- Processed Food

- Egg White Substitute Market

Egg White Substitute Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Egg White Substitute Market by Source (Plant-based proteins Starch, Hydrocolloids, Others), Form (Powder, Liquid), End-user (Bakery & Confectionery, Sauces & dressings, Plant-based meat & Seafood, Ready Meals & Convenience Foods), and Regional Analysis, 2026 - 2033

Egg White Substitute Market Share and Trends Analysis

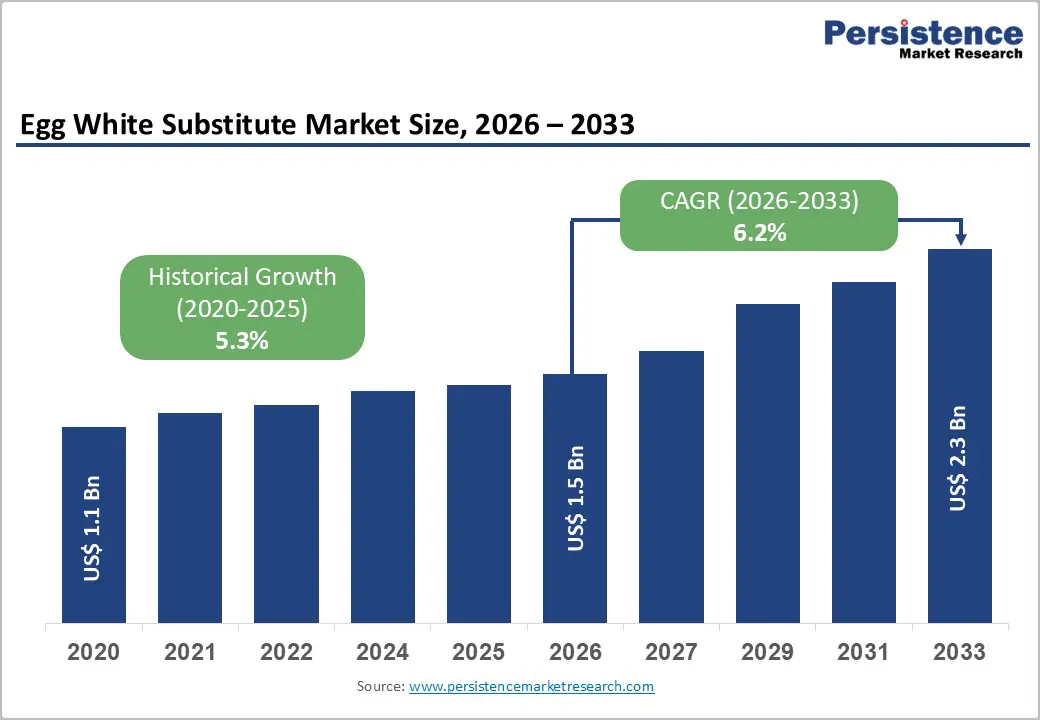

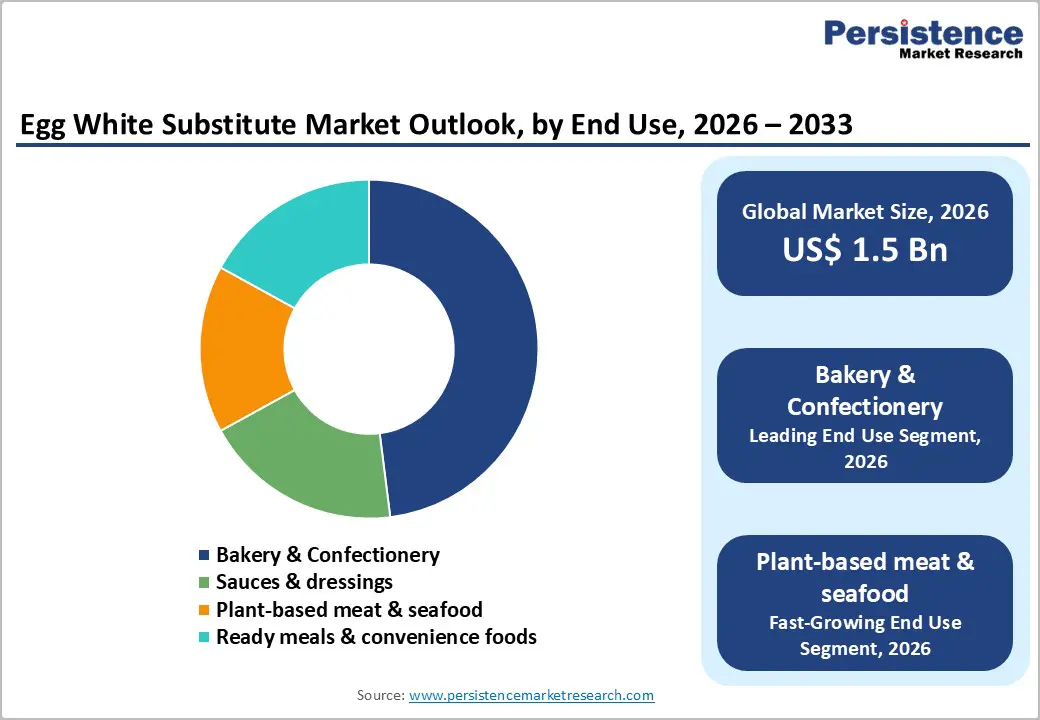

The global egg white substitute market size is expected to be valued at US$ 1.5 billion in 2026 and projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The growth is underpinned by rising vegan, vegetarian, and flexitarian populations, along with increasing concerns about egg allergies, cholesterol, and animal-welfare issues. Food manufacturers are turning to plant-derived and functional ingredient systems that can replicate egg whites’ foaming, gelling, and binding properties in bakery, sauces, and meat analogues while delivering more stable pricing and longer shelf life than shell eggs or liquid whites.

Key Industry Highlights:

- Fastest-Growing Region: Asia Pacific, driven by rapid expansion of modern bakery, convenience foods, urban vegan and flexitarian diets, and strong regional capabilities in plant protein and starch processing.

- Dominant Form Segment: Powdered egg white substitutes, holding nearly 70% share, favored for shelf stability, ambient storage, formulation flexibility, and cost-efficient scalability across bakery, snacks, and instant foods.

- Fastest-Growing End-Use Segment: Plant-based meat and seafood, expanding at around 8.2% CAGR, as manufacturers seek egg-free binders that deliver gel strength, juiciness, and bite in burgers, nuggets, and seafood analogues.

- Market Drivers: Rising plant-based diets combined with widespread egg allergen management needs are accelerating reformulation across bakery, ready meals, and protein foods without compromising texture or performance.

- Key Opportunities: Development of advanced, clean-label binding and gelling systems for plant-based meat and seafood, enabling large-scale substitution of eggs while maintaining sensory quality and processing reliability.

- Key Developments: In September 2025, Meala introduced Groundbaker, a single-ingredient pea protein designed to replicate egg functionality in baked goods. In May 2025, BENEO validated fava bean protein as an effective egg substitute in muffin formulations, supporting clean-label bakery innovation.

| Key Insights | Details |

|---|---|

| Global Egg White Substitute Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Dynamics

Driver - Surge in Plant-Based Diets and Egg Allergy Management

One of the strongest growth drivers is the global rise in plant-forward eating patterns and the need to manage egg allergies without compromising product quality. Surveys from organizations such as the International Food Information Council (IFIC) show that more than one-third of U.S. consumers report actively seeking plant-based options, while egg is among the top eight allergens identified by the U.S. Food and Drug Administration (FDA).

This convergence pushes manufacturers to reformulate bakery, confectionery, and ready meals with egg white substitutes that deliver comparable aeration, structure, and moisture retention. Ingredient houses like Ingredion, Cargill, Incorporated, and Kerry Group plc are developing pea, fava bean, and wheat-based protein systems that can whip, foam, and gel similar to egg whites, enabling brands to label products as vegan or egg-free and reach a wider consumer base that includes vegans, vegetarians, and allergy sufferers.

Restraints - Higher Formulation Complexity and Cost for Advanced Systems

A key restraint lies in the higher formulation complexity and cost of advanced egg white substitutes. While simple starch- or gum-based solutions remain relatively affordable, they often fall short in delivering the full functional performance needed for demanding bakery applications. As a result, formulators rely on multi-component systems combining specialty proteins, fibers, and emulsifiers to achieve comparable structure, aeration, and stability. These blends are typically more expensive per kilogram than conventional egg whites and require precise technical integration to avoid disruptions in mixing times, baking profiles, or pH balance. Smaller bakeries and regional manufacturers frequently lack in-house R&D capabilities to optimize such formulations, which slows adoption and limits penetration across fragmented markets.

Opportunity - Advanced Systems for Plant-Based Meat and Seafood

A strong opportunity is emerging in the development of advanced egg-free binding and gelling systems tailored for plant-based meat and seafood applications. Egg whites have traditionally delivered structure, gel strength, and juiciness in products such as surimi, fish balls, sausages, and patties, setting a high functional benchmark. As plant-based burgers, nuggets, vegan fish fillets, and deli slices scale commercially, manufacturers require alternatives that can replicate these performance attributes using non-animal ingredients while maintaining clean-label positioning.

Suppliers are responding by engineering synergistic blends of plant proteins, fibers, and hydrocolloids that deliver egg-like bite, cohesion, and water-holding capacity. These systems support consistent processing and sensory quality at scale. Companies offering application-specific, label-friendly solutions can capture significant value as plant-based meat and seafood adoption continues to accelerate globally.

Category-wise Analysis

By Form, powder dominates the global market

By form, powder is projected to remain the dominant format in the egg white substitute market, accounting for an estimated around 70% share in 2025. Powdered substitutes offer strong advantages in shelf stability, logistics efficiency, and formulation flexibility. They can be stored and transported at ambient conditions, easily rehydrated during processing, and seamlessly incorporated into dry mixes for bakery, snacks, and instant food applications. This significantly reduces dependence on cold-chain infrastructure and lowers contamination and spoilage risks compared with liquid egg alternatives.

From a manufacturing perspective, powdered egg white substitutes enable consistent batch-to-batch performance and simplified inventory management. Systems based on plant proteins, starches, and hydrocolloids provide reliable foaming, binding, and emulsification across applications. While liquid formats are expanding in foodservice and ready-to-use vegan egg products, the cost efficiency, scalability, and operational convenience of powders are expected to sustain their market leadership over the forecast period.

By End-user, plant-based meat and seafood are expected to show promising growth during the forecast period

By end-user, bakery & confectionery emerges as the dominant application, accounting for an estimated 46% share of the egg white substitute market in 2025. Egg whites have traditionally played a critical role in baked goods such as cakes, muffins, meringues, cookies, and pastries by providing aeration, structure, and volume. As demand for vegan and egg-free bakery products accelerates, manufacturers and artisanal bakers are turning to functional alternatives that preserve softness, lift, and crumb integrity. Blends of plant proteins, starches, and hydrocolloids are increasingly adopted to deliver consistent performance while supporting clean, plant-based product positioning.

Beyond bakery, plant-based meat and seafood represent the fastest-expanding end-use segment, with growth projected at around 8.2% CAGR between 2025 and 2032. Producers of vegan burgers, sausages, nuggets, and seafood analogues require high-performance binders that replicate the gel strength and water-holding capacity of egg whites. Advanced egg-free systems enable improved texture, bite, and juiciness, making them essential as plant-based protein formulations continue to evolve and scale.

Region-wise Insights

North America Egg White Substitute Market Trends

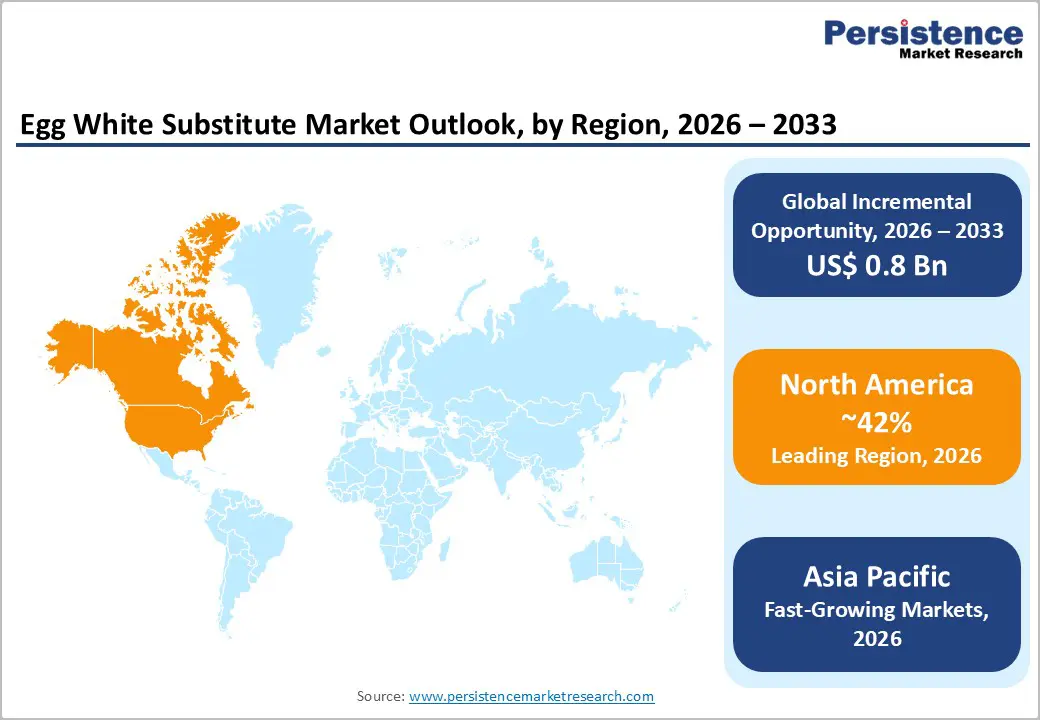

North America is currently the leading regional market, accounting for about 42% of the egg white substitute market in 2025. The United States plays a central role, driven by high per-capita egg consumption, strong penetration of processed foods, and rapid growth in plant-based alternatives. Regulatory oversight from agencies such as the FDA and USDA ensures strict labeling of allergens and nutrition information, pushing manufacturers to clearly declare egg content and motivating some to switch to egg-free systems in order to reach broader consumer groups. The region has also experienced recurrent avian influenza outbreaks, which have periodically constrained egg supply and inflated prices, encouraging bakeries, sauce manufacturers, and ready-meal producers to explore more stable substitute systems.

North America benefits from a robust innovation ecosystem featuring major ingredient companies such as Cargill, Incorporated, Ingredion, Tate & Lyle PLC, Kerry Group plc, DSM-Firmenich AG, and IFF. These players operate R&D centers that collaborate directly with CPG brands, quick-service restaurant chains, and food-tech startups to tailor egg substitute solutions for specific applications, from vegan mayonnaise to protein-rich snack cakes. The well-developed e-commerce infrastructure also supports direct-to-consumer launches of powdered vegan egg products and baking kits, further amplifying regional demand.

Asia Pacific Egg White Substitute Market Trends

Asia Pacific is projected to be the fastest-growing regional segment for egg white substitutes between 2025 and 2032, benefiting from rising incomes, rapid urbanization, and evolving dietary preferences. While traditional diets in China, Japan, India, and ASEAN countries have relied less on eggs than Western diets, modern bakery, confectionery, and ready-meal sectors have expanded quickly, increasing the use of egg-containing products. Simultaneously, a growing number of consumers are adopting flexitarian or vegan lifestyles, particularly in urban centers, increasing interest in plant-based alternatives. Governments and health authorities in several Asia Pacific markets are also promoting reductions in cholesterol and saturated fat intake, which indirectly supports interest in egg-free or plant-forward products.

On the supply side, the region benefits from strong capabilities in plant protein and starch production, with extensive processing of soy, wheat, rice, and pulses that can be leveraged to create locally sourced egg substitute systems. Companies such as Ardent Mills, Ingredion, and regional players collaborate with bakery chains, instant noodle manufacturers, and convenience food producers to design systems suitable for soft cakes, steamed buns, tempura batters, and coated snacks. The combination of manufacturing cost advantages and rising consumer interest is expected to make Asia Pacific a critical engine of future growth for the egg white substitute market.

Competitive Landscape

The egg white substitute market shows a moderately fragmented structure, shaped by the presence of both large ingredient suppliers and specialized solution developers targeting specific applications. Broad-based players compete by offering multifunctional ingredient platforms that combine plant proteins, starches, hydrocolloids, and enzymes into integrated egg replacement systems. These solutions are designed to address diverse functional needs such as foaming, binding, emulsification, and structure formation across bakery, confectionery, and plant-based foods. At the same time, smaller specialists focus on high-performance, allergen-free, and label-friendly formulations tailored for niche or premium segments.

Competitive differentiation is increasingly driven by application-level performance and technical collaboration rather than price alone. Suppliers that provide hands-on formulation support, customized blends, and consistent results in demanding recipes gain stronger customer loyalty. Clean-label positioning, transparent ingredient sourcing, and compatibility with vegan and allergen-free claims further strengthen market standing. Partnerships with bakery producers and plant-based food manufacturers are expanding, with co-development and co-branding strategies helping ingredient suppliers embed their technologies deeper into finished products.

Key Developments:

- In September 2025, Israel-based food-tech innovator Meala unveiled Groundbaker, a single-ingredient pea protein designed to replicate the multi-functional performance of eggs in baked goods, enabling cleaner labels and improved plant-based baking applications.

- In May 2025, BENEO tested fava bean protein in bakery applications, demonstrating its effectiveness as an egg substitute in muffins while supporting plant-based and clean-label formulation goals.

Companies Covered in Egg White Substitute Market

- Ingredion

- Cargill, Incorporated

- Kerry Group plc

- Tate & Lyle PLC

- DSM-Firmenich AG

- Taranis

- Ardent Mills

- IFF

- All American Foods

- Fabumin

- Meala

- BENEO

- Others

Frequently Asked Questions

The global egg white substitute market is expected to reach approximately US$ 1.5 billion in 2026, reflecting steady expansion from 2020 as manufacturers adopt plant‑based and allergen‑free solutions in bakery, sauces, and prepared foods.

A major demand driver is the rapid growth of plant‑based diets and the need to manage egg allergies, prompting food producers to replace egg whites with plant protein, starch, and hydrocolloid systems that offer similar functionality without animal ingredients.

North America currently leads the market with around 42% share in 2025, supported by strong innovation from major ingredient companies, stringent allergen labeling requirements, and periodic egg supply disruptions that encourage adoption of substitutes.

A key opportunity lies in developing clean‑label, high‑performance systems for plant‑based meat & seafood and premium bakery products, enabling brands to deliver realistic texture and volume while supporting vegan, allergen‑free, and sustainability claims.

Leading companies include Ingredion, Cargill, Incorporated, Kerry Group plc, Tate & Lyle PLC, DSM‑Firmenich AG, IFF, and BENEO, along with several regional and niche innovators.