- Medical Devices

- Nanotechnology-based Implants Market

Nanotechnology-based Implants Market Size, Share, and Growth Forecast 2026 - 2033

Nanotechnology-based Implants Market by Product Type (Active Implants, Nano-coated Implants, Biosensor Implants, Others), by Material (Titanium-based, Polymer-based, Ceramic-based, Others), by Application (Orthopedic, Dental, Cardiovascular, Neurological, Others), by End User (Hospitals, Clinics, Research Institutes), by Regional Analysis, 2026 - 2033

Nanotechnology-based Implants Market Share and Trends Analysis

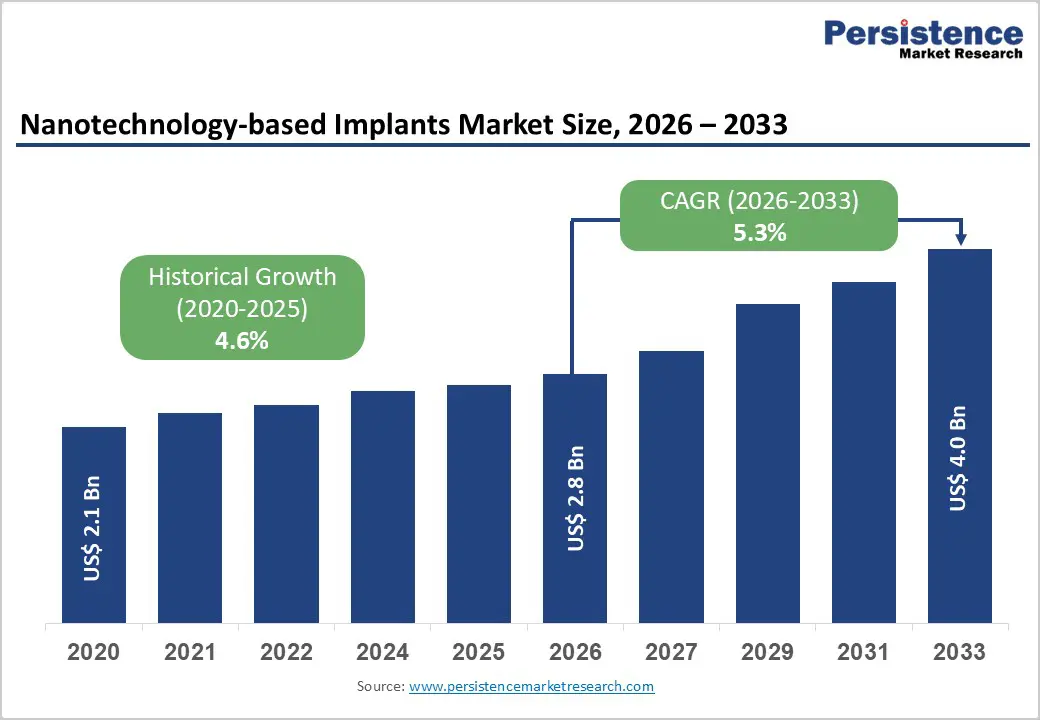

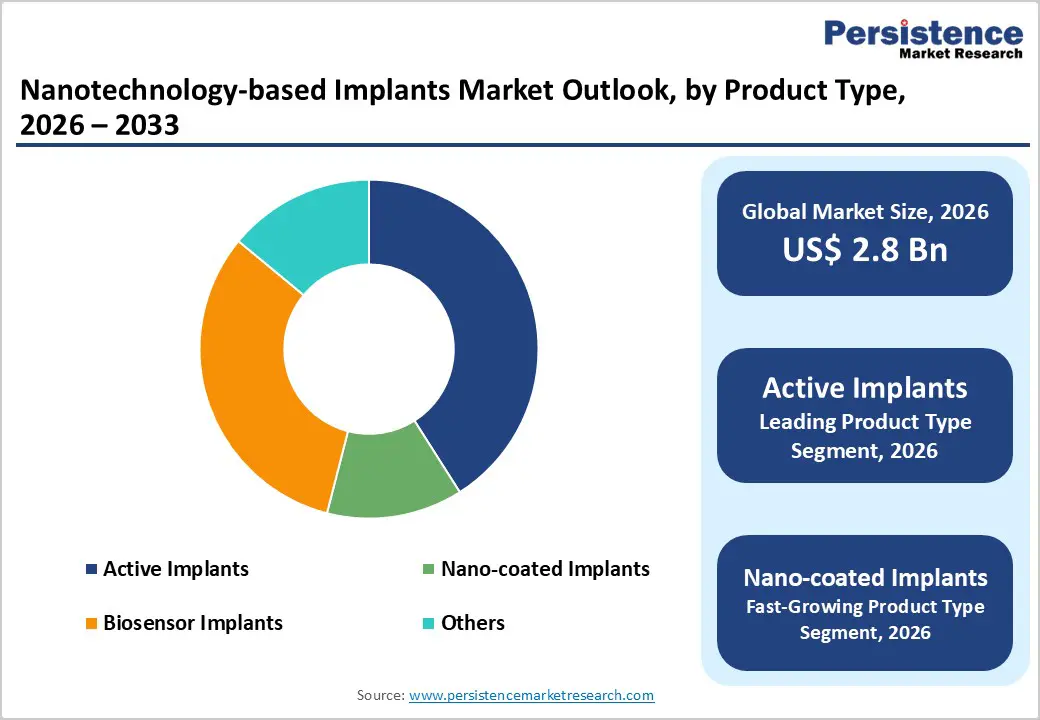

The global nanotechnology-based implants market size is expected to be valued at US$ 2.8 billion in 2026 and projected to reach US$ 4.0 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

Market expansion is primarily driven by escalating demand for advanced orthopedic implants featuring nano-engineered surfaces that accelerate osseointegration by 30-50%, alongside burgeoning adoption of active implantable devices incorporating biosensor technology for real-time patient monitoring.

Aging demographics with 2 billion people aged 60+ expected by 2050, combined with rising procedure volumes (over 1 million annual hip/knee replacements in the U.S. alone), create sustained demand. Regulatory advancements, including FDA nanotechnology guidance and EU MDR implementation, further catalyze clinical translation of innovative nano-implant technologies across orthopedics, cardiology, and neurology applications.

Key Industry Highlights:

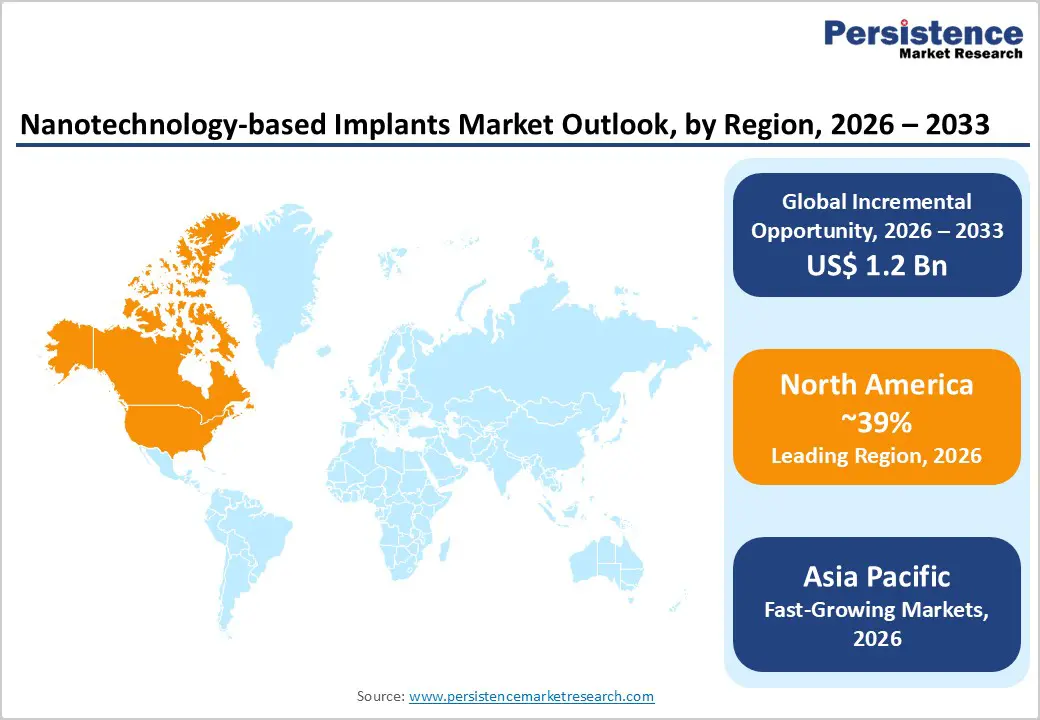

- North America dominates (39% share) due to a strong regulatory and innovation ecosystem led by the U.S. Food and Drug Administration, along with significant R&D investments from major medical device manufacturers. The region performs over 1 million orthopedic procedures annually, supporting high adoption of advanced nano-enabled implants.

- Asia Pacific is the fastest-growing region (6.0% CAGR), driven by large-scale manufacturing capabilities in China and India. The region offers nearly 30% cost advantages and expanding clinical trial capacity, accelerating commercialization and accessibility of nanotechnology-based implants.

- Active implants lead the market (41% share), particularly in cardiac and neurological applications, where nano-enabled biosensors improve monitoring and reduce complications by enhancing precision and long-term performance.

| Key Insights | Details |

|---|---|

| Nanotechnology-based Implants Market Size (2026E) | US$ 2.8 billion |

| Market Value Forecast (2033F) | US$ 4.0 billion |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Advancements in Nano-engineered Implant Surfaces

Nanotechnology surface modifications have fundamentally transformed implant performance by creating hierarchical nano/micro-textures that mimic the morphology of the native bone extracellular matrix. Clinical research demonstrates that nanostructured titanium implants achieve 30-50% faster osseointegration compared to conventional micro-roughened surfaces, significantly reducing fibrous encapsulation and implant failure rates. Osteoblast differentiation accelerates on nanotopographic surfaces via integrin-mediated signaling pathways, while osteoclast activity diminishes, creating optimal microenvironments for bone remodeling. Medtronic's acquisition of Nanovis nano-textured PEEK technology exemplifies industry momentum, with FDA-cleared Adaptix interbody devices demonstrating superior fusion rates in IDE clinical studies. Europe's MDR nanomaterial guidelines and Asia-Pacific manufacturing scale-up further support global adoption, positioning nano-engineered surfaces as a standard of care across orthopedic, dental, and spinal applications.

Proliferation of Active Implants with Biosensor Capabilities

Active implantable medical devices integrating nanotechnology biosensors represent transformative growth drivers, enabling real-time physiological monitoring that reduces complications by 25-40% and hospital readmissions by 30%. Cardiovascular stents with endothelialization sensors, intracranial pressure monitors, and glucose-sensing implants exemplify this convergence, supported by NIH funding of $200+ million annually in nanotechnology. FDA's risk-based regulatory framework and EU MDR AI provisions accelerate smart implant commercialization, while China/India clinical trial capacity (40% global share) expands validation pipelines. Economic analyses confirm $10,000-20,000 per-patient cost savings through remote monitoring, positioning biosensor-enabled nano-implants for ubiquitous adoption across high-prevalence chronic diseases, including heart failure, diabetes, and neurological disorders.

Restraints - Complex Regulatory Pathways for Nanomaterials

Nanotechnology-based implants face significantly complex and evolving regulatory frameworks, which act as a major barrier to market growth. Regulatory bodies such as the U.S. Food and Drug Administration and European authorities enforce stringent requirements for nanomaterial characterization, including detailed analysis of particle size, surface properties, toxicity, and long-term biological interactions. Standards like ISO 10993 have expanded to include nano-specific evaluations such as genotoxicity and nanoparticle migration risks. Additionally, compliance with Good Manufacturing Practices under 21 CFR Part 820 increases documentation and validation burdens. In Europe, the Medical Device Regulation (MDR) mandates enhanced scrutiny, traceability through EUDAMED, and post-market clinical follow-ups. These requirements significantly extend approval timelines compared to those for conventional implants, often by nearly 2 years. Small and mid-sized companies are particularly impacted due to limited regulatory expertise and financial resources. As a result, delayed product launches and increased compliance costs slow innovation and commercialization across the nanotechnology implant ecosystem.

Manufacturing Scalability and Cost Premiums

The commercialization of nanotechnology-based implants is further constrained by challenges in large-scale manufacturing and high production costs. Advanced fabrication techniques such as atomic layer deposition (ALD), electron beam lithography (EBL), and glancing angle deposition (GLAD) require specialized infrastructure, skilled labor, and precise environmental controls, making them significantly more expensive than traditional implant manufacturing processes. These technologies often result in lower production yields, especially for complex nano-enabled biosensors and coatings, increasing material wastage and operational inefficiencies. Moreover, the need for high-purity raw materials and stringent quality assurance under GMP standards further inflates overall costs. While regions in the Asia-Pacific offer relatively lower manufacturing expenses, regulatory validation requirements in markets like Japan and China limit cost advantages. In contrast, Western markets adopt premium pricing strategies, restricting accessibility in price-sensitive regions. Consequently, conventional implants continue to dominate in emerging economies, creating a gap between technological advancement and widespread adoption of nano-enabled solutions.

Nano-coated Implants for Infection Prevention

Nano-coated implants represent a high-impact opportunity in the nanotechnology-based implants market, primarily driven by the need to reduce device-related infections, which impose a significant global healthcare burden. Advanced nanocoatings such as silver nanoparticles, graphene oxide, and zinc oxide exhibit strong antimicrobial properties, enabling effective prevention of bacterial colonization and biofilm formation without contributing to antimicrobial resistance. These coatings enhance implant safety and longevity, particularly in orthopedic and dental procedures where infection risks remain notable. Companies like Xenix Medical are already advancing innovations in nano-enabled implant surfaces, demonstrating improved fixation and clinical outcomes. Additionally, supportive regulatory developments, including flexible evaluation pathways and sandbox environments, are encouraging faster validation of such technologies. Cost advantages in manufacturing hubs like India and China further enhance scalability. With infection rates still prevalent in implant procedures, nano-coatings are expected to gain substantial adoption and drive market growth through 2030.

Polymer-based Nanocomposites for Patient-Specific Implants

Polymer-based nanocomposites are emerging as a strong opportunity area, enabling the development of patient-specific implants with enhanced mechanical and biological performance. Materials such as nano-reinforced PEEK and polycaprolactone combined with nano-hydroxyapatite offer improved strength, durability, and biocompatibility compared to conventional polymers. These materials also support advanced manufacturing techniques, such as 3D printing, enabling customization based on patient anatomy, which is especially valuable for orthopedic and cranial implants. Leading companies such as Stryker Corporation and Zimmer Biomet are leveraging nanengineered structures to improve implant integration and reduce complications such as stress shielding. Favorable regulatory pathways, including established approval frameworks, are accelerating product development. Additionally, the growing aging population and increasing demand for joint replacements and spinal procedures are creating sustained opportunities for personalized, high-performance nano-enabled implants in the coming years.

Category-wise Analysis

Material Insights

Titanium-based nanomaterials dominate the nanotechnology-based implants market, accounting for nearly 60% share in 2025 due to their superior strength, corrosion resistance, and proven biocompatibility. Medical-grade titanium, particularly Ti6Al4V alloys, is widely used owing to its compliance with standards such as ISO 5832-3, which ensure safety and long-term stability. Nano-texturing of titanium surfaces significantly enhances osseointegration, accelerating bone bonding and improving implant longevity. Clinical validations and material testing standards such as ASTM F67 further support adoption. Meanwhile, polymer-based nanocomposites are emerging as the fastest-growing segment, driven by advancements in nano-PEEK and hybrid biomaterials. These materials offer improved mechanical strength, flexibility, and biological response, making them ideal for next-generation implants, particularly in spinal and orthopedic applications where performance and customization are critical.

Application Insights

Orthopedic applications hold the largest share of around 45% in the nanotechnology-based implants market, primarily due to the high volume of joint replacement and spinal fusion procedures. Nano-engineered implant surfaces play a crucial role in reducing complications such as aseptic loosening by improving bone integration and implant stability. Leading manufacturers like Zimmer Biomet and Stryker Corporation are actively advancing nanocomposite implant technologies to enhance clinical outcomes. Additionally, data support from organizations like the American Academy of Orthopaedic Surgeons reinforces the effectiveness of these innovations. On the other hand, dental applications are witnessing the fastest growth, driven by increasing demand for durable and aesthetic implants. Nano-surface modifications improve implant success rates, faster healing, and long-term stability, making them increasingly preferred over conventional alternatives.

Regional Insights

North America Nanotechnology-based Implants Market Trends and Insights

North America dominates the nanotechnology-based implants market, driven by advanced healthcare infrastructure, strong R&D investments, and early adoption of innovative medical technologies. The region benefits from the presence of leading players such as Stryker Corporation, Zimmer Biomet, and Medtronic plc, which actively develop nano-enabled orthopedic and cardiovascular implants. Regulatory support from the U.S. Food and Drug Administration, along with well-established approval pathways, accelerates innovation despite stringent compliance requirements. Rising prevalence of chronic diseases, increasing joint replacement procedures, and a rapidly aging population further boost demand for high-performance implants. Additionally, strong reimbursement frameworks and widespread adoption of advanced surgical techniques support market growth. Continuous clinical research and collaborations between academia and industry are enhancing the development of nano-coated and smart implants, reinforcing North America’s leadership position.

Asia Pacific Nanotechnology-based Implants Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the nanotechnology-based implants market, driven by expanding healthcare infrastructure, rising medical tourism, and increasing demand for advanced yet cost-effective treatments. Countries such as China, India, and Japan are witnessing rapid adoption of nano-enabled orthopedic and dental implants due to an aging population and a higher incidence of chronic conditions. Government initiatives supporting domestic medical device manufacturing and favorable production costs are attracting global players to establish regional facilities. Additionally, improving regulatory frameworks and faster approval timelines compared to Western markets are accelerating product commercialization. The rise of private hospitals and specialty clinics, along with increasing awareness of advanced implant technologies, is further supporting market expansion, positioning the Asia Pacific as a key future growth hub.

Competitive Landscape

The nanotechnology-based implants market is highly competitive and innovation-driven, characterized by continuous advancements in biomaterials, surface engineering, and smart implant technologies. Companies are focusing on developing nano-coated and nanocomposite implants to enhance biocompatibility, durability, and infection resistance. Strategic collaborations with research institutions and healthcare providers are accelerating product development and clinical validation. The market also reflects strong investment in R&D to meet evolving regulatory standards and improve patient outcomes.

Key Developments:

- In January 2026, Curiteva received 510(k) clearance from the U.S. Food and Drug Administration for its 3D-printed trabecular PEEK-based spinal implant system under a nanotechnology designation. The implant incorporated a proprietary surface technology that created a nanocrystalline hydroxyapatite layer (10-20 nm thick), enhancing surface hydrophilicity and improving interaction with biological tissues.

- In January 2026, Spineology Inc. announced the launch of its OptiMesh® HA Nano implant, a next-generation spinal interbody fusion device incorporating a nano-scale hydroxyapatite surface technology. The innovation introduced a conformable, engineered mesh platform designed to enhance osseointegration through an ultra-thin, bioactive nano-layer that promotes rapid cellular activity and bone integration.

- In November 2025, Zavation Medical Products launched of NanoPrime™, a next-generation hybrid implant material combining PEEK and titanium, aimed at enhancing spinal implant performance. The technology utilized an advanced nanoelectrode process involving ion-beam and evaporation techniques to create a strong atomic-level bond between titanium and PEEK, reducing the risk of coating delamination.

Companies Covered in Nanotechnology-based Implants Market

- Stryker Corporation

- 3M Company

- Smith & Nephew

- Abbott Laboratories

- Medtronic plc

- Boston Scientific Corporation

- Zimmer Biomet

- Dentsply Sirona

- Mitsui Chemicals

- Nanospectra Biosciences

- Nanobiotix

- AAP Implantate

- Xenix Medical

- Nanovis, Bioretec

Frequently Asked Questions

The global nanotechnology-based implants market reaches US$ 2.8 billion in 2026, expanding to US$ 4.0 billion by 2033 (5.3% CAGR), driven by nano-orthopedic surfaces and active implant biosensors.

Nano-engineered surfaces accelerate osseointegration 30-50% while biosensor implants reduce complications 25%, supported by FDA/NIH frameworks and 2B aging population demand.

North America (39% in 2025) leads through U.S. orthopedic volume (1M+ procedures), FDA approvals, Medtronic/Stryker R&D leadership.

Nano-coated implants (6.2% CAGR) target $10-20B infection market via AgNP/GO antimicrobial surfaces, leveraging EU MDR/Asia manufacturing scale-up.

Medtronic plc, Stryker Corporation, Zimmer Biomet, Smith & Nephew, Xenix Medical, Nanovis, Boston Scientific, Abbott, 3M, Dentsply Sirona lead nano-implant innovation.