- Specialty & Fine Chemicals

- Hydrogel Market

Hydrogel Market Size, Share, and Growth Forecast, 2026 - 2033

Hydrogel Market By Composition (Synthetic Hydrogels, Natural Hydrogels, Others), Form (Semi-crystalline, Amorphous, Others), End-user Industry and Regional Analysis for 2026 - 2033

Hydrogel Market Size and Trends Analysis

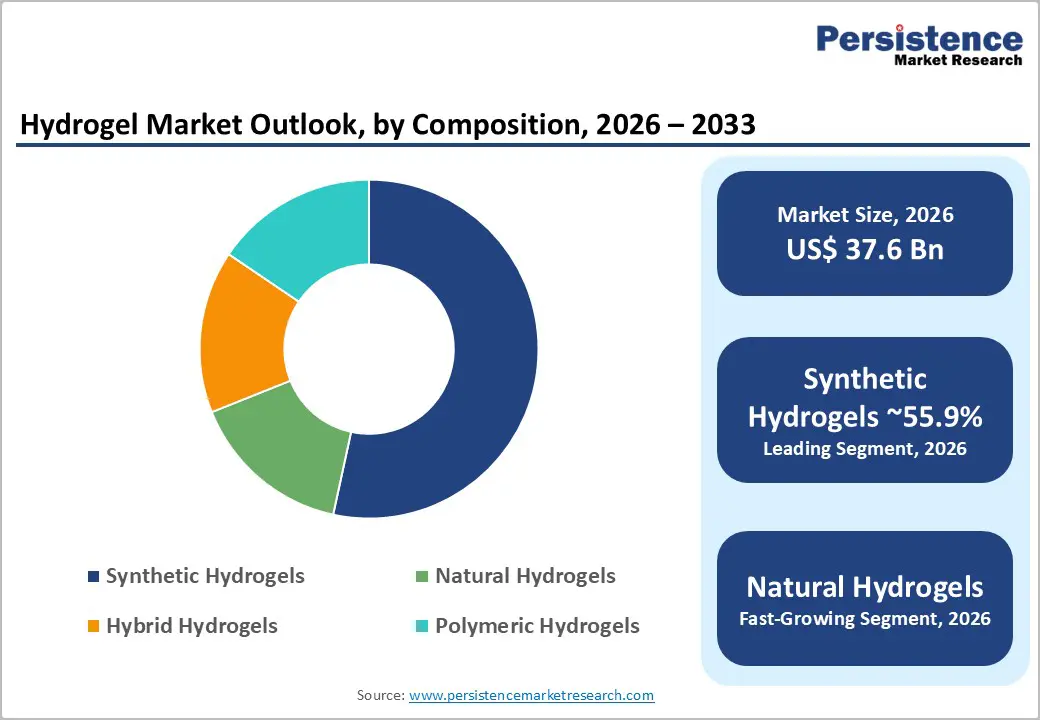

The global hydrogel market size is likely to be valued at US$ 37.6 billion in 2026 and is expected to reach US$59.9 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by sustained cross-industry demand, led by high-volume personal care applications and accelerating adoption in healthcare and medical technologies.

Aging populations, expanding healthcare infrastructure, and growing consumer demand for high-performance absorbent materials support structural growth. At the same time, technological advancements in bioactive hydrogels, drug-delivery matrices, and tissue engineering platforms are increasing the value mix of the market. These converging factors reinforce a stable yet innovation-driven growth trajectory through 2033.

Key Industry Highlights:

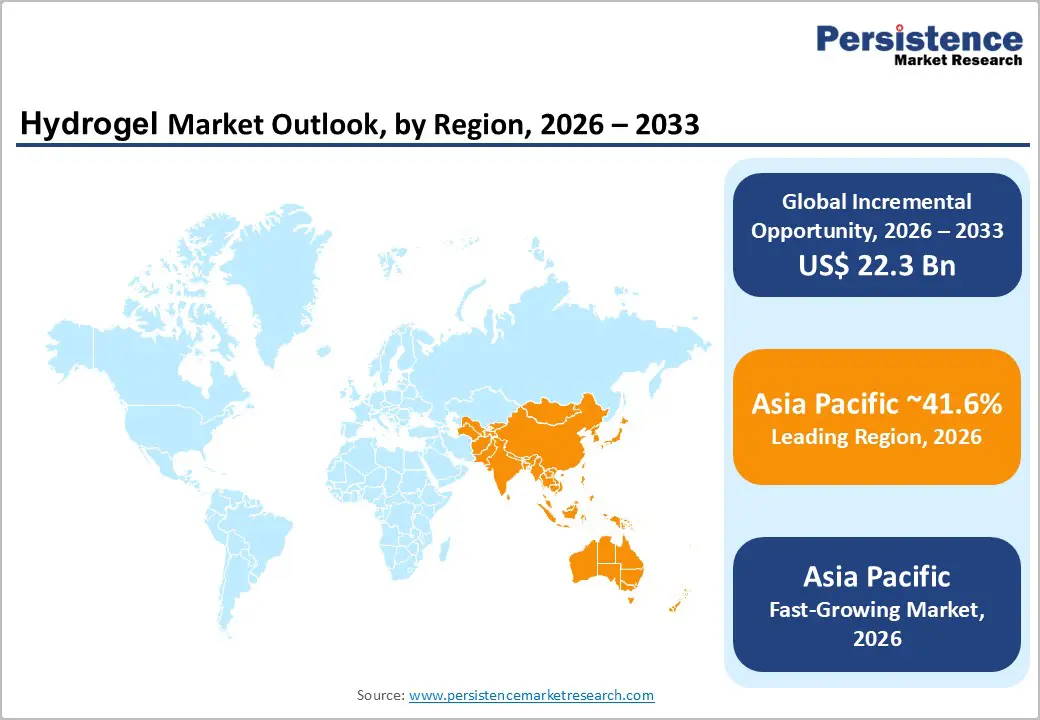

- Leading Region: Asia Pacific is projected to hold 41.6% of market share, driven by large-scale hygiene manufacturing in China and high-value medical hydrogel innovation in Japan.

- Fastest-growing Region: Asia Pacific is supported by rising hygiene penetration in India and ASEAN markets, expanding healthcare infrastructure, and localized polymer production investments.

- Investment Plans: Increased funding in biofabrication, drug-delivery platforms, and biodegradable polymer research across North America and Europe, alongside greenfield manufacturing and joint ventures in Asia Pacific to strengthen supply chain resilience.

- Dominant Composition: Synthetic hydrogels are anticipated to account for 55.9% share, supported by scalability, cost efficiency, and strong integration in hygiene, contact lenses, and wound-care products.

- Leading End-user Industry: Personal care & hygiene is anticipated to hold 61.2% share, driven by high-volume diaper, sanitary, and skincare mask applications with stable long-term procurement contracts.

| Key Insights | Details |

|---|---|

| Hydrogel Market Size (2026E) | US$37.6 Bn |

| Market Value Forecast (2033F) | US$59.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Advanced Wound Care and Medical Applications

Hydrogels play a clinically validated role in maintaining a moist wound environment, facilitating autolytic debridement, and enabling controlled therapeutic release. The global rise in chronic wounds, diabetic ulcers, and burn injuries continues to increase demand for advanced wound-care products. Aging demographics significantly influence this trend, as older populations are more susceptible to chronic wounds and delayed healing. Regulatory approvals for hydrogel-based dressings, scaffolds, and implantable matrices have broadened therapeutic applications. Growth in certified medical hydrogels supports higher average selling prices and margin expansion. Manufacturers investing in antimicrobial, bioactive, and drug-loaded hydrogel systems are positioned to capture premium hospital procurement contracts.

Scale and Recurring Demand in Personal Care & Hygiene

Personal care and hygiene products represent the volume backbone of the hydrogel market. Superabsorbent hydrogels are essential in diapers, feminine hygiene products, and adult incontinence solutions. Rising global birth rates in emerging markets and increasing life expectancy globally sustain demand for absorbent hygiene products. Consumer expectations for improved comfort, thinner profiles, and enhanced absorbency further drive material innovation. In skincare, hydrogel masks and patches benefit from strong consumer adoption due to improved moisture retention and skin adherence compared to conventional materials. The recurring, high-volume nature of hygiene applications provides revenue stability, while innovation in biodegradable and low-residue hydrogels increases pricing power.

Technological Convergence in Drug Delivery and Biofabrication

Hydrogel technologies are increasingly integrated into advanced biomedical systems, including injectable drug-delivery platforms, hydrogel-forming microneedles, and 3D bioprinting bioinks. These systems enable controlled release kinetics, localized therapeutic delivery, and structural support for tissue regeneration. Research institutions and biotechnology firms are accelerating translational research in hydrogel-based regenerative medicine. This innovation pipeline shifts the revenue mix toward higher-margin specialty products. Technology-intensive hydrogel segments are expected to outpace commodity growth, improving overall market value density and strengthening intellectual property-driven competition.

Barrier Analysis - Regulatory and Clinical Validation Complexity

Medical-grade hydrogels, particularly drug-device combination products, are subject to stringent regulatory review. Biocompatibility testing, sterility validation, toxicology studies, and multi-phase clinical trials extend commercialization timelines. Products classified as combination therapies can incur development costs two to four times higher than standard dressings and may face 12 to 36 months of additional regulatory review. These requirements increase capital intensity and delay revenue realization, especially for small and mid-sized innovators.

Raw Material Volatility and Sustainability Pressures

Hydrogel production depends on specialty monomers, crosslinking agents, and purified water systems. Price volatility in petrochemical-derived inputs affects margins for synthetic hydrogel manufacturers. Environmental scrutiny regarding the disposal of non-biodegradable superabsorbents further adds reformulation costs. Manufacturers may incur compliance-driven reformulation expenditures equivalent to low-single to mid-single digit percentages of revenue over multi-year transition periods, particularly in regions enforcing stricter sustainability mandates.

Opportunity Analysis - Growth in Biodegradable and Natural Hydrogels

Regulatory and consumer preference shifts toward sustainable materials are creating premium demand for biodegradable hydrogels derived from polysaccharides and proteins. Natural hydrogels offer compostability and reduced environmental impact compared to conventional synthetic polymers. Companies capable of scaling certified biodegradable formulations can secure preferred supplier status with multinational consumer goods firms. Early certification, supply chain traceability, and performance parity with synthetic alternatives create a clear path to premium pricing.

Expansion in Emerging Markets and Localized Manufacturing

Asia Pacific and other emerging markets present strong volume growth in both personal care and healthcare applications. Establishing regional manufacturing reduces logistics costs, tariff exposure, and lead times. Localized production also enables formulation customization for regional conditions, such as climate-specific hygiene products or soil-optimized agricultural hydrogels. Strategic joint ventures and contract manufacturing agreements provide capital-efficient entry pathways.

Category-wise Analysis

Composition Insights

Synthetic hydrogels are anticipated to account for approximately 55.9% of market revenue in 2026, maintaining their dominance due to scalability, tunable mechanical properties, and cost efficiency. These materials are extensively used in disposable hygiene products such as baby diapers and adult incontinence pads, where superabsorbent polymers provide high fluid retention capacity. In healthcare, synthetic hydrogels are widely applied in wound dressings, hydrogel sheets, and ophthalmic products such as soft contact lenses. Industrial applications, including water-retention agents and absorbent pads, further support volume stability. Manufacturing advantages play a central role in segment leadership.

Large-scale polymerization processes, established global distribution networks, and backward integration into petrochemical feedstocks enhance supply reliability. Performance customization through crosslink density, polymer composition, and swelling ratio control allows manufacturers to tailor products for specific absorption rates, tensile strength requirements, and shelf-life parameters. For example, polyacrylate-based hydrogels are optimized for hygiene absorption performance, while polyvinyl alcohol hydrogels are preferred in biomedical matrices. These characteristics collectively ensure that synthetic hydrogels retain the largest revenue contribution within the overall market.

Natural hydrogels are emerging as the fastest-growing composition segment, supported by sustainability mandates and increasing regulatory emphasis on biodegradable materials. These hydrogels are typically derived from polysaccharides such as alginate, chitosan, cellulose derivatives, and proteins, including gelatin. Their biocompatibility and biodegradability make them particularly attractive in wound healing, drug delivery, and agricultural soil-conditioning applications. In agriculture, starch-based hydrogels are used to enhance soil moisture retention and reduce irrigation frequency, especially in water-stressed regions. In cosmetics, naturally derived hydrogels are incorporated into clean-label skincare masks and patches to align with consumer preferences for plant-based ingredients.

Demand for eco-certified inputs enhances supplier differentiation, particularly among multinational personal care brands with formal sustainability targets. Companies offering traceable renewable feedstocks and validated biodegradation performance are capturing incremental market share in environmentally sensitive applications, positioning natural hydrogels as a strategic long-term growth vector.

End-user Industry Insights

Personal care and hygiene are anticipated to account for approximately 61.2% of market share in 2026. High-volume applications such as baby diapers, feminine hygiene products, adult incontinence solutions, and hydrogel-based facial masks drive recurring demand. Superabsorbent hydrogel particles form the functional core of modern diaper technology, enabling thinner designs with improved absorption efficiency.

In skincare, hydrogel sheet masks and under-eye patches are widely adopted for enhanced skin adhesion and moisture retention compared to traditional fabric-based alternatives. Long-term supply agreements between hydrogel manufacturers and global consumer goods companies provide predictable procurement cycles and revenue stability. Economies of scale, optimized logistics, and mature retail distribution networks reinforce the segment’s leadership position.

Healthcare and medical applications are the fastest-growing end-user segment. Growth is driven by advanced wound-care solutions, implantable scaffolds for tissue regeneration, ophthalmic hydrogels used in contact lenses, and controlled drug-delivery systems. Hydrogel dressings are increasingly utilized in diabetic ulcer management and post-surgical wound care due to their moisture-balancing and antimicrobial delivery capabilities.

Injectable hydrogel matrices are also being explored for cartilage repair and localized chemotherapy delivery. As hospitals adopt advanced treatment protocols and outpatient care expands, demand for certified medical-grade hydrogels continues to rise. Higher regulatory barriers create pricing resilience, while product differentiation through bioactive additives and sustained-release formulations supports margin expansion opportunities for manufacturers.

Regional Insights

North America Hydrogel Market Trends - High Healthcare Expenditure and Clinical Innovation Sustaining Premium Hydrogel Demand

North America remains a significant revenue contributor, with the U.S. driving the majority of regional demand due to high healthcare expenditure and a mature personal care industry. According to the Centers for Medicare & Medicaid Services, U.S. healthcare spending exceeds 17% of GDP, supporting strong procurement of advanced wound-care solutions that utilize hydrogel dressings and bioactive matrices. Companies such as 3M Company and ConvaTec Group maintain extensive wound-care portfolios distributed across U.S. hospitals and outpatient clinics, reinforcing stable hydrogel demand through institutional purchasing agreements.

The regulatory framework, overseen by the U.S. Food and Drug Administration, emphasizes rigorous clinical validation for medical-grade hydrogels. While this increases development timelines and compliance costs, it enhances post-approval pricing stability and brand credibility. In parallel, innovation ecosystems are expanding. For instance, MIT and affiliated biotech startups have advanced hydrogel-based drug-delivery and tissue-engineering platforms, attracting venture capital funding. Investment in biofabrication technologies, including 3D bioprinting hydrogels for regenerative medicine, continues to rise across innovation hubs such as Boston and California.

In personal care, multinational brands including Procter & Gamble integrate superabsorbent hydrogel polymers into premium diaper lines under Pampers, sustaining recurring volume consumption. Home-based healthcare expansion, accelerated by post-pandemic telehealth adoption, has increased demand for easy-to-apply hydrogel wound dressings suitable for outpatient and elderly care settings. These structural healthcare and consumer trends collectively reinforce North America’s high-value market positioning.

Europe Hydrogel Market Trends - Regulatory Harmonization and Sustainability Mandates Advancing Bio-Based Hydrogel Innovation

Europe demonstrates steady hydrogel demand supported by advanced medical infrastructure and strong environmental governance frameworks. Countries such as Germany, the U.K., France, and Spain contribute significantly through medical device manufacturing and consumer goods production. German-based B. Braun Melsungen and Paul Hartmann AG actively supply hydrogel wound dressings across European hospital networks, strengthening regional procurement consistency.

The implementation of the European Medicines Agency and the Medical Device Regulation framework has harmonized compliance requirements across EU member states. Although certification processes have become more stringent and costly, standardized approval pathways streamline cross-border distribution and enhance product traceability. This regulatory alignment supports premium positioning of clinically validated hydrogel products throughout the region.

Sustainability priorities are particularly influential in Europe. The European Green Deal and circular economy strategies encourage biodegradable and bio-based materials in consumer and agricultural applications. Companies such as BASF SE are investing in sustainable polymer research, including bio-based superabsorbent technologies that reduce fossil-feedstock dependency. In personal care, brands owned by Unilever increasingly emphasize recyclable and responsibly sourced materials, indirectly stimulating innovation in biodegradable hydrogel substrates for cosmetic masks and hygiene products. These sustainability-led shifts position Europe as a center for environmentally responsible hydrogel development.

Asia Pacific Hydrogel Market Trends - Manufacturing Scale and Hygiene Penetration Accelerating Volume Expansion

Asia Pacific is projected to hold approximately 41.6% of the market share in 2026 and remains the fastest-growing regional market. China leads in manufacturing scale and cost competitiveness, supported by integrated polymer supply chains and export-oriented production models. Major hygiene product manufacturers such as Hengan International Group utilize superabsorbent hydrogel materials in large-volume diaper and sanitary product lines, contributing to strong domestic consumption and export growth. Japan maintains leadership in high-value medical and ophthalmic hydrogels. Companies such as Nitto Denko Corporation and Menicon Co., Ltd. advance hydrogel technologies for contact lenses and specialty biomedical applications, supporting premium-margin segments. In India, expanding hygiene penetration and rising disposable incomes drive growth for diaper brands under Unicharm Corporation and domestic producers, accelerating hydrogel consumption in fast-growing urban centers.

Regional expansion is closely tied to rapid urbanization, healthcare infrastructure upgrades, and government-backed manufacturing initiatives. China’s focus on advanced materials under national industrial strategies encourages localized hydrogel innovation, while India’s medical device parks promote domestic production capacity. Joint ventures and greenfield investments remain common entry strategies for multinational firms seeking cost advantages and supply chain resilience. Localized production reduces logistics costs and mitigates cross-border trade risks, further strengthening Asia Pacific’s leadership and long-term growth trajectory in the hydrogel market.

Competitive Landscape

The global hydrogel market exhibits a hybrid structure. Commodity hygiene materials are moderately consolidated among large chemical and consumer goods suppliers. In contrast, medical and biofabrication segments remain more fragmented, driven by innovation-focused firms. Competitive positioning centers on scale efficiency in commodity segments and intellectual property strength in specialty medical applications.

Leading companies emphasize innovation in smart and bioactive hydrogels, cost optimization through regional manufacturing, and strategic partnerships for geographic expansion. Regulatory compliance and proprietary formulation technologies serve as primary competitive differentiators.

Key Industry Developments

- In February 2025, Biomiq Inc. launched PureGel™, a nanotechnology-based hydrogel for advanced wound care that delivers stable hypochlorous acid for extended antimicrobial activity, now licensed as a Class II medical device in Canada.

- In January 2025, Beiersdorf expanded its Hansaplast/Second Skin wound care portfolio by introducing invisible spray and liquid hydrogel-based formats designed to improve everyday wound treatment convenience and support global category growth.

Companies Covered in Hydrogel Market

- BASF SE

- Evonik Industries AG

- Nippon Shokubai Co., Ltd.

- Sumitomo Seika Chemicals Co., Ltd.

- LG Chem Ltd.

- Sanyo Chemical Industries, Ltd.

- Kuraray Co., Ltd.

- SNF Group

- Arkema S.A.

- Ashland Inc.

- Henkel AG & Co. KGaA

- 3M Company

- ConvaTec Group

- Coloplast A/S

- Paul Hartmann AG

- Nitto Denko Corporation

- DSM Biomedical

- Johnson & Johnson

Frequently Asked Questions

The global hydrogel market size in 2026 is estimated at US$37.6 billion.

The hydrogel market is projected to reach US$59.9 billion by 2033.

The hydrogel market is expected to grow at a CAGR of 6.9% between 2026 and 2033, reflecting steady expansion across both consumer and medical-grade applications.

Key trends include increasing adoption of hydrogel-based advanced wound-care products, rising use in controlled drug-delivery systems, expansion of biodegradable and bio-based hydrogel solutions, and sustained innovation in ophthalmic and tissue-engineering applications. Investment in sustainable polymer chemistry and localized production capacity is also shaping competitive dynamics.

By composition, synthetic hydrogels lead the market with an anticipated 55.9% share, supported by scalability and cost efficiency. By end-user industry, personal care & hygiene dominates with approximately 61.2% share, driven by high-volume diaper and sanitary product applications.

Major companies include BASF SE, Evonik Industries AG, Nippon Shokubai Co., Ltd., LG Chem Ltd., and 3M Company.