecedented cybersecurity vulnerabilities. The Colonial Pipeline ransomware attack in May 2021, which disrupted fuel supply across the U.S. East Coast and triggered a US$ 4.4 million ransom payment, served as a watershed event, compelling governments and operators globally to dramatically accelerate OT cybersecurity investment. The U.S. Transportation Security Administration (TSA) subsequently issued mandatory pipeline cybersecurity directives requiring incident reporting, vulnerability assessments, and the designation of cybersecurity coordinators. Dragos Inc.'s 2024 ICS/OT Cybersecurity Year in Review reported that 17 threat groups actively targeted industrial infrastructure globally, with oil and gas among the highest-priority sectors. This threat landscape is directly translating into surging procurement of OT-specific intrusion detection, network segmentation, and incident response services from providers including Honeywell, Cisco, and Siemens.

Expanding Global Upstream Exploration Activity and Remote Asset Security Requirements

Renewed capital investment in upstream oil and gas exploration and production, particularly in deepwater, ultra-deepwater, and remote onshore environments, is generating substantial new demand for physical security, manned guarding, and emergency response services. According to the International Energy Agency (IEA), global upstream oil and gas investment reached US$ 570 billion in 2023, a 9% year-on-year increase, with significant activity in the Gulf of Mexico, Guyana, Brazil's pre-salt basins, and East Africa. Remote exploration assets operating in conflict-affected or high-crime regions require comprehensive, integrated security packages that combine surveillance technology, armed escort, emergency medical response, and crisis management, generating high per-asset revenue for security service providers. International SOS and Securitas AB have both expanded their energy sector specialist capabilities in response to this geographic diversification of global upstream activity.

Restraints - Volatile Oil Price Cycles Creating Unpredictable Security Budget Allocation

The oil and gas industry's well-documented exposure to commodity price volatility creates inherent cyclicality in security services procurement. Brent crude price oscillations, ranging from negative values in April 2020 to over US$ 120 per barrel in June 2022, directly impact upstream capital and operating expenditure budgets, with security services often among the first cost-reduction targets in low-price environments. The IEA's World Energy Outlook 2024 projects continued uncertainty in oil demand through 2030 as the energy transition accelerates, creating planning challenges for security service providers dependent on multi-year contract renewals tied to operator capital spending cycles.

Shortage of Specialized OT Cybersecurity Talent for Oil and Gas Environments

The intersection of oil and gas process engineering knowledge with industrial cybersecurity expertise represents one of the scarcest talent categories globally. The World Economic Forum (WEF) estimates a global shortfall of 3.5 million cybersecurity professionals by 2025, with OT-specialized practitioners, capable of understanding SCADA, DCS, and safety instrumented systems in oil and gas environments, representing a small fraction of this already scarce pool. This talent constraint limits the pace at which security service providers can scale OT cybersecurity engagements, particularly for brownfield upstream and midstream assets requiring specialized operational knowledge.

Opportunities - AI and Machine Learning-Powered Threat Intelligence for Oil and Gas Critical Infrastructure

The integration of AI and machine learning into oil and gas security monitoring platforms represents the market's most transformative growth opportunity. AI-powered security operations centers (SOCs) can analyze millions of OT network events per second, identifying anomalous patterns indicative of cyberattacks or physical intrusion attempts with accuracy rates that significantly exceed those of manual analyst review. Honeywell's Forge Cybersecurity Suite and Schneider Electric's EcoStruxure Security platform both incorporate AI-driven anomaly detection for industrial control system monitoring. The U.S. Department of Energy (DOE) allocated US$ 70 million in 2023 for AI-enabled energy infrastructure cybersecurity research under its Cybersecurity, Energy Security, and Emergency Response (CESER) program. As oil and gas operators deploy AI-powered digital twins and autonomous monitoring systems, the demand for AI-integrated security solutions capable of protecting these intelligent operational environments will compound significantly through the forecast period.

Growing Demand for Integrated Security-as-a-Service for LNG and Offshore Wind-Gas Hybrid Assets

The rapid global expansion of liquefied natural gas (LNG) export infrastructure, with the IEA projecting over 200 million tonnes per annum (MTPA) of new LNG export capacity additions by 2030, is creating a high-value, long-lifecycle security service opportunity. LNG terminals, FLNG vessels, and associated pipeline infrastructure represent among the highest-consequence security environments in the energy sector, requiring continuously staffed integrated security programs covering cybersecurity, physical perimeter protection, maritime patrol, and emergency response. In 2024, BAE Systems expanded its energy infrastructure protection practice, targeting Middle East and Australian LNG operators. Lockheed Martin and Motorola Solutions are also positioning integrated command-and-control security platforms specifically for LNG terminal operators, combining video analytics, perimeter intrusion detection, and communication systems into unified managed security service contracts.

Category-wise Analysis

Component Insights

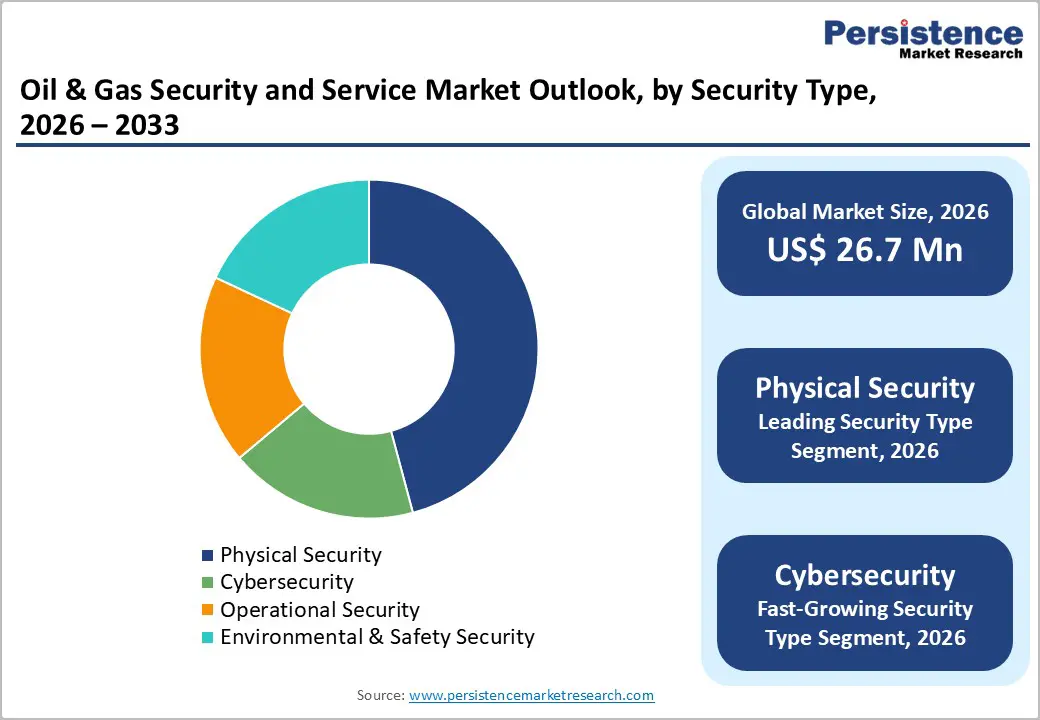

Cybersecurity Services is the leading component segment in the global Oil & Gas Security and Service market, commanding approximately 28% of total market share in 2025. The escalating frequency and sophistication of cyberattacks targeting oil and gas OT environments, including the Colonial Pipeline attack (2021) and the Saudi Aramco Shamoon malware incidents, have elevated cybersecurity from a discretionary to a mandatory operational expenditure across all oil and gas subsectors. The U.S. TSA and EU Network and Information Security (NIS2) Directive have both expanded mandatory cybersecurity requirements for energy sector operators, creating non-discretionary procurement. Surveillance & Monitoring Services is the fastest-growing component, driven by AI-powered video analytics and IoT sensor deployment across remote upstream and midstream infrastructure globally.

Security Type Insights

Physical Security remains the dominant security type in the global Oil & Gas Security and Service market, accounting for approximately 42% of total market share in 2025. The oil and gas sector operates in a uniquely hazardous and geographically dispersed physical infrastructure, spanning offshore platforms, onshore well sites, cross-country pipeline networks spanning thousands of kilometers, and high-value refinery complexes, all requiring continuous physical protection. Manned guarding, perimeter surveillance, access control, and physical response capabilities represent the foundational security layer on which all other security services are built. In high-risk operating environments including Nigeria, Iraq, and Libya, physical security may constitute over 60% of total site security expenditure. Cybersecurity is the fastest-growing security type, expanding at an above-market CAGR as OT/IT convergence in digital oil fields accelerates the attack surface.

Sector Insights

The Upstream sector is the leading segment in the global Oil & Gas Security and Service market, representing approximately 45% of total revenue share in 2025. Upstream operations, encompassing exploration, drilling, and production, present the most complex and costly security requirements within the oil and gas value chain. Remote offshore platforms and onshore exploration sites in politically unstable regions require comprehensive multidimensional security packages that integrate physical protection, drone surveillance, emergency medical response, and crisis management capabilities. The IEA's reported US$ 570 billion in global upstream investment in 2023 directly correlates with proportional security services procurement. Midstream is the fastest-growing sector, propelled by expanding LNG infrastructure, cross-border pipeline security requirements, and mandatory pipeline cybersecurity frameworks following high-profile ransomware attacks.

Application Insights

Pipelines represent the leading application segment in the global Oil & Gas Security and Service market, accounting for approximately 30% of total revenue share in 2025. Pipeline networks constitute among the most extensive and geographically dispersed critical infrastructure assets in the energy sector, with the U.S. alone operating over 3.3 million kilometers of pipeline according to the U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA). This vast network requires continuous monitoring against physical interference, unauthorized access, and increasingly, cybersecurity threats to SCADA pipeline management systems. Post-Colonial Pipeline attack mandates have significantly elevated per-kilometer security spending. Exploring and Drilling is the fastest-growing application, driven by the expansion of deepwater and frontier exploration programs requiring integrated security services in operationally challenging and geopolitically complex environments.

Regional Insights

North America Oil & Gas Security and Service Market Trends and Insights

North America is the leading regional market for oil and gas security and services, commanding approximately 32% of global revenue share in 2025, driven by the world's largest oil and gas production base and its increasingly stringent cybersecurity regulatory framework. The U.S. TSA's Security Directives for pipeline operators, mandating incident reporting, implementing cybersecurity measures, and conducting annual cybersecurity assessment reviews, have created a defined, recurring compliance-driven market for OT security services. The U.S. Department of Homeland Security (DHS) and CISA jointly publish annual energy sector threat assessments that drive security investment prioritization across major operators, including ExxonMobil, Chevron, and ConocoPhillips.

The rapid expansion of U.S. LNG export capacity, with facilities including Sabine Pass, Corpus Christi, and Freeport LNG operating and multiple new terminals under development, is generating high-value, long-duration physical and cybersecurity service contracts. Canada's expanding Trans Mountain Pipeline system and Alberta oil sands infrastructure similarly require integrated security programs. Technology providers, including Honeywell, Cisco, and Motorola Solutions, maintain their strongest energy security market positions in North America through established OEM and managed services relationships with major operators.

Europe Oil & Gas Security and Service Market Trends and Insights

Europe's oil and gas security market has been significantly reshaped by the post-2022 energy security crisis triggered by Russia's invasion of Ukraine, which elevated critical energy infrastructure protection to the top of national security agendas across EU member states. The EU NIS2 Directive, which became enforceable in October 2024, classifies oil and gas infrastructure as essential entities subject to mandatory cybersecurity risk management measures, vulnerability assessments, and incident reporting obligations. Germany, as Europe's largest industrial gas consumer, and the United Kingdom, as the North Sea's dominant oil and gas producer, are the region's highest-spending markets for security services.

The deliberate sabotage of the Nord Stream pipelines in September 2022 catalyzed unprecedented investment in submarine pipeline monitoring, physical infrastructure protection, and emergency response capabilities across the Baltic and North Sea regions. Norway's Equinor and TotalEnergies France have both significantly increased their procurement of security services following these events. Spain's role as an LNG regasification hub, with the largest LNG terminal capacity in Europe, positions it as a growing security services demand center as energy imports increase. BAE Systems and Siemens are among the key security services providers expanding their practices in European energy infrastructure protection.

Asia Pacific Oil & Gas Security and Service Market Trends and Insights

Asia Pacific is the fastest-growing regional market for oil and gas security and services, projected to register a CAGR of 7.8% during 2026–2033, driven by rapidly expanding LNG import infrastructure, growing offshore production in the South China Sea and Bay of Bengal, and escalating cybersecurity threats to national energy systems. China National Petroleum Corporation (CNPC) and CNOOC are significantly scaling cybersecurity investments following multiple state-attributed cyberattacks on Chinese energy infrastructure. Japan's Ministry of Economy, Trade and Industry (METI) issued revised critical infrastructure cybersecurity guidelines in 2024, covering LNG terminals and oil refineries, driving increased procurement of compliance-related security services.

India's rapidly expanding refining capacity, with Indian Oil Corporation and Reliance Industries operating some of Asia's largest refinery complexes, and the country's National Critical Information Infrastructure Protection Centre (NCIIPC) framework, are jointly driving security services demand. Indonesia, Malaysia, and Vietnam are expanding offshore gas production programs, each requiring integrated physical and maritime security solutions. Schneider Electric and ABB have both expanded their Asia-Pacific energy cybersecurity and operational security practices, positioning them for the region's accelerating trajectory of security services procurement.

Competitive Landscape

The global oil and gas security and service market exhibits a moderately fragmented structure, comprising technology-driven security solution providers, defense and intelligence contractors, and specialized security service companies operating across multiple protection layers. These include physical infrastructure protection, industrial control system cybersecurity, surveillance systems, and risk management services tailored to upstream, midstream, and downstream energy operations.

Competition in the market is primarily driven by the ability to deliver integrated security solutions that combine operational technology cybersecurity, advanced monitoring systems, and on-ground security services. Providers increasingly focus on deploying AI-enabled surveillance, predictive threat detection, and remote monitoring platforms to enhance asset protection for pipelines, refineries, offshore platforms, and LNG terminals. Strategic priorities include expanding presence in high-risk oil and gas producing regions and developing long-term service contracts with energy operators. In addition, integrated security-as-a-service models are gaining traction, allowing operators to outsource complex security operations while converting large capital investments into predictable operational expenditures supported by managed service agreements and performance-based response frameworks.

Key Developments:

- March 2026: SMX (Security Matters) PLC introduced a molecular-traceability platform that embeds invisible markers in fuels to verify origin, detect adulteration, and track oil and gas products across supply chains using sensors and blockchain-enabled digital records.

- June 2025: Rockwell Automation introduced the SecureOT Solution Suite, designed to strengthen industrial cybersecurity resilience by integrating asset visibility, network monitoring, and threat detection capabilities that help energy and manufacturing operators protect operational technology environments from escalating cyber threats.

Companies Covered in Oil & Gas Security and Service Market

- Cisco Systems, Inc.

- Honeywell International Inc.

- Huawei Technologies Co., Ltd.

- Intel Corporation

- Microsoft Corporation

- NortonLifeLock Inc. (Gen Digital)

- Schneider Electric SE

- Siemens AG

- United Technologies Inc. (RTX Corporation)

- ABB Ltd.

- Lockheed Martin Corporation

- Motorola Solutions, Inc.

- BAE Systems plc

- Securitas AB

- International SOS

- Dragos, Inc.

- Claroty Ltd.

- Palo Alto Networks

Frequently Asked Questions

The global Oil & Gas Security and Service market is expected to reach US$ 26.7 Billion in 2026 and is projected to grow to US$ 40.9 Billion by 2033 at a CAGR of 6.3% during 2026-2033.

The market is driven by rising cybersecurity threats to energy infrastructure, strict regulatory compliance requirements, and increasing global upstream and LNG infrastructure investments.

North America leads the global Oil & Gas Security and Service market, supported by strong oil and gas production, advanced cybersecurity regulations, and the presence of major security technology providers.

The key opportunity lies in AI-powered integrated cybersecurity and physical security solutions for oil, gas, and LNG infrastructure.

Key companies include Honeywell International Inc., Siemens AG, Schneider Electric, BAE Systems plc, Lockheed Martin Corporation, Cisco Systems Inc., ABB Ltd., Motorola Solutions Inc., Securitas AB, and International SOS.