- Specialty & Fine Chemicals

- Lignosulfonates Market

Lignosulfonates Market Size, Share, and Growth Forecast 2026 - 2033

Lignosulfonates Market by Product Type (Calcium Lignosulfonate, Sodium Lignosulfonate, Magnesium Lignosulfonate, Ammonium Lignosulfonate, Potassium Lignosulfonate, Others), by Form (Liquid, Powder), by Function (Dispersant, Binder, Emulsifier), by End-Use Industry (Construction, Agriculture, Oil & Gas, Mining, Chemical & Industrial Processing), by Regional Analysis, 2026 - 2033

Lignosulfonates Market Size and Trend Analysis

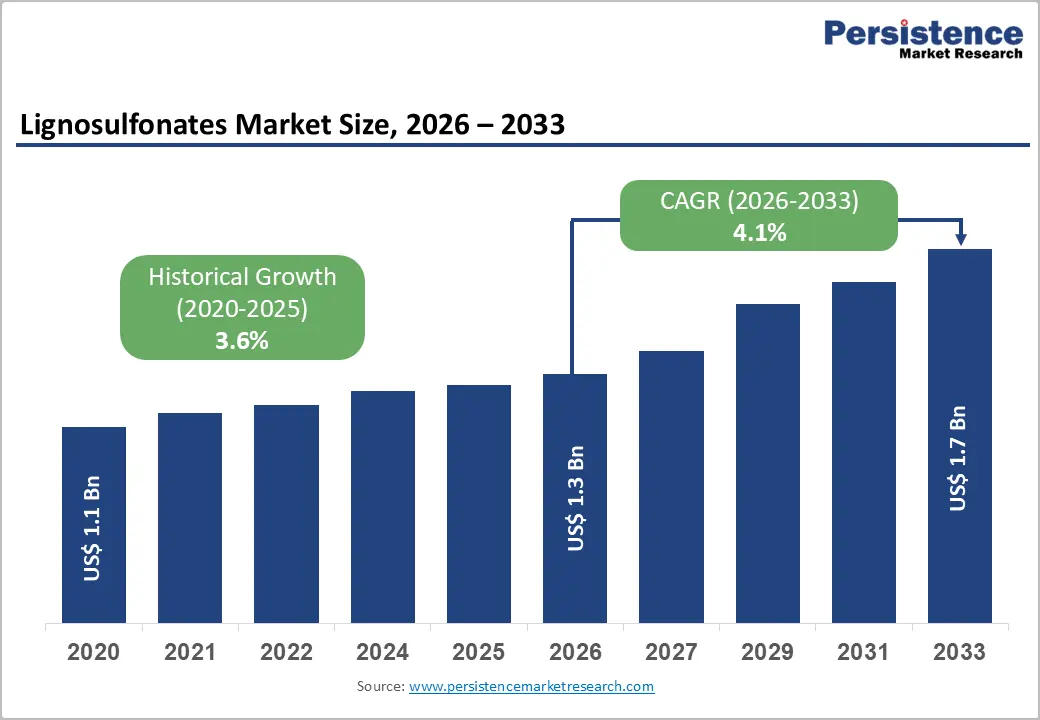

The global lignosulfonates market size is expected to be valued at US$ 1.3 billion in 2026 and projected to reach US$ 1.7 billion by 2033, growing at a CAGR of 4.1% between 2026 and 2033.

The market growth is largely driven by rising demand from the construction sector, fueled by global infrastructure development and urbanization. Lignosulfonates are increasingly used as eco-friendly additives in concrete, supporting sustainable building practices. Expansion in agriculture for soil conditioners and animal feed binders further propels demand. Additionally, the shift toward green chemistry and bio-based alternatives encourages wider adoption of lignosulfonates across industries.

Key Industry Highlights

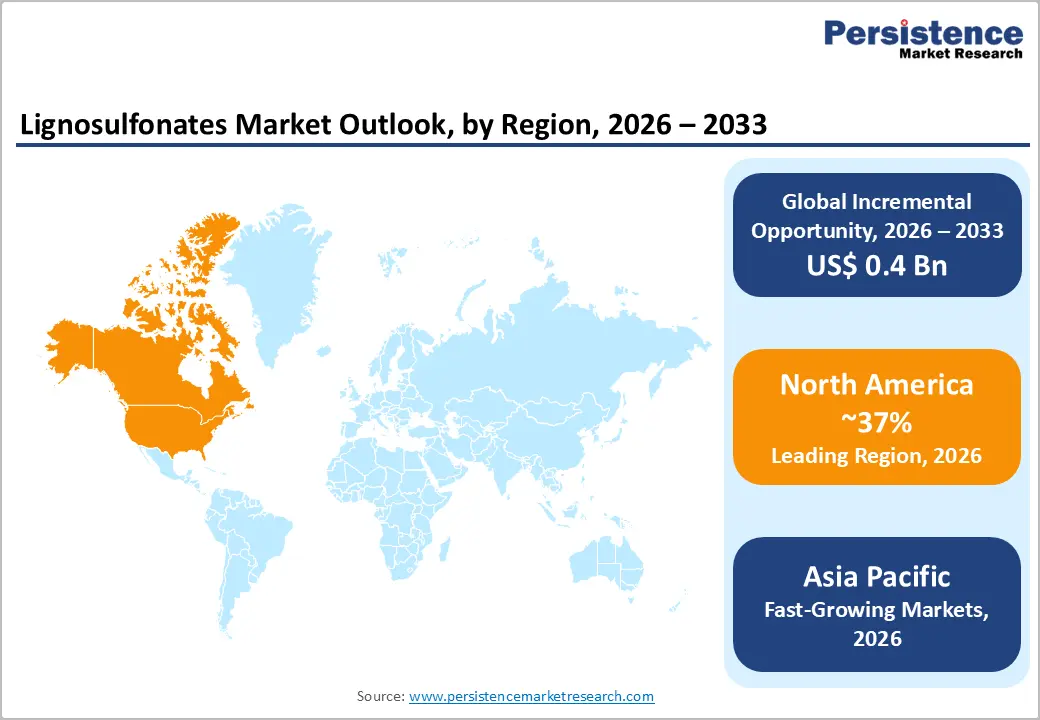

- Leading Region: North America holds 37% share in 2025, driven by strong construction demand, shale oil & gas application, and government support for bio-based chemical innovations.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a CAGR of 5.2% from 2025 to 2032, fueled by manufacturing and infrastructure investments.

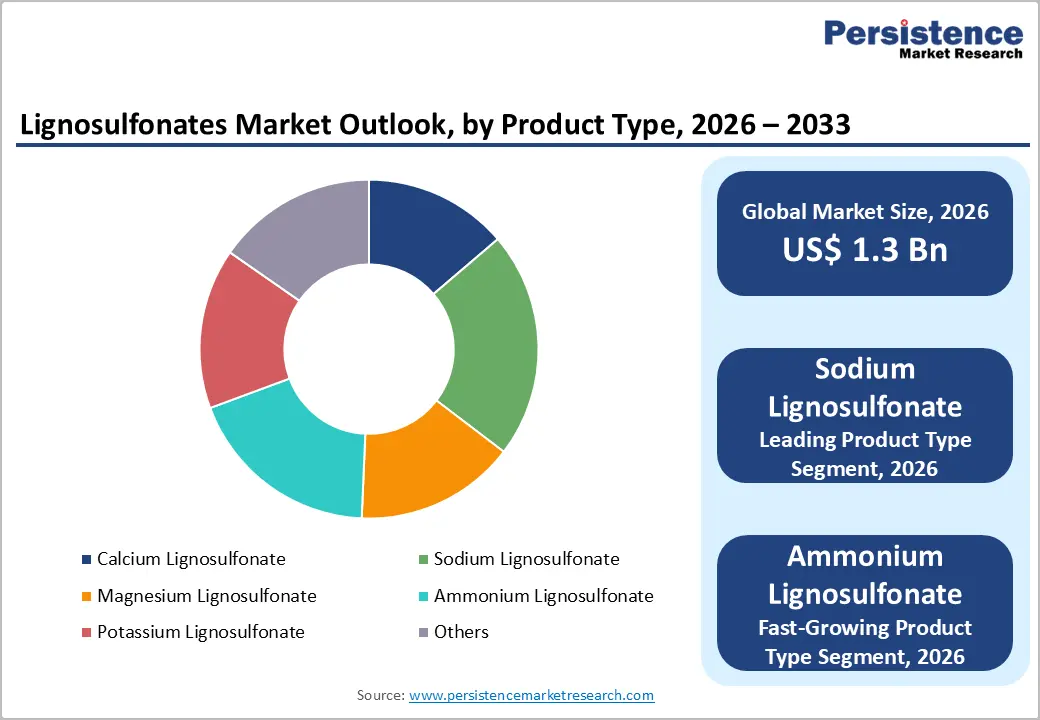

- Leading Product Type: Sodium Lignosulfonate dominates the market with 45% share in 2025, excelling in dispersancy for construction applications.

- Leading Form: Powder form holds 55% share in 2025, preferred for logistics and storage efficiency in agriculture and industrial operations.

- Key Market Opportunity: Green construction innovations provide significant growth potential, aligning with global sustainability policies and eco-friendly building initiatives.

| Key Insights | Details |

|---|---|

| Lignosulfonates Size (2026E) | US$ 1.3 billion |

| Market Value Forecast (2033F) | US$ 1.7 billion |

| Projected Growth CAGR (2026 - 2033) | 4.1% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics

Drivers - Rising Global Construction Activities and Sustainability Initiatives Driving Demand

The surge in construction worldwide, fueled by rapid urbanization and infrastructure expansion, is a primary driver for the lignosulfonates market. United Nations estimates indicate that urban populations will reach 68% by 2050, prompting large-scale projects across Asia Pacific, Europe, and North America. Lignosulfonates act as essential plasticizers and water reducers in concrete, enhancing workability, improving strength, and reducing cement consumption by 10-15%, supporting eco-friendly and sustainable construction practices.

In addition, green building initiatives and low-carbon material mandates in regions like the EU encourage adoption of lignosulfonates in high-performance concrete. Mega-infrastructure developments, including international beltway and port projects, require durable and efficient materials. The demand for these bio-based additives is rising steadily, as they help contractors achieve higher quality while minimizing environmental impact, ensuring widespread market penetration over the coming decade.

Expanding Agricultural Applications and Sustainable Farming Practices Driving Growth

Lignosulfonates are increasingly used in agriculture to improve soil structure, enhance nutrient retention, and support sustainable farming practices. Intensive agriculture has strained soil health, and these additives serve as biodegradable dispersants in pesticides and binders in animal feed pellets. Their multifunctional properties reduce dust in fertilizers, improving handling efficiency by up to 20% while promoting safer and more environmentally friendly applications.

With global food demand projected to increase by 50% by 2050, farmers in emerging economies are adopting these additives to boost crop yields sustainably. Lignosulfonates help optimize fertilizer performance and reduce environmental impact, addressing regulatory and ecological pressures. This growing focus on sustainable agricultural solutions and productivity enhancement is driving significant adoption of lignosulfonates across farming systems worldwide, reinforcing steady market growth.

Restraints - Volatility in Raw Material Supply Chains Poses Challenges to Lignosulfonates Production

The availability of wood pulp, the primary feedstock for lignosulfonates, is subject to significant fluctuations, creating supply chain volatility that restrains market growth. Climate events and variable forestry outputs, as reported by FAO, have caused periodic shortages, such as the 2023 European deficit that raised raw material costs by 15-20%. Such inconsistencies affect manufacturers’ ability to maintain steady production levels.

Additionally, sulfite pulping mills face rising operational costs due to strict emission regulations and environmental compliance requirements. These factors hinder consistent supply to industries like construction and agriculture, increasing production expenses and limiting the scalability of lignosulfonate-based products. Manufacturers must navigate these uncertainties to ensure reliable delivery, which can delay market expansion and affect profitability.

Stringent Environmental and Industrial Regulations Restrict Lignosulfonates Usage

Regulatory barriers present significant challenges for the lignosulfonates market, slowing adoption across industrial sectors. In Europe, compliance with REACH regulations mandates extensive toxicity testing for chemical additives, delaying product approvals and raising adherence costs by roughly 25%. Such requirements affect all new formulations, making market entry cumbersome for smaller producers.

In addition, industry-specific standards impose further restrictions. For example, the Oil & Gas sector’s API standards limit emulsifier usage due to biodegradability and environmental impact concerns. Similarly, mining operations require dispersants that meet zero-discharge norms. These regulatory hurdles constrain product application, slow innovation, and limit market penetration, particularly in environmentally sensitive and highly regulated regions.

Market Opportunities

Advancements in Bio-Based Lignosulfonates Create Growth Opportunities in Sustainable Construction

The shift toward green and sustainable construction practices presents significant opportunities for lignosulfonates. The Global Cement and Concrete Association forecasts a 30% increase in eco-friendly projects by 2030, driving demand for bio-based additives. Lignosulfonates, sourced from renewable lignin, are increasingly replacing synthetic superplasticizers, enhancing concrete performance while reducing environmental impact. Innovations such as modified sodium lignosulfonate improve dispersion by up to 40%, enabling high-strength and durable concrete formulations.

Supportive policies, including the US Inflation Reduction Act and regional green building incentives, further encourage the adoption of bio-additives. R&D initiatives focused on high-performance and eco-friendly concretes, particularly across Asia Pacific’s expanding infrastructure, position lignosulfonates as a key component in sustainable construction, fostering long-term market growth.

Rising Demand in Oilfield Chemicals Opens New Revenue Streams for Lignosulfonates

The Oil & Gas sector provides strong opportunities for lignosulfonates amid ongoing industry recovery. The International Energy Agency projects a 5% annual increase in drilling activities through 2030, heightening the need for efficient drilling fluid additives. Lignosulfonates act as emulsifiers, stabilizing fluids and reducing fluid loss by up to 25% in shale operations, enhancing operational efficiency and lowering costs.

Emerging carbon capture, utilization, and storage (CCUS) projects require dispersants for slurry handling, while government incentives and DOE grants supporting green chemical applications accelerate market adoption. These trends create significant revenue potential for suppliers targeting high-demand regions like the Middle East and North America, reinforcing the strategic value of lignosulfonates in oilfield chemical applications.

Category-wise Analysis

Product Type Insights

Sodium lignosulfonate dominates the market, holding 45% share in 2025 due to its superior solubility, cost-effectiveness, and versatility. It is widely used in concrete admixtures, accounting for 50% of construction applications, with pH stability (7-10) and 20% higher dispersancy performance compared to other types. Reliable supply from Nordic sulfite pulp mills ensures consistent availability, reinforcing its strong position across industrial applications including agriculture, oilfield chemicals, and mining.

Emerging demand for magnesium and ammonium lignosulfonates is notable in niche applications requiring specialized binding and emulsifying properties. These variants are increasingly adopted in high-performance concrete, animal feed formulations, and specialty chemical processes, where tailored functional performance is critical. Innovation in modified lignosulfonates further supports their expansion, particularly in environmentally conscious and high-efficiency applications.

Form Insights

Powder lignosulfonates hold a 55% market share in 2025, favored for bulk handling, storage efficiency, and reduced moisture content (<5%) that prevents caking. Their suitability for dry-mix concrete and feed binder applications, along with ease of transport, particularly in Asia Pacific logistics hubs, reinforces dominance. The powder’s versatility and stability make it the preferred choice in large-scale industrial and agricultural operations.

Liquid lignosulfonates are witnessing faster adoption due to convenience in field applications and seamless blending in industrial processes. Ready-to-use formulations reduce preparation time and improve consistency in high-volume concrete plants and oilfield chemical operations. Growing interest in liquid dispersants in emerging markets and for specialized agricultural treatments is driving their uptake.

Function Insights

Dispersants account for 50% of the market in 2025, being essential in cement hydration control, improving particle flow by up to 30%, and preventing slurry settling in mining, boosting throughput by 25%. Their multifunctional role across construction, mining, and chemical processing secures a dominant position, supported by standardized performance validation in industry protocols.

Binder and emulsifier functions are gaining momentum as industries seek multifunctional additives. Binders improve feed pellet durability and soil conditioning, while emulsifiers stabilize drilling fluids and pesticide formulations. Increasing regulatory emphasis on eco-friendly, bio-based solutions amplifies the adoption of these functional applications, particularly in agriculture and oilfield chemicals, offering growth potential.

Industry Insights

Construction dominates with 40% market share in 2025, driven by global infrastructure expansion and high-rise projects funded through World Bank and regional investment initiatives exceeding US$ 100 billion annually. Lignosulfonates enhance concrete performance by reducing water usage by 15-20% and contribute to green building certifications, strengthening their role in sustainable construction practices.

Agriculture and oil & gas sectors are rapidly emerging as growth engines. In agriculture, lignosulfonates improve soil structure, fertilizer dispersal, and animal feed binding efficiency. In oil & gas, they stabilize drilling fluids and reduce fluid loss in shale operations. Rising demand for sustainable and high-performance applications across these industries is accelerating market adoption beyond traditional construction usage.

Regional Insights

North America Lignosulfonates Market Trends and Insights

North America accounts for 37% of the global lignosulfonates market in 2025, with the U.S. as the primary contributor. Strong innovation is driven by DOE bioeconomy initiatives and NIST-funded R&D projects for advanced concrete admixtures. EPA regulations promote lignin valorization from over 200 pulp mills, ensuring a steady supply of high-quality feedstock. Construction dominates usage, supported by the ASCE infrastructure report card rating of D+, which has triggered over US$ 1 trillion in infrastructure investments. The oil & gas sector also drives demand, particularly shale plays that rely on lignosulfonates as efficient emulsifiers for drilling fluids.

Emerging applications in sustainable agriculture and industrial processing are creating additional growth opportunities. The push for eco-friendly additives, combined with government support for bio-based chemical adoption, is strengthening market adoption. Industrial stakeholders are increasingly focusing on high-performance dispersants and binders, supporting steady growth in North America over the forecast period.

Europe Lignosulfonates Market Trends and Insights

Europe is witnessing steady growth in the lignosulfonates market, with a projected CAGR of 4.3% from 2025 to 2032. Germany leads production with REACH-compliant facilities, while Fraunhofer Institute trials demonstrate up to 20% emission reductions using lignosulfonates. EU Green Deal policies harmonize sustainability standards across agriculture and construction, promoting the adoption of eco-friendly additives. The UK and France are emphasizing renewable applications, while Spain’s mining sector increasingly uses lignosulfonates to comply with EU zero-waste directives. Powder forms are expanding following 2024 ECHA approvals, supporting versatility across multiple industries.

Growing demand in sustainable construction, industrial processing, and agriculture is driving product innovation. Companies are focusing on high-performance formulations to meet stricter environmental regulations. Expansion in green building projects, mining compliance requirements, and bio-based additive adoption ensures Europe remains a key strategic market with long-term growth potential.

Asia Pacific Lignosulfonates Market Trends and Insights

Asia Pacific holds 35% of the global lignosulfonates market in 2025 and is the fastest-growing region with a CAGR of 5.2% from 2025 to 2032. China drives growth through its 14th Five-Year Plan, emphasizing green chemicals, with over 50 new pulping facilities reported by MIIT. India extensively incorporates lignosulfonates in its PM Gati Shakti infrastructure program, boosting construction applications. Japan focuses on bio-dispersant innovations, supported by METI subsidies, while ASEAN hubs such as Indonesia leverage low-cost manufacturing to serve domestic and export markets.

Urbanization, industrial expansion, and green infrastructure initiatives underpin demand across the region. Lignosulfonates are increasingly adopted in construction, agriculture, and oilfield chemicals for high-performance, eco-friendly applications. Continuous investment in manufacturing capacity and R&D further strengthens Asia Pacific’s market leadership and ensures sustainable growth momentum over the forecast period.Top of Form

Competitive Landscape

The lignosulfonates market is moderately consolidated, with leading players leveraging integrated pulping operations to maintain a strong position. Companies focus on expanding production capacities, particularly in high-growth regions, while investing in R&D to develop high-purity and specialty grades that meet diverse industrial requirements. Sustainability and eco-friendly practices, such as ISO 14001 certifications, serve as key differentiators in a competitive environment.

Emerging market models emphasize the circular economy, promoting the recycling and valorization of lignin byproducts to create bio-based, high-performance additives. Customization of formulations for construction, agriculture, and industrial applications further strengthens competitive positioning and supports long-term growth opportunities.

Key Market Developments

- In March 2025, Borregaard launched a bio-based lignosulfonate specifically for concrete applications, claiming a 25% improvement in strength per internal company tests. The product targets sustainable construction projects and aligns with growing green building initiatives globally.

- In July 2024, LignoStar expanded its production capacity in Europe by 20,000 tons to meet increasing demand, driven by EU green building mandates and sustainability regulations. The expansion strengthens its supply chain for construction and industrial applications across the region.

- In November 2023, GreenValue introduced an ammonium lignosulfonate variant for agricultural use, certified under FAO standards. The product enhances soil conditioning and fertilizer dispersal, supporting eco-friendly and efficient crop production across emerging and established farming markets.

Companies Covered in Lignosulfonates Market

- Borregaard ASA

- Rayonier Advanced Materials

- Sappi Limited

- Nippon Paper Industries Co., Ltd.

- Domsjö Fabriker AB

- Burgo Group S.p.A.

- Domtar Corporation

- Flambeau River Papers

- LignoTech USA LLC

- Kemira Oyj

- Green Agrochem

- Shenyang Xingzhenghe Chemical Co., Ltd.

- Wuhan Xinyingda Chemicals Co., Ltd.

- Fujian Xinxin Chemical Co., Ltd.

- Tianjin Yeats Chemical Co., Ltd.

Frequently Asked Questions

The global Lignosulfonates Market is expected to reach US$ 1.3 billion in 2026, growing to US$ 1.7 billion by 2033 at 4.1% CAGR.

Construction infrastructure and agriculture applications drive demand, with lignosulfonates enabling water reduction and soil enhancement amid urbanization and food security needs.

North America leads with 37% share in 2025, supported by construction investments, shale oil & gas applications, and government initiatives for bio-based chemical adoption.

Bio-based innovations for green construction offer significant potential, supported by policies like EU Green Deal and US incentives for sustainable additives.

Leading companies include Borregaard LignoTech, LignoStar Group, GreenValue Additives, Sino-Lignin, and Nippon Paper Industries, focusing on R&D and expansions.