- Smart Packaging

- Lubricant Packaging Market

Lubricant Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Lubricant Packaging Market by Product Type (Engine Oil, Greases, Others), Packaging Type (Drums & Kegs, Intermediate Bulk Containers (IBC), Others), Material Type, End-use Industry, and Regional Analysis for 2026 - 2033

Lubricant Packaging Market Size and Trends Analysis

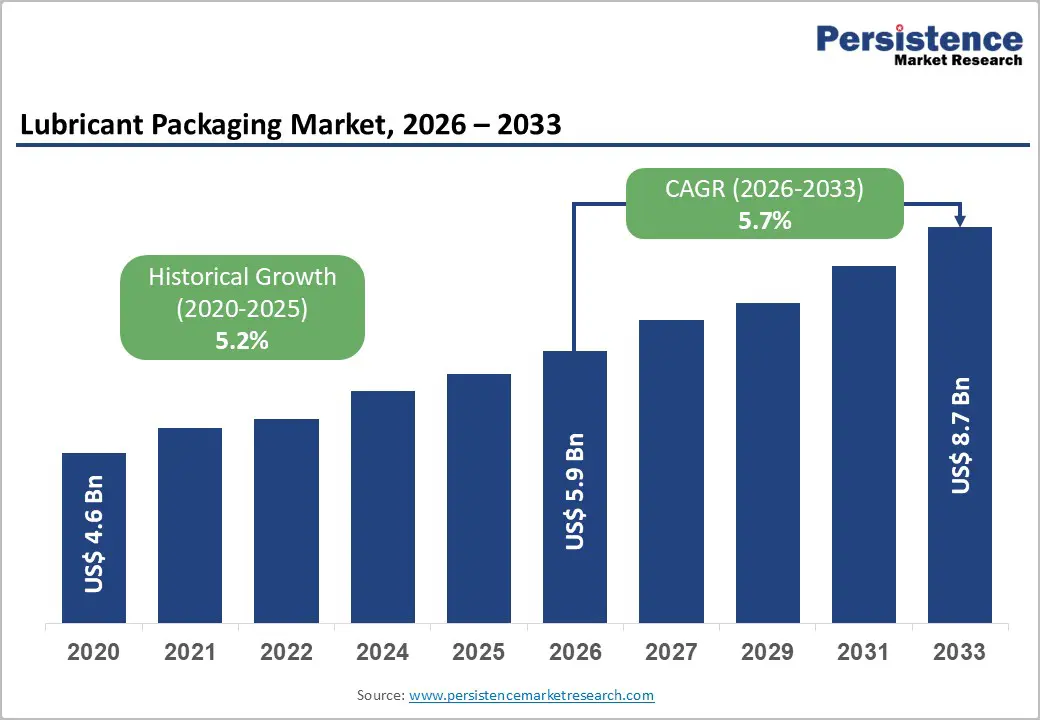

The global lubricant packaging market size is likely to be valued at US$ 5.9 billion in 2026 and is expected to reach US$8.7 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033, supported by rising automotive production volumes, expanding aftermarket servicing activities, and increasing industrial lubrication demand from manufacturing and power generation sectors.

Structural shifts toward bulk logistics efficiency, particularly through Intermediate Bulk Containers (IBCs) and lightweight plastic packaging, are improving cost economics across the value chain. Growth momentum is partially constrained by raw-material price volatility, regulatory pressure on chemical packaging and recycling compliance, and the transition away from single-use plastics. Strategic priorities for market participants center on sustainability integration, supply-chain optimization through regionalized filling models, and value-added dispensing and closure solutions.

Key Industry Highlights

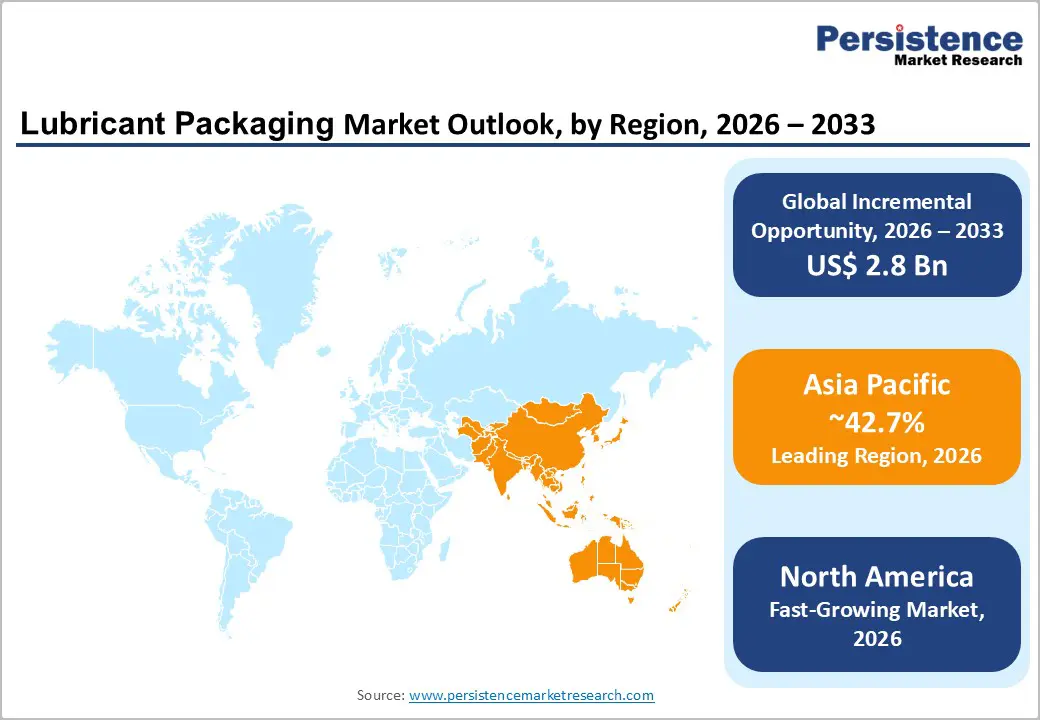

- Leading Region: Asia Pacific is expected to lead the market with approximately 42.7% share, driven by rapid industrialization, automotive production, and high lubricant demand in countries such as China and India.

- Fastest-growing Region: North America, driven by fleet modernization, industrial reshoring, and adoption of recycled-content packaging solutions.

- Investment Plans: Focus on recycled-content integration, lightweighting, IBC pooling, and regional micro-filling hubs, with notable capacity expansions by SCHÜTZ, Greif, and Mauser Packaging Solutions across North America, Europe, and APAC.

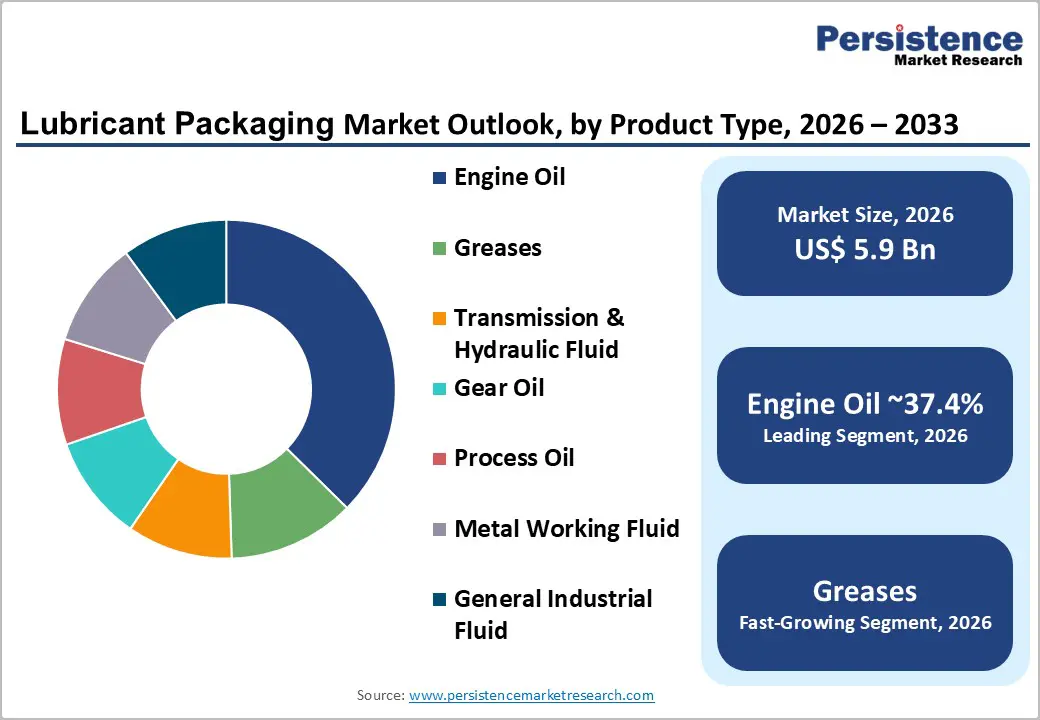

- Dominant Product Type: Engine oil is anticipated to account for 37.4% of the total market share due to recurring vehicle maintenance and widespread consumer adoption.

- Leading Packaging Type: Drums & kegs are estimated to account for approximately 39.8% of the bulk industrial market share, favored for durability, regulatory acceptance, and stackability across industrial sectors.

| Key Insights | Details |

|---|---|

| Lubricant Packaging Market Size (2026E) | US$5.9 Bn |

| Market Value Forecast (2033F) | US$8.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automotive Production and Aftermarket Services Driving Volume Demand

Automotive manufacturing output and aftermarket maintenance cycles remain the primary volume drivers for lubricant packaging demand. Growth in vehicle parc size, particularly in emerging economies, combined with rising vehicle utilization rates, sustains recurring demand for packaged engine oils. Engine oil represents the largest product category, accounting for approximately 37.4% of the total lubricant packaging demand by product type. Increased servicing frequency in commercial vehicle fleets further supports consistent consumption of cans, bottles, and pails. HDPE bottles dominate consumer-facing formats due to ease of handling and cost efficiency, while steel containers are preferred for specialty lubricant grades. Packaging demand shows a direct correlation with the volumes of lubricant packaged, reinforcing the importance of aligning regional packaging capacity with OEM production clusters and aftermarket service hubs.

Logistics Efficiency and Transition toward Bulk Packaging Formats

Industrial lubricant consumers across manufacturing, mining, and power generation are increasingly shifting from small packaging formats to bulk solutions such as drums, kegs, and IBCs. Drums and kegs account for roughly 39.8% of bulk lubricant packaging, while IBCs represent the fastest-growing packaging type due to reduced handling requirements and improved logistics efficiency. Capital investment in modular filling lines and returnable container systems is lowering the total cost of ownership for high-volume lubricant users. This transition is reshaping packaging demand toward large-format containers and service-based models. Packaging suppliers that scale industrial-grade production and offer pooling or refurbishment programs are positioned to capture long-term contracts with industrial lubricant producers.

Material Economics and Sustainability Influencing Packaging Choices

Plastic materials, particularly HDPE and LDPE, account for more than 50% of lubricant packaging volumes, driven by low cost, lightweight properties, and design flexibility. At the same time, regulatory pressure and sustainability commitments from lubricant brands are accelerating the adoption of recycled-content plastics and metal packaging alternatives. Metal containers are gaining traction in premium and high-temperature lubricant applications where durability and barrier protection are critical. Lightweighting initiatives and increased recycled content in metal packaging are improving cost competitiveness while supporting circular economy goals. Packaging suppliers must balance cost efficiency, recyclability, and performance requirements to remain competitive.

Barrier Analysis - Raw-Material Price Volatility and Margin Pressure

Volatility in plastic resins such as HDPE and LDPE, along with fluctuations in steel and tinplate prices, creates persistent margin pressure for lubricant packaging manufacturers. Feedstock cost increases are often not fully passed on to lubricant producers, particularly in price-sensitive segments. Historical price volatility has led to single-digit to double-digit percentage swings in container production costs. For example, a 10% increase in resin prices can raise plastic bottle costs by approximately 2-4%, materially affecting profitability under fixed-price supply contracts. This structural sensitivity increases reliance on long-term supply agreements, diversified material sourcing, and operational efficiency improvements.

Regulatory and Waste-Management Constraints

Regulations governing chemical packaging, hazardous material transport, and waste management add compliance complexity and cost. Packaging must meet certification standards for chemical resistance, stacking strength, and transport safety, increasing testing and documentation requirements. Waste-reduction mandates and recycling targets further restrict packaging material choices, particularly for single-use plastics. Compliance costs can add low single-digit percentage increases to per-unit packaging costs and delay new product introductions by several months. To mitigate these risks, packaging manufacturers must invest in certified designs, traceability systems, and take-back or refurbishment programs.

Opportunity Analysis - Circular Packaging and Recycled-Content Solutions

Growing sustainability commitments from lubricant brands and OEMs are creating strong demand for recycled-content packaging and circular container systems. High-recycled-content plastic bottles and returnable IBC programs are gaining acceptance across North America, Europe, and parts of the Asia Pacific. If circular packaging solutions capture 10-15% of the total market value during the forecast period, this represents a multi-hundred-million-dollar opportunity. Packaging suppliers can capitalize by introducing certified post-consumer recycled plastic containers, closed-loop IBC programs, and refurbishment services. These offerings not only improve sustainability credentials but also generate recurring service revenue.

Regionalized Filling and Fill-At-Source Models

Localized filling hubs near major industrial clusters reduce transportation costs, inventory lead times, and carbon emissions. Industrial lubricant producers increasingly favor regionalized micro-filling models to improve supply-chain resilience. Shifting 15-20% of centralized filling volumes to regional hubs can reduce logistics costs by low double-digit percentages for large consumers. Packaging manufacturers that co-invest in localized filling infrastructure and offer integrated co-packaging services can secure long-term supply agreements and increase margin capture through value-added logistics solutions.

Category-wise Analysis

Product Type Insights

Engine oil packaging is anticipated to account for approximately 37.4% of the market share in 2026, reflecting the recurring nature of engine oil replacement cycles. Growth in passenger vehicle ownership across Asia Pacific, particularly in China and India, combined with stable vehicle maintenance patterns in North America and Europe, sustains consistent per-capita lubricant consumption. This segment generates high packaging volumes through frequent oil changes across passenger cars, light commercial vehicles, and two-wheelers. Packaging demand is heavily concentrated in small-format consumer bottles (0.5-5 liters), multi-pack configurations, and retail-ready packaging formats designed for auto parts stores and service stations. Molded HDPE bottles with tamper-evident closures, induction seals, and integrated pouring spouts remain the industry standard due to chemical resistance and ease of handling. Leading lubricant brands such as Shell, Castrol, TotalEnergies, and ExxonMobil increasingly differentiate through bottle ergonomics, label durability, and anti-counterfeiting features. Engine oil packaging delivers the highest unit volumes and margin stability in the retail lubricant channel, favoring suppliers with advanced blow molding, in-house decoration, and high-speed customization capabilities.

Greases are likely to be the fastest-growing product type in lubricant packaging, driven by rising industrialization, infrastructure development, and increased automation across manufacturing economies. Demand is strongest in mining, construction, marine, railways, wind energy, and heavy equipment manufacturing, where grease lubrication is critical for bearings, gears, and load-bearing components operating under extreme conditions. Grease packaging requires robust pails, drums, cartridges, and heavy-wall containers capable of handling high-viscosity products and repeated mechanical stress. Growth is further supported by the shift from centralized lubrication systems toward cartridge-based and point-of-use lubrication solutions, improving maintenance efficiency and reducing downtime. For example, SKF, Shell Gadus, and Klüber Lubrication increasingly promote cartridge and pail formats for industrial customers. Packaging suppliers that invest in reinforced pail designs, leak-proof lids, and specialized dispensing compatibility are well positioned to secure higher-value industrial contracts and long-term supply agreements.

Packaging Type Insights

Drums and kegs are expected to account for approximately 39.8% of market share in 2026, forming the backbone of bulk lubricant distribution across industrial value chains. Their durability, regulatory acceptance, and compatibility with standard handling equipment make them indispensable in oil & gas operations, power generation facilities, metal processing plants, and large-scale manufacturing units. Both steel and plastic drums are widely used, with material selection guided by temperature tolerance, corrosion resistance, and total cost of ownership. Steel drums are favored for high-temperature and hazardous environments, while HDPE drums are increasingly adopted for corrosion resistance and lower weight. Integrated service offerings, such as filling, palletization, reconditioning, and closed-loop drum pooling, create high switching costs for lubricant producers. Global packaging providers such as Mauser Packaging Solutions, Greif, and SCHÜTZ leverage reconditioning networks to extend drum lifecycles, supporting both cost-efficiency and sustainability objectives while generating recurring service revenue.

Intermediate Bulk Containers (IBCs) are expected to experience accelerated adoption and are the fastest-growing packaging type, driven by superior logistics efficiency, reduced packaging waste, and optimized storage utilization. IBCs are increasingly preferred in centralized lubrication systems, automotive manufacturing plants, chemical processing facilities, and fleet maintenance depots, where high lubricant throughput and controlled dispensing are critical. Recent innovations, such as integrated agitation systems, improved discharge valves, and RFID-enabled tracking, enhance operational visibility and reduce product loss. IBC pooling and refurbishment models, offered by players such as SCHÜTZ and Hoover Ferguson, allow lubricant manufacturers to reduce capital expenditure while improving supply chain efficiency. The shift toward IBCs is driving packaging suppliers to invest in high-volume extrusion blow molding capacity, advanced cage designs, and returnable logistics infrastructure, reinforcing the long-term growth prospects for this segment.

Regional Insights

North America Lubricant Packaging Market Trends - Aftermarket-Driven Demand, PCR Adoption, and Certified Industrial Formats

North America is likely to be the fastest-growing region, supported by a large automotive aftermarket, a diversified industrial base, and one of the world’s most advanced logistics and materials-handling infrastructures. The U.S. accounts for the majority of regional demand, driven by high vehicle ownership, long average vehicle age, and sustained engine oil replacement cycles. Retail lubricant packaging is dominated by HDPE bottles for engine oils, while industrial lubricants rely heavily on steel drums and intermediate bulk containers (IBCs). The presence of major lubricant brands such as ExxonMobil, Chevron, Valvoline, and Phillips 66 reinforces steady packaging volumes across consumer and industrial channels. Growth momentum is further supported by industrial reshoring initiatives, particularly in automotive manufacturing, chemicals, and metalworking, which increase localized lubricant consumption and packaging demand.

Key growth drivers include the expansion of commercial vehicle fleets, rising industrial maintenance intensity, and fleet electrification programs that still require specialty lubricants and greases. Sustainability initiatives are reshaping packaging specifications, with lubricant producers increasingly mandating post-consumer recycled (PCR) content in plastic bottles. Packaging suppliers such as Berry Global, Greif, and Mauser Packaging Solutions have expanded recycled-HDPE integration and reconditioning services to meet these requirements. Regulatory frameworks enforced by agencies such as the U.S. Department of Transportation (DOT) and Environmental Protection Agency (EPA) mandate certified packaging for hazardous materials transport and waste management, increasing compliance complexity and favoring established suppliers. Investment trends emphasize lightweight bottle designs, closed-loop drum programs, and regionalized filling models, while market risks remain tied to volatility in petrochemical feedstock prices and evolving state-level environmental regulations.

Europe Lubricant Packaging Market Trends - EPR-Led Sustainability, Premium Packaging, and Closed-Loop Systems

Europe is a mature, regulation-intensive lubricant packaging market, characterized by strong sustainability mandates, advanced recycling infrastructure, and harmonized regulatory standards. Germany and the U.K. lead regional demand, supported by large automotive manufacturing bases, industrial machinery sectors, and established aftermarket service networks. France, Italy, and Spain contribute meaningful volumes through automotive maintenance and industrial lubrication demand. The region’s packaging ecosystem benefits from well-developed extended producer responsibility (EPR) frameworks and cross-border regulatory alignment under EU packaging and waste directives, which favor reusable, recyclable, and certified packaging solutions.

Growth is driven by stringent environmental policies, OEM sustainability commitments, and demand for premium packaging formats that support brand differentiation and compliance. Lubricant producers such as BP (Castrol), Shell, TotalEnergies, and FUCHS increasingly require high recycled-content HDPE bottles, lightweight steel drums, and IBC pooling systems to reduce lifecycle emissions. Packaging suppliers, including SCHÜTZ, Greif Europe, and Mauser, have expanded IBC pooling, drum reconditioning, and PCR plastic offerings across Germany and the Benelux region. While regulatory complexity raises compliance costs and lengthens product qualification timelines, it also creates high barriers to entry, strengthening the competitive position of certified suppliers. Opportunities are strongest in premium metal packaging, closed-loop IBC systems, and food-grade recycled plastics, while risks include delays in product launches due to evolving certification and reporting requirements.

Asia Pacific Lubricant Packaging Market Trends - Motorization-Led Volume Growth, Localized Production, and Cost-Efficient Formats

Asia Pacific is projected to be the leading region, accounting for 42.7% of the market share, driven by rapid motorization, expanding manufacturing output, and large-scale infrastructure investment. China and India are the primary growth engines, supported by rising passenger vehicle ownership, commercial fleet expansion, and strong demand for industrial lubricants across construction, power generation, and manufacturing. Retail lubricant packaging demand is dominated by small-format HDPE bottles, while bulk industrial consumption fuels growth in drums, pails, and IBCs. Japan, by contrast, emphasizes high-specification lubricants, often packaged in precision-engineered metal containers for automotive and industrial applications.

Key drivers include industrial mechanization, logistics network expansion, and the growth of organized aftermarket services, particularly in India and Southeast Asia. Global lubricant brands such as Shell, BP Castrol, ExxonMobil, and TotalEnergies continue to expand localized packaging and filling operations to improve supply chain responsiveness and reduce costs. Packaging companies, including Time Technoplast, Greif, and SCHÜTZ, have increased investments in blow-molding, drum manufacturing, and IBC assembly facilities across China, India, and ASEAN markets. Regulatory standards vary significantly across countries, influencing material choices and packaging formats, with less harmonization than in Europe. Investment activity remains focused on capacity expansion, localization of production, and cost-efficient packaging designs, positioning Asia Pacific as the primary volume growth region despite ongoing regulatory and infrastructure disparities.

Competitive Landscape

The global lubricant packaging market is moderately concentrated at the global supplier level, with large multinational packaging companies controlling significant shares of IBCs, drums, and rigid plastic containers. At the regional level, the market remains fragmented, particularly in retail bottle production and specialty packaging. Competitive positioning increasingly depends on the ability to integrate material innovation, logistics services, and filling partnerships.

Market leaders emphasize service bundling, material diversification, regional filling partnerships, and digital traceability. Competitive differentiation is increasingly driven by sustainability credentials, certified packaging solutions, and integrated logistics offerings.

Key Industry Developments

- In January 2025, SCHÜTZ signed a strategic licence agreement with the National Plastic Factory Company to begin production of ECOBULK Intermediate Bulk Containers (IBCs) in Saudi Arabia, expanding its regional manufacturing network to serve the Middle East lubricant and chemical markets, with production slated to begin in 2026.

Companies Covered in Lubricant Packaging Market

- Greif

- SCHÜTZ

- Mauser Packaging Solutions

- Berry Global

- Crown Holdings

- Amcor

- Graham Packaging

- Plastipak Packaging

- Time Technoplast

- Balmer Lawrie

- Hoover CS

- DS Smith

- Ardagh Group

- Can-Pack

- Nampak

- Mondi Group

- ALPLA

- BWAY Holding

Frequently Asked Questions

The global lubricant packaging market size is valued at US$ 5.9 billion in 2026.

By 2033, the lubricant packaging market is expected to reach US$ 8.7 billion.

Key trends include growing adoption of recycled-content plastic packaging, expansion of IBC pooling and drum reconditioning programs, increasing demand for retail-ready HDPE engine oil bottles, and rising focus on lightweighting and compliance-driven packaging designs aligned with sustainability regulations.

Engine oil packaging is the leading segment, accounting for approximately 37.4% of market share, due to recurring vehicle maintenance cycles and high-volume consumption in passenger and commercial vehicles.

The lubricant packaging market is projected to grow at a CAGR of 5.7% between 2026 and 2033.

Major players include Greif, Mauser Packaging Solutions, Berry Global, SCHÜTZ, and Time Technoplast.