- Metals & Minerals

- North America Engineered Quartz Market

North America Engineered Quartz Market Size, Share, and Growth Forecast 2026 - 2033

North America Engineered Quartz Market by Product Type (Quartz Slabs, Quartz Tiles, Prefabricated Countertops, Custom Quartz Surfaces), Application (Kitchen Countertops, Bathroom Vanities, Flooring, Wall Cladding, Decorative Surfaces, Others), Distribution Channel (Direct Sales, Distributors/Dealers, Home Improvement Retailers, Online Channels), End-user (Residential, Commercial, Institutional), and Regional Analysis, 2026 - 2033

North America Engineered Quartz Market Size and Trend Analysis

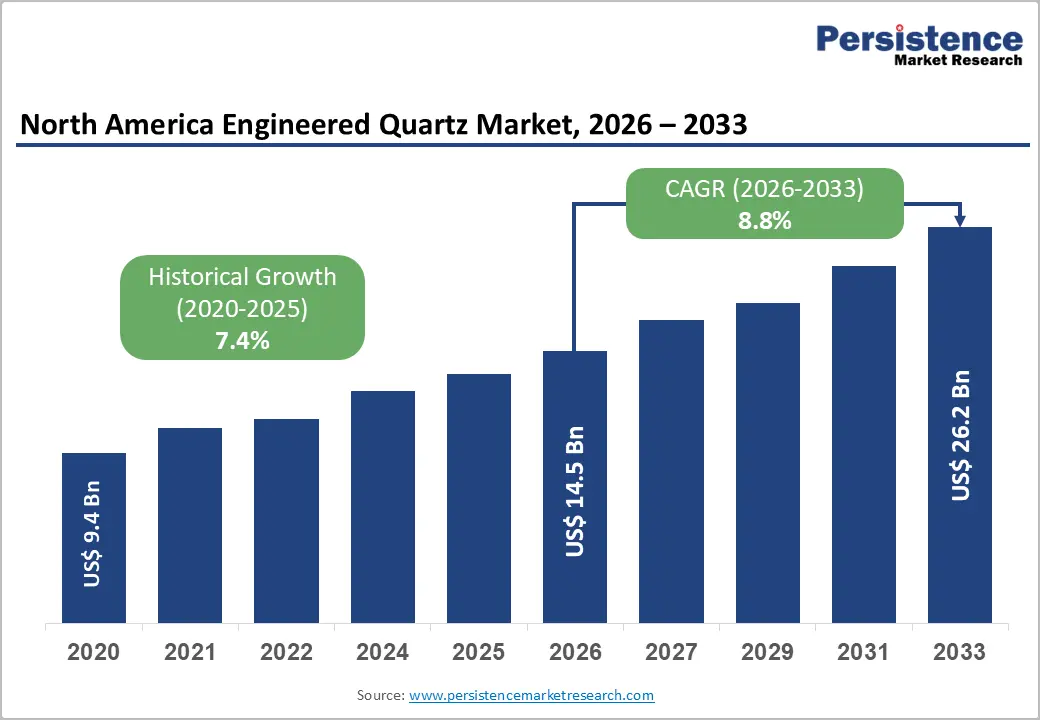

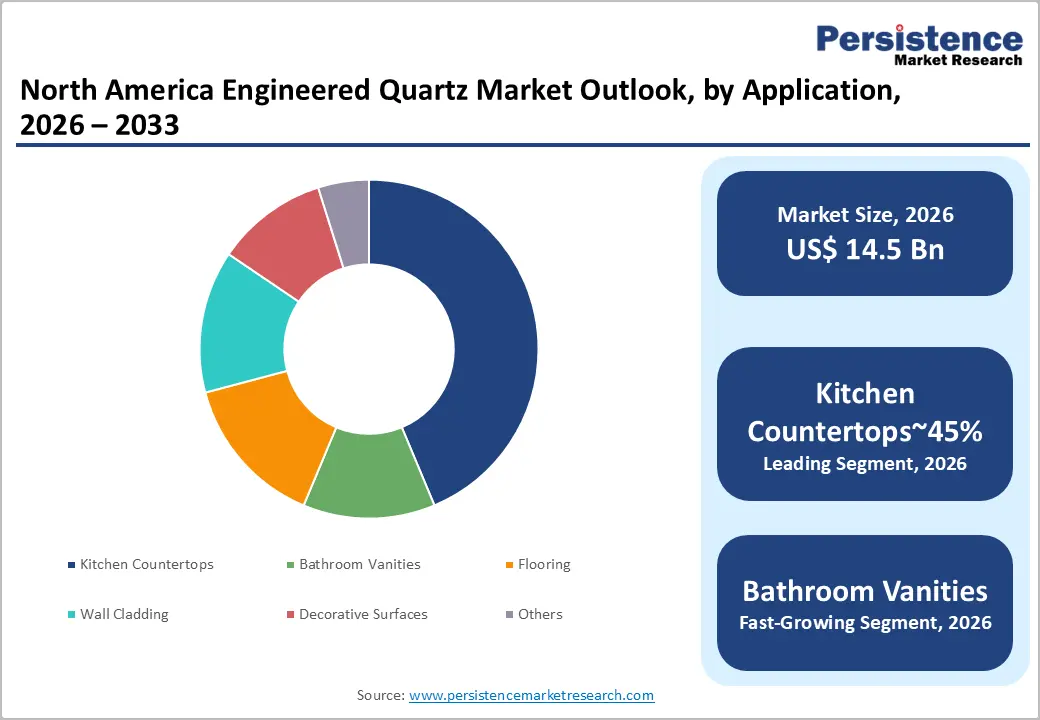

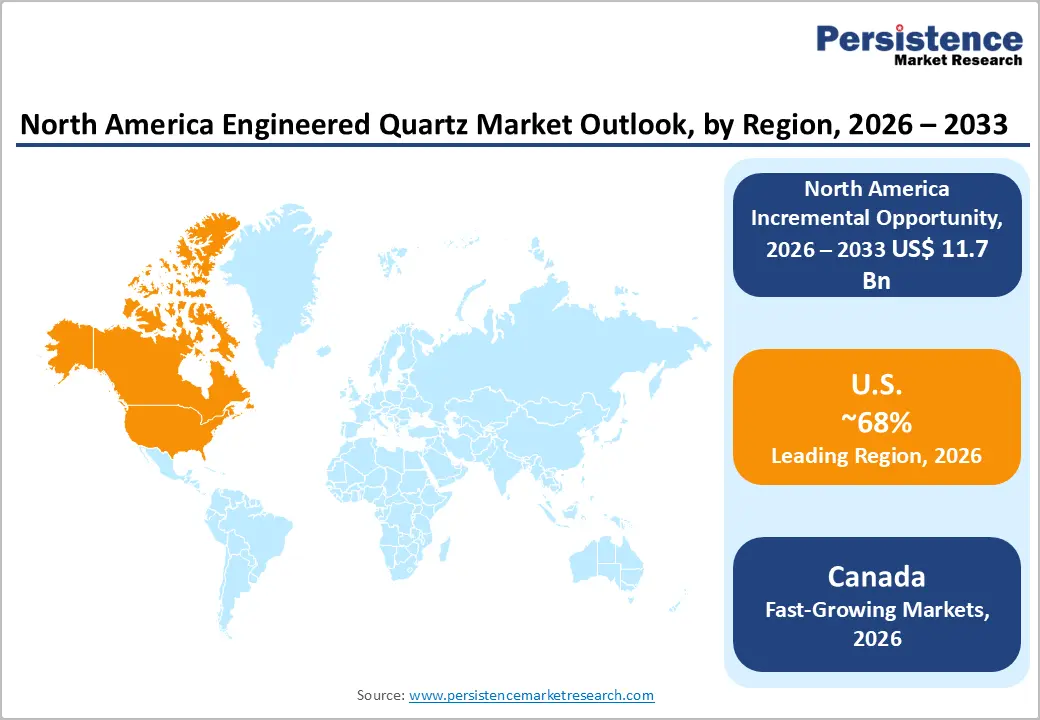

The North America engineered quartz market size is likely to be valued at US$ 14.5 billion in 2026 and is expected to reach US$ 26.2 billion by 2033, growing at a CAGR of 8.8% during the forecast period from 2026 to 2033.

The market is experiencing robust growth driven by escalating residential remodeling activity, widespread adoption of quartz in commercial interiors, and a sustained shift in consumer preference from natural stone to engineered surfaces.

Key Industry Highlights:

- Dominant Application: Kitchen countertops lead application demand with approximately 45% market share, supported by consistent residential remodeling expenditure and widespread adoption by residential developers as a standard feature in new home construction.

- Fastest-Growing Distribution Segment: Online channels are the fastest-growing segment, driven by expanding e-commerce platforms, AR-enabled virtual visualization tools, and direct-to-consumer sales initiatives from leading quartz brands such as Cambria and Caesarstone.

- Key Opportunity: The accelerating demand for large-format and jumbo quartz slabs, driven by open-plan design trends and the fact that over 70% of new U.S. homes now feature kitchen islands, presents a high-margin growth opportunity for manufacturers investing in advanced pressing and processing capabilities.

Market Dynamics

Drivers - Surging Residential Renovation and Construction Activity

The North American housing market has witnessed a sustained surge in home renovation and remodeling expenditure, which is directly amplifying demand for engineered quartz surfaces. According to the Joint Center for Housing Studies (JCHS) of Harvard University, annual home improvement and repair expenditure in the U.S. exceeded US$480 billion in 2023. Engineered quartz, composed of approximately 90% natural quartz crystals bound with polymer resins, offers superior hardness, nonporosity and resistance to staining compared with natural granite and marble, making it the preferred choice for kitchen countertops and bathroom vanities.

The proliferation of open-plan kitchen designs and luxury bathroom remodels, particularly among millennial and Gen Z homeowners, is further catalyzing adoption across the region. This sustained remodeling culture, combined with high housing turnover rates in major U.S. metropolitan areas, is expected to remain a primary growth engine through 2033.

Expansion of Commercial Construction and the Hospitality Sector

Commercial end-users, including hotels, restaurants, office complexes, and healthcare facilities, are increasingly specifying engineered quartz for interior surfaces owing to its hygienic, non-porous properties and long-term durability. The U.S. Green Building Council (USGBC) reports that buildings targeting LEED certification represent a growing share of new commercial construction starts, and quartz surfaces frequently contribute to LEED credits for materials and resources.

According to the American Institute of Architects (AIA) Consensus Construction Forecast, non-residential construction spending in the U.S. grew approximately 5% in 2023, with the hospitality and healthcare sectors demonstrating outsized momentum. This sectoral expansion is compelling quartz manufacturers to develop larger-format slabs and antimicrobial surface technologies specifically tailored for high-traffic commercial environments.

Restraints - Silica Dust Exposure and Occupational Health Regulations

A critical challenge facing the engineered quartz industry is growing regulatory scrutiny around crystalline silica dust exposure during fabrication and installation. The U.S. Occupational Safety and Health Administration (OSHA) revised its permissible exposure limit (PEL) for respirable crystalline silica to 50 micrograms per cubic meter (μg/m³), a 50% reduction from the prior standard.

Fabricators are now required to invest in wet-cutting equipment, vacuum extraction systems, and comprehensive respiratory protection programs, significantly raising operational costs. Several high-profile silicosis-related lawsuits and workers' compensation claims have led to manufacturing shutdowns, creating a regulatory headwind that constrains the pace of market expansion, particularly for mid-sized fabricators lacking capital for compliance infrastructure.

Competition from Alternative Premium Surfacing Materials

Engineered quartz faces intensifying competition from ultra-compact surfaces (sintered stone), large-format porcelain slabs, and recycled glass composites. Sintered stone products such as Dekton (by Cosentino) and Lapitec offer greater heat and UV resistance, areas where quartz surfaces have inherent limitations.

According to the National Kitchen and Bath Association (NKBA), consumer interest in sintered stone products has been rising steadily, with over 15% of design professionals reporting increased specification of ultra-compact surfaces in high-end projects as of 2023. This competitive pressure is forcing quartz manufacturers to invest heavily in design differentiation, surface texture innovation, and antimicrobial technology to maintain category dominance.

Opportunities - Rising Demand for Large-Format and Jumbo Quartz Slabs

The growing preference among architects and interior designers for seamless, uninterrupted surface aesthetics is creating significant demand for jumbo quartz slabs, typically measuring 3,200 mm × 1,600 mm or larger. Leading manufacturers, including Caesarstone and Cambria, have already introduced jumbo slab collections for high-end residential and commercial applications.

According to the National Association of Home Builders (NAHB), the share of new homes with kitchen islands has surpassed 70% in recent years, driving demand for larger, seamless quartz countertops. Jumbo slabs command premium pricing, enabling manufacturers to improve per-unit revenue and gross margins. Investment in advanced pressing, polishing, and logistics infrastructure capable of handling large-format slabs represents a strategically valuable growth avenue for market participants targeting the premium tier.

Accelerating Adoption of Online Sales Channels and Digital Visualization Tools

The proliferation of e-commerce and augmented reality (AR)-enabled design tools is transforming how consumers discover, evaluate, and purchase engineered quartz products. Major home improvement retailers, including The Home Depot and Lowe's, have significantly expanded their online quartz product catalogs, integrating virtual room visualization features and digital slab sampling.

According to the U.S. Department of Commerce, e-commerce retail sales in the building materials category grew by approximately 18% between 2020 and 2023. The integration of AR tools allows consumers to visualize quartz surfaces in their actual living spaces before purchase, significantly reducing decision friction and product return rates. Market participants investing in digital-first distribution strategies and direct-to-consumer online platforms are well-positioned to capture incremental demand from tech-savvy millennial homeowners.

Category-wise Analysis

Product Type Insights

Quartz slabs (encompassing polished, textured, and jumbo formats) dominate the North America Engineered Quartz Market, accounting for approximately 58% of total market revenue. The segment's leadership reflects its broad application versatility across kitchen countertops, bathroom vanities, wall cladding, and decorative surfaces in both residential and commercial settings.

Polished slabs remain the most specified format due to their reflective finish and ease of maintenance, while textured slabs are gaining traction in contemporary interior design projects seeking tactile differentiation. The emergence of jumbo slabs, capable of spanning large kitchen islands without visible seams, has further reinforced segment dominance. According to the Kitchen and Bath Industry Show (KBIS) trend reports, slab-format engineered quartz remains the top specified product category among kitchen and bath designers across North America.

Application Insights

Kitchen countertops represent the leading application segment, capturing approximately 45% of the North America Engineered Quartz Market share. Engineered quartz is favored in kitchen applications for its exceptional scratch, stain, and heat resistance compared to laminate and tile alternatives, as well as its expansive design palette that can replicate natural stone aesthetics.

According to the Joint Center for Housing Studies (JCHS), kitchen remodeling consistently ranks among the top home improvement projects by expenditure in the U.S., with a growing proportion of homeowners specifying quartz as their material of choice. The segment is further supported by builder-grade upgrades, with residential developers broadly adopting quartz countertops as a standard feature in mid-range and premium new-home offerings across the U.S. and Canada.

Distribution Channel Insights

Home Improvement Retailers constitute the leading distribution channel segment, accounting for approximately 38% of market revenue. Major retail chains, including The Home Depot and Lowe's, offer extensive quartz product selections and serve as critical consumer touchpoints through in-store design centers and kitchen planning services.

These retailers leverage broad geographic store networks, competitive pricing, and financing options to drive high-value countertop and surface purchases. According to The Home Depot's annual reports, the kitchen and bath categories have consistently ranked among the highest-growth merchandise segments, validating the retailer's investment in expanding its quartz product line. The combination of physical showroom experience and growing online catalogs positions home improvement retailers as the preferred procurement channel for residential consumers.

End-user Insights

The residential segment holds the dominant position in the North America Engineered Quartz Market, accounting for approximately 62% of total market revenue. This leadership is underpinned by sustained consumer spending on home renovation, kitchen and bathroom remodeling, and new home construction.

The U.S. Census Bureau reported that new privately owned housing completions totaled approximately 1.4 million units in 2023, each representing potential demand for engineered quartz countertops, flooring, and bathroom surfaces. Rising disposable incomes, growing homeownership aspirations among millennials, and media-driven interior design trends propagated through platforms such as Houzz and Pinterest are reinforcing quartz adoption in residential applications. The material's durability and low-maintenance profile further enhance its value proposition for residential end-users.

Competitive Landscape

The North America engineered quartz market exhibits a moderately consolidated structure, with a core group of established global and regional players commanding significant collective market share. Caesarstone, Cambria, Silestone (by Cosentino), and MSI Surfaces collectively represent a substantial competitive bloc, leveraging strong brand equity, expansive distribution networks, and continuous product innovation.

Key competitive differentiators include proprietary surface textures, antimicrobial technologies, large-format slab capabilities, and sustainability credentials. Emerging business model trends include direct-to-consumer digital platforms, virtual design showrooms, and customization-as-a-service offerings. Mid-tier players such as HanStone Quartz and Vicostone are pursuing geographic expansion and private-label partnerships with home improvement retailers to strengthen their competitive footprint.

Key Developments:

- May 2025: LOTTE Chemical partnered with EKO Stone to distribute its Radianz Quartz products across the U.S. Midwest, aiming to expand its regional footprint, enhance supply chain efficiency, and capitalize on rising demand for high-quality engineered quartz surfaces.

- August 2024: Vadara Quartz Surfaces strengthened its U.S. market presence by announcing four new distribution partnerships across the East Coast, improving product availability, logistics efficiency, and regional accessibility to meet growing demand for premium engineered quartz surfaces.

- April 2025: MSI Surfaces expanded its engineered quartz portfolio by launching eight new Q Premium Natural Quartz colors at KBIS 2025 in Las Vegas, enhancing design versatility for residential and commercial interiors with improved aesthetics and application flexibility.

North America Engineered Quartz Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 9.4 Bn |

| Current Market Value (2026) | US$ 14.5 Bn |

| Projected Market Value (2033) | US$ 26.2 Bn |

| CAGR (2026 - 2033) | 8.8% |

| Leading Region | U.S, 68% share |

| Dominant Application | Kitchen Countertops, 45% share |

| Top-ranking End Use | Residential, 62% |

| Incremental Opportunity | US$ 11.7 Bn |

Companies Covered in North America Engineered Quartz Market

- Caesarstone

- Silestone

- Cambria

- MSI Surfaces

- DuPont

- Daltile

- LG Hausys

- Pental Surfaces

- HanStone Quartz

- Wilsonart

- Vicostone

- Quartz Master

- Raphael Stone

- Santa Margherita

- Okite

- Cosentino Group

- Compac Quartz

- Arizona Tile

Frequently Asked Questions

The North America Engineered Quartz Market is projected to reach US$ 26.2 Billion by 2033, expanding at a CAGR of 8.8% during the forecast period 2026-2033, up from an estimated US$ 14.5 Billion in 2026. The market recorded a historical CAGR of 7.4% during the 2020-2025 period, reflecting sustained structural demand growth.

The primary growth drivers include rising residential renovation expenditure, which exceeded US$ 480 Billion annually in the U.S. per the Joint Center for Housing Studies (JCHS), and expanding commercial construction activity driven by LEED-certified building projects, hospitality sector development, and strong consumer preference for durable, hygienic surfacing materials over natural stone.

Quartz Slabs represent the dominant product type segment, accounting for approximately 58% of total market revenue. Their leadership is driven by broad application versatility across kitchen countertops, bathroom vanities, and wall cladding, along with accelerating demand for large-format and jumbo slab formats favored by architects, interior designers, and residential developers.

North America, led by the United States, is the dominant regional market for engineered quartz. The region benefits from high consumer spending on home renovation, a well-established distribution network encompassing fabricators, specialty dealers, and major home improvement retailers, and strong brand presence from leading manufacturers such as Caesarstone and Cambria.

The most significant opportunity lies in the accelerating demand for large-format and jumbo quartz slabs, driven by architectural trends favoring seamless interior surfaces. Additionally, the rapid growth of online sales channels, where e-commerce in building materials grew 20% between 2020 and 2023 per the U.S. Department of Commerce, presents a high-growth revenue avenue for brands investing in digital-first distribution and AR-enabled consumer engagement.

Leading companies operating in the North America Engineered Quartz Market include Caesarstone, Silestone (by Cosentino), Cambria, MSI Surfaces, DuPont, Daltile, LG Hausys, Pental Surfaces, HanStone Quartz, Wilsonart, Vicostone, Quartz Master, Raphael Stone, Santa Margherita, and Okite, among others.