- Executive Summary

- Global Military Boots Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Military Boots Market Outlook: Boot Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Pairs) Analysis by Boot Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- Market Attractiveness Analysis: Boot Type

- Global Military Boots Market Outlook: Material

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Pairs) Analysis by Material, 2020-2025

- Current Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- Market Attractiveness Analysis: Material

- Global Military Boots Market Outlook: End User

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Pairs) Analysis by End User, 2020-2025

- Current Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- Market Attractiveness Analysis: End User

- Global Military Boots Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Pairs) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Pairs) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Pairs) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- North America Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- North America Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- Europe Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Pairs) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- Europe Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- Europe Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- East Asia Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Pairs) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- East Asia Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- East Asia Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- South Asia & Oceania Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Pairs) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- South Asia & Oceania Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- South Asia & Oceania Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- Latin America Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Pairs) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- Latin America Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- Latin America Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- Middle East & Africa Military Boots Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Pairs) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Pairs) Forecast, by Boot Type, 2026-2033

- Combat Military Boots

- Desert Boots

- Jungle Boots

- Cold Weather Boots

- Parade Boots

- Tactical Boots

- Middle East & Africa Market Size (US$ Bn) and Volume (Pairs) Forecast, by Material, 2026-2033

- Leather

- Nylon & Synthetic Blends

- Rubber

- Advanced Composite Materials

- Middle East & Africa Market Size (US$ Bn) and Volume (Pairs) Forecast, by End User, 2026-2033

- Army

- Navy

- Air Force

- Special Forces

- Paramilitary & Homeland Security

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- NS Footwear PVT. Ltd.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- McRae

- Wolverine World Wide

- Belleville Boot Company

- Magnum Boots

- Butex

- Bates Footwear

- Rampage

- Under Armour

- Haix

- Rocky Brands

- Danner

- Altama

- LOWA

- Meindl Boots

- Garmont International S.r.l.

- Corcoran

- Oakley

- Milforce Equipment Co., Ltd.

- Arris Composites

- OTB Boots Inc.

- NS Footwear PVT. Ltd.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Clothing, Footwear, & Accessories

- Military Boots Market

Military Boots Market Size, Share, and Growth Forecast 2026 - 2033

Military Boots Market by Boot Type (Combat Military Boots, Desert Boots, Jungle Boots, Cold Weather Boots, Parade Boots, Tactical Boots), Material (Leather, Nylon & Synthetic Blends, Rubber, Advanced Composite Materials), End-user (Army, Navy, Air Force, Special Forces, Paramilitary & Homeland Security), by Regional Analysis, 2026 - 2033

Military Boots Market Size and Trend Analysis

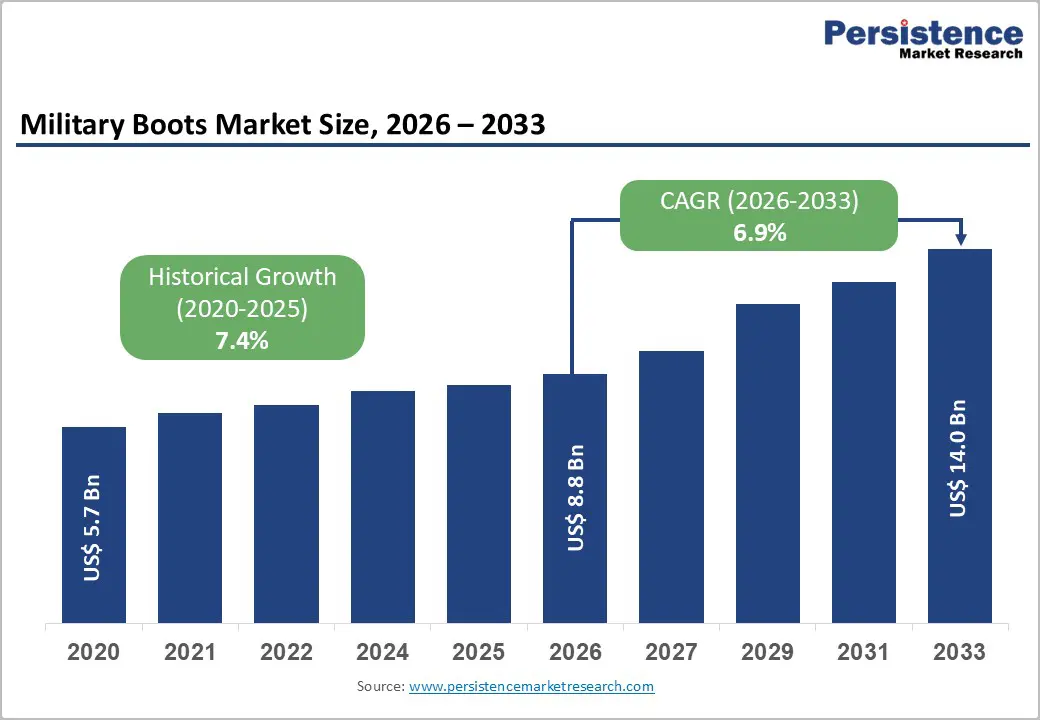

The global military boots market size is expected to be valued at US$ 8.8 billion in 2026 and projected to reach US$ 14.0 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

The military boots market is advancing on a strong and durable growth trajectory, underpinned by a broad-based global escalation in defense budgets, rising geopolitical tensions, and the accelerating modernization of soldier equipment programs across both established and emerging military powers.

As NATO member states commit to the 2% of GDP defense spending target and nations in Asia Pacific rapidly expand their armed forces, procurement volumes for advanced military footwear, integrating ballistic-resistant materials, ergonomic support systems, and climate-specific performance engineering, are expanding substantially. Parallel growth in paramilitary forces, border security agencies, and homeland security establishments globally is further broadening the addressable end-user base beyond traditional standing armed forces, sustaining multi-year demand momentum through the forecast period.

Key Industry Highlights

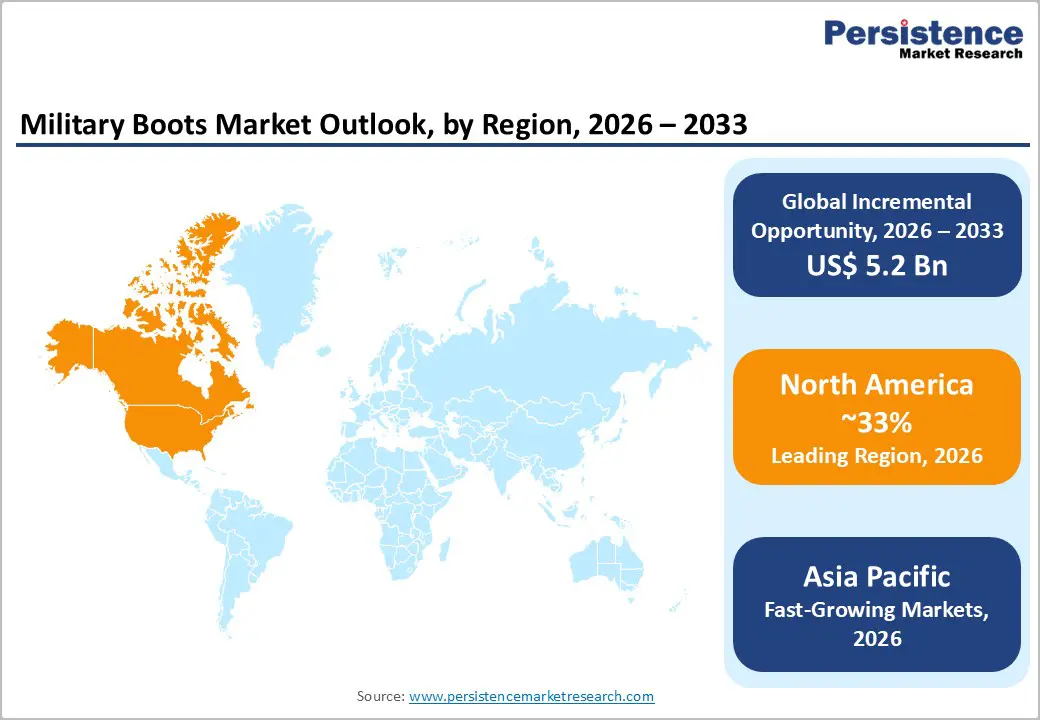

- Leading Region: North America leads the global Military Boots market with approximately ~33% revenue share in 2025, anchored by massive U.S. DoD procurement volumes, Berry Amendment domestic supply chain protections, and established manufacturers including Belleville Boot Company, Bates Footwear, and Rocky Brands.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market over 2026 - 2033, driven by China’s PLA modernization programs, India’s Atmanirbhar Bharat defense indigenization push, Japan’s defense budget doubling commitment, and expanding military headcounts across ASEAN nations.

- Dominant Segment: Combat Military Boots dominate the Boot Type segment with approximately ~34% market share in 2025, reflecting universal mandatory procurement across all global army branches and the high annual replacement volumes driven by 12 to 18-month average operational service life per pair.

- Fastest Growing Segment: Special Forces and Tactical Units represent the fastest growing end-user segment over 2026 - 2033, with global SOF expansion programs across NATO allies and SOCOM driving demand for premium mission-specific tactical boots at significantly higher unit price points than standard-issue procurement.

- Key Opportunity: Smart military footwear with embedded biometric and terrain-sensing technology is the key market opportunity, with U.S. Army DEVCOM and NATO Future Soldier programs actively evaluating sensor-integrated boot prototypes, opening a new high-margin product category for technically capable manufacturers.

| Key Insights | Details |

|---|---|

| Military Boots Market Size (2026E) | US$ 8.8 Billion |

| Market Value Forecast (2033F) | US$ 14.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 7.4% |

Market Dynamics

Drivers - Rise in Global Defense Budgets and Armed Forces Modernization Programs

Rising geopolitical instability and the reassessment of national security priorities across multiple regions are driving unprecedented increases in global defense expenditure, directly translating into expanded procurement of military personal equipment, including advanced footwear. The Stockholm International Peace Research Institute (SIPRI) reported that global military expenditure reached a record US$ 2,443 billion in 2023, growing for the ninth consecutive year. In Europe, NATO’s renewed focus on collective defense following the Russia-Ukraine conflict has prompted member states including Germany, Poland, and the United Kingdom to dramatically increase defense budgets and launch large-scale soldier modernization programs. The U.S. Department of Defense (DoD) consistently allocates billions annually to individual soldier systems, with military footwear representing a mandatory, high-turnover procurement category across all service branches given average service life of 12 to 18 months per pair under operational conditions.

Technological Innovation in Soldier Performance Footwear

Military organizations worldwide are increasingly recognizing that advanced footwear directly impacts soldier operational effectiveness, injury prevention, and mission endurance, driving demand for technologically superior boots beyond conventional leather designs. Modern military boot development incorporates vibration-dampening midsole systems, moisture-wicking and anti-microbial liner treatments, thermoplastic polyurethane (TPU) outsoles with multi-surface traction geometries, and flame-resistant upper materials compliant with standards such as ASTM F2413 and MILSPEC MIL-A-43455. The U.S. Army Research Laboratory (ARL) has documented that musculoskeletal injuries, many of which are footwear-related, account for a substantial portion of training and operational duty losses, with studies indicating that properly engineered footwear can reduce lower-limb injury incidence by up to 30%. This data-backed case for performance footwear is motivating procurement specification upgrades and higher unit price tolerance across defense establishments globally.

Restraints - Stringent Military Procurement Standards and Long Qualification Timelines

One of the primary structural constraints in the military boots market is the complexity and duration of the defense procurement qualification process. Military footwear must meet rigorous national and international performance standards, including Berry Amendment compliance requirements in the United States, which mandate that textile and footwear items procured by the U.S. Department of Defense be manufactured domestically from American-sourced materials. Qualification cycles for new military boot models can extend from 18 months to over 3 years, encompassing material certification, environmental testing, wear trials, and bureaucratic tender processes. These barriers significantly restrict the ability of new entrants to access defense contracts and limit the pace at which innovative materials and designs can be commercialized into military supply chains.

Budget Austerity and Procurement Delays in Developing Nations

While global defense spending is rising in aggregate, many developing-nation military establishments, particularly across sub-Saharan Africa, parts of Latin America, and South and Southeast Asia, face significant fiscal constraints that delay or downgrade military equipment procurement, including standardized footwear. The International Monetary Fund (IMF)’s fiscal monitors consistently highlight that low-income and lower-middle-income countries devote a disproportionately small share of GDP to defense, and what is budgeted is frequently diverted to hardware platforms over personal equipment. This limits per-capita investment in quality military footwear and sustains a market for lower-cost, functionally inferior products in these geographies, moderating overall global average selling price growth and constraining premium segment penetration in high-growth regional markets.

Opportunity - Surging Demand from Special Forces and Tactical Law Enforcement Units

The global proliferation of special operations forces (SOF) and elite tactical law enforcement units represents one of the highest-value and fastest-growing demand segments in the military boots market. Unlike conventional infantry forces, special operations units operate across an extraordinarily diverse range of terrain and climate environments, from arctic conditions to tropical jungles, desert plateaus, and urban environments, requiring mission-specific, high-performance footwear solutions that command significant price premiums. The U.S. Special Operations Command (SOCOM) manages one of the world’s largest and most technically sophisticated SOF ecosystems, with procurement authority to source specialized commercial-off-the-shelf (COTS) footwear outside standard DoD acquisition channels, enabling faster adoption of advanced materials and designs. As NATO allies collectively expand their SOF capabilities and as counter-terrorism operations sustain demand for rapid-response, mission-versatile tactical boots, manufacturers such as LOWA, Haix, and Danner, recognized SOF suppliers, are exceptionally well-positioned to capture incremental revenue in this premium segment.

Integration of Smart Wearable Technology into Military Footwear

The convergence of soldier systems digitization and advanced materials science is creating a transformative near-term opportunity for military boot manufacturers capable of integrating embedded sensor and connectivity technologies into their products. Research programs at institutions including the MIT Lincoln Laboratory and the U.S. Army Combat Capabilities Development Command (DEVCOM) are advancing wearable foot-mounted sensors capable of real-time soldier biometric monitoring, including fatigue assessment, step count, terrain feedback, and physiological stress indicators, that can be integrated into next-generation military boot platforms. Several NATO nations are actively evaluating smart boot prototypes as components of broader Future Soldier systems. Companies that invest in partnerships with defense electronics integrators and materials specialists to develop certified, ruggedized smart military footwear will be positioned to access a rapidly expanding, high-margin product category that is structurally distinct from conventional boot procurement cycles.

Category-wise Analysis

Boot Type Insights

Combat military boots represent the dominant product category within the military boots market, commanding approximately ~34% of total global market revenue in 2025. Their primacy reflects the universal and non-discretionary nature of combat boot procurement across all standing armies globally, virtually every military service member requires a certified combat boot as their standard-issue footwear regardless of specialization or branch. Combat boots are engineered for durability, ankle support, and protection across rough and mixed terrain, typically incorporating full-grain leather or leather-Cordura® combination uppers, oil- and slip-resistant rubber outsoles, and moisture management systems. The scale of global army procurement programs, including multi-year supply agreements with the U.S. Army, Indian Army (with active strength exceeding 1.4 million personnel), and People’s Liberation Army (PLA), sustains the combat boot segment as the highest-volume category by a significant margin.

Material Insights

Leather remains the dominant material in the military boots market, accounting for approximately ~42% of total segment revenue in 2025. Full-grain and nubuck leather continue to be the most widely specified upper material in military boot procurement standards globally, reflecting leather’s well-established track record of durability, waterproofing performance, abrasion resistance, and conformability to the soldier’s foot over extended wear. Multiple national defense procurement standards, including the U.S. Army’s Military Specifications (MIL-SPEC) and UK Ministry of Defence (MoD) requirements, mandate leather as the primary upper material in standard-issue combat and parade boot categories, providing a regulatory basis for segment dominance. Established military boot suppliers including Bates Footwear, Belleville Boot Company, and Meindl Boots have built their primary product ranges around premium leather construction, reinforcing the material’s commanding commercial position.

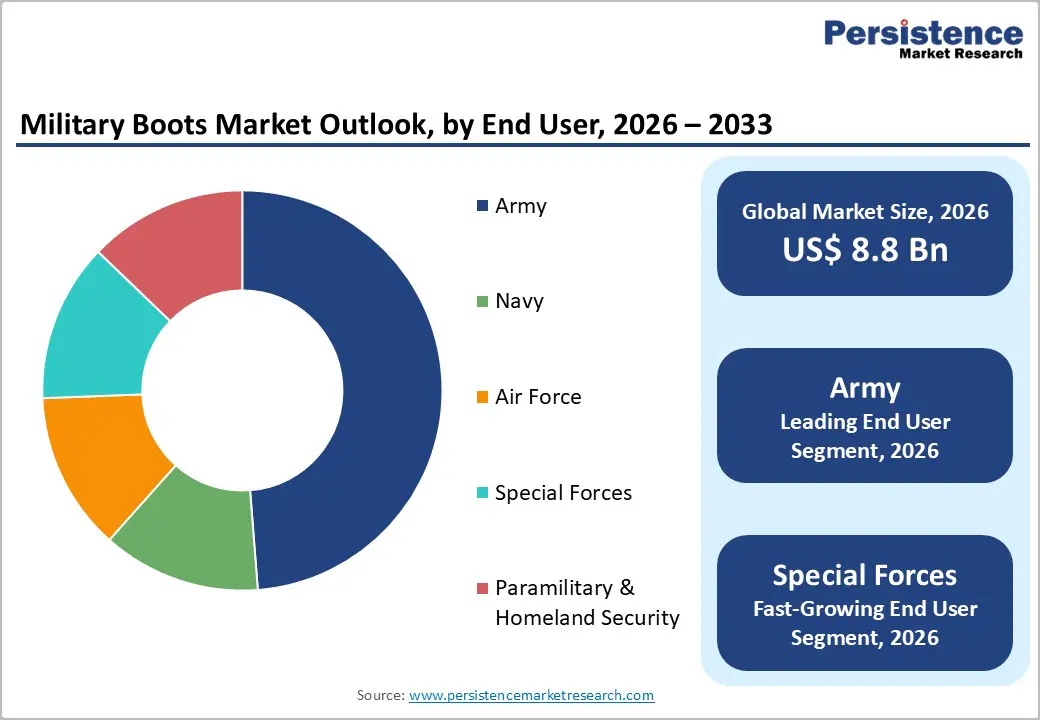

End-user Insights

The Army end-user segment represents the largest and most strategically critical demand category in the military boots market, accounting for approximately ~48% of total market revenue in 2025. Land armies globally constitute the largest branch of national armed forces in virtually every nation, and consequently generate the highest absolute volumes of military boot procurement. The International Institute for Strategic Studies (IISS) Military Balance 2023 estimated that global active military personnel across all branches totals approximately 20 million, with land army personnel representing the substantial majority. Large standing armies, including the People’s Liberation Army (PLA) of China with over 2 million active personnel, the Indian Army with approximately 1.4 million, and the U.S. Army with approximately 450,000 active-duty soldiers, collectively drive enormous annual boot replacement procurement volumes that far exceed other service branches in unit terms.

Regional Insights

North America Military Boots Market Trends and Insights

North America is the leading region in the global military boots market, accounting for an estimated ~33% of global revenue share in 2025, with the United States as the dominant national market by a wide margin. The U.S. Department of Defense (DoD) operates one of the world’s most sophisticated and highest-value military procurement ecosystems, with the U.S. Army, Marine Corps, Navy, and Air Force collectively procuring millions of pairs of boots annually across a wide range of specification categories. The Berry Amendment (10 U.S.C. § 2533a), which requires that footwear and textile products procured by the DoD be manufactured in the United States from domestically sourced materials, creates a protected domestic supply base supporting established manufacturers such as Belleville Boot Company, Bates Footwear, Altama, and Rocky Brands.

Innovation in North America is driven by active U.S. Army Research Laboratory (ARL) and SOCOM programs pursuing next-generation soldier footwear with embedded biometric sensors, thermally adaptive insulation, and additive-manufactured custom orthotic insoles. Canada’s expanding defense commitments under NATO obligations and increasing Arctic sovereignty focus are also driving procurement of specialized cold-weather military boots. The region’s combination of large standing procurement volumes, premium unit prices, stringent domestic content requirements, and active R&D investment sustains North America’s market leadership through the forecast period.

Europe Military Boots Market Trends and Insights

Europe is the second-largest regional market for military boots and is experiencing accelerating demand growth driven by the historic reassessment of defense posture across the continent following Russia’s invasion of Ukraine. NATO member states, particularly Germany, Poland, France, the United Kingdom, and the Nordic nations, are significantly increasing defense spending and executing rapid armed forces expansion and re-equipment programs that include large-scale military boot procurement. The German Bundeswehr has publicly cited critical shortfalls in personal soldier equipment including footwear under its rearmament initiative, with the German Federal Office of Bundeswehr Equipment (BAAINBw) awarding major footwear supply contracts. The UK Ministry of Defence (MoD) has similarly expanded its soldier personal equipment budget under the Integrated Review Refresh 2023.

European military boot manufacturers hold significant competitive advantages in the premium and special forces segments: HAIX, LOWA, and Meindl Boots, all German-headquartered, are among the most widely specified brands by European NATO SOF and commando units, competing on ergonomic certification, terrain-specific engineering, and GORE-TEX® waterproofing technology. France’s Direction Générale de l’Armement (DGA) procurement framework prioritizes domestically certified suppliers, while Spain’s expanding defense budget under its 2024-2028 Defense Plan is generating incremental boot procurement volumes for both conventional and special operations units.

Asia Pacific Military Boots Market Trends and Insights

Asia Pacific is the fastest growing regional market for military boots over the 2026-2033 forecast period, driven by rapid defense budget expansion, large active military personnel bases, and ongoing armed forces modernization programs across China, India, South Korea, Japan, Australia, and ASEAN nations. China commands the world’s largest standing army, the People’s Liberation Army (PLA) with approximately 2 million active personnel, and is executing comprehensive soldier modernization programs under its defense modernization roadmap, prioritizing technologically upgraded personal equipment including terrain-specific performance boots produced by domestic suppliers under centralized procurement through the Central Military Commission (CMC).

India represents one of the highest-growth individual country markets globally for military boots. The Indian Army, with approximately 1.4 million active personnel and ongoing capability upgrades under the Atmanirbhar Bharat (self-reliant India) defense indigenization program, has significantly boosted domestic military footwear procurement, with companies including NS Footwear PVT. Ltd. benefiting from government directives prioritizing Indian-made defense products. Japan’s 2022 National Security Strategy committed to doubling defense spending to 2% of GDP by 2027, creating multi-year procurement expansion opportunities across all personal soldier equipment categories. ASEAN nations including Indonesia, Vietnam, Philippines, and Thailand are similarly expanding military headcounts and modernizing equipment, collectively generating meaningful incremental demand for both domestic and imported military boot products.

Competitive Landscape

The global military boots market is moderately fragmented, comprising large diversified footwear groups, specialized defense footwear manufacturers, and regional suppliers operating within country-specific procurement systems. Competition is strongly influenced by national defense sourcing policies, domestic content mandates, and long-term framework contracts, which create structured but competitive bidding environments. Established manufacturers differentiate through proven performance in extreme environments, compliance with military technical standards, and multi-year supply agreements with armed forces and paramilitary agencies.

Strategic focus areas include advanced material integration for waterproofing, slip resistance, flame retardancy, and enhanced durability under varied terrain conditions. Certification compliance with domestic manufacturing regulations and NATO-aligned standards remains a key competitive lever. Companies are also investing in ergonomic design optimization to reduce soldier fatigue and injury risk, while expanding into digitally enabled fit customization and modular boot systems. Increasingly, sustainability initiatives and recyclable material usage are being incorporated to align with evolving defense procurement guidelines and ESG-oriented supply chain requirements.

Key Developments:

- January, 2026: Milforce Equipment Co., Ltd. showcased its new range of waterproof combat boots designed for tactical and military applications at the IWA OutdoorClassics exhibition in Nuremberg, highlighting enhanced performance and rugged durability.

- May, 2025: Arris Composites developed advanced carbon fibre insoles for military boots following US Army research, now being tested in warm-weather combat boots to assess performance benefits and reduce soldier fatigue and injury risk.

- November, 2024: OTB Boots, Inc. launched its elite tactical footwear line featuring high-performance boots engineered with input from special operations forces for rugged operational use across sea, air, and land environments.

Companies Covered in Military Boots Market

- NS Footwear PVT. Ltd.

- McRae

- Wolverine World Wide

- Belleville Boot Company

- Magnum Boots

- Butex

- Bates Footwear

- Rampage

- Under Armour

- Haix

- Rocky Brands

- Danner

- Altama

- LOWA

- Meindl Boots

- Garmont International S.r.l.

- Corcoran

- Oakley

- Milforce Equipment Co., Ltd.

- Arris Composites

- OTB Boots Inc.

Frequently Asked Questions

The global Military Boots market is valued at US$ 8.8 billion in 2026 and is projected to reach US$ 14.0 billion by 2033 at a CAGR of 6.9%.

Demand is driven by rising global defense spending, military modernization programs, and increasing adoption of ergonomic and performance-enhancing tactical footwear.

North America leads with around 33% revenue share in 2025, supported by strong U.S. defense procurement and domestic manufacturing mandates.

The key opportunity lies in smart military boots integrated with biometric sensors and soldier health monitoring systems.

Key players include Wolverine World Wide, Rocky Brands, Belleville Boot Company, HAIX, and LOWA, among others competing through defense certifications and advanced performance technologies.