- Medical Devices

- Implantable Collamer Lens Market

Implantable Collamer Lens Market Size, Share, and Growth Forecast 2026 - 2033

Implantable Collamer Lens Market is segmented by Product Type (Visian ICL, EVO ICL), by Application (Myopia, Hyperopia, Astigmatism), by End User (Hospitals, Ophthalmology Clinics, Ambulatory Surgery Centers, Eye Research Institutes), and by Regional Analysis for the period 2026 - 2033

Implantable Collamer Lens Market Share and Trends Analysis

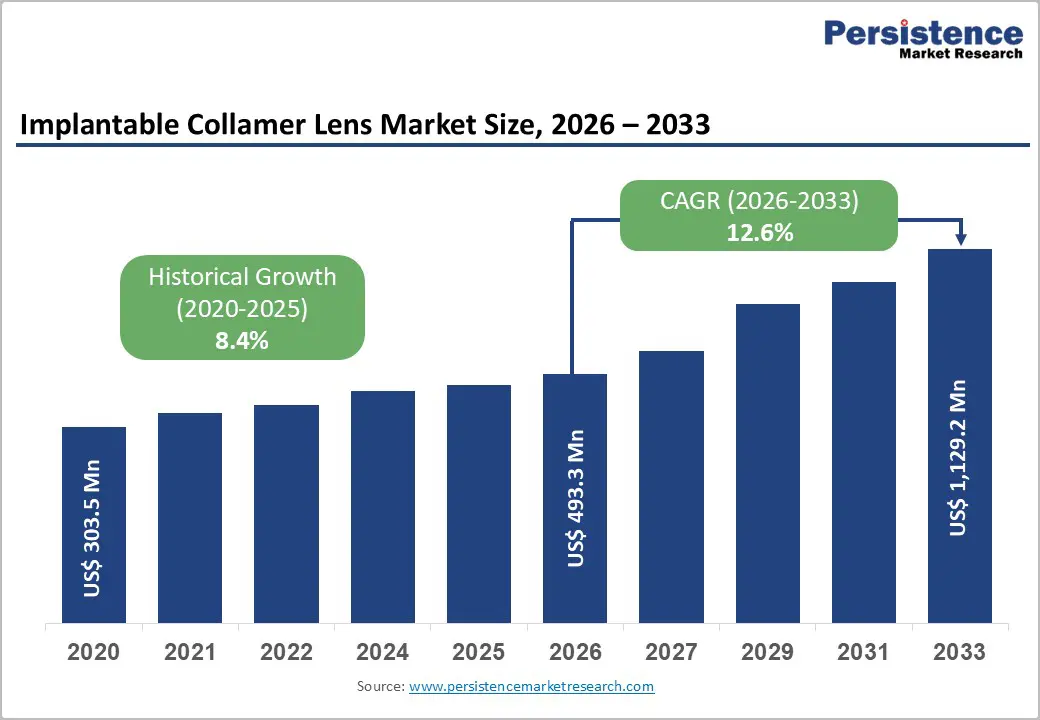

The global implantable collamer lens market size is expected to be valued at US$ 493.3 million in 2026 and projected to reach US$ 1,129.2 million by 2033, growing at a CAGR of 12.6% between 2026 and 2033. This expansion is primarily driven by the rising global burden of refractive errors, increasing preference for reversible vision correction procedures, and growing adoption of premium ophthalmic implants.

According to World Health Organization (WHO) estimates, over 2.2 billion people globally live with some form of vision impairment, creating sustained demand for procedures. Technological advancements in biocompatible collamer materials, along with regulatory approvals in major markets such as the U.S. FDA and the European CE marking, continue to reinforce surgeons' confidence and patients' adoption, accelerating long-term market momentum.

Key Industry Highlights:

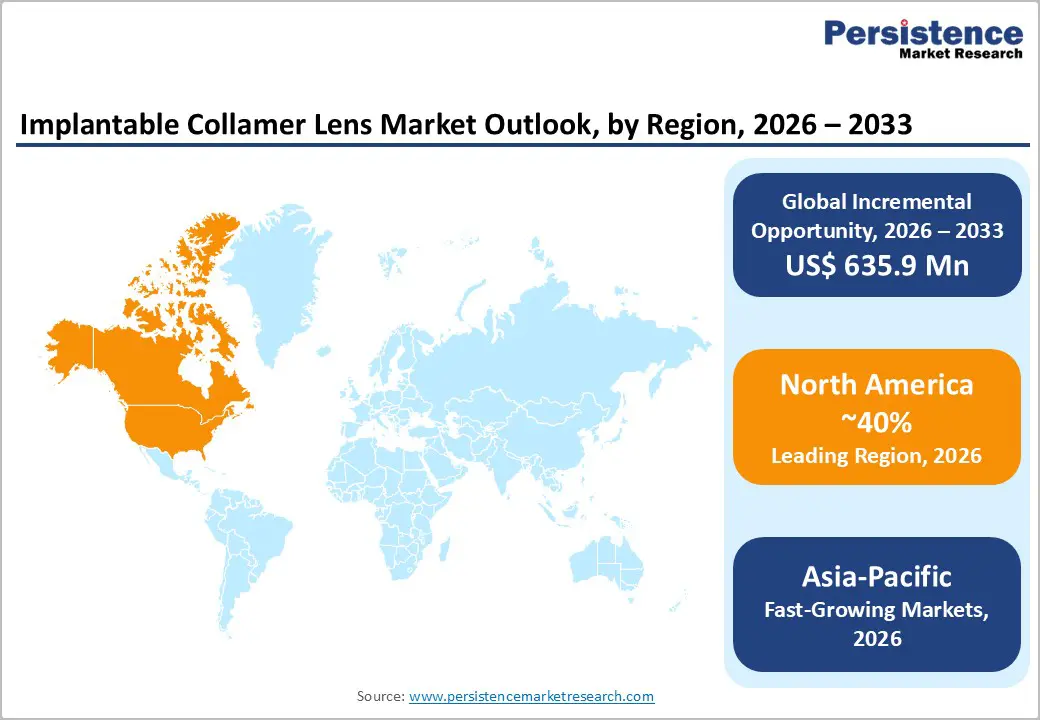

- Leading Region: North America leads the global implantable collamer lens market, supported by advanced ophthalmology infrastructure, high awareness of premium vision correction procedures, early adoption of innovative ophthalmic technologies, and a strong regulatory and clinical research ecosystem.

- Fastest Growing Region: Asia-Pacific is the fastest-growing region, driven by rapidly rising myopia prevalence, expanding middle-class populations, improving access to advanced eye care services, growth in medical tourism, and increasing availability of skilled refractive surgeons.

- Dominant Segment: EVO ICL dominates the product segment due to its improved safety design, elimination of peripheral iridotomy requirements, strong long-term clinical outcomes, and widespread surgeon preference for complex refractive error correction.

- Fastest-Growing Segment: Hyperopia applications are the fastest-growing segment, fueled by the limited effectiveness of laser-based procedures in high hyperopic cases, growing clinical evidence supporting ICL outcomes, and increasing

- adoption in tertiary and specialty ophthalmology centers.

| Key Insights | Details |

|---|---|

| Implantable Collamer Lens Market Size (2026E) | US$ 493.3 million |

| Market Value Forecast (2033F) | US$ 1,129.2 million |

| Projected Growth CAGR (2026 - 2033) | 12.6% |

| Historical Market Growth (2020 - 2025) | 8.4% |

Market Dynamics

Driver - Rising Prevalence of Refractive Errors and Myopia Epidemic

The rising prevalence of myopia and other refractive disorders is a fundamental driver of demand for implantable collamer lenses globally. According to World Health Organization, nearly 50% of the global population is projected to be myopic by 2050, with particularly high incidence rates reported across East Asia, urban Europe, and North America. This growing disease burden has increased the number of patients seeking permanent and high-precision vision correction solutions. Implantable collamer lenses are especially attractive for individuals with high refractive errors who are unsuitable for laser-based procedures. Unlike corneal reshaping techniques, ICLs preserve corneal integrity and offer reversibility, addressing long-term safety concerns. Peer-reviewed clinical studies consistently demonstrate excellent visual acuity outcomes, stable refractive correction, and low complication rates over extended follow-up periods. These advantages are reinforcing surgeon confidence and expanding adoption across both developed and emerging healthcare systems, positioning refractive error prevalence as a long-term structural growth driver for the market.

Technological Advancements and Regulatory Support in Ophthalmology

Ongoing technological innovation in ophthalmic implants and supportive regulatory frameworks are significantly accelerating the adoption of implantable collamer lenses. Advances in collagen-based materials science have resulted in lenses with high oxygen permeability, UV protection, and improved biocompatibility, reducing risks such as cataract formation and endothelial cell loss. Continuous refinement in lens design and surgical techniques has shortened procedure times and improved patient recovery outcomes. Regulatory clearances from authorities such as the U.S. Food and Drug Administration and the European Medicines Agency have expanded approved indications, strengthened physician trust and accelerated clinical adoption. In parallel, government-supported funding for ophthalmology research and vision science has increased the volume of long-term clinical data available, supporting evidence-based decision-making. Enhanced surgeon training programs and standardized clinical protocols are further improving procedural success rates, collectively reinforcing sustained market growth.

Restraints - High Procedure Cost and Limited Insurance Coverage

Despite strong clinical performance, the high cost of implantable collamer lens procedures remains a key barrier to wider adoption. In many healthcare systems, refractive surgeries are classified as elective procedures and are therefore excluded from public reimbursement schemes and private insurance coverage. As a result, patients must bear the full out-of-pocket expense, which can significantly limit demand, particularly in price-sensitive markets. This challenge is most pronounced in low- and middle-income countries, where disposable income constraints persist despite rising awareness of advanced vision correction technologies. Even in developed economies, the lack of insurance coverage can delay patient decision-making or shift preference toward lower-cost alternatives. The capital-intensive nature of advanced ophthalmic equipment and the need for highly trained surgeons further contribute to overall procedural costs. Unless broader financing models or insurance inclusion frameworks are introduced, cost-related barriers will continue to restrict penetration beyond affluent patient segments.

Opportunity - Rapid Growth in Hyperopia and Complex Refractive Error Treatment

Hyperopia and complex refractive error cases present a compelling growth opportunity for the implantable collamer lens market as clinical limitations of laser-based procedures become more evident. High hyperopic corrections often yield suboptimal outcomes with corneal laser surgeries due to biomechanical instability, regression risk, and reduced long-term predictability. Implantable collamer lenses overcome these challenges by providing stable, reversible, and cornea-sparing vision correction, making them increasingly preferred by refractive surgeons for complex cases. Clinical studies have consistently reported strong improvements in visual acuity, high patient satisfaction, and durable refractive stability among hyperopic patients treated with ICLs, particularly those unsuitable for laser surgery. Growing dissemination of these outcomes through professional ophthalmology associations, scientific congresses, and peer-reviewed clinical guidelines is improving awareness among surgeons and patients alike.

As a result, tertiary eye care centers and specialty ophthalmology clinics are progressively positioning ICLs as a premium solution for complex refractive errors. This evolving clinical practice creates substantial opportunities for manufacturers to expand approved indications, introduce customized lens designs, and address higher-value patient segments over the next decade.

Category-wise Analysis

Product Type Insights

The EVO ICL segment emerged as the leading product type in the implantable collamer lens market, accounting for approximately 65% market share in 2025. Its dominance is primarily driven by significant design advancements that have improved procedural safety and clinical outcomes. Unlike earlier-generation lenses, EVO ICL eliminates the need for peripheral iridotomy, simplifying the surgical workflow and reducing the risk of post-operative complications such as elevated intraocular pressure. Clinical data from long-term follow-up studies highlight stable refractive correction, high patient satisfaction, and a favorable safety profile, thereby strengthening surgeons' confidence globally.

Additionally, the lens’s high oxygen permeability and biocompatible collamer material support better ocular health, particularly in younger and high-risk patients. Continuous product refinement, along with robust post-market surveillance and real-world evidence generation, has further reinforced EVO ICL’s leadership. These factors collectively position EVO ICL as the preferred choice among refractive surgeons for premium vision correction procedures.

By End User Analysis

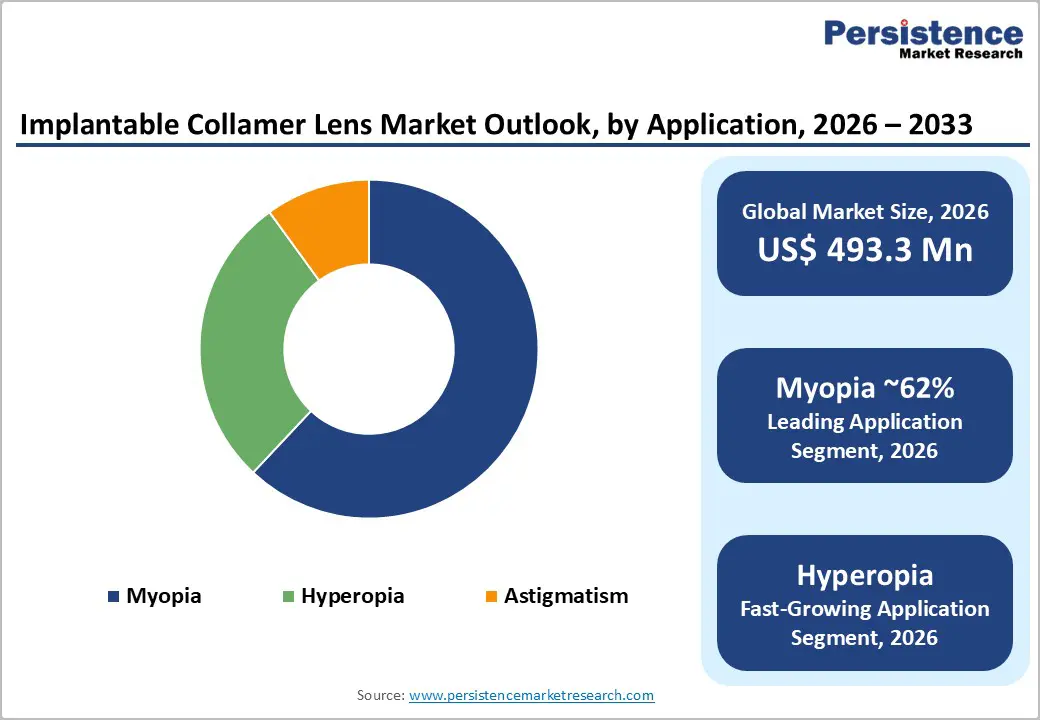

Myopia dominated the application segment, capturing nearly 62% market share in 2025, largely due to its widespread global prevalence and strong clinical suitability for implantable collamer lens procedures. Rising screen exposure, urban lifestyles, and genetic predisposition have significantly increased myopia incidence, particularly among younger populations. Implantable collamer lenses are especially effective for patients with moderate-to-high myopic corrections who are unsuitable for laser-based surgeries due to thin corneas or high refractive power requirements. Clinical studies consistently demonstrate excellent visual acuity outcomes, long-term refractive stability, and low rates of regression in myopic patients treated with ICLs. These advantages make Myopia the most established and trusted application area for implantable collamer lenses. Furthermore, growing patient awareness of premium, reversible vision correction options and strong surgeon familiarity with myopia correction protocols continue to support sustained dominance in the global market.

Regional Insights

North America Implantable Collamer Lens Market Trends

North America maintained its leadership position in the implantable collamer lens market, accounting for approximately 40% market share in 2025, driven by a highly developed healthcare ecosystem and early adoption of advanced ophthalmic technologies. The region benefits from a strong base of refractive surgeons, widespread availability of specialized ophthalmology clinics, and high patient awareness regarding premium vision correction solutions. These factors collectively support consistent procedural volumes and steady technology uptake.

The U.S. remains the dominant contributor within North America due to favorable regulatory pathways, including timely approvals from the U.S. Food and Drug Administration (FDA), and a robust innovation environment. Significant investments in clinical research, ophthalmic device trials, and surgeon training programs further enhance market maturity. Additionally, the strong presence of leading implantable lens manufacturers and well-established reimbursement and financing options for elective procedures continue to reinforce North America’s sustained market leadership.

Asia Pacific Implantable Collamer Lens Market Trends

Asia Pacific is the fastest-growing regional market for implantable collamer lenses, driven by a rapidly rising prevalence of myopia and other refractive disorders. Urbanization, rising screen exposure, and lifestyle changes have significantly increased the need for vision correction, particularly among younger populations. Expanding middle-class demographics and improving affordability of advanced ophthalmic procedures are further accelerating patient demand across the region.

Countries such as China, Japan, and India are witnessing rapid growth in surgical volumes due to expanding ophthalmology infrastructure and increasing availability of skilled refractive surgeons. Government-backed healthcare investments, combined with the development of local medical device manufacturing capabilities, are strengthening regional competitiveness. In addition, Asia-Pacific’s growing role in medical tourism and cost-effective surgical care positions the region as a key growth engine for the global implantable collagen lens market.

Competitive Landscape

The implantable collamer lens market is moderately consolidated, with a small number of specialized manufacturers holding a significant share due to strong intellectual property portfolios and long-term clinical validation. Market leaders prioritize continuous product innovation, advanced collamer material development, and extensive surgeon training programs to strengthen adoption. Strategic focus on global regulatory approvals and expansion into emerging markets further enhances competitive positioning. Investments in research and development, supported by robust post-market surveillance and long-term clinical outcome data, serve as key differentiators. Meanwhile, emerging players are pursuing regional partnerships, localized manufacturing, and cost-optimization strategies to improve accessibility and compete effectively in high-growth markets.

Key Industry Developments:

- In March 2024: STAAR Surgical expanded EVO ICL indications across additional international markets following regulatory approvals.

- In September 2023: Alcon enhanced its refractive surgery portfolio through strategic investments in ophthalmic innovation platforms.

Companies Covered in Implantable Collamer Lens Market

- STAAR Surgical

- Carl Zeiss Meditec

- Bausch + Lomb

- Alcon

- Johnson & Johnson

- Others

Frequently Asked Questions

The implantable collamer lens market is estimated to be valued at US$ 493.3 Mn in 2026.

Government investment and funding initiatives supporting research and development in ophthalmic technologies and advanced vision correction procedures are expected to significantly drive the global implantable collamer lens market.

The global market is expected to witness a CAGR of 5.2% between 2026 and 2033.

A few of the prominent players operating in the market are STAAR Surgical, Carl Zeiss Meditec, Bausch + Lomb, Alcon, Johnson & Johnson, and Others.

North America is the leading region in the global implantable collamer lens market.