- Marine

- Global Inboard Engines Market

Global Inboard Engines Market Size, Share, and Growth Forecast 2026–2033

Inboard Engines Market by Engine Type (Diesel Inboard Engines, Gasoline Inboard Engines, Electric Inboard Engines, Hybrid Inboard Engines), Power Output (Below 100 HP, 100–300 HP, 300–500 HP, Above 500 HP), Application (Recreational Boats, Commercial Boats, Military & Defense Boats), and Regional Analysis, 2026–2033

Global Inboard Engines Market Size and Trend Analysis

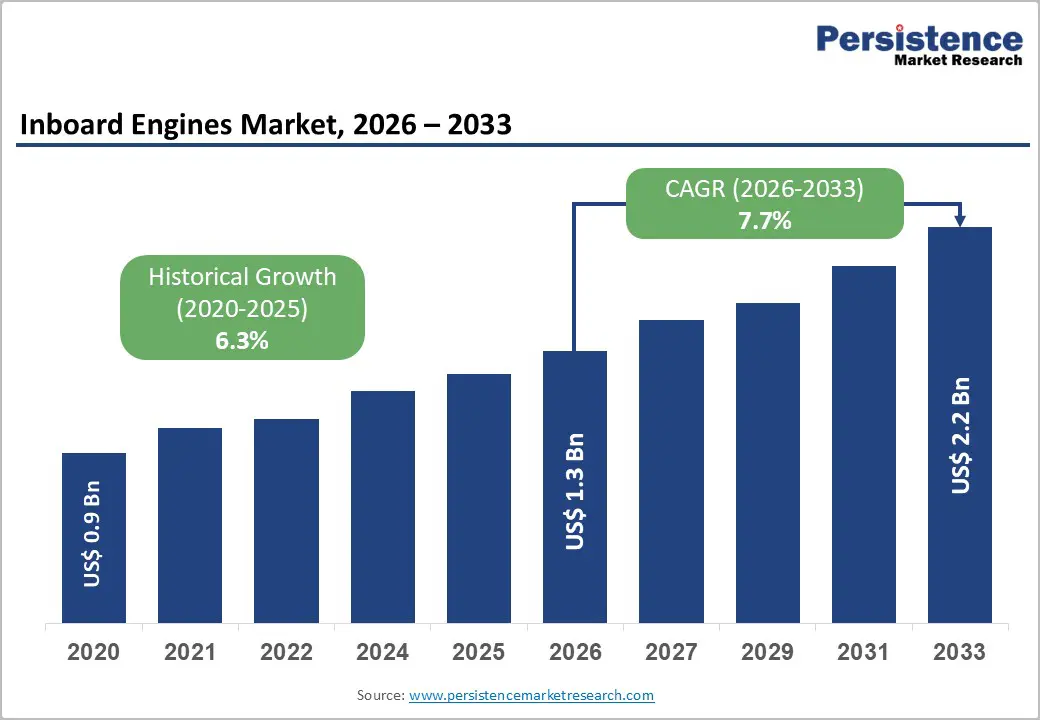

The global inboard engines market is expected to be valued at US$ 1.30 Billion in 2026 and is projected to reach US$ 2.19 Billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033. Growth is being driven by stricter marine emission regulations, particularly the IMO 2023 GHG Strategy, which is encouraging vessel operators to adopt cleaner and more efficient propulsion systems.

Key Market Highlights

- Leading Region: North America holds the largest market share at 37.0%, valued at US$ 0.48 Billion in 2026. A large recreational boating fleet and ongoing engine replacement driven by EPA Tier 4 emission standards continue to support regional dominance.

- Fastest Growing Region: Asia Pacific is expected to expand at a 9.5% CAGR, the fastest globally. Government initiatives such as China's inland waterway development plans and India's Sagarmala Programme are boosting demand for modern inboard engines across commercial vessel fleets.

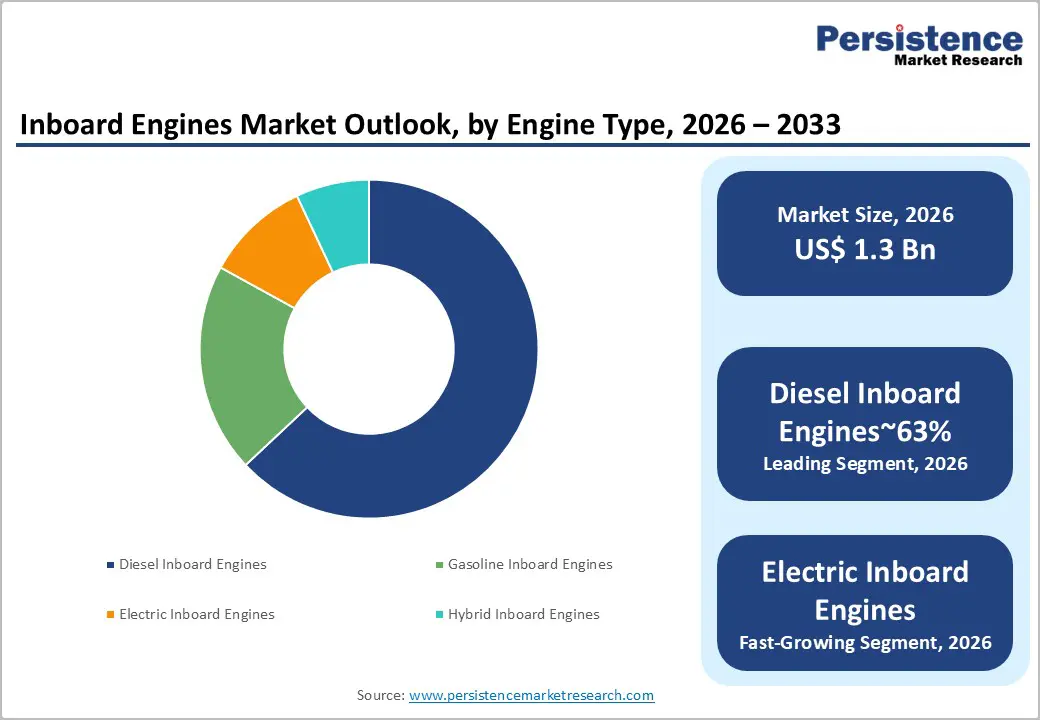

- Leading Segment: Diesel inboard engines account for 63.0% of the market in 2026. Their high torque output, fuel efficiency, and suitability for commercial and long-range marine operations make them the preferred choice for vessel operators.

- Fastest Growing Segment: Electric inboard engines are expected to witness the highest growth during the forecast period. Increasing emission restrictions in waterways and significantly lower operating costs are accelerating adoption in both recreational and commercial applications.

- Key Opportunity: The commercial boats segment offers the strongest growth opportunity through 2033. Rising adoption of hybrid propulsion systems and increasing fleet modernization programs are creating significant opportunities for engine manufacturers with certified marine solutions and strong service networks.

Market Dynamics

Market Growth Drivers

Accelerating Regulatory-Driven Fleet Modernisation Across Commercial Marine Sectors

Fleet operators that delay engine replacement now face direct financial exposure through port surcharges and restricted access to emission-controlled waterways, making inboard engine upgrades a compliance obligation, not a discretionary capital decision. The EU's FuelEU Maritime Regulation, which entered into force in 2023 and imposes progressively tightening greenhouse gas intensity limits from 2025 onward, is already prompting European inland shipping operators to replace aging diesel powertrains

Wärtsilä Corporation responded in 2023 by expanding its low-emission marine engine portfolio specifically targeting inland waterway vessels under 500 gross tonnes. Over the next two to three years, compliance timelines will compress procurement windows, creating a concentrated replacement demand surge that directly benefits OEM marine engine suppliers with certified low-emission inboard configurations.

Sustained Recreational Boating Participation Rates Driving OEM and Aftermarket Demand

Recreational boating's post-2020 participation surge has permanently enlarged the addressable owner base, generating parallel demand streams for new inboard powertrains and aftermarket services as existing vessels age into replacement cycles. The Recreational Boating & Fishing Foundation (RBFF) reported that U.S. recreational boating participation reached approximately 100 million participants in 2022, a figure that solidified the sport's mainstream consumer status and elevated marina capacity utilisation to levels requiring fleet expansion at charter and rental operators.

As these vessels, typically equipped with gasoline or diesel inboard engines in the 100–300 HP range, approach their standard 10-to-15-year powertrain service life between 2028 and 2032, OEM suppliers and marine powertrain aftermarket distributors will face a measurable volume step-up in repower demand.

Market Restraints

High Capital Cost and Long Payback Periods for Hybrid and Electric Marine Propulsion Systems

The cost premium associated with marine-certified hybrid propulsion systems compresses adoption rates among price-sensitive owner segments, particularly small commercial operators and entry-level recreational buyers who cannot amortise the upfront differential across sufficient annual operating hours.

DNV, the international classification society, estimates that hybrid marine propulsion systems carry an installed cost premium of 30% over equivalent-output conventional diesel inboard engines when accounting for battery storage, power management systems, and certified installation, creating a payback horizon that frequently exceeds seven to ten years at typical leisure vessel utilisation rates. For new entrants targeting the hybrid and electric inboard segment, this cost barrier necessitates either a financing-integrated go-to-market strategy or a focus on commercial operator segments where daily utilisation justifies the economics.

Supply Chain Concentration and Critical Component Lead Times

The global inboard engines market faces structural margin pressure from concentrated supply chains for precision marine engine components, particularly fuel injection systems, turbocharger assemblies, and marine-grade electronic control units, where single-source supplier dependency creates lead time volatility that inflates working capital requirements for both OEMs and dealers.

The U.S. International Trade Commission documented that Section 232 tariffs and Section 301 tariffs on imported steel and aluminium, materials central to engine block and manifold manufacturing, increased raw material input costs for domestic marine engine assemblers by an estimated 12 to 18% between 2022 and 2024, with larger OEMs better positioned to absorb these costs through vertical integration than smaller specialist manufacturers.

Market Opportunities

Electric Inboard Engine Commercialisation for Premium Recreational Yacht Segments

Marine propulsion technology investors and established OEMs should target the premium sailing and motor yacht segment, specifically vessels between 30 and 60 feet, where owner demographics support high willingness-to-pay for zero-emission auxiliary and primary drive systems.

Torqeedo, acquired by Deutz AG in 2017 and consistently expanding its marine electric portfolio through 2024, launched its Deep Blue Hybrid system targeting sailing yachts with diesel-electric configurations that reduce harbour emissions to zero, validating commercial demand at price points above US$ 20,000 per installation. For this opportunity to fully materialise, marine-grade battery energy density must reach approximately 300 Wh/kg at commercially viable cost, a threshold that solid-state marine battery development programmes at companies including Samsung SDI are targeting for the 2026–2028 window.

Commercial Inland Waterway Vessel Repowering Across Emerging Asian Markets

Inland waterway logistics operators across Southeast Asia and South Asia represent a structurally underpenetrated buyer cohort for modern high-efficiency diesel and hybrid inboard engines, as governments invest in waterway infrastructure to relieve road congestion.

India's National Waterways Act 2016, which designated 111 national waterways and has driven cumulative investment exceeding US$ 1.5 Billion in waterway infrastructure through the Jal Marg Vikas Project by 2024, is creating a commercially viable fleet of cargo vessels that require certified, service-supported inboard powertrains. Mid-tier OEMs with established distribution networks in India, Bangladesh, and Vietnam, and the technical capacity to offer IMO-compliant engine configurations at competitive total cost of ownership, are best positioned to capture this structurally growing repowering pipeline.

Category-wise Insights

Engine Type Analysis

Diesel inboard engines account for 63.0% of the global inboard engines market in 2026, equivalent to US$ 0.82 Billion, driven by their strong fuel efficiency and ability to deliver continuous high torque for long operating hours. Commercial fishing vessels and long-range cruising yachts prefer diesel engines because diesel fuel offers higher energy density, helping vessels travel longer distances while reducing fuel storage requirements. According to Ship & Boat International, diesel inboard engines remain the preferred choice for displacement-hull vessels, where steady torque and operational reliability are more important than high peak power.

Electric inboard engines are emerging as the fastest-growing segment, supported by rising zero-emission regulations across European waterways and marinas. Cities such as Amsterdam are restricting combustion-engine vessels in canal networks, encouraging operators to adopt electric propulsion systems. Swedish boat manufacturer Candela demonstrated in 2024 that its electric hydrofoil vessel significantly lowers energy costs compared to diesel alternatives, strengthening interest in electric ferries and water taxis. Growing availability of marine lithium iron phosphate batteries is expected to further expand electric inboard adoption through 2027–2030.

Power Output Analysis

The 100–300 HP power output segment accounts for 42.0% of the global inboard engines market in 2026, equivalent to US$ 0.55 Billion, due to its suitability across a wide range of marine applications. Mid-size cruising boats, cabin cruisers, harbour patrol vessels, and passenger ferries commonly operate within this range because it provides balanced speed, efficiency, and maintenance convenience. Charter tourism operators particularly favour 150–250 HP engines for dependable planing performance. Mercury Marine has also identified the 200–300 HP class as one of its highest-volume inboard engine categories in North America.

Within this category, the 150–250 HP sub-segment is growing the fastest, supported by rising adoption of hybrid diesel-electric propulsion systems. These engines offer the performance needed for recreational and coastal vessels while helping operators comply with tightening marina emission standards in Europe and North America. Volvo Penta’s hybrid-compatible IPS platform in the 230–270 HP range is increasingly being selected by Nordic and Baltic boat manufacturers. As more coastal cities introduce emission-control policies, hybrid inboard systems in this power range are expected to become a preferred option for new vessel production.

Application Analysis

Recreational boats account for 67.0% of the global inboard engines market in 2026, equivalent to US$ 0.87 Billion, supported by strong boating participation across North America and Western Europe. Performance-focused recreational vessels, especially wakeboarding and water-skiing boats, rely heavily on direct-drive inboard engines to generate the precise wake conditions required for watersports activities. Manufacturers such as MasterCraft Boat Holdings and Malibu Boats continue to design their vessels around inboard propulsion systems. In addition, installation standards set by the American Boat and Yacht Council help strengthen the position of established engine suppliers in this segment.

Commercial boats represent the fastest-growing application segment for inboard engines, driven by increasing electrification initiatives across urban ferry and water taxi networks. European and Asian port authorities are implementing stricter emission regulations, encouraging fleet operators to shift toward hybrid and electric propulsion systems. In 2024, STENA Line accelerated its hybrid ferry conversion programme across the Irish Sea and Baltic Sea routes, highlighting the industry’s move toward large-scale adoption of cleaner marine technologies. Expanding emission-control policies are expected to create strong long-term demand for advanced commercial inboard propulsion systems.

Regional Insights

North America Inboard Engines Market Trends and Insights

North America accounts for 37.0% of the global inboard engines market in 2026, representing US$ 0.48 Billion, sustained by the continent's structurally deep recreational boating culture and an active fleet of approximately 12 million registered recreational boats per U.S. Coast Guard data. The U.S. Environmental Protection Agency's (EPA) Tier 4 marine engine emission standards, which require progressively lower particulate and NOx outputs from inboard diesel engines, are compelling marina operators and vessel owners to retire pre-Tier 4 powertrains ahead of regional Clean Air Act compliance deadlines. North America's combination of a mature but actively repowering fleet and a nascent electric inboard adoption curve positions the region to maintain its market leadership through the forecast period.

- United States Inboard Engines Market Size

The United States represents an estimated 85% of the North American regional inboard engines market, approximately US$ 0.41 Billion in 2026, underpinned by Florida, California, and the Great Lakes states commanding the highest registered boat densities in the country. Indmar Marine Engines, a Tennessee-based OEM, has deepened its OEM supply relationships with tow-sport boat manufacturers including Nautique Boat Company through 2024, reinforcing domestic inboard engine supply chain integration. As the U.S. marina network expands electric charging infrastructure under funding provisions of the Infrastructure Investment and Jobs Act 2021, electric inboard repower demand will begin contributing measurable volume growth from 2027 onward.

Europe Inboard Engines Market Trends and Insights

Europe accounts for 26.0% of the global inboard engines market in 2026, representing US$ 0.34 Billion, shaped by the continent's dual imperatives of decarbonising leisure and commercial maritime activity while sustaining a sophisticated yacht-building and inland waterway cargo sector. The European Green Deal and its maritime-specific Fit for 55 legislative package are accelerating OEM investment in certified low-emission inboard configurations, with the Rhine-Main-Danube inland waterway corridor serving as a live testbed for alternative-fuel vessel regulations under the CCNR (Central Commission for Navigation on the Rhine) 2023 Emission Standards. Europe's regulatory environment creates a durable structural demand signal for next-generation marine powertrains through the entire 2026–2033 forecast window.

- Germany Inboard Engines Market Size

Germany represents an estimated 25% of the European regional inboard engines market, approximately US$ 0.085 Billion in 2026, driven by its position as the largest inland shipping nation on the Rhine corridor and a significant leisure boating market on the Baltic and North Sea coasts. MAN Energy Solutions, headquartered in Augsburg, is actively certifying its medium-speed diesel engine platforms to IMO Tier III NOx standards for European river and coastal vessel applications, reinforcing Germany's dual role as a market and manufacturing hub. Germany's industrial base in precision engine manufacturing positions it to disproportionately benefit from European fleet modernisation procurement through 2030.

- United Kingdom Inbound Engines Market Size

The United Kingdom represents an estimated 20% of the European regional inboard engines market, approximately US$ 0.068 Billion in 2026, supported by a strong coastal leisure boating sector concentrated in Southwest England, Scotland, and the Solent maritime region. The UK's Clean Maritime Plan, updated in 2023 by the Department for Transport, sets a target for zero-emission domestic shipping and inland waterway vessels by 2040, creating a medium-term compliance timeline that is already influencing new vessel specification decisions by commercial water taxi and ferry operators. British marina operators investing in shore-power infrastructure are directly enabling the hybrid inboard repower cycle across the leisure fleet.

France Inboard Engines Market Size

France represents an estimated 16% of the European regional inboard engines market, approximately US$ 0.054 Billion in 2026, reflecting its status as a major recreational boating nation with over 1 million registered pleasure craft according to the Fédération des Industries Nautiques (FIN). FPT Industrial, the powertrain brand of CNH Industrial, supplies diesel inboard engines to several French commercial and workboat OEMs operating on the Canal du Midi and Rhône-Saône inland waterway networks, where low-emission compliance is increasingly a tender prerequisite. France's Mediterranean coastline and Atlantic leisure sailing market will drive progressive hybrid inboard adoption among premium sailing yacht owners over the 2027–2033 period.

Asia Pacific Inboard Engines Market Trends and Insights

Asia Pacific accounts for 22.0% of the global inboard engines market in 2026, representing US$ 0.29 Billion, and is the fastest-growing region at a projected CAGR of 9.5% through 2033, driven by simultaneous expansion in commercial inland waterway freight, coastal tourism vessel fleets, and government-backed naval modernisation programmes. China's 14th Five-Year Plan (2021–2025) explicitly targets expansion of its inland waterway transport network to carry 1.8 billion tonnes of freight annually by 2025, catalysing procurement of modern diesel and hybrid inboard-powered cargo vessels across the Yangtze and Pearl River systems. Southeast Asian coastal tourism growth, particularly in Thailand, Indonesia, and Vietnam, is generating fleet expansion demand for mid-power inboard-engined passenger vessels that require certified OEM supply and after-sales support networks.

- China Inboard Engines Market Size

China represents an estimated 45% of the Asia Pacific regional inboard engines market, approximately US$ 0.130 Billion in 2026, driven by its scale as the world's largest inland waterway freight system operator and an expanding domestic leisure boating market centred on Hainan Island's Free Trade Port designation. Yanmar Marine International has established technical service partnerships with Chinese shipyard networks to support diesel inboard engine deployments across inland cargo vessel builds, with supply agreements active through 2025. China's 2024 coastal leisure boating regulation revisions, which relaxed recreational boat licensing requirements in selected coastal zones, are unlocking a structurally new domestic recreational demand cohort that will accelerate inboard engine volume through 2030.

- India Inboard Engines Market Size

India represents an estimated 23% of the Asia Pacific regional inboard engines market, approximately US$ 0.067 Billion in 2026, with growth anchored in the government's active expansion of national waterway freight capacity and coastal fishing vessel modernisation subsidies. The Ministry of Ports, Shipping and Waterways under its Sagarmala Programme has sanctioned fleet development projects across Kerala, West Bengal, and Assam that collectively require hundreds of new inboard-powered commercial vessels by 2027. India's nascent recreational marina infrastructure, with Kochi, Mumbai, and Goa developing certified berthing capacity, will begin contributing to leisure segment inboard demand from 2027 onward.

- Japan Inboard Engines Market Size

Japan represents an estimated 20% of the Asia Pacific regional inboard engines market, approximately US$ 0.058 Billion in 2026, supported by a mature coastal leisure boating sector and active procurement by the Japan Coast Guard for patrol vessel repowering. Yanmar Co., Ltd., headquartered in Osaka, leads Japan's domestic inboard diesel engine supply for both recreational and commercial applications, with its 4LHA and 6LPA series engines widely specified across domestic fishing and workboat classifications. Japan's Green Growth Strategy, which targets carbon neutrality by 2050 and includes specific maritime decarbonisation milestones, is prompting domestic ferry operators such as those serving inter-island routes in the Seto Inland Sea to pilot hybrid inboard configurations ahead of regulatory mandates expected by 2030.

Competitive Landscape

The global inboard engines market operates as a moderately consolidated oligopoly at the high-power commercial end and a more fragmented competitive environment in the recreational and sub-300 HP segments. Volvo Penta and Mercury Marine (Brunswick Corporation) collectively command estimated 35% of the recreational inboard segment by revenue, competing primarily on integrated drivetrain systems, dealer network depth, and digital engine management platforms.

Cummins Inc. and Caterpillar Inc. anchor the above-300 HP commercial and defence segments, where product certification, global service infrastructure, and long-term supply agreements determine contract wins over price. The disruptive entrant dynamic is most pronounced in the electric inboard sub-segment, where Torqeedo and Pure Watercraft, the latter having received investment from Amazon's Climate Pledge Fund, are challenging incumbent OEMs with purpose-built electric marine drivetrain architectures that incumbents are racing to match through acquisition or internal development programmes.

Key Market Developments

- January, 2025: Volvo Penta announced the commercial availability of its IPS Hybrid system for production boat builders, integrating a diesel inboard with electric harbour-mode drive capability, targeting Nordic and Baltic Sea recreational vessel OEMs seeking marina emission-zone compliance from the 2026 model year onward.

- March, 2024: Cummins Inc. signed a multi-year supply agreement with a European inland waterway operator group to provide QSB6.7 Tier III-certified diesel inboard engines for a fleet renewal programme covering 40 cargo vessels across the Rhine-Danube corridor, reinforcing its commercial marine segment position.

- October, 2024: Wärtsilä Corporation completed delivery of its HY marine hybrid module to a Scandinavian passenger ferry operator, marking the first commercial deployment of its integrated hybrid inboard propulsion system on a Baltic Sea short-sea route, validating hybrid inboard technology at commercial vessel scale.

Companies Covered in Global Inboard Engines Market

- Volvo Penta

- Mercury Marine

- Cummins Inc.

- Caterpillar Inc.

- Yanmar Marine International

- MAN Energy Solutions

- FPT Industrial

- Scania AB

- Wärtsilä Corporation

- MTU Friedrichshafen GmbH

- Nanni Industries

- Indmar Marine Engines

- Ilmor Engineering

- PCM Engines

- Perkins Marine

- Torqeedo (Deutz AG)

- Pure Watercraft

- Rolls-Royce Marine

- ZF Friedrichshafen AG

- John Deere Marine Engines

Frequently Asked Questions

The global inboard engines market is valued at US$ 1.30 Billion in 2026 and is projected to reach US$ 2.19 Billion by 2033 at a CAGR of 7.7%, driven primarily by fleet modernisation mandates enforced through the IMO's 2023 GHG Strategy and sustained post-pandemic recreational boat ownership that is now entering active powertrain replacement cycles.

Two primary drivers are propelling the global inboard engines market: mandatory marine engine emission upgrades under frameworks including the EU FuelEU Maritime Regulation effective from 2025, and the expansion of commercial inland waterway freight infrastructure, particularly under India's Jal Marg Vikas Project, which requires certified modern inboard powertrains across newly commissioned vessel fleets.

Diesel inboard engines hold the largest share at 63.0% of the global inboard engines market in 2026, owing to diesel's unmatched energy density of approximately 35.8 MJ/litre and its compatibility with the sustained high-torque load cycles of commercial fishing and long-range cruising applications; this structural advantage insulates the segment from substitution pressure through at least 2030.

North America dominates the global inboard engines market with a 37.0% share in 2026, sustained by the continent's approximately 12 million registered recreational boats and EPA Tier 4 marine engine compliance requirements that are actively forcing fleet-wide powertrain upgrades; the region's dense, well-funded marina network and established OEM dealer infrastructure will sustain this leadership position through the 2033 forecast horizon.

The highest-conviction opportunity lies in the commercial inland waterway vessel repowering cycle across South and Southeast Asia, where infrastructure programmes such as India's National Waterways Act 2016 are activating a commercially scalable fleet of cargo and passenger vessels requiring certified inboard powertrains; OEMs with IMO Tier III-certified engine portfolios and established regional service networks are best positioned to capture this demand as procurement pipelines formalise between 2026 and 2029.

Volvo Penta, Mercury Marine, Cummins Inc., and Caterpillar Inc. are the leading companies in the global inboard engines market, competing on product certification depth, integrated drivetrain systems, and global service network coverage rather than price alone; competitive intensity is moderate-to-high in the recreational segment and lower but more strategically complex in commercial and defence segments, where long-term supply agreements and classification society approvals create durable switching barriers.