- Pharmaceuticals

- Obesity GLP-1 Market

Obesity GLP-1 Market Size, Share, and Growth Forecast, 2026 - 2033

Obesity GLP-1 Market by Drug Type (Semaglutide, Tirzepatide, Liraglutide & Generics, Orforglipron, CagriSema, Pipeline Dual Agonists, Next-Gen Triple Agonists), Therapeutic Indication (Primary Weight Management, Obesity + Type 2 Diabetes, Obesity + CVD, Obesity + Sleep Apnea, Obesity + Liver Disease (MASH), Obesity + Heart Failure, Obesity + CKD), Route of Administration (Injectable, Oral), and Regional Analysis for 2026 - 2033

Obesity GLP-1 Market Share and Trends Analysis

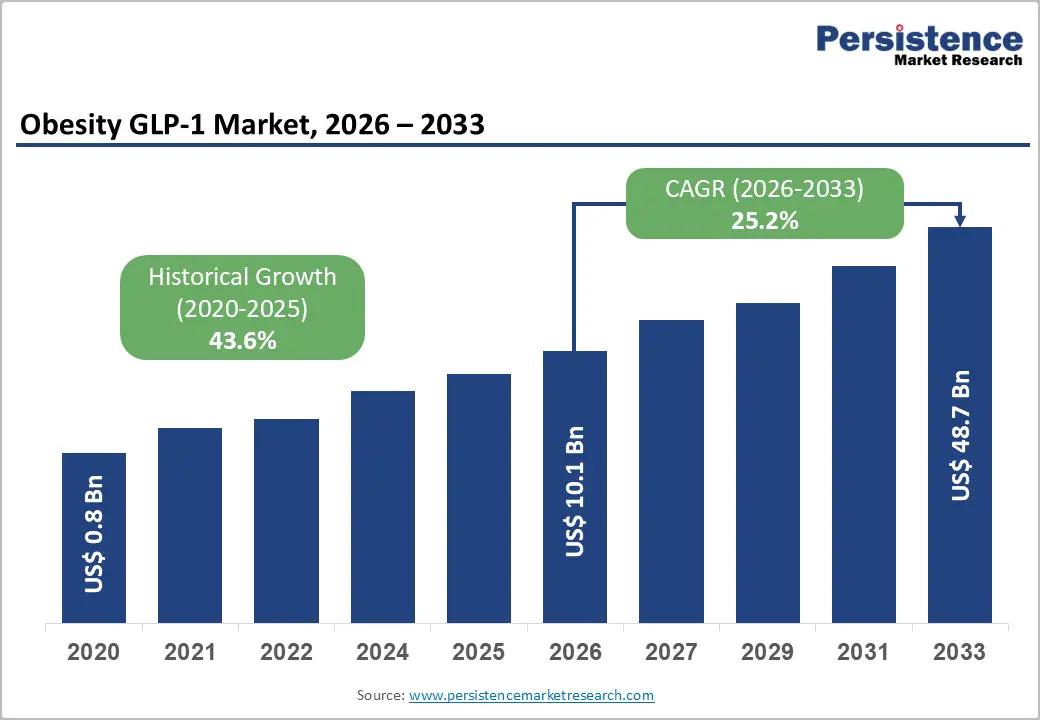

The global obesity GLP-1 market size is likely to be valued at US$ 10.1 billion in 2026, and is projected to reach US$ 48.7 billion by 2033, growing at a CAGR of 25.2% during the forecast period 2026 - 2033.

The market is entering a sustained expansion phase as pharmacological treatment is becoming a central component of obesity management across modern healthcare systems. Clinical studies consistently demonstrate that incretin-based therapies can achieve weight reduction of 10-15% or more of total body weight. These clinical outcomes are encouraging physicians to adopt pharmacotherapy as part of routine obesity treatment rather than relying solely on lifestyle modification programs. According to the World Health Organization (WHO), more than one billion people worldwide are currently living with obesity, highlighting the scale of the potential treatment population. Pharmaceutical companies are therefore expanding research programs focused on incretin-based drugs and increasing production capacity to meet rapidly rising global demand.

Growth is also supported by expanding reimbursement policies, increased physician awareness, and the development of next-generation therapies, such as dual incretin drugs and oral glucagon-like peptide-1 (GLP-1) receptor agonists. Healthcare systems are also recognizing obesity as a chronic metabolic disease that contributes significantly to conditions such as type 2 diabetes, cardiovascular disease (CVD), and metabolic dysfunction. Governments and health authorities are therefore prioritizing obesity management as part of long-term chronic disease prevention strategies. Continued innovation in multi-agonist metabolic drugs will further reshape clinical treatment pathways and expand the long-term potential of the obesity pharmacotherapy market.

Key Industry Highlights

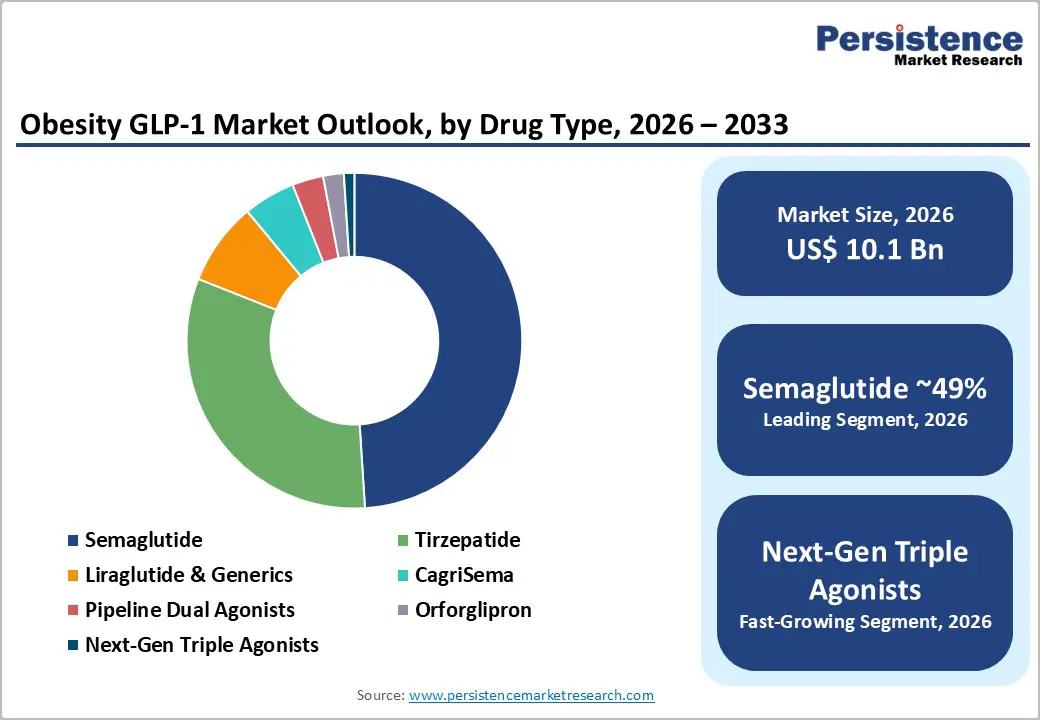

- Dominant Drug Type: Semaglutide-based therapies are projected to account for approximately 49% revenue share in 2026, reflecting their early regulatory approvals and strong clinical efficacy.

- Fastest-growing Drug Type: Next-generation triple-agonist incretin therapies are expected to expand at the highest CAGR of roughly 30% during 2026 - 2033, driven by superior weight-loss outcomes and strong pharmaceutical pipeline investments.

- Dominant Therapeutic Indication: Primary weight management is anticipated to represent nearly 54% of total market demand in 2026, supported by increasing physician recognition of obesity as a chronic disease.

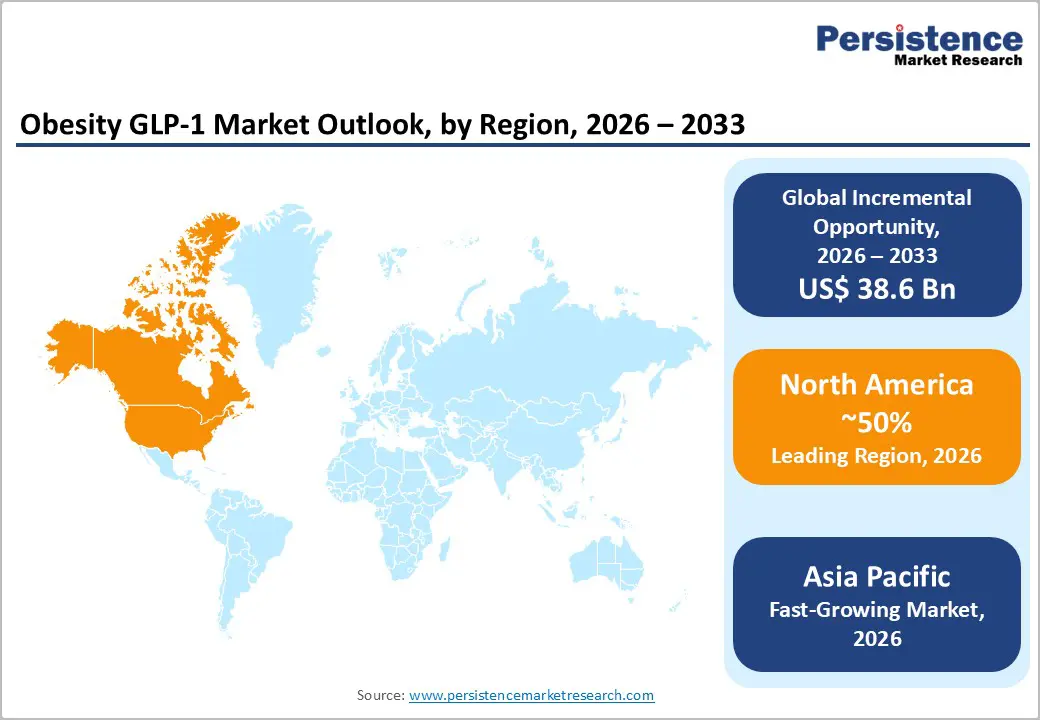

- Regional Leadership: North America is expected to lead with nearly 50% market share in 2026, fueled by high obesity prevalence and strong reimbursement ecosystem.

- Fastest-growing Market: The Asia Pacific market is poised to register the highest 2026 - 2033 CAGR of around 27%, on account of massive pharmaceutical investment across China, India, and Southeast Asia.

- November 2025: Eli Lilly’s obesity and diabetes drug Mounjaro (tirzepatide) became India’s top-selling pharmaceutical brand by value, generating about INR 1 billion (US$ 11.38 million) in monthly sales.

| Key Insights | Details |

|---|---|

| Obesity GLP-1 Market Size (2026E) | US$ 10.1 Bn |

| Market Value Forecast (2033F) | US$ 48.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 25.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 43.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Clinical Reclassification of Obesity as a Chronic Metabolic Disease

Global healthcare systems are increasingly recognizing obesity as a chronic metabolic condition requiring pharmacological intervention. According to WHO data, global obesity prevalence has nearly tripled since 1975, and more than 650 million adults are currently obese. The WHO and the American Medical Association (AMA) have already classified obesity as a disease rather than a lifestyle condition, which is influencing reimbursement policies and treatment guidelines. In September 2025, the WHO added several GLP-1 drugs, including semaglutide and tirzepatide, to its Model List of Essential Medicines to improve global access to therapies used for diabetes and obesity-related conditions. Healthcare systems are therefore prioritizing pharmacological solutions that can reduce downstream costs associated with diabetes, cardiovascular disease, and kidney disease.

Healthcare providers are increasingly prescribing GLP-1 drugs as first-line therapies for medically eligible patients. Clinical trials published in journals such as The New England Journal of Medicine are demonstrating sustained weight loss of more than 15% with semaglutide and up to 22% with tirzepatide. These results are significantly outperforming older anti-obesity medications, which typically produced 5-8% weight loss. As a result, treatment guidelines from organizations such as the American Diabetes Association (ADA) are increasingly incorporating GLP-1 receptor agonists for obesity and cardiometabolic risk management. This shift is expanding the prescription base beyond endocrinology specialists to primary care providers.

Expansion of Incretin Drug Pipelines and Manufacturing Capacity

Pharmaceutical companies are aggressively building development pipelines for incretin-based obesity therapies in order to capture rising global demand for effective metabolic treatments. Research programs are increasingly focusing on advanced hormone-based drugs that target multiple metabolic pathways simultaneously. Industry analyses indicate that more than 80 incretin-based therapies for obesity are currently progressing through various stages of clinical development. These candidates include dual and triple agonist compounds that activate GLP-1, glucose-dependent insulinotropic polypeptide (GIP), and glucagon receptors. As pharmaceutical pipelines continue to grow, the industry is expected to introduce a broader range of therapeutic options that address obesity and its associated metabolic complications.

Manufacturing investments are also increasing rapidly as pharmaceutical companies respond to supply constraints that affected several incretin therapies between 2023 and 2025. The production of peptide-based drugs requires specialized manufacturing infrastructure that supports complex synthesis and purification processes. Major pharmaceutical companies such as Novo Nordisk A/S and Eli Lilly and Company are therefore investing heavily in new production facilities and capacity expansion projects. Novo Nordisk has announced investments exceeding US$ 6 billion to increase the manufacturing capacity for its GLP-1 products at its facility in Denmark. These investments are strengthening global supply chains while reducing production bottlenecks that previously limited product availability.

High Treatment Costs and Reimbursement Limitations

GLP-1 therapies used for obesity management are currently positioned at premium price levels, which is limiting treatment accessibility across several healthcare systems. In the U.S., for instance, the cost of GLP-1 obesity drugs ranges between US$ 900 and US$ 1,300 per patient, according to estimates from the Institute for Clinical and Economic Review (ICER). These pricing structures reflect the high research & development (R&D) investments required to bring innovative peptide-based drugs to market. However, elevated treatment costs are creating financial pressures for both private insurers and public healthcare programs that are evaluating reimbursement coverage. As a result, treatment access remains uneven across different socioeconomic groups and healthcare systems.

Coverage restrictions remain prominent in several countries where public health systems apply strict cost-effectiveness thresholds before approving reimbursement for obesity pharmacotherapy. For example, across Europe, national health authorities are conducting detailed health technology assessments to determine whether incretin-based drugs provide sufficient clinical benefit relative to their cost. These evaluations are influencing reimbursement decisions and shaping market access strategies for pharmaceutical companies.

Supply Chain Constraints and Manufacturing Complexity

GLP-1 therapies for obesity treatment are biologic drugs that require highly specialized manufacturing infrastructure. The production process involves complex peptide synthesis, purification, and formulation steps that must be carried out in tightly controlled pharmaceutical environments. These technical requirements are creating vulnerabilities within the global supply chain, particularly when demand increases faster than manufacturing capacity. The U.S. FDA has reported several shortages of GLP-1 formulations in its drug shortage database during 2023-2024. The demand for incretin-based obesity therapies has expanded rapidly following strong clinical trial results and increasing physician adoption.

Scaling production for peptide-based drugs also requires significant capital investment and long development timelines. Pharmaceutical manufacturing facilities must comply with rigorous Good Manufacturing Practice (GMP) standards that regulate product safety, quality control, and process validation. Building or expanding such facilities typically requires several years of construction, regulatory approval, and operational testing before full production capacity is achieved. As a result, pharmaceutical companies are facing challenges when attempting to align supply levels with rapidly rising global demand for obesity therapies. These constraints are temporarily limiting the availability of certain GLP-1 drugs in several markets and are creating uneven distribution patterns across regions.

Strengthening Healthcare Systems in Developing Markets

Large emerging economies are presenting substantial expansion potential for GLP-1 obesity therapies as demographic and lifestyle transitions are accelerating the prevalence of metabolic disorders. Countries such as China, India, Brazil, and Mexico are experiencing rapid growth in obesity rates as urbanization, processed food consumption, and sedentary work environments are becoming more widespread. The World Obesity Federation (WOF) is projecting that obesity prevalence across Asia Pacific will increase by more than 40 percent by 2035, indicating a rapidly expanding treatment-eligible population that remains largely underserved by pharmacological interventions. Public health systems in these regions are also recognizing obesity as a major contributor to non-communicable diseases such as type 2 diabetes, cardiovascular disease, and fatty liver disease.

Pharmaceutical manufacturers are increasingly positioning emerging markets as strategic expansion zones for obesity-focused GLP-1 therapies. Companies are conducting clinical trials, pursuing regulatory approvals, and establishing commercial partnerships to accelerate product launches in high-growth regions. China alone has more than 100 million adults living with obesity, according to estimates from the National Health Commission of the People's Republic of China (NHC), representing one of the largest potential treatment populations globally. Healthcare spending across emerging economies is also increasing as middle-income populations expand and private health insurance coverage becomes more accessible.

Development of Oral and Multi-Hormone Incretin Therapies

The next phase of obesity pharmacotherapy innovation focuses on oral GLP-1 receptor agonists and multi-hormone metabolic drugs that target multiple biological pathways simultaneously. Pharmaceutical companies are intensifying research and development efforts to improve treatment convenience and clinical efficacy. Organizations such as Eli Lilly and Company and Novo Nordisk A/S are advancing small-molecule oral GLP-1 agonists that are designed to replicate the metabolic benefits of injectable therapies while simplifying drug administration. These oral formulations aim to overcome one of the primary barriers to long-term adherence in obesity management. As a result, pharmaceutical innovation is shifting toward therapies that combine potent metabolic effects with convenient dosing formats.

Oral incretin therapies are gaining strong attention as patient preference is consistently favoring pill-based medications over injectable treatments. Pipeline candidates such as orforglipron are currently progressing through Phase III clinical trials and demonstrating clinically meaningful weight-reduction outcomes. These drugs are expected to broaden the addressable patient population by enabling obesity pharmacotherapy in primary care settings rather than specialized endocrinology clinics. At the same time, pharmaceutical developers are advancing multi-agonist metabolic drugs that simultaneously stimulate GLP-1, GIP, and glucagon receptors. These triple-pathway therapies are designed to enhance energy expenditure while improving appetite regulation and glycemic control.

Category-Wise Analysis

Drug Type Insights

Semaglutide is slated to dominate with approximately 49% of the obesity GLP-1 market revenue share in 2026. The segment is benefiting from extensive clinical validation and early regulatory approvals from agencies such as the U.S. FDA and the European Medicines Agency (EMA). Physicians are increasingly recognizing semaglutide as an effective pharmacological option for chronic weight management because clinical studies are consistently demonstrating meaningful and sustained weight reduction outcomes. The once-weekly administration schedule is simplifying treatment adherence while supporting long-term therapy continuation among patients. Healthcare providers are also integrating semaglutide into broader metabolic care strategies, since obesity is closely linked with cardiometabolic disorders such as type 2 diabetes and cardiovascular disease.

Next-generation triple-agonist therapies are likely to be the fastest-growing drug type between 2026 and 2033, expected to exhibit a CAGR of nearly 30%. These therapies target multiple hormonal pathways simultaneously by activating GLP-1, GIP, and glucagon receptors. Researchers are designing these compounds to enhance appetite regulation, improve insulin sensitivity, and increase energy expenditure through coordinated metabolic signaling. Early clinical trial results are indicating that triple-pathway drugs may deliver greater weight reduction outcomes compared with single-receptor therapies. Pharmaceutical companies are therefore increasing investments in multi-agonist drug development programs to create differentiated metabolic treatments that address complex obesity-related conditions.

Therapeutic Indication Insights

Primary weight management is anticipated to command nearly 54% of the obesity GLP-1 market share in 2026. Growing physician awareness regarding the clinical benefits of GLP-1 therapies is strengthening adoption across obesity treatment programs. Healthcare providers are recognizing that sustained weight reduction significantly reduces the risk of chronic metabolic diseases, which is encouraging earlier therapeutic intervention. Medical associations such as the ADA and the WHO are increasingly emphasizing obesity as a chronic disease that requires structured clinical management rather than short-term lifestyle modification alone. As clinical familiarity with incretin-based drugs improves, treatment adoption is poised to expand beyond endocrinology practices into primary care settings.

Obesity combined with cardiovascular disease is set to record the highest CAGR during the 2026-2033 forecast period. Clinical evidence is increasingly demonstrating that GLP-1 receptor agonists provide cardiometabolic benefits beyond weight reduction. Several large cardiovascular outcomes trials are reporting meaningful reductions in major adverse cardiovascular events among patients receiving incretin-based therapies. These findings are encouraging cardiologists and metabolic disease specialists to incorporate GLP-1 drugs into treatment plans for patients who present with both obesity and elevated cardiovascular risk. Regulatory authorities are also gradually expanding therapeutic recommendations to reflect emerging clinical evidence. For example, the U.S. FDA and the EMA are evaluating new indications for GLP-1 therapies that highlight their cardiovascular benefits.

Regional Insights

North America Obesity GLP-1 Market Trends

North America is expected to dominate in 2026, holding an estimated 50% of the obesity GLP-1 market value. Multiple factors are supporting this leadership, including a high prevalence of obesity, advanced healthcare infrastructure, and strong pharmaceutical innovation ecosystems. The United States represents the largest national market within the region and is driving the majority of treatment adoption. Data from the Centers for Disease Control and Prevention (CDC) indicates that more than 42% of adults in the country are living with obesity, which is creating a large treatment-eligible population for incretin-based therapies. Healthcare providers are increasingly recognizing obesity as a chronic metabolic condition that requires long-term pharmacological management. This broader prescribing base is expanding access to obesity pharmacotherapy and brightening regional market prospects.

Pharmaceutical companies are prioritizing North America for commercial expansion due to its regulatory and reimbursement environment, which promotes faster product adoption. The U.S. FDA maintains a relatively efficient regulatory review framework for innovative metabolic therapies, which is enabling quicker market entry for new drugs. At the same time, favorable pricing structures and strong private insurance coverage are supporting premium drug pricing and higher treatment adoption rates. Investment activity across the region is also increasing as pharmaceutical manufacturers scale production and clinical development programs, reinforcing North America’s position as the primary hub for obesity pharmacotherapy development and commercialization.

Europe Obesity GLP-1 Market Trends

Europe has established itself as the second-largest regional market for obesity GLP-1 therapies. Rising obesity prevalence across several European countries is strengthening the demand for advanced pharmacological interventions. Public health data from organizations such as the WHO and the Organisation for Economic Co-operation and Development (OECD) indicate steady increases in obesity rates across both Western and Central Europe. Healthcare authorities are recognizing that untreated obesity significantly contributes to chronic conditions such as type 2 diabetes, cardiovascular disease, and metabolic dysfunction. As a result, healthcare systems are expanding clinical treatment frameworks that incorporate pharmacotherapy alongside lifestyle modification programs.

European regulatory and reimbursement frameworks are gradually evolving to support wider adoption of obesity pharmacotherapy. The EMA is actively approving new incretin-based drugs after evaluating strong clinical evidence demonstrating sustained weight reduction and improved metabolic outcomes. Several national healthcare systems, including those in Germany and the U.K., are expanding reimbursement eligibility for GLP-1 therapies within targeted patient groups. These programs are prioritizing individuals with obesity who also present with comorbid conditions such as type 2 diabetes or cardiovascular disease. Companies are investing in research partnerships with European biotechnology firms and academic institutions to accelerate the development of metabolic drugs. Manufacturing investments are also increasing to support long-term supply reliability across the European Union (EU).

Asia Pacific Obesity GLP-1 Market Trends

The market for obesity GLP-1 receptor agonists in the Asia Pacific is projected to expand at an estimated 2026-2033 CAGR of 27%. Rapid economic development, changing dietary habits, and increasing urbanization are contributing to surging obesity prevalence across several Asia Pacific countries. National governments are responding by strengthening chronic disease management strategies and allocating higher healthcare budgets to address metabolic disorders. Healthcare providers in the region are also increasingly recognizing obesity as a clinical condition that requires structured treatment rather than lifestyle counseling alone. As a result, the demand for pharmacological interventions that support long-term weight management is increasing steadily across the region.

Pharmaceutical companies are actively expanding their presence in the Asia Pacific by pursuing regulatory approvals, launching clinical trials, and forming partnerships with regional healthcare organizations. Countries such as China, India, Japan, and South Korea are becoming strategic markets due to their large patient populations and improving healthcare infrastructure. China represents one of the most significant growth opportunities because the country has a large population of adults living with obesity, according to China’s NHC. Healthcare reforms and expanding medical insurance coverage are enabling greater patient access to innovative therapies. Domestic pharmaceutical companies are also entering the incretin drug development field, intensifying competition and accelerating product innovation in the region.

Competitive Landscape

The global obesity GLP-1 market structure is moderately concentrated, with a handful of pharmaceutical companies controlling the majority of industry revenue. Two major pharmaceutical manufacturers are holding dominant positions due to their early entry into incretin-based obesity therapies and strong clinical validation. Novo Nordisk A/S is maintaining the largest market share, supported by the widespread adoption of semaglutide therapies that are approved for chronic weight management. The company has established a strong leadership position through extensive clinical evidence, broad physician familiarity, and large-scale manufacturing investments that support global distribution. Eli Lilly and Company is the second-largest market participant, driven primarily by the commercialization of tirzepatide, which targets both GLP-1 and GIP pathways. These dual incretin therapies are gaining physician acceptance as they deliver strong weight reduction and metabolic outcomes.

The competitive landscape is expected to evolve significantly as additional pharmaceutical companies advance next-generation incretin therapies through clinical development. Several biotechnology firms and multinational drug manufacturers are investing in innovative metabolic drugs that target multiple hormonal pathways simultaneously. These therapies are aiming to improve treatment efficacy while addressing obesity-related comorbidities such as cardiovascular disease and metabolic dysfunction. Strategic collaborations, licensing agreements, and research partnerships are also becoming more common as companies seek to accelerate drug discovery timelines and share development risks. This collaborative approach is enabling smaller biotechnology firms to leverage the global commercialization capabilities of larger pharmaceutical organizations.

Key Industry Developments

- In March 2026, China approved Pfizer’s once-weekly injectable GLP-1 weight-loss drug Xianweiying (ecnoglutide) for long-term weight management in overweight or obese adults, strengthening Pfizer’s position in the rapidly expanding obesity therapeutics market.

- In January 2026, the U.S. FDA approved Novo Nordisk’s once-daily oral GLP-1 therapy for chronic weight management, offering a pill alternative to injectable obesity treatments. In the OASIS 4 clinical trial, patients achieved an average 16.6% body-weight reduction, with about one-third losing more than 20%.

- In December 2025, the WHO issued its first global guidelines recommending the use of GLP-1 drugs for treating obesity in adults, marking a major shift in international obesity management policy. The guidance conditionally supports long-term GLP-1 therapy alongside lifestyle interventions such as diet and physical activity.

Companies Covered in Obesity GLP-1 Market

- Novo Nordisk A/S

- Eli Lilly and Company

- Pfizer Inc.

- AstraZeneca plc

- Amgen Inc.

- Roche Holding AG

- Boehringer Ingelheim International GmbH

- Sanofi S.A.

- Merck & Co., Inc.

- Viking Therapeutics, Inc.

- Zealand Pharma A/S

- Structure Therapeutics Inc.

- Altimmune, Inc.

- Regeneron Pharmaceuticals, Inc.

- Jiangsu Hengrui Pharmaceuticals Co., Ltd.

Frequently Asked Questions

The global obesity GLP-1 market is projected to reach US$ 10.1 billion in 2026.

Widening recognition of obesity as a chronic metabolic disease across healthcare systems and definitive results of the efficacy of incretin-based therapies for weight reduction are driving the market.

The market is poised to witness a CAGR of 25.2% from 2026 to 2033.

Expanding reimbursement policies, increasing physician awareness, and the development of next-generation therapies such as dual incretin drugs and oral glucagonGLP-1 receptor agonists are key market opportunities.

Novo Nordisk, Eli Lilly and Company, Pfizer, and AstraZeneca are some of the key players in the market.