- Medical Devices

- Europe Neurothrombectomy Devices Market

Europe Neurothrombectomy Devices Market Size, Share, and Growth Forecast, 2026 – 2033

Europe Neurothrombectomy Devices Market by Product (Stent Retrievers, Aspiration/Suction Devices, Vascular Snares), End-user (Hospitals, Ambulatory Surgical Centers, Others), and Country Analysis 2026 – 2033

Europe Neurothrombectomy Devices Market Size and Trends Analysis

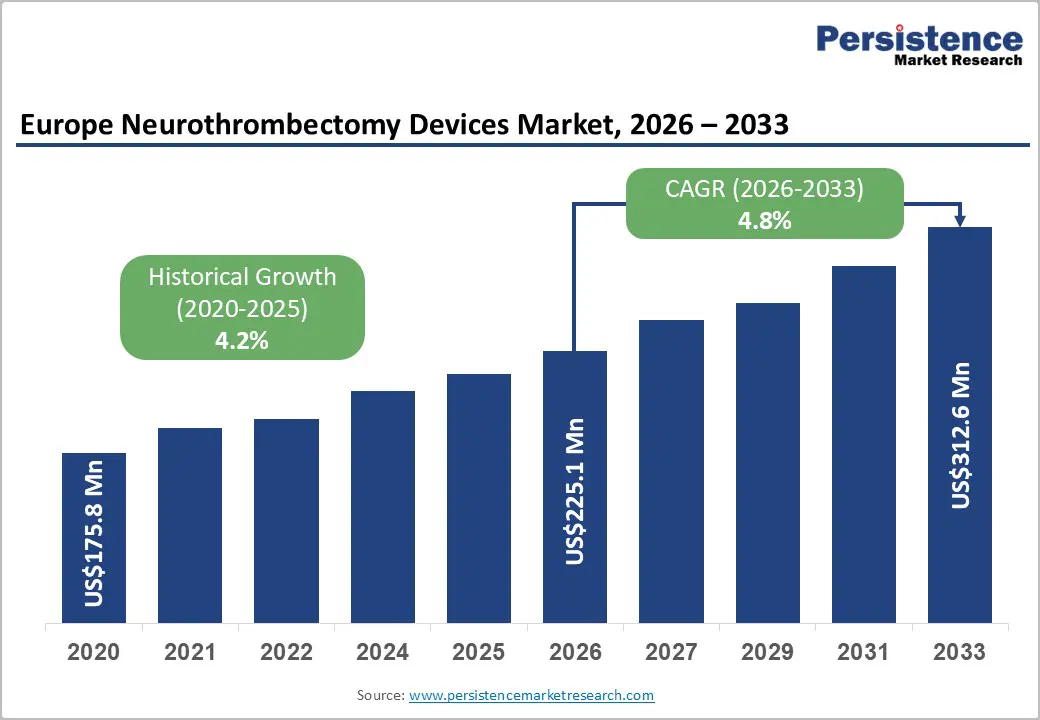

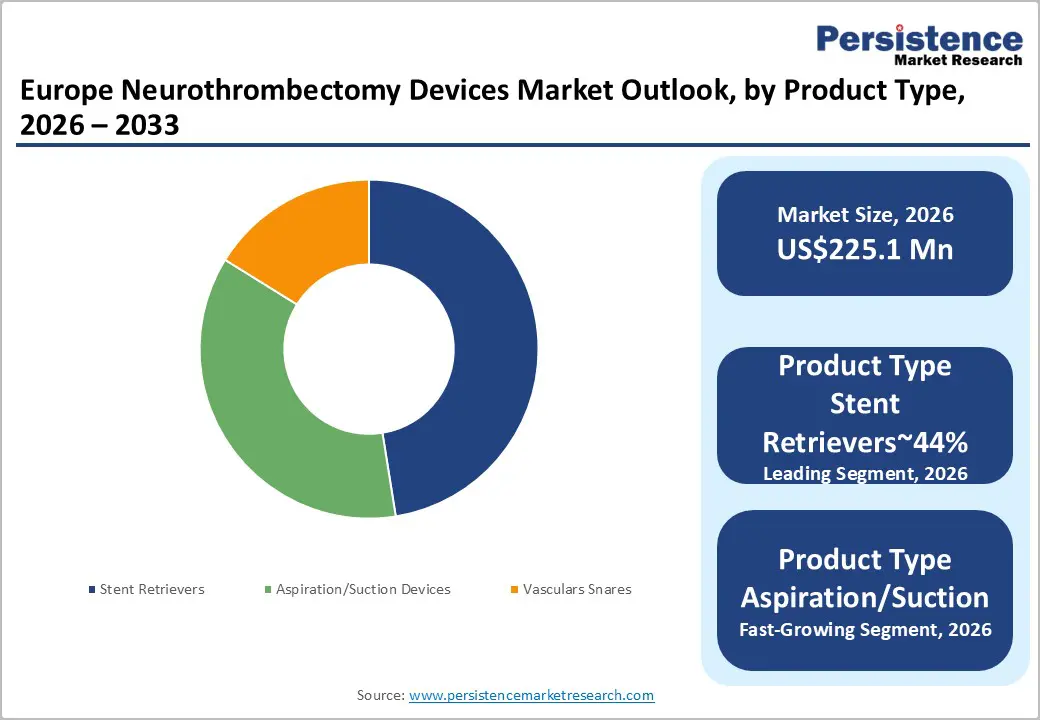

The Europe neurothrombectomy devices market size is likely to be valued at US$225.1 million in 2026 and is expected to reach US$312.6 million by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033.

The market is primarily propelled by the increasing clinical preference for Mechanical Thrombectomy (MT) over traditional pharmacological thrombolysis, particularly for large vessel occlusions (LVOs). Furthermore, the continuous expansion of specialized stroke centers across Western Europe and the integration of AI-driven triage systems have significantly reduced "door-to-puncture" times, enhancing the utilization rates of these life-saving devices.

Key Industry Highlights:

- Leading Country: Germany is projected to lead due to dense networks of certified stroke units, advanced reimbursement frameworks, and integrated digital health initiatives, accounting for approximately 33% share in 2026, supported by AI-assisted stroke triage, tele-thrombectomy adoption, and strong hospital ecosystem integration.

- Fastest-Growing Country: Germany is anticipated to grow the fastest due to a “mechanical-first” clinical shift, robust G-DRG reimbursement incentives, widespread direct-to-Angio protocols, and mobile stroke units enhancing device utilization across urban and rural centers.

- Leading Product: Stent retrievers are expected to lead, accounting for approximately 47% share in 2026 through industrial adoption in high-volume hospitals, first-pass recanalization efficiency, procedural reliability, and integration with AI-assisted imaging platforms for complex thrombi.

- Leading End-user: Hospitals are projected to dominate for simplicity, high procedural throughput, guideline-driven adoption, and functional use across key stroke intervention sectors, holding approximately 71% share in 2026.

| Key Insights | Details |

|---|---|

|

Europe Neurothrombectomy Devices Market Size (2026E) |

US$225.1 Mn |

|

Market Value Forecast (2033F) |

US$312.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expansion of Therapeutic Window and Guideline Endorsement

The European neurothrombectomy devices market is experiencing significant momentum due to the expansion of treatment eligibility windows. Landmark trials extended mechanical thrombectomy protocols from six to twenty-four hours, reshaping clinical practice and standardizing late-intervention eligibility across multiple healthcare systems. Regulatory and guideline adoption in countries such as Germany and the U.K. has formalized these extended windows, compelling hospitals to upgrade procedural infrastructure and device inventories. This has increased institutional demand for advanced stent retrievers, aspiration catheters, and vascular access tools.

Hospitals are now required to align treatment pathways with the updated clinical recommendations, embedding device readiness into acute stroke management protocols while influencing procurement strategies and operating budgets.

The guideline-driven extension has also amplified patient inclusion across neurovascular care programs, structurally expanding the addressable market. Late-presenting patients now receive intervention opportunities previously unavailable, reinforcing hospital-level investments in device portfolios and training. Clinical adoption pressures are integrating with technology evolution, necessitating optimized catheters and retrievers capable of complex vessel navigation. The combined effect of regulatory endorsement, expanded eligibility, and procedural standardization is establishing a durable, high-demand environment for neurothrombectomy solutions across Europe.

Technological Advancements in Neurothrombectomy Devices

The neurothrombectomy devices market in Europe is being structurally influenced by next-generation stent retrievers and aspiration systems. Enhanced device designs have substantially improved first-pass success rates, reducing intra-procedural complications and shortening procedure durations. Integration of AI-enhanced imaging into stroke workflows allows real-time identification of large vessel occlusions, accelerating intervention and improving functional outcomes.

Regulatory approvals, including CE marking, have facilitated faster market access, enabling hospitals to adopt advanced device portfolios efficiently. High-volume centers benefit from optimized catheter navigation, reduced procedure times, and improved patient throughput, which collectively reinforce procurement demand and operational efficiency across neurointerventional networks.

Artificial intelligence platforms deployed across hub-and-spoke hospital systems provide automated CT angiogram analysis, streamlining team alerts and decision-making. These innovations reduce treatment delays, enhance procedural accuracy, and increase capacity for late-presenting or complex stroke cases. The convergence of device refinement, AI-assisted imaging, and regulatory facilitation creates a robust environment for sustained demand growth in aspiration and stent retriever segments. Institutional adoption trends are driving structural expansion in the European neurothrombectomy ecosystem.

Barrier Analysis – High Procedural Costs and Economic Pressure

The European neurothrombectomy devices market faces structural constraints from elevated procedural costs, including device kits, specialized labor, and post-operative care requirements. Hospitals and public health systems are compelled to balance acute stroke intervention needs against finite budget allocations, creating economic pressure on device procurement decisions. High unit costs for stent retrievers and large-bore aspiration catheters restrict widespread adoption, particularly in lower-income regions.

Financial limitations influence treatment accessibility, constraining the ability of healthcare providers to deliver timely mechanical thrombectomy interventions across diverse clinical settings. Cost pressures also affect hospital capital planning and reimbursement negotiations, impacting long-term device investment strategies and operational readiness in acute neurovascular care programs.

Budgetary constraints amplify regional disparities in stroke treatment access, with economically challenged areas experiencing lower procedural volumes despite clinical eligibility. The combination of high upfront device expenditure and limited reimbursement adjustments impedes uniform adoption of neurothrombectomy solutions. These financial barriers reinforce differences in clinical outcomes, restrict procedural throughput, and influence technology integration priorities. Consequently, economic pressures continue to serve as a key restraint on market growth and equitable device utilization across Europe.

Operator Training and Infrastructure Shortages

The European neurothrombectomy devices market is constrained by the limited availability of specialized neurointerventionalists, particularly in France and Spain, where practitioner density remains extremely low. This scarcity contributes to delayed patient transfers, resulting in a substantial portion of eligible cases being excluded from timely intervention.

Rural and semi-urban regions face persistent access gaps, as a significant share of centers lack hybrid operating suites required for complex thrombectomy procedures. These infrastructure limitations impede procedural efficiency, restrict device utilization, and necessitate extensive investment in facility upgrades to meet clinical guideline standards. Workforce shortages also affect hospital scheduling, training programs, and patient throughput, creating operational bottlenecks across high-demand centers.

The combined effect of skill scarcity and infrastructure deficits suppresses market potential, delaying adoption of advanced stent retrievers and aspiration systems in under-resourced regions. Training and certification programs require considerable time and financial commitment, while facility modernization is capital-intensive. Until workforce density and hybrid suite availability improve, procedural volumes and device penetration remain constrained. This structural challenge continues to moderate market growth and reinforce regional disparities in neurothrombectomy access across Europe.

Opportunity Analysis – Expansion of Ambulatory Surgical Centers

The European neurothrombectomy devices market presents structured opportunities from the growth of ambulatory surgical centers, which are increasingly equipped to manage stroke interventions. Policy reforms and targeted recovery fund allocations across key EU countries are enabling same-day discharge protocols, expanding procedural feasibility in low-volume outpatient settings.

Modular and compact device platforms allow these centers to perform thrombectomy procedures without the infrastructure intensity of traditional hospitals. This creates new adoption pathways for stent retrievers, aspiration systems, and supporting catheters, particularly in regions previously constrained by hospital capacity or operational throughput.

The shift toward outpatient care strengthens procedural accessibility while diversifying end-user segments beyond major hospitals. By reducing dependence on centralized neurointerventional hubs, ASCs facilitate faster intervention for eligible patients and optimize resource utilization. Integration of compact thrombectomy systems within ASC workflows enhances patient throughput and operational efficiency. Consequently, ASC expansion represents a significant structural opportunity for device manufacturers to capture incremental demand in underpenetrated European markets, supporting broader adoption of advanced neurothrombectomy solutions.

AI-Integrated Thrombectomy Systems

The European neurothrombectomy devices market is being structurally enhanced by AI integration for clot detection and workflow optimization. CE-marked platforms analyze imaging in real-time, increasing patient eligibility by identifying previously undetectable occlusions and streamlining interventional decision-making. This technology reduces treatment delays, allowing more patients to access timely mechanical thrombectomy procedures. Integration with existing imaging infrastructure at high-volume centers enables scalable adoption across hub-and-spoke hospital networks, optimizing device utilization and procedural throughput.

Partnerships between AI platform providers and imaging device manufacturers facilitate bundled solutions that combine advanced software with stent retrievers and aspiration systems. These collaborations support standardized workflows, enhance clinical accuracy, and improve operational efficiency across European neurointerventional networks. Early pilot programs demonstrate increased procedural volumes and structural revenue growth potential, highlighting the significance of AI-enabled thrombectomy systems as a market expansion lever. Adoption of these technologies positions hospitals to capture previously untreatable cases while reinforcing device demand across the continent.

Category–wise Analysis

Product Insights

Stent retrievers are anticipated to lead, accounting for approximately 47% share in 2026, underpinned by their entrenched role as the clinical gold standard across major hospital networks in the U.K., France, and Germany. Adoption is anchored by high first-pass recanalization rates, procedural reliability, and flexibility in treating complex thrombi, with providers prioritizing workflow integration and operational efficiency in high-volume stroke centers. Continuous design evolution, including segmented stent structures and hydrophilic coatings, reinforces usage intensity and replacement cycles.

AI-assisted imaging platforms, such as Viz.ai and RapidAI, further enhance patient identification and procedure planning, expanding retriever deployment. Leading brands like Medtronic (Solitaire X), Stryker (Trevo NXT), and Cerenovus (J&J) maintain strong portfolio ecosystems, locking in enterprise workflows. This combination of mature technology, clinical trust, and integrated device suites sustains the segment’s dominance in structured neurointerventional settings.

Aspiration/Suction devices are expected to be the fastest-growing segment, driven by emerging procedural speed requirements and limitations of traditional mechanical retrieval in distal or large-clot scenarios. Growth is catalyzed by advanced large-bore catheter designs and the adoption of the ADAPT technique, which improves clot debulking efficiency while reducing distal embolization risk. Accelerating adoption is supported by AI-guided catheter navigation, automated vacuum pump systems, and modular platforms that lower operational friction for first-time users.

Leading manufacturers, including Penumbra, Stryker, and Medtronic, are expanding product lines with high-trackability catheters and hybrid suction-retriever systems to capture early-cycle demand. As clinical validation, workflow integration, and procedural standardization improve, aspiration devices are positioned to outpace the overall market.

End-user Insights

Hospitals are anticipated to dominate, accounting for approximately 71% share, underpinned by their entrenched role as the primary care setting for complex stroke interventions across major EU healthcare systems. Adoption is anchored by comprehensive stroke centers equipped with biplane angiography suites, intensive care units, and 24/7 neurointerventional teams, with providers prioritizing high procedural volume, guideline compliance, and operational efficiency. AI-assisted platforms such as Viz.ai and RapidAI optimize LVO detection and door-to-puncture times, reinforcing hospital reliance on stent retrievers and aspiration systems. Leading brands, including Medtronic (Solitaire), Stryker (Trevo), and Penumbra (Indigo/Lightning), integrate devices within hospital workflows, strengthening ecosystem lock-in.

Expansion of hub-and-spoke networks, hybrid operating rooms, and value-based procurement models sustains hospitals’ dominance, ensuring they retain primary responsibility for acute mechanical thrombectomy interventions across Europe.

Ambulatory surgical centers (ASCs) are expected to be the fastest-growing segment, driven by emerging outpatient procedural needs and cost-efficiency imperatives. Growth is catalyzed by miniaturized imaging platforms, radial-access protocols, and vascular closure devices that allow safe, same-day interventions without the infrastructure intensity of traditional hospitals. Accelerating adoption is supported by AI-assisted patient triage, subscription-based device management, and remote proctoring technologies, lowering operational friction for first-time users.

Leading manufacturers, including Penumbra, Stryker, and MicroVention, are providing modular aspiration-focused platforms optimized for low-volume sites. As ISO 13485 certification, outpatient-specific reimbursement pathways, and procedural standardization improve, ASCs are positioned to outpace overall market growth, enabling broader access to neurothrombectomy in cost-conscious and urban European settings.

Country Insights

Germany Neurothrombectomy Devices Market Trends

Germany is expected to lead, accounting for approximately 33% of total European revenue in 2026, supported by a dense network of certified stroke units, advanced reimbursement frameworks, and integrated digital health initiatives. Core demand is anchored in Germany, France, and the U.K., with Germany maintaining structural dominance through high procedure volumes, widespread hospital adoption of mechanical thrombectomy, and early integration of AI-assisted stroke triage platforms.

The industrial ecosystem is characterized by concentrated vendor presence, including Medtronic, Stryker, Acandis, and Phenox, whose comprehensive device portfolios reinforce hospital workflow lock-in. Germany to reinforce Europe’s structural dominance, creating a high-reliability ecosystem for neurovascular intervention and cross-border device distribution.

Germany is also expected to be the fastest-growing market, with projected expansion supported by a “mechanical-first” clinical shift and robust G-DRG reimbursement incentives. Widespread direct-to-Angio protocols and mobile stroke units are expected to increase device utilization, while local manufacturing expansions by Acandis and Phenox ensure rapid MDR-compliant stent retriever availability. Regulatory frameworks, including G-BA certification and TÜV-led MDR oversight, are likely to reinforce hospital compliance and quality standards.

Domestic leaders such as Acandis, Phenox, and Siemens Healthineers, alongside international players Medtronic, Stryker, and Penumbra, are expected to consolidate high-end market penetration, positioning Germany as both the growth engine and innovation reference point for European neurothrombectomy. Vendor concentration, led by Medtronic, Stryker, Acandis, and Phenox, is expected to reinforce enterprise lock-in, supporting both domestic and cross-border device supply.

Competitive Landscape

The Europe neurothrombectomy devices market is moderately consolidated, with Stryker, Medtronic, Penumbra, and Cerenovus (Johnson & Johnson) controlling the majority of market share. These leaders influence procurement strategies through extensive hospital networks, platform-level innovation, and bundled device offerings, establishing clinical and technological benchmarks across neuro-interventional suites. Competitive positioning reflects horizontal differentiation through product specialization, vertical integration in manufacturing and service support, and regional niche expertise by firms such as Acandis and Phenox, which focus on advanced stent retrievers for complex occlusions.

Industry dynamics are shaped by incremental M&A activity, platform evolution integrating aspiration and stent systems, and service-led adoption models that streamline hospital workflows. Forward-looking, the market is expected to continue balancing consolidation with niche innovation, as global leaders maintain platform dominance while specialized European firms reinforce competitive diversity, driving both procedural efficiency and high-end technology penetration across regional stroke centers.

Key Industry Developments:

- In February 2026, Vesalio secured CE-Mark for the NeVa 3.0 mm Thrombectomy System and NeVa VS vasospasm device. This enables clinicians to treat smaller vessels and complex vasospasms with higher precision, significantly expanding the treatable patient pool for acute ischemic stroke.

- In December 2025, Penumbra Inc. secured CE-Mark approvals for the next-generation Lightning Bolt 12 and Lightning Bolt 6X with TraX devices. Features modulated aspiration technology that significantly increases the speed of clot removal while reducing potential blood loss during the procedure.

- In June 2025, Terumo Neuro commercially launched the Sofia Flow 88 neurovascular aspiration catheter across EMEA markets. The Sofia Flow 88's trackability allows for deeper access into the neurovasculature, providing a more reliable platform for both aspiration and stent retriever delivery.

Companies Covered in Europe Neurothrombectomy Devices Market

- Stryker

- Medtronic

- Penumbra

- Cerenovus (Johnson & Johnson)

- MicroVention (Terumo Corporation)

- Acandis GmbH & Co. KG

- Phenox GmbH

- Boston Scientific Corporation

- Imperative Care, Inc.

- Rapid Medical Ltd.

- Vesalio

- Siemens Healthineers

- Terumo

- Balt

- Inari Medical

- Sensome

Frequently Asked Questions

The Europe neurothrombectomy devices market is projected to be valued at US$225.1 million in 2026 and is expected to reach US$312.6 million by 2033, driven by increased adoption of mechanical thrombectomy, expansion of specialized stroke centers, and integration of AI-enabled triage systems that reduce door-to-puncture times.

AI-assisted imaging platforms, including Viz.ai and RapidAI, accelerate the identification of large vessel occlusions and streamline procedural decision-making, enabling hospitals to treat more patients efficiently. Integration with hub-and-spoke networks and tele-thrombectomy guidance improves workflow, increases first-pass recanalization rates, and enhances operational throughput across high-volume stroke centers.

The Europe neurothrombectomy devices market is forecast to grow at a CAGR of 4.8% from 2026 to 2033, reflecting expanding procedural eligibility windows, increased device adoption, and optimized hospital workflows across the region.

Germany is expected to lead, accounting for approximately 33% of total European revenue in 2026, supported by a dense network of certified stroke units, high procedural volumes, MDR-compliant local manufacturing, and robust G-DRG reimbursement frameworks.

The Europe neurothrombectomy devices market is moderately consolidated, with leading players, including Medtronic, Stryker, Penumbra, and Cerenovus (Johnson & Johnson). Specialized European firms such as Acandis and Phenox provide niche, high-precision stent retrievers, reinforcing competitive diversity and supporting advanced neurointerventional workflows.