- Automotive Components & Materials

- Electronic Ignition Module Market

Electronic Ignition Module Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Electronic Ignition Module Market by Technology (Conventional Ignition Modules, Distributor-Based Ignition Modules, Capacitor Discharge Ignition, Inductive Discharge Ignition), Vehicle Type (Passenger Cars, Two-Wheelers, Commercial Vehicles, Others), Sales Channel (Original Equipment Manufacturer (OEM), Aftermarket), and Regional Analysis for 2026-2033

Electronic Ignition Module Market Share and Trends Analysis

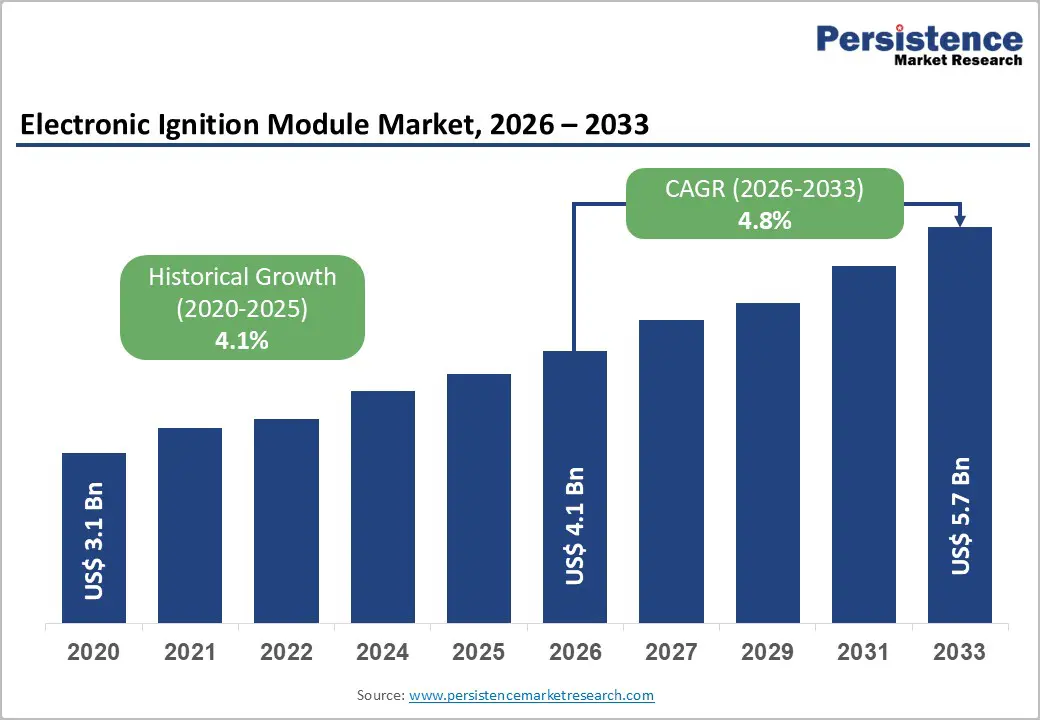

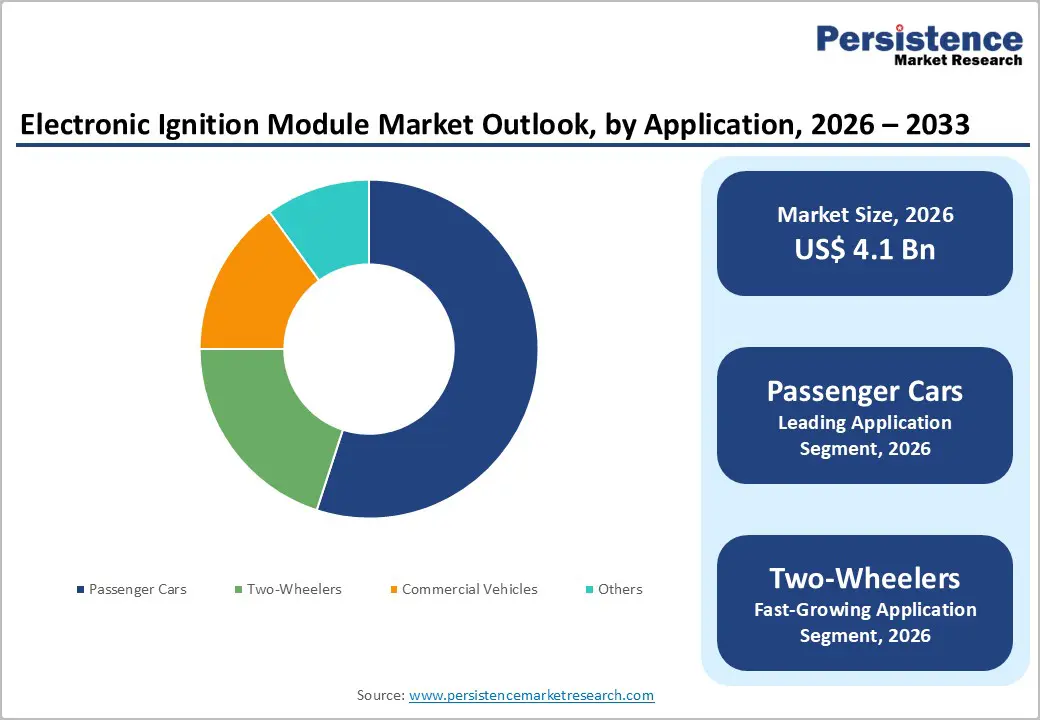

The global electronic ignition module market size is likely to be valued at US$ 4.1 billion in 2026, and is projected to reach US$ 5.7 billion by 2033, growing at a CAGR of 4.8% during the forecast period 2026−2033. The market demonstrates steady expansion driven by rising vehicle electrification, tightening emission regulations, and increasing demand for fuel-efficient ignition systems. Growth is further supported by advancements in semiconductor-based ignition technologies and the sustained production of internal combustion engine (ICE) vehicles in emerging economies. Replacement demand in aging vehicle fleets also contributes to consistent aftermarket revenues.

Key Industry Highlights

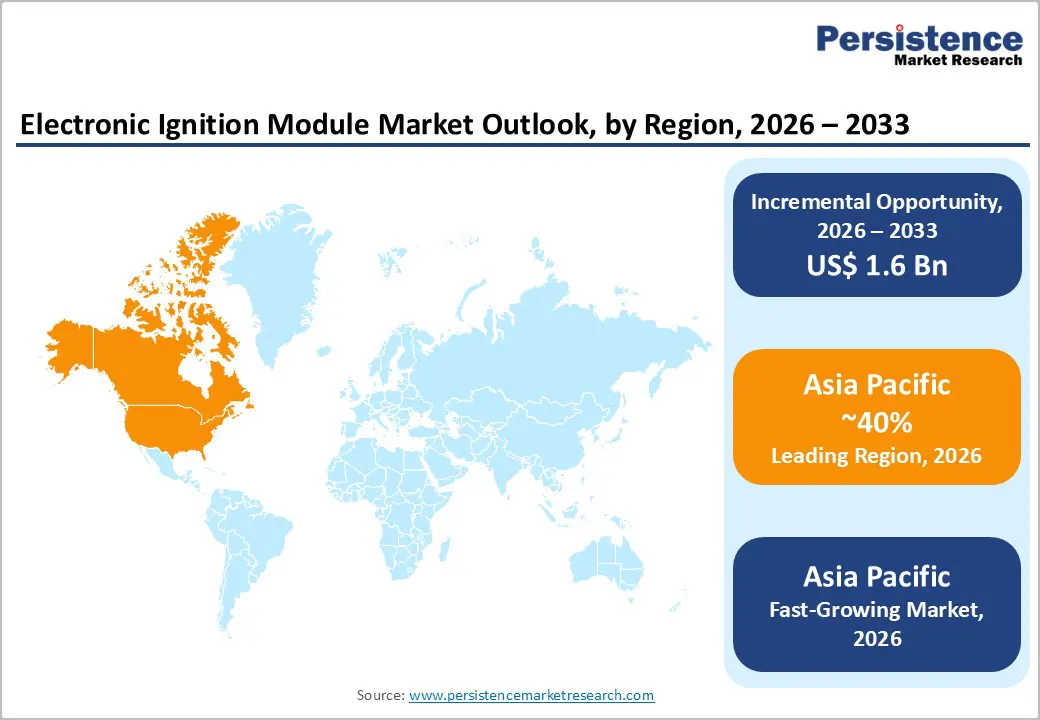

- Regional Dominance: Asia Pacific is likely to be both the dominant and fastest-growing regional market through 2033, accounting for approximately 40% share in 2026, supported by strong automotive production across key economies.

- Leading & Fastest-growing Technology: Inductive discharge ignition (IDI) is set to dominate with approximately 60% revenue share in 2026, while capacitive discharge ignition (CDI) is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing Vehicle Type: Passenger cars represent the dominant segment, capturing approximately 55% of market revenue share in 2026, two-wheelers are expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Market Trends: Electronic ignition modules (EIMs) are evolving toward higher efficiency, compact designs, and smart integration, driven by stricter emission regulations and the need for improved fuel economy.

| Key Insights | Details |

|---|---|

| Electronic Ignition Module Market Size (2026E) | US$4.1 Bn |

| Market Value Forecast (2033F) | US$5.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

DRO Analysis

Rising Stringency in Emission Regulations and Fuel Efficiency Standards

Regulatory bodies across major automotive markets are strengthening emission compliance requirements, and this shift is continuously shaping ignition system performance standards. Authorities such as the United States Environmental Protection Agency (EPA) and the European Environment Agency (EEA) are enforcing stricter limits on nitrogen oxide (NOx) and carbon emissions, which is pushing manufacturers to refine combustion processes. Electronic ignition modules are playing a central role in this transition, as they are enabling more accurate spark timing and controlled fuel combustion. Improved combustion efficiency is reducing unburnt fuel output and supporting cleaner engine operation. Original equipment manufacturers are increasingly integrating these systems into gasoline engines to align with evolving environmental mandates and maintain regulatory approval across multiple regions.

Developing economies are also reinforcing compliance frameworks, and countries such as India and China are implementing advanced emission standards including Bharat Stage VI (BS VI) and China VI regulations. These policy shifts are encouraging manufacturers to upgrade ignition technologies across mid-range and mass-market vehicles. Electronic ignition modules are helping automakers meet compliance targets without compromising engine reliability or drivability. The ongoing transition is also creating a more uniform regulatory environment, which will have been simplifying product standardization for global manufacturers. Industry participants are therefore prioritizing ignition system innovation to ensure long-term compliance readiness and sustained market competitiveness.

Technological Advancements in Ignition Systems

Rapid progress in microelectronics is redefining the role of ignition modules, and manufacturers are embedding advanced sensing capabilities to improve engine control. These systems are continuously monitoring parameters such as engine speed, load conditions, and temperature, which is allowing precise adjustment of ignition timing. Components such as insulated-gate bipolar transistors (IGBTs) and metal-oxide-semiconductor field-effect transistors (MOSFETs) are enhancing switching performance and energy efficiency. This technological shift is reducing energy losses during ignition while maintaining consistent spark delivery. Engineers are also focusing on durability improvements, and newer module designs are resisting heat and vibration more effectively, which is extending component lifespan and ensuring stable engine operation under varying conditions.

Integration with engine control units (ECUs) is further strengthening the functionality of electronic ignition systems. These connected systems are enabling real-time diagnostics, allowing vehicles to detect irregularities and adjust performance parameters instantly. Predictive maintenance capabilities are also emerging, as ignition modules are continuously generating operational data that will have been used to identify potential failures before they occur. This approach is reducing downtime and improving overall vehicle reliability. Automakers are increasingly adopting these intelligent systems to enhance user experience and meet evolving performance expectations. The ongoing convergence of electronics and mechanical systems is shaping a more responsive and efficient ignition ecosystem.

Shift toward Electric Vehicles Reducing Long-Term Demand

The automotive industry is undergoing a structural transition, and battery electric vehicles (BEVs) are steadily reducing the relevance of conventional ignition systems. These vehicles are operating without internal combustion engines, which means they are not requiring spark generation or ignition timing components. Automakers are actively expanding electric vehicle portfolios to align with environmental goals and regulatory expectations. This shift is gradually decreasing dependence on traditional engine technologies, especially in passenger vehicle segments. Manufacturers of ignition modules are therefore facing a changing demand landscape, as product relevance is becoming closely tied to the pace of electrification across key markets.

Market dynamics are evolving more rapidly in developed regions, where electric vehicle adoption is accelerating due to supportive policies, charging infrastructure expansion, and consumer awareness. Original equipment manufacturers are reallocating investments toward electric powertrains, which will have been limiting future production volumes of internal combustion engine vehicles. This transition is creating long-term uncertainty for ignition module suppliers, particularly those heavily dependent on original equipment demand. Companies are increasingly evaluating diversification strategies, including hybrid vehicle components and electronic system integration, to remain competitive. The industry is adjusting to a scenario where ignition technologies are serving a shrinking but still necessary segment of the global vehicle fleet.

Volatility in Semiconductor Supply Chains

Electronic ignition modules are depending heavily on semiconductor components, and this dependence is increasing exposure to supply chain disruptions. These modules are using integrated circuits and power devices to control ignition timing and energy delivery, which is making semiconductor availability a critical factor in production continuity. The COVID-19 pandemic offered such a lesson in the semiconductor supply chain’s fragilities. As the coronavirus spread and triggered a spike in consumer spending, the demand for semiconductors surged. But sweeping lockdowns in Asia and Europe in 2020 and 2021 caused significant labor shortages that left fabs, assembly sites, and other chip facilities severely understaffed or forced to halt production altogether.

Geopolitical developments and resource limitations are continuing to influence semiconductor supply dynamics. Trade restrictions, regional conflicts, and concentration of chip manufacturing in specific countries are creating vulnerabilities in the supply chain. Raw material dependencies, particularly for silicon and rare elements used in chip fabrication, are adding another layer of risk. Automotive suppliers are responding by diversifying sourcing strategies and strengthening relationships with semiconductor producers. Some companies are also increasing inventory buffers and exploring localized manufacturing options to reduce dependency on external markets. These adjustments will have been improving supply resilience, yet cost pressures and lead time variability are likely to remain ongoing challenges.

Expansion of Automotive Aftermarket Services

Vehicle fleets across North America and Europe are aging steadily, and this trend is increasing the need for replacement of critical engine components. Older vehicles are experiencing higher wear in ignition systems, which is driving consistent demand for electronic ignition modules in the aftermarket. Owners are prioritizing maintenance to extend vehicle life, especially in regions where replacement cycles are lengthening. Service centers and independent repair networks are responding by stocking a wider range of compatible ignition components. This pattern is strengthening the aftermarket ecosystem, as demand is becoming more predictable and less dependent on new vehicle sales cycles.

Aftermarket sales channels are gaining strategic importance because they are offering better margins compared to original equipment manufacturer (OEM) supply. Suppliers are focusing on branding, product reliability, and distribution reach to capture customer loyalty in this segment. Digital transformation is also playing a significant role, as e-commerce platforms are expanding access to automotive parts for both consumers and repair professionals. Online marketplaces are simplifying product comparison and availability, which is improving purchasing efficiency. Manufacturers are increasingly investing in digital catalogs and logistics networks, and these efforts will have been enhancing market penetration while supporting faster delivery and improved customer experience.

Growth in Hybrid Vehicle Segment

Hybrid electric vehicles (HEVs) are continuing to depend on internal combustion engines, which is sustaining the need for advanced ignition systems. These vehicles are combining electric propulsion with conventional engines, and this configuration is requiring precise ignition control to ensure smooth transitions between power sources. Electronic ignition modules are playing a critical role in managing combustion timing under varying operating conditions. Manufacturers are focusing on improving accuracy and responsiveness, as hybrid systems are demanding higher performance compared to traditional engine setups. This ongoing shift is positioning ignition modules as essential components in hybrid powertrains rather than legacy technologies.

Design requirements for hybrid applications are becoming more demanding, and ignition modules are evolving to meet these expectations. Systems are being engineered to handle frequent engine start and stop cycles, which is increasing stress on ignition components. Enhanced durability and thermal resistance are therefore becoming key priorities for suppliers. Companies are also developing premium-grade modules with improved reliability and longer service life, which is supporting higher-value product offerings. This transition is creating opportunities for manufacturers to move toward specialized solutions tailored for hybrid platforms. Industry participants are aligning product development strategies with hybrid vehicle growth, and these efforts will have been strengthening revenue potential in this segment.

Category-wise Analysis

Technology Insights

IDI is poised to dominate by commanding approximately 60% of the electronic ignition module market revenue share in 2026. Strong adoption of IDI systems is being driven by their cost efficiency, operational reliability, and seamless integration with high-volume vehicle platforms. These systems are widely used in entry-level passenger cars and two-wheelers, where buyers are prioritizing affordability and dependable performance. Manufacturers are favoring IDI technology because it supports stable ignition without requiring complex architecture. Maintenance requirements are also remaining relatively low, which is appealing to cost-sensitive markets. Demand in emerging economies is continuing to rise, as IDI systems are aligning well with the need for durable and economical automotive components.

Capacitive discharge ignition is likely to be the fastest-growing segment during the 2026-2033 forecast period. The systems are delivering stronger spark output and more consistent ignition at elevated engine speeds, which is enhancing overall engine responsiveness. These characteristics are making CDI technology well suited for performance-oriented vehicles and motorcycles that operate under demanding conditions. Automakers are increasingly adopting these systems to achieve better combustion efficiency and improved throttle response. Regulatory pressure on emission control is also encouraging the shift toward advanced ignition solutions. Demand is rising across developed markets, where premium vehicle segments are prioritizing performance, efficiency, and compliance with evolving environmental standards.

Vehicle Type Insights

Passenger cars are expected to capture nearly 55% of the electronic ignition module market share in 2026. Large-scale vehicle production across Asia Pacific is sustaining strong demand for ignition modules, particularly within high-volume passenger car segments. Manufacturers are continuously supplying ignition components to support ongoing assembly requirements in key automotive hubs. Replacement demand is also remaining steady, as widespread vehicle ownership and extended usage cycles are increasing the need for periodic component maintenance. Consumers are holding vehicles for longer durations, which is reinforcing aftermarket demand. Compact and mid-size gasoline-powered cars are continuing to dominate this segment, as they are balancing affordability, fuel efficiency, and practicality for a broad customer base.Top of FormBottom of Form

Two-wheelers are expected to be the fastest-growing segment over the 2026-2033 forecast period. Motorcycles, scooters, and mopeds are increasingly integrating electronic ignition systems, and this shift is supporting steady segment expansion. Urban mobility patterns are favoring two-wheelers, as consumers are choosing them for cost efficiency, fuel savings, and easier navigation in congested areas. Manufacturers are responding to evolving preferences by equipping vehicles with more advanced technologies, including precise ignition control systems. Demand is also rising for models that deliver improved performance and reduced emissions. Growth in hybrid and electrically assisted two-wheelers is further encouraging the adoption of more sophisticated ignition solutions across this segment.

Regional Insights

North America Electronic Ignition Module Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for electronic ignition modules in 2026, accounting for approximately 40% of the market share, supported by strong automotive production across key economies. Countries such as China, Japan, India, and members of the ASEAN are contributing significantly to regional demand. China is maintaining leadership due to its extensive manufacturing ecosystem and well-established supplier networks. India is experiencing accelerated growth, driven by rising vehicle ownership and the implementation of BS VI emission standards. Japan is continuing to lead in technological innovation, particularly in hybrid vehicle development and advanced automotive electronics. These factors are collectively strengthening the region’s influence in the global supply chain.

Competitive advantages in Asia Pacific are emerging from cost-effective manufacturing and increasing localization of production. Automotive companies are investing in regional facilities to optimize costs and reduce dependency on imports. Supply chain efficiency is improving as manufacturers are building closer relationships with component suppliers and logistics partners. Urban expansion and income growth are encouraging higher vehicle adoption, which is sustaining long-term demand for ignition systems. Governments are also supporting industrial development through policy incentives and infrastructure improvements. These developments are creating a stable environment for continued investment and capacity expansion across the automotive components sector.

Europe Electronic Ignition Module Market Trends

Europe is maintaining a strong position in the market, reinforced by well-established automotive industries across key countries such as Germany, the United Kingdom, France, and Spain. Regulatory frameworks are playing a central role in shaping market direction, as emission standards under Euro 6 and the upcoming Euro 7 regulations are becoming increasingly stringent. These policies are requiring automakers to enhance engine efficiency and reduce environmental impact, which is encouraging the adoption of advanced ignition technologies. Germany is continuing to lead in automotive manufacturing and engineering innovation, while other major economies are strengthening their focus on component replacement and service-driven demand.

A unified regulatory structure across the European Union (EU) is ensuring consistent compliance requirements, which is simplifying product development and market entry for manufacturers. Investment activity is increasingly targeting hybrid vehicle technologies, as these platforms are still depending on internal combustion engines supported by efficient ignition systems. Suppliers are concentrating on improving system integration and operational efficiency to meet evolving technical standards. Competitive pressure is intensifying, as established companies are advancing product capabilities and optimizing performance to retain market share. These developments are reinforcing Europe’s position as a technologically driven and regulation-focused automotive components market.

North America Electronic Ignition Module Market Trends

North America is maintaining a significant position in the global market, with the United States acting as the primary contributor to regional demand. A large base of aging vehicles is increasing the need for replacement components, which is strengthening aftermarket sales for ignition modules. Vehicle owners are continuing to invest in maintenance to extend usage cycles, and this trend is supporting consistent demand across service networks. Regulatory authorities such as the U.S. EPA are enforcing strict emission and fuel efficiency standards. These requirements are encouraging automakers to adopt more advanced ignition systems that can improve combustion control and reduce environmental impact.

Technology development is becoming a key area of focus, as manufacturers are integrating ignition modules with vehicle diagnostics and control systems. Smart ignition solutions are enabling real-time monitoring and performance optimization, which is enhancing overall engine efficiency. Hybrid vehicle adoption is also expanding, and these vehicles are still relying on internal combustion engines supported by high-performance ignition components. Investment activity is increasingly targeting semiconductor manufacturing and localized supply chains to improve production stability. Companies are strengthening sourcing strategies and building resilience against potential disruptions, which will have been supporting long-term operational efficiency and market competitiveness.

Competitive Landscape

The global electronic ignition module market structure is moderately consolidated, dominated by leading players such as Robert Bosch, Denso Corporation, Delphi Technologies, Hitachi Astemo, and NGK Spark Plug. These players collectively capture 35-40% of the market share. Leading companies are strengthening their market position by relying on advanced engineering capabilities, extensive global distribution networks, and long-standing partnerships with OEMs. These firms are continuously investing in product development and system integration to meet evolving industry requirements. Their established relationships with automakers are ensuring consistent demand and stable revenue streams. Regional players are adopting a different approach, as they are focusing on cost competitiveness and localized production strategies. This positioning is allowing them to serve price-sensitive markets effectively, especially in emerging economies where affordability and supply flexibility are influencing purchasing decisions.

Key Industry Developments

- In November 2025, Pavna Industries established a new R&D center in Noida focused on electronic components, lock systems, and advanced automotive solutions to strengthen product development and engineering capabilities. The facility aims to accelerate innovation, improve efficiency, and enhance value delivery to OEM customers.

- In September 2025, Inductive Automation launched Ignition 8.3 LTS, an upgraded industrial platform for SCADA, IIoT, MES, and HMI applications, emphasizing enhanced data efficiency, security, and scalability to bridge OT and IT demands.

Companies Covered in Electronic Ignition Module Market

- Robert Bosch GmbH

- Denso Corporation

- Delphi Technologies

- Hitachi Astemo Ltd.

- NGK Spark Plug Co., Ltd.

- Mitsubishi Electric Corporation

- Continental AG

- Standard Motor Products, Inc.

- Walker Products Inc.

- Diamond Electric Mfg. Co., Ltd.

- Valeo SA

- HELLA GmbH & Co. KGaA

- AC Delco

- Magneti Marelli

Frequently Asked Questions

The global electronic ignition module market is projected to reach US$ 4.1 billion in 2026.

The market is driven by stringent emission regulations and rising demand for fuel-efficient ignition systems in advanced vehicles.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Major opportunities lie in expansion in emerging markets such as Asia Pacific and aftermarket upgrades for high-performance vehicles.

Robert Bosch GmbH, Denso Corporation, Delphi Technologies, Hitachi Astemo Ltd., and NGK Spark Plug Co., Ltd. are some of the key players in the market.