- Specialty & Fine Chemicals

- India Carbon Black Market

India Carbon Black Market Size, Share, and Growth Forecast, 2026 - 2033

India Carbon Black Market by Product Type (Furnace Black, Thermal Black, Acetylene Black, Channel Black, Misc.), Grade (Standard Grade, Speciality Grade), Application (Tires, Non-Tire Rubber Products, Plastics, Inks & Coatings, Electrical & Electronics), and Regional Analysis for 2026 - 2033

India Carbon Black Market Size and Trends Analysis

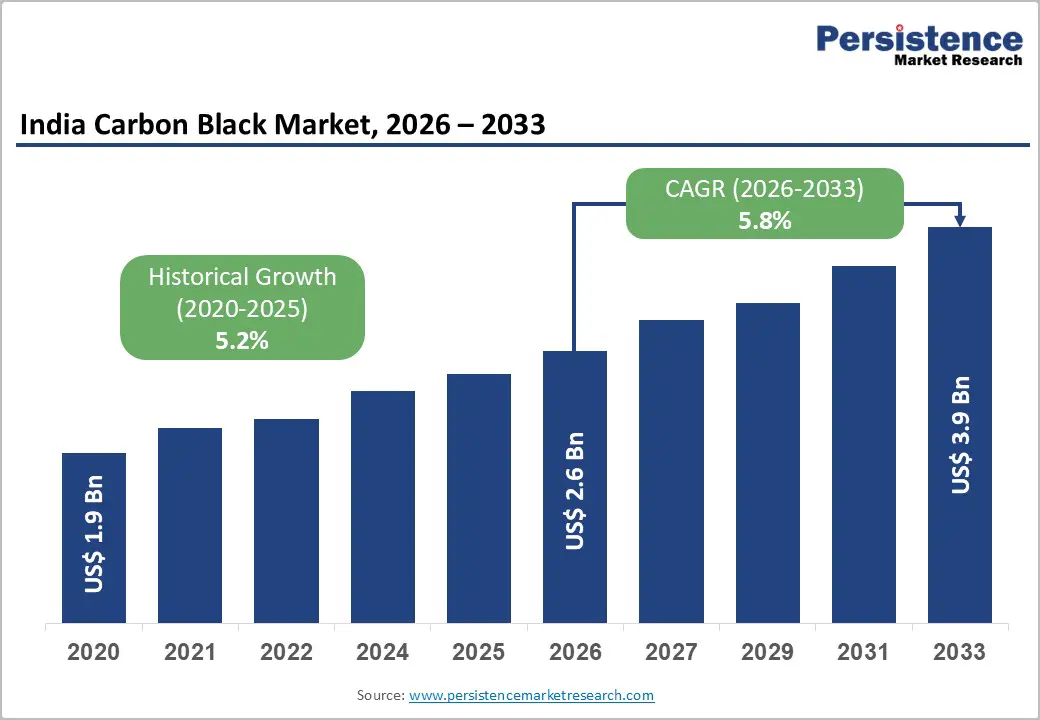

India Carbon Black Market size is likely to be valued at US$2.6 billion in 2026 and is projected to reach US$3.9 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. The market recorded a valuation of US$1.9 billion in 2020, advancing to US$2.6 billion in 2026 at a historical CAGR of 5.2%, underscoring consistent demand momentum across India's industrial base.

Primary growth factors include accelerated automotive and tyre manufacturing activity, strong momentum in the plastics sector, and advancing speciality carbon black applications across coatings, inks, and electrical industries. India's domestic tyre industry revenues increased by approximately 6.4% year-on-year during the first half of FY2026, directly reinforcing downstream feedstock demand.

India's plastics market, estimated at approximately US$26.61 billion in 2025 and projected to reach US$44.59 Billion by 2030, represents a significant and expanding pull for carbon black consumption across pigment, UV stabilisation, and conductive compounding applications.

Key Industry-Highlights:

- Leading Application Segment: Tires dominate the market with approximately 55% share, driven by carbon black’s critical role in tread, sidewall, and carcass compounding across OEM and replacement tyres.

- Fastest-Growing Application Segment: Non-tire rubber products are the fastest-growing segment, supported by automotive components, belts, hoses, footwear, medical goods, and infrastructure-related rubber applications.

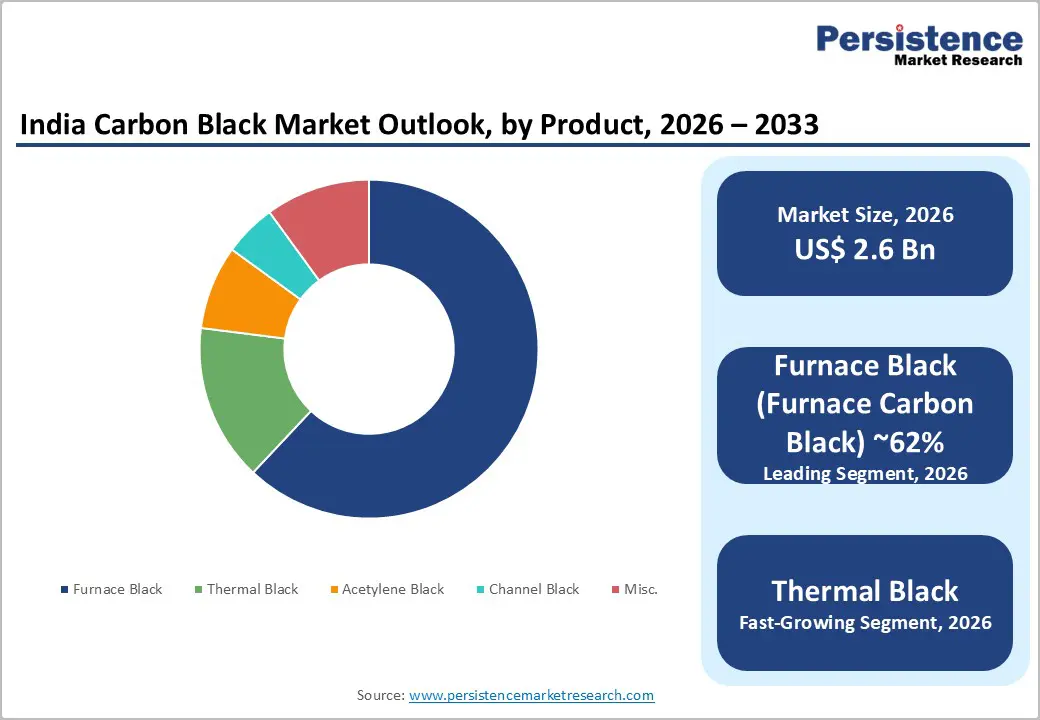

- Leading Product Type: Furnace Black leads with 62% share, favoured for scalable production, cost efficiency, and compatibility with tyres, rubber, and plastics.

- Fastest-Growing Product Type: Thermal Black is the fastest-growing segment, gaining traction in speciality elastomers, wire and cable insulation, and high-performance engineering applications due to high purity and controlled conductivity.

- Growth Opportunity: Circular and sustainable carbon blacks, including Birla Carbon’s Continua™ SCM and Cabot’s pyrolysis-based products, offer environmentally aligned solutions for tyres, plastics, inks, and coatings.

- Capacity Expansion Trend: Domestic production is scaling rapidly, with Himadri, Epsilon Carbon, and Birla Carbon adding new speciality lines and integrated complexes to meet rising demand and reduce import dependency.

| Key Insights | Details |

|---|---|

|

India Carbon Black Market Size (2026E) |

US$ 2.6 Bn |

|

Market Value Forecast (2033F) |

US$ 3.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Dynamics

Drivers - India's Tyre Manufacturing Sector as the Primary Demand Anchor for the India Carbon Black Market

The tyre industry is the most critical demand channel for the India Carbon Black Market, as carbon black serves as an essential reinforcing agent in tyre compounding across tread, sidewall, and carcass constructions. India's domestic tyre sector has demonstrated resilience and structural strength, with tyre industry revenues recording approximately 6.4% year-on-year growth during the first half of FY2026. Domestic tyre demand is projected to advance by 6 to 8% in FY2026, supported by an anticipated recovery in replacement demand in the second half of the fiscal year, particularly following expected reductions in GST rates that could stimulate retail tyre purchases.

Major tyre manufacturers are collectively expected to invest INR 20,000 to 25,000 crore over the next three years in capacity additions and technology upgrades. Over the longer term, India's total tyre industry revenue is projected to reach approximately INR 13,00,000 crore by 2047, reflecting a nearly 12-fold expansion from current levels. These structural demand signals reinforce the long-term consumption outlook for carbon black across both OEM and replacement tyre categories within the India Carbon Black Market.

Rapid Expansion of India's Plastics Sector Fuelling Carbon Black Consumption

India's plastics sector constitutes a key downstream market for the India Carbon Black Market, particularly for applications in plastic compounding, masterbatches, speciality films, and conductive polymer systems. The Indian plastics industry, estimated at approximately US$26.61 billion in 2025, is expected to reach around US$44.59 Billion by 2030, driven by strong demand across packaging, automotive, infrastructure, agriculture, and healthcare end-uses. India's plastic exports reached US$5.8 billion in FY25, recording an 11.54% increase compared to FY24, while the cumulative export value for FY26 increased by 6.61% year-on-year.

The government has approved the establishment of 10 Plastic Parks across states, including Madhya Pradesh, Assam, Tamil Nadu, Odisha, and Jharkhand, to support integrated plastic manufacturing infrastructure. With more than 30,000 plastic processing units operational across India, the plastics value chain provides a broad and diversified base of demand for carbon black used as a pigment, UV stabiliser, and conductivity enhancer. These dynamics position the India Carbon Black Market to benefit directly from plastics sector capacity additions and export-led production acceleration.

Policy Support and Industrial Development of India's Rubber Ecosystem

India's rubber manufacturing sector, encompassing approximately 5,000 rubber manufacturing units and supporting exports worth around INR 37,500 crore, serves as a structurally important demand channel for the India Carbon Black Market beyond tyre applications alone. India currently ranks as the second-largest consumer of natural rubber and the fourth-largest consumer of gross elastomers globally, reflecting the depth of the industrial rubber ecosystem. The National Rubber Policy 2019 outlines a vision for a globally competitive and environmentally sustainable rubber value chain, emphasizing quality standardisation, innovation, and export competitiveness.

Government measures such as revised import duties on compounded rubber, introduced in the Union Budget 2023, support domestic rubber production by providing price stability to farmers and raw material security to manufacturers. The Reserve Bank of India's Industrial Outlook Survey of the Manufacturing Sector confirms continued positive business sentiment, with improving expectations for production levels, order books, and capacity utilisation. These policy and demand signals collectively sustain the carbon black consumption trajectory across non-tyre rubber applications within the India Carbon Black Market.

Restraint - Raw Material Price Volatility and Feedstock Dependency

Carbon black production is heavily dependent on feedstocks such as coal tar oil, anthracene oil, and petrochemical derivatives, whose prices are closely linked to crude oil and coal market fluctuations. Global economic uncertainties, including persistent inflation and rising interest rates observed in the post-COVID period, have contributed to price instability across petrochemical supply chains.

For Indian carbon black producers, this translates into compressed profit margins and production planning challenges, particularly for smaller manufacturers that lack hedging capabilities or long-term supply contracts. Feedstock cost volatility directly undermines cost predictability and poses a structural pricing risk that limits near-term investment visibility within the market.

Environmental Regulations and Emission Compliance Pressure

Carbon black manufacturing is associated with significant emissions, including SOx, NOx, and CO2, making the industry subject to tightening environmental regulations at both the central and state levels in India. Compliance with evolving emission standards requires capital investment in pollution control equipment, waste management systems, and cleaner production technologies.

Smaller manufacturers with limited financial resources face disproportionate compliance burdens, and failure to meet regulatory standards risks production disruptions or operational penalties. As India advances its commitment to net-zero carbon emissions by 2070, the regulatory environment for carbon-intensive industries is expected to become progressively more demanding, raising the structural cost of compliance for all market participants.

Opportunities - Circular Carbon Black and Sustainable Carbonaceous Material Commercialisation

The global and domestic shift toward circular economy principles is creating a significant opportunity within the India Carbon Black Market, particularly through the development and commercialisation of sustainable carbonaceous materials derived from recovered end-of-life tyres. This opportunity is directly actionable for Indian manufacturers seeking to differentiate their product portfolios and align with tightening sustainability mandates from global automotive and tyre OEMs.

Birla Carbon has taken a leading role in this transition through its Continua™ Sustainable Carbonaceous Material range, including Continua™ 8000 and Continua™ 8030, produced from recovered end-of-life tyres and offering circular alternatives to conventional carbon black. Following a European launch, Birla Carbon expanded Continua™ production to India through a joint venture with Finster Black, targeting Asian markets with a stated goal of repurposing 300,000 tonnes of tyres annually by 2030 and a corporate commitment to Net Zero by 2050.

Cabot Corporation similarly achieved full-scale manufacturing of circular reinforcing carbon across the Asia Pacific in February 2026, using tyre pyrolysis oil and the ISCC PLUS mass balance approach as drop-in replacements for conventional carbon black. These developments confirm that circular carbon black is transitioning from pilot scale to commercial viability, offering the Indian Carbon Black Market a credible pathway toward sustainable production aligned with both regulatory and customer-driven decarbonization goals.

Speciality Carbon Black Demand in Coatings, Inks, and Advanced Material Applications

The speciality carbon black segment presents a distinct and commercially significant opportunity in the India Carbon Black Market, driven by the needs of high-performance coatings, printing inks, electrical conductive applications, and advanced polymer systems. As India's plastics and chemicals industries scale up and domestic manufacturing sophistication deepens, demand for precisely engineered carbon black grades with controlled particle size, structure, and surface chemistry is accelerating across both domestic and export-oriented production facilities.

Birla Carbon's participation in PaintIndia 2026 in February 2026 demonstrated the commercial depth of this opportunity, showcasing Raven™ carbon black grades, including Raven™ 5000 Ultra™, Raven™ 5100 Ultra™, and Raven™ 3500, engineered for superior jetness and performance across waterborne, solvent-based, and powder coatings. The company also presented Nanocyl™ multi-walled carbon nanotubes and Conductex™ conductive blacks, reflecting the convergence of nanotechnology and carbon black chemistry for advanced applications, including food-contact-compliant formulations.

India's plastics export strategy targeting more than 200 countries worldwide, combined with duty-free access arrangements under select trade agreements, creates strong tailwinds for speciality carbon black suppliers capable of supporting high-performance formulations required by global brand manufacturers.

Domestic Capacity Expansion and Backwards Integration Toward Self-Reliance

Strategic capacity additions by Indian producers represent a material opportunity to deepen domestic self-sufficiency in carbon black supply, reduce import dependency, and strengthen competitive positioning within the Indian Carbon Black Market. This opportunity is particularly significant given India's industrial policy objective of Atmanirbhar Bharat and the alignment of large-scale manufacturing investments with national self-reliance goals.

Himadri Speciality Chemical initiated trial production at its Mahistikry plant in January 2026, introducing a new speciality carbon black line with an estimated capacity of 70,000 MTPA through brownfield expansion. Epsilon Carbon commissioned India's first integrated carbon black complex in Bellary, Karnataka, with a capacity of 115,000 TPA, utilising backward integration with anthracene oil and low-sulphur feedstock with waste coke oven gas, targeting a total capacity of 300,000 TPA in subsequent phases.

Birla Carbon's announcement of two new manufacturing sites in Naidupet, Andhra Pradesh and Rayong, Thailand, in February 2024, adding over 240,000 tonnes per year, further illustrates the scale of capacity investment directed at meeting demand across India and Southeast Asia and reinforces the India Carbon Black Market's trajectory toward domestic production leadership.

Category-wise Analysis

Product Type Insights

Furnace Black, also referred to as Furnace Carbon Black, commands approximately 62% of the total market share in 2026, establishing its position as the dominant product type within the India Carbon Black Market. Its leadership stems from a highly scalable and controllable manufacturing process that allows producers to tailor particle size, structure, and surface chemistry to meet diverse industrial specifications across tyre, rubber, and plastic applications. Furnace Black's cost efficiency and production consistency make it the preferred grade for the majority of industrial end-uses in India.

India's major carbon black producers have concentrated their largest capacity investments in furnace black technology. Epsilon Carbon's integrated Bellary facility, for instance, specifically produces Tread and Carcass ASTM carbon blacks aligned with furnace-grade demand in tyre and non-tyre rubber applications. Birla Carbon's capacity additions in Naidupet, Andhra Pradesh, adding over 240,000 tonnes per year, further reinforce domestic furnace black supply capability. The availability of integrated feedstock supply chains and the alignment of furnace black specifications with India's dominant industrial rubber and tyre segments are expected to sustain its market leadership position through the 2026 to 2033 forecast period.

Thermal Black, or Thermal Carbon Black, is the fastest-growing product segment within the Indian Carbon Black Market, driven by its distinctive large particle size and low structure characteristics suited to applications requiring high purity, controlled electrical conductivity, and compatibility with speciality elastomers. Demand for thermal black is gaining momentum across speciality rubber compounding, wire and cable insulation, and high-performance engineering applications as India's industrial manufacturing base becomes more technically sophisticated.

Application Insights

The Tires segment leads the India Carbon Black Market with approximately 55% of total market share in 2026, reflecting carbon black's indispensable role as a reinforcing and performance-enhancing agent in tyre compounding. India's tyre sector is backed by strong structural fundamentals, with a sample set of major manufacturers projected to achieve revenue growth of approximately 8 to 10% in FY2026, supported by stable domestic demand, improving product mix, and selective price realisation gains.

The tyre segment's demand for carbon black spans multiple grades and specifications, from high-abrasion furnace blacks used in tread compounds to softer grades applied in sidewalls and inner liner components. India's longer-term tyre industry trajectory, targeting approximately INR 13,00,000 crore in total industry revenue by 2047, provides a structural foundation for sustained carbon black consumption in this application segment across both replacement and OEM tyre categories. The industry's stated commitment to premiumisation and speciality tyre product development further supports demand for higher-performance carbon black grades with precise reinforcing properties.

The Non-Tire Rubber Products segment is the fastest-growing application category within the India Carbon Black Market, supported by broad-based industrial demand across automotive sealing components, belts, hoses, vibration dampers, footwear, medical rubber goods, and infrastructure-related rubber applications. India's rubber industry, with approximately 5,000 manufacturing units and rubber product exports worth around INR 37,500 crore, represents a strong and diversified demand base for carbon black in non-tyre end-uses.

Competitive Landscape

The India Carbon Black Market is largely consolidated, with a handful of major players controlling a significant share of production and supply across the country. Leading companies such as Birla Carbon, Himadri Speciality Chemical, Epsilon Carbon, Cabot Corporation, and Phillips Carbon Black Limited dominate the market, leveraging advanced manufacturing technologies, strong distribution networks, and strategic expansions to meet growing demand from the tyre, rubber, plastics, and speciality applications sectors.

These key players continuously invest in capacity expansions and sustainable innovations to strengthen their market position. For instance, Birla Carbon is expanding production in India and Thailand while advancing circular carbon black solutions, whereas Himadri Speciality Chemical has increased speciality carbon black production through its Mahistikry plant expansion. Epsilon Carbon has commissioned India’s first integrated carbon black complex in Karnataka, focusing on high-quality ASTM grades for tyres and plastics.

Global players such as Cabot Corporation are also entering the Indian market, offering circular and sustainable carbon black products, enhancing competitive intensity while promoting environmentally conscious solutions. Smaller domestic manufacturers and niche speciality producers contribute to a fragmented segment within the broader consolidated market, catering to regional and customised requirements.

Key Industry Developments

- On January 16, 2026, Himadri launched trial production at its Mahistikry plant, introducing a new speciality carbon black line with 70,000 MTPA capacity. This expansion targets high-performance speciality applications, enhancing India’s domestic production and reducing dependence on imports.

- December 17, 2025, Birla Carbon advanced sustainability in the carbon black market by scaling its Continua™ Sustainable Carbonaceous Material (SCM) solutions, derived from recovered end-of-life tyres. The company’s Continua™ 8000 and Continua™ 8030 products offer circular alternatives to traditional carbon black, balancing performance and environmental benefits. Following its European launch, Birla Carbon expanded production to India through a joint venture with Finster Black, targeting Asian markets. With a goal to repurpose 300,000 tonnes of tyres annually by 2030, Birla Carbon reinforces its commitment to decarbonisation, Net Zero by 2050, and long-term integration of circular carbon black across tyres, plastics, inks, and coatings applications.

- On February 13, 2024, Birla Carbon established two new state-of-the-art manufacturing sites in Naidupet, Andhra Pradesh (India), and Rayong (Thailand), adding over 240,000 tonnes/year, with plans to double production. This expansion strengthens supply in India and Southeast Asia, supporting growing demand in tyre, rubber, and specialty applications.

Companies Covered in India Carbon Black Market

- PCBL Limited

- Birla Carbon (Aditya Birla Group)

- Himadri Speciality Chemical Ltd

- Epsilon Carbon Pvt Ltd

- Continental Carbon India Ltd (Continental Carbon Asia)

- BKT Carbon

- Cabot Corporation (Cabot India Ltd)

- Jiangxi Black Cat Carbon Black Co. Ltd

- OCI Company Ltd

- Orion Engineered Carbons S.A.

- Tokai Carbon Co. Ltd.

Frequently Asked Questions

The India Carbon Black Market is projected to be valued at US$ 2.6 Bn in 2026.

The Furnace Black (Furnace Carbon Black) segment is expected to account for approximately 62% of the India Carbon Black Market by Product Type in 2026.

The market is expected to witness a CAGR of 5.8% from 2026 to 2033.

The India Carbon Black Market growth is primarily driven by robust demand from the tyre and rubber sectors, rapid expansion of the plastics industry, and supportive government policies fostering industrial development and capacity additions.

Key market opportunities in the India Carbon Black Market lie in circular and sustainable carbon blacks, growing demand for speciality grades in coatings, inks, and advanced materials, and domestic capacity expansion toward self-reliance and reduced import dependency.

Key players in the Carbon Black Market include Birla Carbon, Himadri Speciality Chemical, Epsilon Carbon, Cabot Corporation, and Phillips Carbon Black Limited.