- Biotechnology

- Laboratory Developed Testing Market

Laboratory Developed Testing Market Size, Share, Trends, Growth, and Regional Forecast, 2025 - 2032

Laboratory Developed Testing Market by Test Type (Clinical Biochemistry, Hematology, Immunology, Microbiology, Molecular Diagnostics, Others), Application (Oncology, Genetics, Infectious Diseases, Autoimmune Disorders, Others), End-user, and Regional Analysis from 2025 - 2032

Laboratory Developed Testing Market Share and Trends Analysis

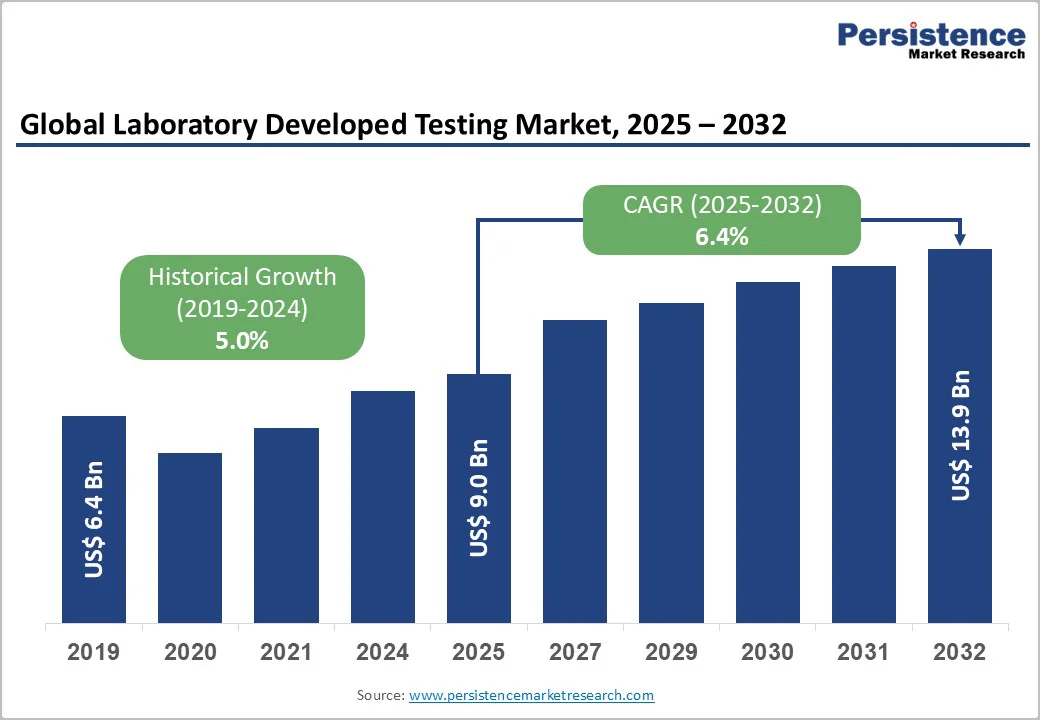

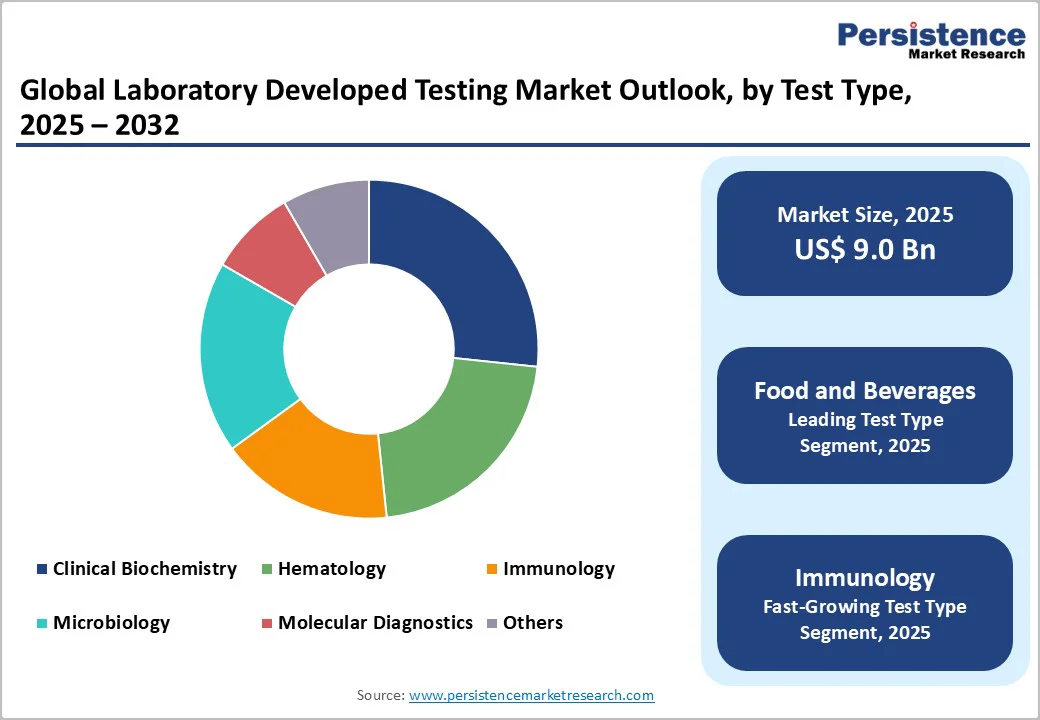

The global laboratory developed testing market size is valued at US$9.0 billion in 2025 and is projected to reach US$13.9 billion growing at a CAGR of 6.4% during the forecast period from 2025 to 2032.

Rising demand for precision medicine, increasing prevalence of cancer and genetic disorders, and advances in molecular diagnostics and immunoassays have encouraged the need for the laboratory-developed testing market. LDTs are gaining traction due to their ability to offer personalized and accurate diagnostic solutions, especially in complex disease management. The market is also influenced by technological innovations that enhance test accuracy and turnaround time. However, evolving regulatory frameworks and quality standards pose challenges.

Key Industry Highlights:

- Next-Generation Sequencing (NGS) and molecular diagnostics dominate the LDT market. These technologies offer high accuracy, rapid turnaround, and the ability to detect complex genetic and molecular anomalies.

- Oncology remains the largest application for LDTs, while rare and genetic disorders are the fastest-growing segments.

- LDTs are increasingly using non-invasive sample types such as saliva, urine, or blood spots, facilitating patient-friendly diagnostics.

- While hospital-based laboratories remain dominant, there is a noticeable shift toward direct-to-consumer (DTC) testing and specialized reference laboratories.

| Key Insights | Details |

|---|---|

|

Laboratory Developed Testing Market Size (2025E) |

US$9.0 Bn |

|

Market Value Forecast (2032F) |

US$13.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.0% |

Market Dynamics

Driver - Increasing Product Offerings Related to Genetic Health Risks

Manufacturers of laboratory-developed tests (LDTs) are poised for significant growth in the coming years, driven by increasing investment in research and development to expand and diversify their product portfolios. Companies are focusing on innovation to offer comprehensive solutions, including genetic health risk assessments, ancestry insights, and trait analysis.

For example, the merger of 23andMe and Virgin Group’s VG Acquisition Corp. has created a publicly traded entity aimed at advancing personalized healthcare and therapeutics through human genetics. Additionally, regulatory approvals are fueling market momentum, such as the U.S. FDA’s July 2024 approval of Guardant Health’s Shield™ blood test for colorectal cancer screening in adults aged 45 and above, which also qualifies for Medicare coverage as a primary screening option.

Restraints - Low Consumer Awareness in Developing Regions

Recalls of diagnostic products are a standard safety practice aimed at preventing errors or addressing existing defects. Laboratory-developed tests (LDTs), used to detect a range of conditions, including infectious diseases like COVID-19, genetic disorders, and various cancers, are not centrally registered or tracked, making it difficult to assess their performance or compare them with FDA-approved diagnostics. Furthermore, insurance coverage and eHealth systems do not distinguish between LDTs and FDA-cleared tests, and no comprehensive database exists for all LDTs. Notable recalls highlight these challenges.

- In January 2022, LuSys Laboratories recalled three tests: a saliva antigen test, an IgG/IgM antibody test, and a nasal antigen test due to a high risk of inaccurate results.

- Similarly, in October 2021, Abbott Laboratories issued a Class I recall for its Alinity m Resp-4-Plex AMP and Alinity m SARS-CoV-2 AMP COVID test kits. Such recalls underscore the regulatory and quality challenges that restrain market growth.

Opportunity - Expansion in Liquid Biopsy Techniques

The development of liquid biopsies represents a transformative opportunity in the LDT market, enabling non-invasive, blood-based testing for early cancer detection, disease monitoring, and treatment personalization. Unlike traditional tissue biopsies, liquid biopsies reduce patient discomfort, allow for frequent sampling, and provide real-time insights into tumor genetics and heterogeneity. These tests can detect minimal residual disease, emerging mutations, and therapy resistance, supporting precision oncology. Advances in circulating tumor DNA (ctDNA) and circulating tumor cell (CTC) analysis, combined with AI-driven data interpretation, further enhance diagnostic accuracy. As oncology care increasingly shifts toward personalized and proactive strategies, liquid biopsies are set to redefine cancer management globally.

Category-wise Analysis

By Test Type, the Molecular Diagnostics Segment is Leading in the Market

Molecular diagnostics leads the laboratory-developed testing market due to its ability to detect diseases at the genetic and molecular level with high precision and sensitivity. It enables early diagnosis, monitors disease progression, and guides personalized treatment decisions, particularly in oncology, infectious diseases, and rare genetic disorders. Technological advancements such as PCR, next-generation sequencing, and CRISPR-based assays have expanded its applications and improved turnaround times. Additionally, rising demand for precision medicine, growing awareness of genetic testing, and increasing regulatory approvals for molecular tests have further strengthened its market dominance. Its versatility and clinical relevance make it the preferred choice over other test types.

By End-user, the Hospital-Based Laboratories Segment is Leading

Hospital-based laboratories account for the largest share of the Laboratory Developed Testing (LDT) market due to their direct access to diverse patient populations and complex clinical cases. These facilities possess advanced infrastructure, skilled personnel, and established quality systems, enabling them to rapidly design and validate specialized tests. Integration with hospital care workflows allows for immediate clinical application and faster decision-making. Moreover, hospitals often collaborate with research institutes and diagnostic companies to develop novel assays, particularly for oncology, infectious diseases, and genetic disorders. Their strong funding support, regulatory compliance, and continuous innovation reinforce their leadership in the global LDT market.

Regional Insights

North America Laboratory Developed Testing Market Trends and Analysis

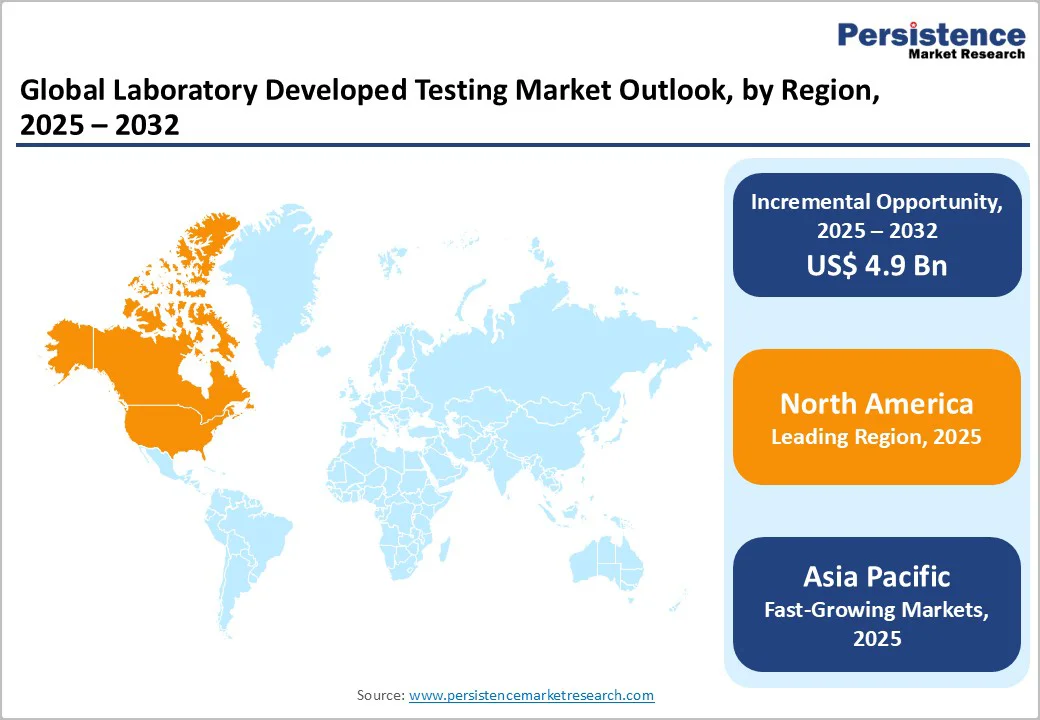

In 2024, the North America laboratory developed test market contributed around 36.4% revenue share within the global market. North America’s advanced healthcare infrastructure, a well-established regulatory framework, high levels of investment in biotechnology, and a robust presence of leading biopharma companies collectively drive the growth and innovation of LDTs.

Furthermore, the development and commercialization of LDTs in the U.S. have also been promoted locally by regulatory agencies such as the FDA, which provide clear and supportive guidelines. The rising prevalence of chronic diseases demands precision diagnostics and personalized medicine, further boosting the adoption of LDTs. Thus, making the U.S. laboratory test market a key driver for growth in the North American diagnostics industry.

- In May 2024, the FDA issued a final rule to enhance the safety and effectiveness of laboratory-developed tests (LDTs). The rule clarifies that in vitro diagnostic products (IVDs) are considered devices under the FD&C Act, even when manufactured by laboratories. The FDA will gradually phase out its general enforcement discretion for LDTs over four years, while introducing targeted enforcement policies for certain IVD categories.

Asia Pacific Laboratory Developed Testing Market Trends and Analysis

Asia Pacific is emerging as a dynamic hub for laboratory-developed testing (LDT) growth, driven by expanding healthcare infrastructure, rising disease burden, and increasing adoption of precision diagnostics. Rapid urbanization, growing middle-class populations, and government initiatives to improve molecular testing capacity are accelerating market penetration. Countries such as China, India, Japan, and South Korea are witnessing strong investments in genomics and biopharmaceutical research. Local laboratories are developing cost-effective and customized LDTs tailored to regional disease profiles. Collaborations between global diagnostic firms and regional players further support technology transfer, regulatory alignment, and innovation across the evolving Asia Pacific diagnostics landscape.

Competitive Landscape

The global laboratory developed testing (LDT) market is moderately competitive, characterized by a blend of large diagnostic networks, academic laboratories, and emerging biotech innovators. Competition is driven by continuous advancements in molecular diagnostics, automation, and data analytics. Laboratories are focusing on developing high-complexity, disease-specific assays to strengthen their clinical value. Strategic collaborations between hospitals, research institutions, and technology developers are fostering innovation and expanding testing capabilities.

Key Industry Developments:

- In January 2025, Adaptive Biotechnologies partnered with NeoGenomics for a multi-year exclusive strategic commercial collaboration to enhance minimal residual disease (MRD) monitoring for patients with certain blood cancers. The partnership combines Adaptive’s next-generation sequencing (NGS)-based clonoSEQ® with NeoGenomics' COMPASS and CHART assessment services.

- In January 2023, Quanterix Corporation announced the validation of a Laboratory Developed Test (LDT) designed to quantitatively measure neurofilament light chain (NfL) in serum, assisting in the evaluation of individuals for potential neurodegenerative conditions or other causes of neuronal or central nervous system damage.

Companies Covered in Laboratory Developed Testing Market

- Thermo Fisher Scientific Inc.

- Kaneka Eurogentec S.A.

- QIAGEN

- Vastian

- Roche Diagnostics

- Adaptive Biotechnologies.

- Guardant Health, Inc.

- Smiths Medical

- Quest Diagnostics

- Beckman Coulter

- OPKO Health, Inc.

- Siemens Medical Solutions USA, Inc.

- Quanterix

- Proteomics International

- Others

Frequently Asked Questions

The global laboratory developed testing market is valued at US$9.0 Bn in 2025.

The global Laboratory Developed Testing (LDT) market is driven by the rising demand for personalized and precision medicine, enabling tailored diagnosis and treatment planning. The increasing prevalence of cancer, infectious, and genetic diseases is fueling the need for advanced diagnostic solutions.

The global Laboratory Developed Testing (LDT) market is poised to witness a CAGR of 6.4% between 2025 and 2032.

The Laboratory Developed Testing (LDT) market offers significant opportunities driven by rapid technological innovation and unmet diagnostic needs.

Thermo Fisher Scientific Inc., Kaneka Eurogentec S.A., QIAGEN, Vastian, Roche Diagnostics, and others.