- Industrial Goods & Service

- Industrial Food Milling Machine Market

Industrial Food Milling Machine Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Food Milling Machine Market by Product Type (Rice Milling Machines, Wheat Flour Milling Machines, Corn Milling Machines, Grain Milling Machines, Spice Milling Machines, Food Processing Mills, Cereal Milling Machines), Technology (Mechanical Milling, Pneumatic Milling, Cryogenic Milling, Ultrasonic Milling, Wet Milling, Dry Milling), Application, End-user, by Regional Analysis, 2026 - 2033

Industrial Food Milling Machine Market Size and Trend Analysis

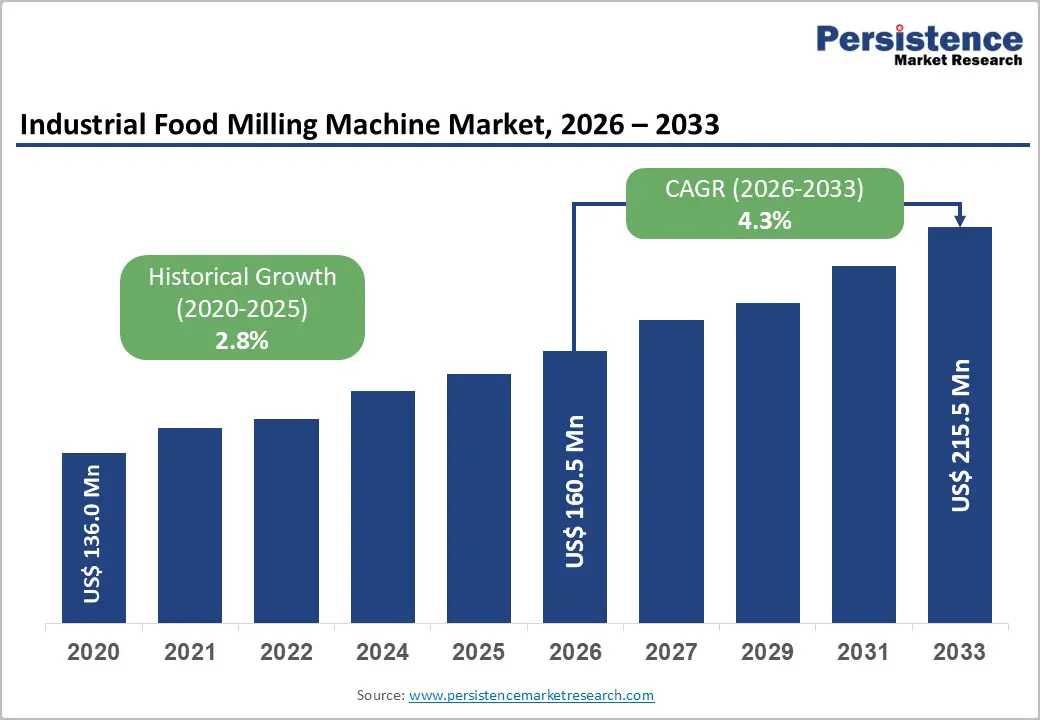

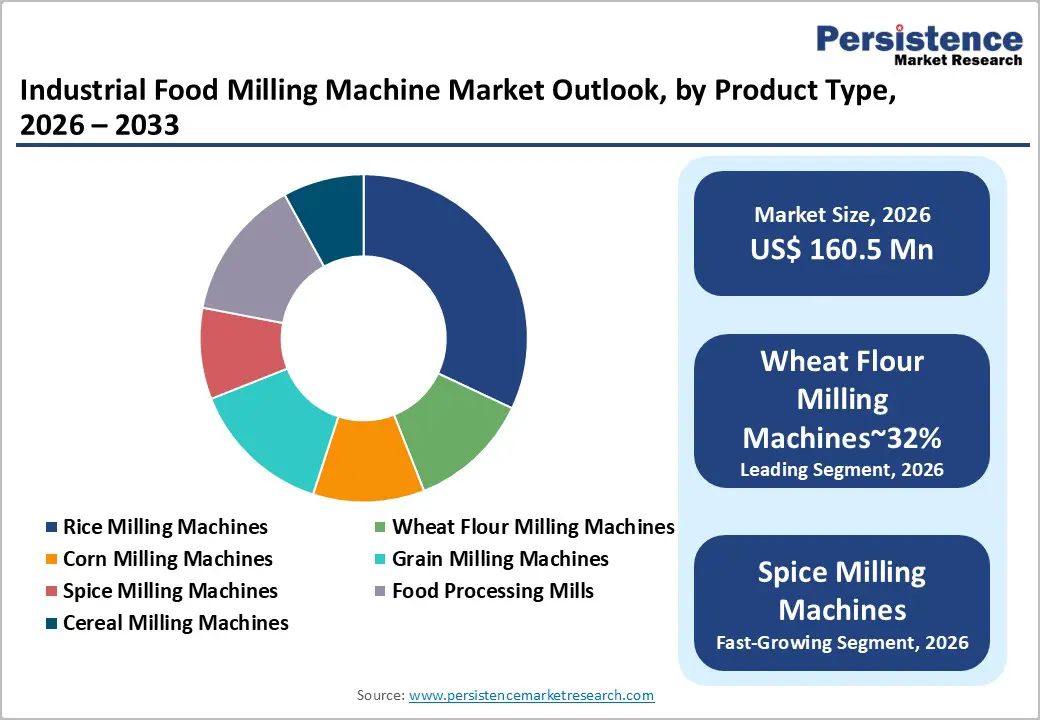

The global industrial food milling machine market size is likely to be valued at US$ 160.5 Million in 2026 and is expected to reach US$ 215.5 Million by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033.

The market is driven by surging global food production demands, accelerating automation in food processing facilities, and rising adoption of advanced milling technologies such as cryogenic and ultrasonic milling for value-added applications.

Key Market Highlights

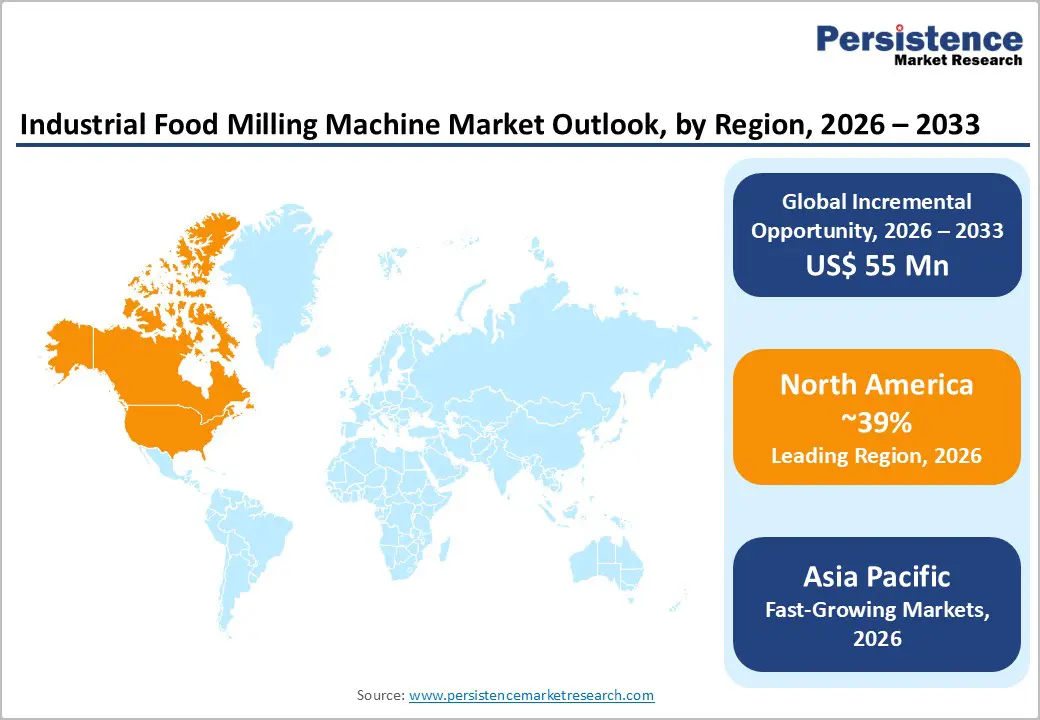

- Leading Region: North America leads the Industrial Food Milling Machine Market holding 39% share, driven by the U.S. food processing industry's scale, FSMA-mandated equipment upgrades, and advanced adoption of automated, IoT-integrated milling systems, with daily U.S. wheat flour milling capacity exceeding 1.4 million hundredweight.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR of 6.1%, propelled by China's grain output exceeding 650 million tonnes annually, India's PLI Scheme attracting food processing investment, and rapid milling capacity expansion across ASEAN nations driven by export-oriented food manufacturing growth.

- Dominant Segment: Wheat Flour Milling Machines dominate the product type category with 32% market share, underpinned by global wheat production consistently exceeding 770 million tonnes annually and structural dependence on wheat flour across major food systems including bakery, noodles, and pasta processing.

- Fastest Growing Segment: Cryogenic Milling technology is the fastest growing segment, driven by expanding nutraceutical, herbal supplement, and plant-based ingredient manufacturing, where preservation of bioactive compounds at ultra-low temperatures commands significant price premiums and differentiates product quality.

- Key Market Opportunity: The herbal, nutraceutical, and specialty food milling segment offers the highest-value growth opportunity, as the global wellness economy, valued at over US$ 5.6 trillion, drives demand for precision cryogenic and ultra-fine milling equipment with strict hygiene and bioactive-preservation specifications.

Market Dynamics

Market Growth Drivers

Escalating Global Demand for Processed and Packaged Food

Rising urbanization, expanding middle-class populations, and shifting dietary preferences toward processed and convenience foods are generating robust demand for high-capacity industrial food milling equipment. The FAO estimates that global food demand will increase by approximately 50% by 2050 compared to 2013 levels, requiring commensurate scaling of food processing infrastructure.

The World Bank notes that agri-food systems now account for roughly one-third of global GDP, with food processing forming the largest manufacturing sector in many economies. Industrial milling machines are foundational equipment for flour milling, rice processing, spice grinding, and confectionery production, segments all experiencing capacity expansion globally. This structural, long-term demand for efficient, high-throughput milling equipment is a primary market growth engine.

Automation and Industry 4.0 Integration in Food Processing

The adoption of automation, digitization, and smart manufacturing principles in food processing facilities is a significant catalyst for premium industrial food milling machine demand. The International Federation of Robotics (IFR) reported that food and beverage was among the top five industries for industrial robot installations globally.

Modern milling systems integrated with SCADA (Supervisory Control and Data Acquisition), IoT sensors, and AI-based quality control are increasingly preferred by large-scale processors seeking to reduce labor costs, minimize waste, and ensure product consistency. Leading manufacturers such as Bühler Group have invested heavily in digital milling platforms, Bühler's Mercury smart milling system exemplifies this trend, offering real-time process monitoring that reduces energy consumption by up to 10-15%. This technology-upgrade cycle is driving higher-value equipment replacements across the sector.

Market Restraints

High Capital Investment and Long Payback Periods

Industrial food milling machines, particularly high-precision systems employing cryogenic, ultrasonic, or pneumatic technologies, represent significant capital expenditure for food processors. Entry-level commercial milling systems can range from tens of thousands to hundreds of thousands of U.S. dollars, while turnkey flour or rice milling plant installations often exceed US$ 1 million.

For small and medium-sized processors in developing markets, these investment thresholds are prohibitive. The World Bank's Enterprise Survey consistently identifies access to finance as a top constraint for agri-food businesses in emerging economies, limiting market penetration in high-growth regions and moderating the pace of equipment adoption.

High Energy Consumption and Operational Efficiency Concerns

Industrial milling operations are energy-intensive, with milling and grinding among the most power-hungry processes in food manufacturing. The U.S. Department of Energy (DOE) estimates that grinding and size reduction account for approximately 5% of total U.S. industrial electricity consumption.

Rising energy costs, exacerbated by post-2022 global energy market disruptions, are squeezing processor margins and creating hesitancy around new equipment acquisitions. While newer generation machines offer improved efficiency, legacy installed bases in cost-sensitive markets present a significant barrier to upgrading, dampening replacement demand and limiting the market's near-term growth rate.

Market Opportunities

Rapid Growth of Herbal, Nutraceutical, and Specialty Food Milling

The global surge in consumer demand for herbal supplements, plant-based proteins, and nutraceutical powders is creating a high-value, fast-growing niche for specialized industrial milling machines. The Global Wellness Institute valued the wellness economy at over US$ 5.6 trillion in 2022, with botanical and herbal supplement manufacturing as a key growth pillar.

Processing heat-sensitive botanical ingredients, such as turmeric, moringa, and ashwagandha, requires cryogenic or ultra-low-temperature milling to preserve bioactive compounds, a technically demanding application where premium equipment from manufacturers like NETZSCH Group and Hosokawa Micron Group commands significant price premiums. As nutraceutical contract manufacturing scales up across North America, Europe, and India, this segment offers strong incremental demand for highly specialized milling solutions.

Expanding Animal Feed and Pet Food Processing Sector

The global animal feed and pet food industries represent a high-growth demand channel for industrial food milling equipment. According to the International Feed Industry Federation (IFIF), global compound feed production exceeded 1.2 billion tonnes in 2022, with Asia-Pacific and North America as the dominant producing regions.

The premium pet food market, driven by humanization trends, is expanding at particularly high rates, with the American Pet Products Association (APPA) reporting U.S. pet food sales surpassing US$ 50 billion in 2023. Both sectors require high-throughput grain and protein milling, hammer milling, and micro-pulverization equipment. Machine manufacturers that develop feed-grade certified, sanitary-design milling systems can capture a fast-expanding, under-served equipment segment with recurring replacement demand.

Category-wise Insights

By Product Type Analysis

Wheat Flour Milling Machines are the dominant product type segment, commanding approximately 32% of the industrial food milling machine market. Wheat remains the world's most widely milled grain, the FAO reports global wheat production consistently exceeding 770 million tonnes annually, creating a vast, ongoing equipment demand base.

Large-scale commercial flour mills typically require continuous, high-capacity roller milling systems with precise sieving and purification stages, necessitating multi-machine turnkey plant installations. The bakery and food processing industries' dependence on refined wheat flour, which accounts for a significant share of caloric intake across North America, Europe, South Asia, and the Middle East, ensures structural, non-cyclical demand for wheat flour milling machinery throughout the forecast period.

By Technology Analysis

Mechanical milling is the leading technology segment, representing approximately 42% of the market. Its dominance reflects its mature, proven cost-effectiveness, versatility across a broad range of food commodities, grains, spices, pulses, and oilseeds, and its compatibility with both large-scale continuous processing and batch operations.

Mechanical milling encompasses roller mills, hammer mills, pin mills, and disc mills, all of which are foundational equipment in flour milling, rice processing, and spice manufacturing facilities worldwide. Established manufacturers such as Bühler Group and Satake Corporation maintain dominant positions in mechanical milling. While advanced technologies like cryogenic and ultrasonic milling are growing rapidly from smaller bases, mechanical milling's installed base, lower operational complexity, and broad applicability ensure its sustained leadership.

By Application Analysis

Grain milling is the dominant application segment, accounting for an estimated 35% of the total market. Grain, encompassing wheat, rice, corn, barley, and sorghum, forms the caloric foundation of human and animal diets globally. The U.S. Grains Council and FAO data consistently underscores that cereals provide over 50% of the world's dietary energy supply.

Industrial grain milling capacity is being expanded across Asia, Africa, and Latin America to reduce post-harvest losses and improve food security, driving sustained equipment procurement. Large-scale grain milling installations also have a well-defined replacement cycle every 15-25 years, providing a recurring revenue base for equipment suppliers beyond initial project sales.

By End-Use Analysis

The Food Processing Industry is the leading end-use segment, holding approximately 38% of market share. The food processing sector serves as the broadest demand aggregator, encompassing operations that transform raw agricultural inputs, grains, spices, herbs, oilseeds, into finished food products through milling, grinding, and size reduction processes.

The U.S. Bureau of Labor Statistics identifies food manufacturing as one of the largest U.S. manufacturing employers, while the European Commission notes the EU food and drink industry as the largest manufacturing sector by turnover. As global food processors scale capacity to meet population growth and shifting dietary patterns, investment in versatile, multi-commodity capable milling equipment with high uptime and sanitation compliance, critical under FSMA and EU food hygiene regulations, remains robust.

Regional Insights

North America Industrial Food Milling Machine Market Trends

The United States dominates North American demand for industrial food milling machines, underpinned by one of the world's largest and most technically advanced food processing industries. The U.S. Food and Drug Administration (FDA)'s Food Safety Modernization Act (FSMA) continues to drive capital investment in hygienic-design milling equipment that meets updated preventive controls and sanitation standards. North American flour milling capacity remains among the highest globally, with the North American Millers' Association (NAMA) reporting U.S. daily wheat flour milling capacity exceeding 1.4 million hundredweight.

Canada is a significant market for grain and oilseed milling equipment, driven by its position as a leading global wheat, canola, and pulse exporter. The innovation ecosystem in North America is robust, with companies integrating AI-based process optimization, real-time moisture sensing, and remote diagnostics into milling platforms. Growing investment in specialty food, plant-based protein, and functional ingredient manufacturing is creating incremental demand for micro-pulverization and cryogenic milling systems across the region.

Europe Industrial Food Milling Machine Market Trends

Europe is a mature, technically sophisticated market for industrial food milling equipment, driven by the region's large-scale flour milling, confectionery, and specialty food processing industries. Germany, home to global milling machine leaders including Brabender GmbH & Co. KG and Retsch GmbH, is both a leading producer and consumer of precision milling equipment. The European Commission's Farm to Fork Strategy, targeting a sustainable, resilient food system by 2030, is driving investment in energy-efficient and waste-minimizing milling technologies across EU member states.

The United Kingdom maintains strong demand from its bakery, ready meals, and functional food sectors, while France and Spain are significant markets for spice, cereal, and confectionery milling. European food machinery standards, governed by EU Machinery Directive 2006/42/EC and Regulation (EC) No 1935/2004 on food contact materials, impose rigorous design and compliance requirements. Regulatory harmonization across the EU27 creates a favorable environment for standardized, pan-European equipment procurement and benefits manufacturers offering certified, CE-marked milling solutions.

Asia Pacific Industrial Food Milling Machine Market Trends

Asia Pacific is the fastest-growing regional market for industrial food milling machines, fueled by massive food production scale, expanding middle-class consumption, and significant public investment in agricultural modernization. China is the world's largest wheat and rice producer, the National Bureau of Statistics of China reports annual grain output exceeding 650 million tonnes, generating enormous domestic demand for industrial milling capacity. Satake Corporation of Japan is a globally recognized leader in rice milling technology, with a strong installed base across Asia.

India's food processing sector is expanding rapidly under the government's Production Linked Incentive (PLI) Scheme for Food Processing, which has attracted substantial investment in modern milling and processing facilities. The Ministry of Food Processing Industries (MoFPI) targets increasing the level of food processing from approximately 10% to 25% of agricultural output by 2025. ASEAN nations, particularly Vietnam, Indonesia, and Thailand, are experiencing rapid expansion in rice and spice milling capacity, benefiting from both domestic consumption growth and export-driven investment.

Competitive Landscape

The Industrial Food Milling Machine Market exhibits a moderately consolidated structure, with a small number of global technology leaders, notably Bühler Group, Hosokawa Micron Group, and Satake Corporation, commanding significant revenue share, alongside a broader tier of regional and application-specialist manufacturers.

Market leaders differentiate through proprietary milling technologies, global service networks, and turnkey plant engineering capabilities. Key strategies include R&D investment in energy-efficient and digitally integrated milling systems, geographic expansion in Asia and Africa, and strategic partnerships with food processing conglomerates. Emerging business model trends include equipment-as-a-service (EaaS) and outcome-based milling contracts, where OEMs guarantee throughput and quality metrics, a shift that is reshaping competitive dynamics in developed markets.

Key Market Developments

- February, 2025: Bühler Group unveiled its next-generation Arrius integrated milling system, featuring AI-driven process optimization and a claimed energy reduction of up to 15% versus conventional roller mill setups, targeting large-scale industrial flour millers globally.

- October, 2024: Hosokawa Micron Group expanded its Alpine product range with a new ultra-fine cryogenic pin mill series designed for heat-sensitive botanical and nutraceutical ingredient processing, targeting the rapidly growing plant-based and herbal supplement manufacturing sector.

- March, 2023: Satake Corporation announced an investment in upgrading its smart rice milling line with integrated IoT quality monitoring, aimed at reducing broken rice ratios and improving milling yield efficiency for large-scale commercial rice mills across Asia Pacific.

Industrial Food Milling Machine Market Report -Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 136.0 Mn |

| Current Market Value (2026) | US$ 160.5 Mn |

| Projected Market Value (2033) | US$ 215.5 Mn |

| CAGR (2026-2033) | 4.3% |

| Leading Region | North America, 39% share |

| Dominant Product Type | Wheat Flour Milling Machines, 32% share |

| Top-ranking End Use | Food Processing Industry, 38% |

| Incremental Opportunity | US$ 55.0 Mn |

Companies Covered in Industrial Food Milling Machine Market

- Bühler Group

- Hosokawa Micron Group

- Satake Corporation

- Alapala Machine Industry & Trade Inc.

- Brabender GmbH & Co. KG

- IKA Werke GmbH & Co. KG

- The Fitzpatrick Company

- Prater Industries

- Kemutec Group Inc.

- Kaps Engineers

- L.B. Bohle Maschinen + Verfahren GmbH

- Modern Process Equipment Corporation

- Retsch GmbH

- NETZSCH Group

- Omas Srl

- CPM Holdings Inc.

- Sprout-Matador A/S

- Van Aarsen International

Frequently Asked Questions

The global Industrial Food Milling Machine Market is estimated at US$ 160.5 Million in 2026 and is forecast to reach US$ 215.5 Million by 2033, at a CAGR of 4.3%. Historically, the market grew at a CAGR of 2.8% from 2020 to 2025, reflecting steady underlying growth in global food processing capacity.

The primary drivers include growing global food demand, with the FAO projecting a 50% increase in global food requirements by 2050, automation of food processing facilities aligned with Industry 4.0, and tightening food safety regulations under FSMA and EFSA frameworks that compel investment in precision, hygienic-design milling systems.

Wheat Flour Milling Machines lead the product type segment with approximately 32% share, driven by global wheat production exceeding 770 million tonnes annually and the critical role of flour milling in serving the bakery, pasta, and processed food industries worldwide. This segment benefits from both new capacity installations and well-defined equipment replacement cycles.

North America is the leading regional market, anchored by the United States' advanced food processing infrastructure, FSMA-driven equipment modernization, and high adoption of automated milling solutions. The North American Millers' Association (NAMA) reports that U.S. flour milling capacity remains among the world's highest, providing a strong, recurring equipment replacement and upgrade demand base.

The highest-potential growth opportunities lie in cryogenic and ultrasonic milling for nutraceutical and herbal ingredient processing, where the Global Wellness Institute's US$ 5.6 trillion wellness economy drives demand for precision bioactive-preserving milling, and in the animal feed and pet food sector, with global compound feed production exceeding 1.2 billion tonnes, requiring high-throughput, feed-grade certified milling equipment.

Leading companies include Bühler Group, Hosokawa Micron Group, Satake Corporation, Alapala Machine Industry & Trade Inc., Brabender GmbH & Co. KG, NETZSCH Group, The Fitzpatrick Company, Retsch GmbH, and Prater Industries, among others. These firms compete on technological innovation, global service reach, turnkey plant capabilities, and energy-efficiency credentials.