- Executive Summary

- Global Cyclohexane Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Automotive Industry Overview

- Global Textile Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Cyclohexane Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- Market Attractiveness Analysis: Application

- Global Cyclohexane Market Outlook: End-user Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End-user Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- Market Attractiveness Analysis: End-user Industry

- Global Cyclohexane Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- Europe Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- East Asia Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by , 2026-2033

- South Asia & Oceania Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- Latin America Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- Middle East & Africa Cyclohexane Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Adipic Acid Production

- Caprolactum Production

- Other

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by End-user Industry, 2026-2033

- Chemical Manufacturing

- Textile

- Automotive

- Construction

- Paints & Coatings

- Other

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- BASF SE

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Sunoco Chemicals

- ExxonMobil Chemical

- Huntsman Coporation

- Chevron Phillips Chemical Company LLC

- Royal Dutch Shell plc

- Sinopec Group

- Koninklijke DSM N.V.,

- Reliance Industries Limited

- Dow Chemical Company

- Shell Chemicals

- BASF SE

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Bulk Chemicals

- Cyclohexane Market

Cyclohexane Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Cyclohexane Market by Application (Adipic Acid Production, Caprolactum Production, other), Industry (Chemical Manufacturing, Textile, Automotive, Construction, Paints & Coatings, Other), and Regional Analysis for 2026 - 2033

Cyclohexane Market Size and Trend Analysis

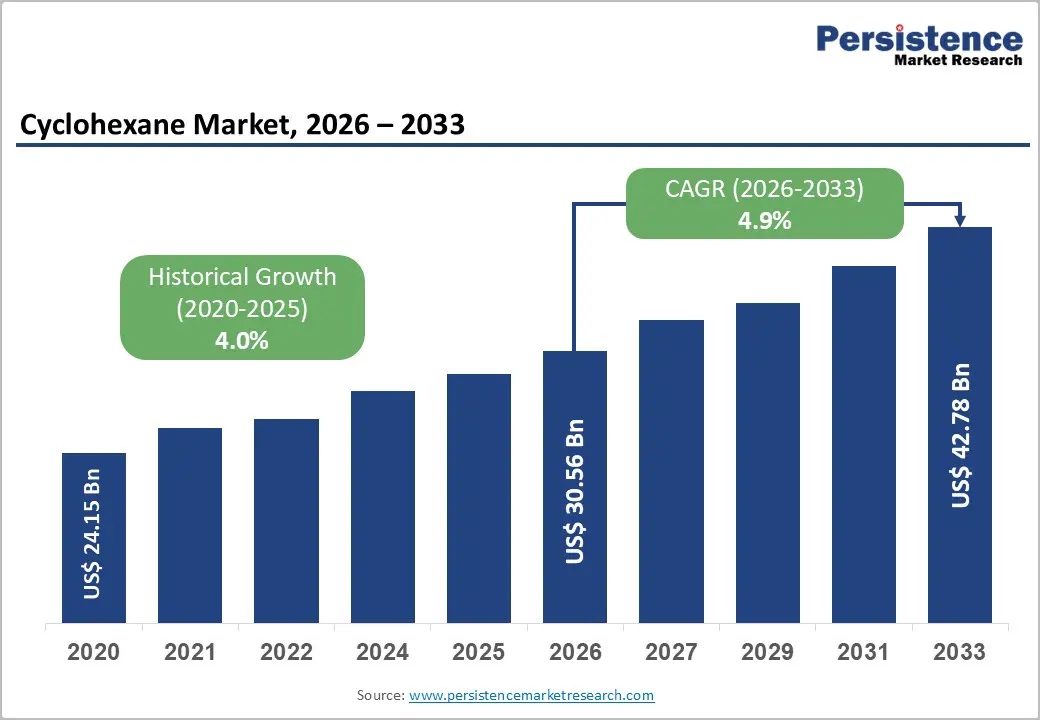

The global cyclohexane market size is supposed to be valued at US$ 30.56 billion in 2026 and is projected to reach US$ 42.78 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033. The market expansion is primarily driven by surging demand for nylon intermediates, particularly adipic acid and caprolactam, which are extensively used in automotive lightweighting initiatives and textile manufacturing.

According to the U.S. Department of Energy, a 10% reduction in vehicle weight can improve fuel economy by 6%-8%, accelerating the adoption of nylon-based engineering plastics. Additionally, the global vehicle production growth, reported at 5.6% in 2023 by the Organisation Internationale des Constructeurs d'Automobiles (OICA), reinforces cyclohexane's critical role in high-performance automotive applications, including radiator end tanks, engine covers, and air intake manifolds.

Key Industry Highlights:

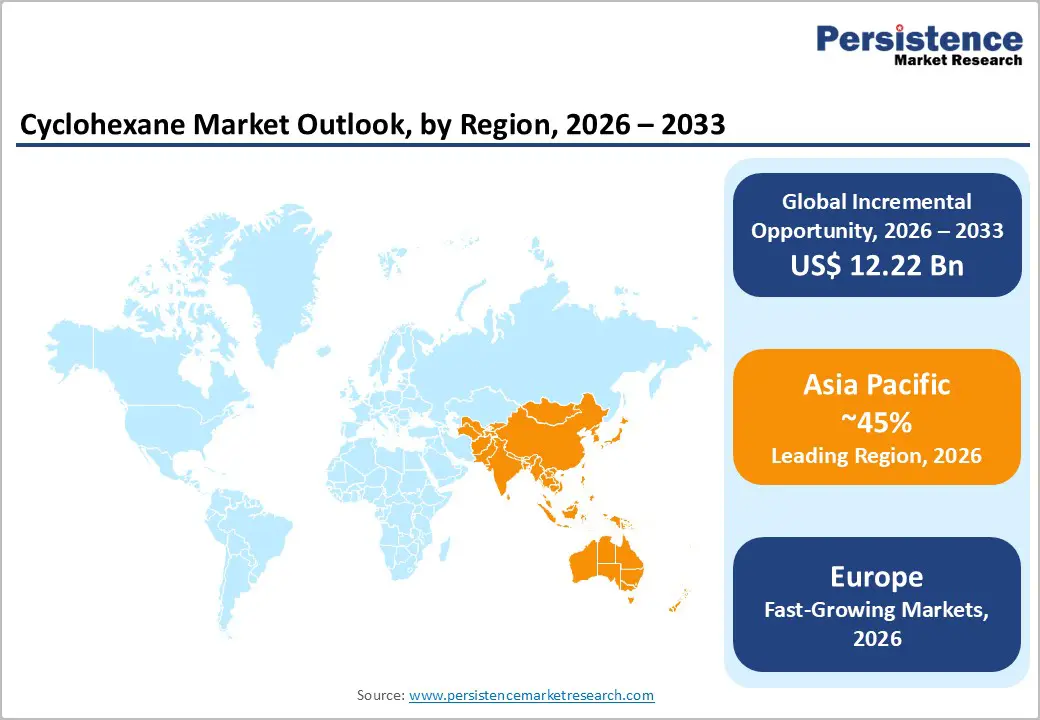

- Leading Region: Asia Pacific dominates the global cyclohexane market with approximately 45% revenue share, driven by massive nylon manufacturing concentration in China, India, and Southeast Asia supported by cost-effective production capabilities and enormous domestic textile and automotive demand growth.

- Fastest Growing Region: Europe emerges as the fastest-growing regional market during the 2026 - 2033 forecast period, driven by stringent environmental regulations promoting sustainable nylon production, technological innovations in advanced manufacturing, and strategic automotive industry investments in lightweight material adoption supporting carbon emission reduction objectives.

- Dominant Segment: Caprolactam production represents the dominant application segment commanding 43% of cyclohexane consumption, driven by extraordinary global nylon-6 fiber and resin demand across textile, automotive, and engineering plastic applications serving diverse industrial and consumer markets.

- Fastest Growing Segment: The automotive Industry segment represents the fastest-growing demand category, expanding at 6.3% CAGR throughout the forecast period as manufacturers accelerate adoption of lightweight nylon components for fuel efficiency improvement and electric vehicle thermal management requirements.

- Key Market Opportunity: Electric vehicle component manufacturing represents the highest-growth opportunity segment, with specialized nylon materials required for battery enclosures, thermal management systems, and electrical insulation applications driving incremental cyclohexane demand as global EV production accelerates toward 20+ million units annually by 2030.

| Key Insights | Details |

|---|---|

| Cyclohexane Market Size (2026E) | US$ 30.56 Bn |

| Market Value Forecast (2033F) | US$ 42.78 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 4.0% |

Market Dynamics

Drivers - Rise in Demand from the Automotive Sector for Lightweight Engineering Plastics

The automotive industry's strategic shift toward lightweight materials represents a transformative growth driver for cyclohexane consumption. Modern vehicles increasingly incorporate 15-20 kilograms of nylon-based components in engine compartments, fuel systems, air intake manifolds, electrical housings, and structural applications, where superior heat resistance and mechanical properties surpass those of traditional metal alternatives. The Lightweight Automotive Body Panels Market is projected to reach USD 197.3 billion by 2032, growing at a CAGR of 4.9%, directly amplifying cyclohexane derivative requirements.

Electric vehicle adoption creates additional demand momentum, as manufacturers specify nylon components for battery housings, thermal management systems, charging infrastructure, and electrical insulation applications that require exceptional performance characteristics. Global vehicle production rose by 5.6% in 2023, according to ACEA, with major automotive manufacturers implementing aggressive lightweighting strategies to comply with stringent fuel efficiency regulations and reduce carbon footprints.

Expanding Textile and Apparel Demand in Developing Economies

The global textile industry’s sustained expansion, particularly in technical textiles and high-performance fabrics, is a key driver of cyclohexane demand. Nylon-6 fibers, derived from caprolactam, offer superior tensile strength, abrasion resistance, moisture-wicking properties, and durability, making them essential for sportswear, industrial textiles, tire cord reinforcement, carpets, and functional apparel. Technical textiles are increasingly utilized in automotive tire manufacturing, where multifilament nylon yarns enhance rubber strength and longevity.

Furthermore, nylon fibers play a critical role in construction applications such as geotextiles and reinforcement materials. The U.S. textile sector is steadily adopting Nylon-6 for durable sportswear, while Germany, Europe’s largest manufacturing hub, demonstrates strong growth momentum. The convergence of performance requirements and sustainability initiatives continues to drive innovation in nylon production technologies, ensuring long-term cyclohexane market growth.

Restraints - Benzene Feedstock Price Volatility and Crude Oil Exposure

Cyclohexane producers face significant supply chain vulnerabilities stemming from their dependence on benzene as the primary hydrocarbon feedstock, which is directly derived from crude oil through steam cracking and catalytic reforming processes. Price fluctuations in crude oil markets create corresponding volatility in benzene availability and costs, directly impacting cyclohexane production economics and profitability. Geopolitical tensions in major oil-producing regions, including disruptions in Middle Eastern supply chains and global trade uncertainties, create additional complexity in raw material procurement planning and force manufacturers to secure alternative feedstock sources at substantial premium costs.

Supply chain disruptions in petroleum refining operations can severely constrain benzene availability, necessitating inventory management challenges and production planning difficulties that cascade through cyclohexane manufacturing operations, ultimately limiting market supply and creating artificial price pressures that dampen demand from price-sensitive end-users.

Stringent Environmental Regulations and VOC Emission Compliance Costs

Environmental regulations on volatile organic compound (VOC) emissions impose significant capital investment and ongoing compliance costs for cyclohexane production facilities across Europe, North America, and increasingly Asia Pacific. Classified as a hazardous air pollutant under frameworks such as EU REACH and U.S. EPA standards, cyclohexane production requires advanced emission control systems, continuous monitoring, and process optimization to meet regulatory mandates.

Restrictions under REACH Annex XVII and similar global instruments add operational complexity and increase capital expenditure, particularly for smaller manufacturers lacking resources for sophisticated environmental infrastructure. These compliance obligations elevate production costs without proportional revenue gains, potentially constraining supply growth and limiting market entry for new participants unable to absorb substantial environmental management investments.

Opportunity - Bio-based and Sustainable Cyclohexane Production Technologies

The growing global emphasis on circular economy principles and sustainability presents significant opportunities for cyclohexane manufacturers pursuing bio-based production methods and recycling technologies. Research into biomass-derived feedstocks and alternative production routes aims to reduce reliance on petroleum while meeting rising demand for environmentally responsible chemical products. Advanced catalytic processes enabling production from renewable carbon sources, coupled with improved efficiency and waste reduction, position innovative producers to capture premium market segments favored by sustainability-conscious industries.

Investments in green production infrastructure align with initiatives such as the EU Green Deal, creating competitive advantages for companies with certified sustainable sourcing. Leading firms, including BASF SE, demonstrate the commercial viability of low-carbon production strategies, which are expected to drive market share growth among progressive chemical manufacturers throughout the forecast period.

EV Sector Expansion in High-Growth Asian Markets

Strategic capacity expansion across Asia Pacific manufacturing hubs offers significant growth potential, particularly in China and India, where industrial infrastructure development and concentrated automotive production are driving cyclohexane demand. Sinopec Group’s recent completion of a 450,000 metric ton per year cyclohexane unit at its Zhenhai refining complex underscores the scale of regional investment, with integrated facility design reducing logistics costs and enhancing supply chain reliability for nylon intermediates.

The electric vehicle segment further accelerates demand for specialized nylon materials with advanced thermal and electrical properties, creating a need for high-purity cyclohexane grades. Integration of cyclohexane production with downstream nylon operations optimizes material flow and cost efficiency, while strategic partnerships between global chemical firms and Southeast Asian industrial clusters enable localized nylon manufacturing and premium margins in emerging EV component applications.

Category-wise Analysis

Application Insights

Caprolactam production remains the dominant application segment for cyclohexane, accounting for approximately 43% of global consumption. This leadership is driven by strong demand for nylon-6 fiber and resin across the textile, automotive, and consumer goods industries. Cyclohexane serves as a critical feedstock for caprolactam synthesis, which is polymerized into nylon-6, a material valued for its exceptional tensile strength, elasticity, and abrasion resistance. Nylon-6 is widely used in apparel, carpeting, industrial textiles, and engineering plastics.

Furthermore, automotive manufacturers increasingly integrate nylon-6 components for lightweight panels, connectors, and under-hood applications, with electric vehicle producers emphasizing its use in battery enclosures and thermal management systems. This segment is expected to maintain its dominance throughout the forecast period, supported by rising textile demand and automotive lightweighting trends.

Industry Insights

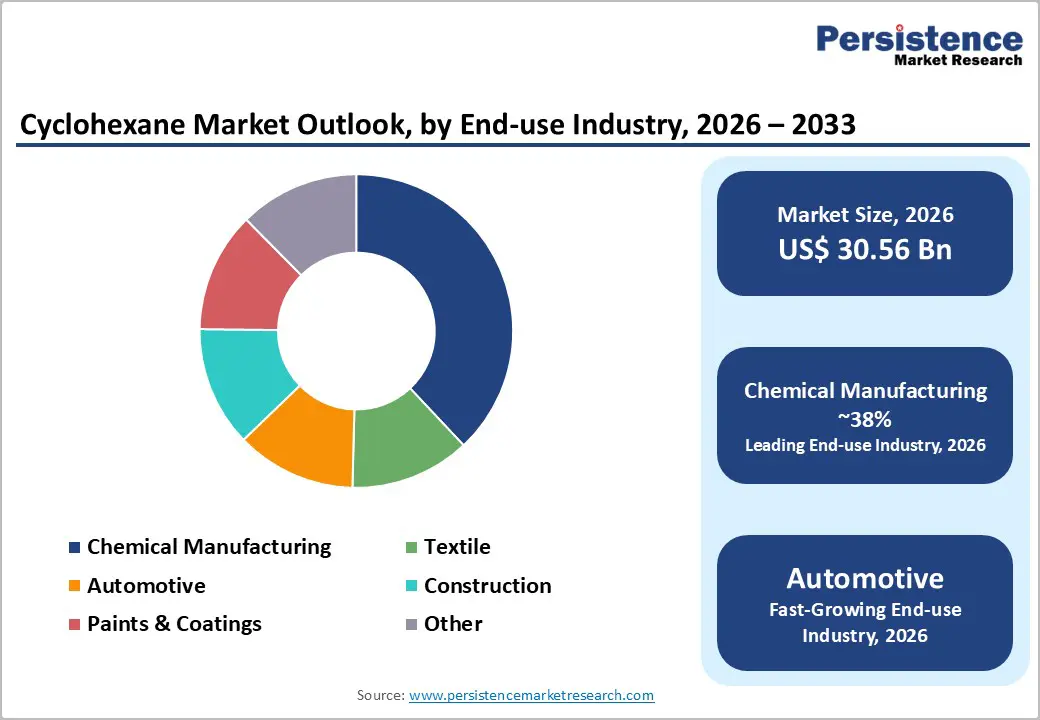

Chemical manufacturing constitutes the largest end-user segment for cyclohexane, holding a dominant market share of 38% market share, due to its critical role as an intermediate in adipic acid and caprolactam synthesis for nylon polymer production across diverse industrial sectors. Beyond polymer intermediates, cyclohexane serves as a solvent and extractant in specialty chemical manufacturing, organic synthesis, and industrial applications such as paints and coatings.

Leading producers, including BASF SE, ExxonMobil Chemical, and Sinopec Group, operate integrated facilities that combine cyclohexane production with downstream nylon manufacturing, ensuring operational efficiency and supply chain reliability. Continuous advancements in process optimization, catalyst technology, and high-purity grade development drive demand, while industry trends favor vertically integrated petrochemical complexes that enhance logistics economics and create significant technical barriers to entry.

Regional Insights

North America Cyclohexane Market Trends

North America remains a high-value, innovation-driven cyclohexane market, supported by advanced refinery infrastructure, robust manufacturing capabilities, and abundant feedstock from domestic crude oil resources. The U.S. accounted for nearly 81% of regional consumption in 2025, driven by strong demand for nylon resins and synthetic fibers in automotive, electronics, and packaging applications. In 2023, the U.S. Department of Energy allocated USD 180 million to enhance chemical manufacturing efficiency, including cyclohexane production optimization through advanced catalyst development and process integration.

Extensive R&D investments, technological innovation, and established supply chains position North America as a key supplier for domestic and export markets. Automotive applications dominate regional demand, with lightweight nylon components supporting fuel efficiency and compliance with EPA regulations, driving steady growth at an estimated 5.4% CAGR.

Europe Cyclohexane Market Trends

Europe is a key cyclohexane market, driven by advanced automotive manufacturing and stringent environmental regulations promoting sustainable production and lightweight material adoption. Germany leads regional consumption, supported by world-class automotive capabilities and BASF SE’s Ludwigshafen complex, a global hub for cyclohexane and nylon intermediates. In 2023, the EU automotive industry produced 12.1 million vehicles, each incorporating significant nylon-based components in engine compartments, interiors, and electrical systems, fueling robust demand.

France and Italy further contribute through luxury automotive and premium textile production. Regulatory emphasis on circular economy principles creates opportunities for bio-based technologies and advanced compliance systems. BASF’s investment in Ludwigshafen to enhance efficiency and reduce energy use underscores this trend. Europe is projected to be the fastest-growing region, driven by sustainability, technological innovation, and downstream chemical investments.

Asia Pacific Cyclohexane Market Trends

Asia Pacific dominates the global cyclohexane market, accounting for approximately 45% of total consumption, driven by a strong concentration of nylon manufacturing facilities, rapid textile industry growth, and expanding automotive production. China leads the region with extensive industrialization, large-scale caprolactam facilities, and abundant petrochemical feedstock, and is projected to achieve the highest CAGR of about 5.2%.

India’s growing textile sector further boosts demand through increased nylon-6 fiber production for global apparel markets, supported by rising income levels and infrastructure development. Southeast Asian countries offer additional opportunities through favorable policies and industrial expansion. Cost advantages, skilled labor, and large domestic markets attract multinational investments in localized production. Japan remains significant for high-purity cyclohexane applications in advanced automotive manufacturing. Sinopec’s 450,000 metric ton annual capacity at Zhenhai exemplifies the region’s momentum in integrated production and supply chain efficiency.

Competitive Landscape

The global cyclohexane market exhibits moderate consolidation, with major players such as BASF SE, Chevron Phillips Chemical Company LLC, ExxonMobil, and Sinopec Group commanding significant production capacity. Numerous mid-sized and regional manufacturers remain competitive through specialization and geographic focus. Leading companies pursue aggressive capacity expansions and invest in advanced catalyst technologies to improve efficiency and strengthen their position in high-growth Asian markets. Emerging trends favor vertical integration with nylon fiber and resin manufacturing, creating operational efficiencies and high entry barriers. Consolidation increasingly benefits large, diversified chemical firms with strong financial resources, customer relationships, and technological capabilities.

Key Developments:

- September 2024: BASF SE announced EUR 180 million investment upgrading its Ludwigshafen, Germany, cyclohexane production facility with advanced catalyst technology, improving conversion efficiency by 8% while reducing energy consumption by 12%.

- December 2024: Sinopec Group announced the mechanical completion of the second-phase expansion and advanced materials project at its Zhenhai Refinery. The refinery's capacity has now been upgraded to 40 million tons per year, contributing to the Zhejiang Ningbo Petrochemical Industrial Base surpassing a total refining capacity of 50 million tons annually.

- December 2025: ExxonMobil, Aramco, and Samref have signed a Venture Framework Agreement to evaluate upgrading the Samref refinery in Yanbu and expanding it into an integrated petrochemical complex. They will explore capital investments for enhanced production of low-emission, high-quality distillates and chemicals, along with strategies to improve energy efficiency and reduce operational emissions.

Top Companies in the Cyclohexane Market

- BASF SE (Ludwigshafen, Germany) represents the global cyclohexane market leader, commanding substantial production capacity across integrated Verbund manufacturing complexes in Ludwigshafen and Antwerp while maintaining strong R&D capabilities and commitment to sustainable production technologies. The company demonstrates technological excellence through continuous process innovation and significant investments in advanced catalyst development, enabling superior conversion efficiency and cost competitiveness that reinforce market leadership positioning across major global markets.

- Chevron Phillips Chemical Company LLC (Woodland, U.S.) operates strategically positioned production facilities across North America and the Asia Pacific regions, leveraging extensive petrochemical expertise and established customer relationships to maintain competitive market share in nylon intermediate supply. The company emphasizes production optimization and quality consistency while investing in advanced catalyst technologies and process innovations supporting sustained competitive advantage in price-sensitive industrial markets.

- ExxonMobil Chemical (Texas, U.S.) maintains significant cyclohexane production capacity across multiple global facilities, capitalizing on integrated refinery operations and established distribution networks serving major automotive, textile, and industrial customers. Strategic investments in joint venture partnerships and advanced hydrogenation technologies position the company to capitalize on emerging growth opportunities in electric vehicle component manufacturing and sustainable polymer production applications.

Companies Covered in Cyclohexane Market

- BASF SE

- Sunoco Chemicals

- ExxonMobil Chemical

- Huntsman Corporation

- Chevron Phillips Chemical Company LLC

- Royal Dutch Shell plc

- Sinopec Group

- Koninklijke DSM N.V.

- Reliance Industries Limited

- Dow Chemical Company

- Shell Chemicals

Frequently Asked Questions

The global cyclohexane market is projected to reach US$ 30.6 Billion in 2026, expanding to US$ 42.8 Billion by 2033, representing a CAGR of 4.9% throughout the forecast period, supported by escalating nylon intermediate demand across automotive, textile, and chemical manufacturing sectors.

Rising automotive industry demand for lightweight materials supporting fuel efficiency improvement and electric vehicle component manufacturing, combined with expanding global textile consumption in developing economies and increasing industrial utilization of nylon-based materials in construction and manufacturing applications, represent the primary market growth catalysts.

Caprolactam production commands the largest market segment with 43% of global cyclohexane consumption, driven by extraordinary demand for nylon-6 fiber and resin production across textile, automotive, and engineering plastic industries requiring this critical monomer.

Asia Pacific dominates global cyclohexane consumption with approximately 45% market share, driven by concentrated nylon manufacturing capacity in China, India, and Southeast Asia, while Europe emerges as the fastest-growing region due to sustainable production emphasis and automotive lightweighting initiatives.

Electric vehicle component manufacturing represents the highest-growth opportunity, with specialized nylon materials required for battery enclosures and thermal management driving incremental cyclohexane demand as global EV production accelerates, complemented by sustainable production technology development addressing environmental regulatory requirements.

BASF SE, Chevron Phillips Chemical Company LLC, ExxonMobil, Sinopec Group, Huntsman Corporation, Reliance Industries Limited, and Dow Chemical Company represent major global manufacturers commanding significant production capacity and market share through technological excellence and strategic geographic positioning.