- Processed Food

- Culinary Sauces Market

Culinary Sauces Market Size, Share, and Growth Forecast, 2025 - 2032

Culinary Sauces Market Consistency Type (Wet sauces, Dry/Concentrate Sauces), Product Type (Tomato/Ketchup, Pasta Sauces, Others), End-user, Packaging, and Regional Analysis for 2025 - 2032

Culinary Sauces Market Size and Trends Analysis

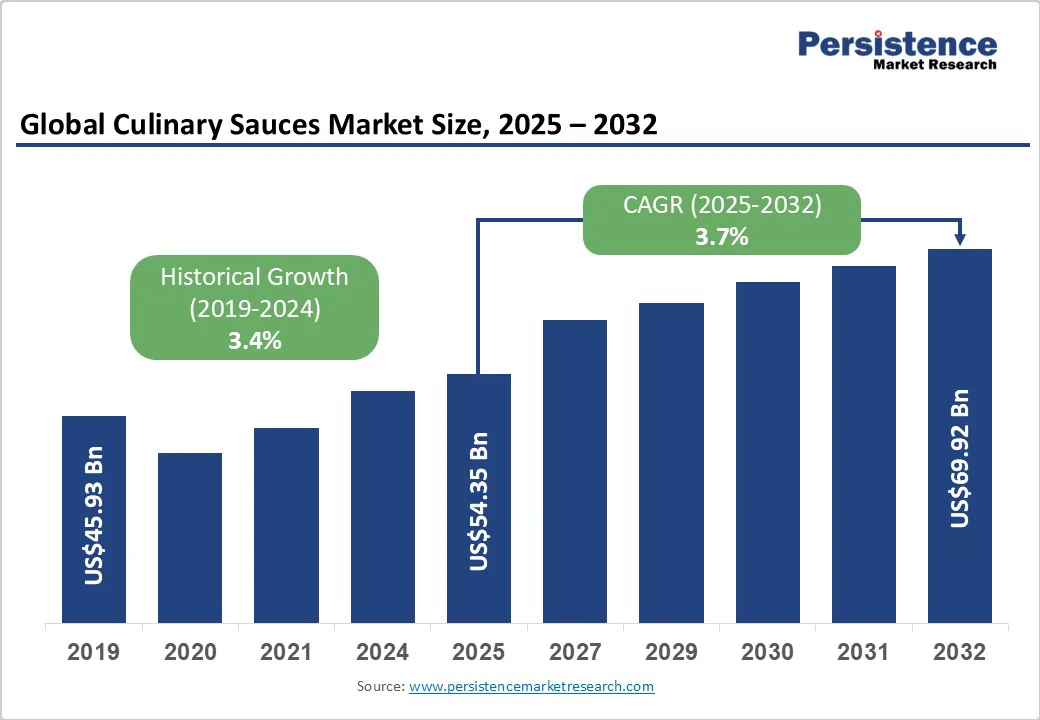

The global culinary sauces market size was valued at US$53.95 Billion in 2025 and is projected to reach US$69.92 Billion by 2032, growing at a CAGR of 3.7% between 2025 and 2032, driven by shifting consumer lifestyles, including an increase in home cooking and a rising preference for ethnic and premium flavors. Retail and e-commerce expansion are raising both unit demand and average selling prices.

Supply-side dynamics, including raw material volatility and logistics, create short-term margin pressure and also open opportunities in premium and private-label sauces. The market remains structurally fragmented and dominated by large packaged-food companies and specialized regional players.

Key Industry Highlights

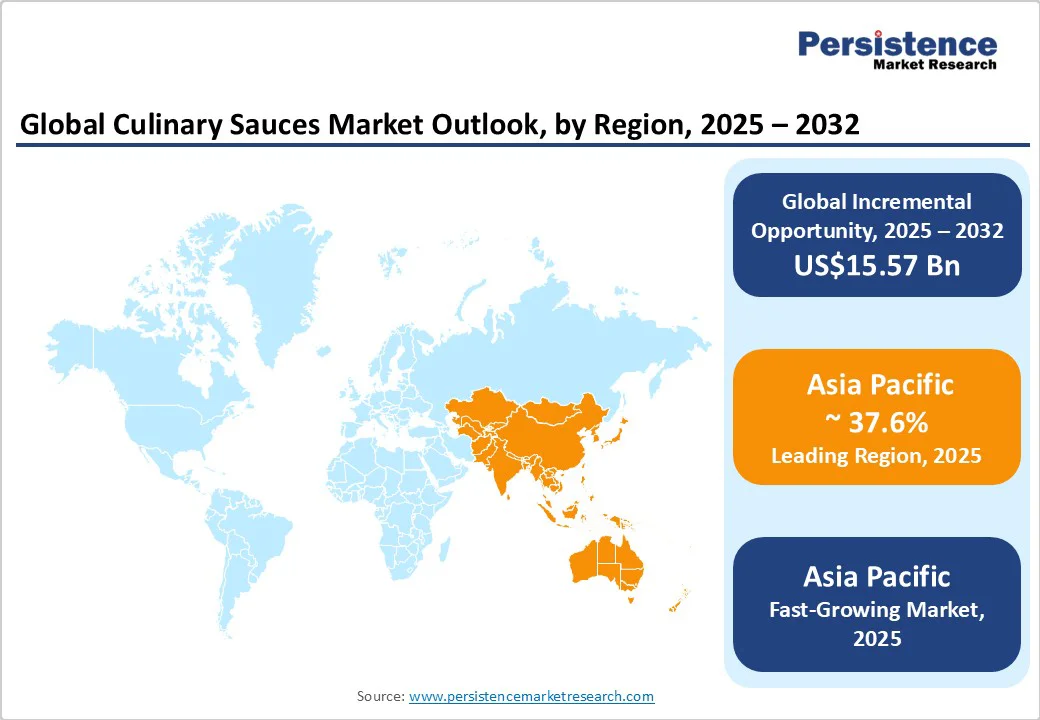

- Leading Region: Asia Pacific, accounting for approximately 37.6% of the global market; driven by high domestic consumption of soy, chili, and fermented sauces, strong manufacturing hubs in China and Japan, and rapid retail expansion in India.

- Fastest-growing Region: Asia Pacific, fueled by demand for convenience, clean-label products, premium flavors, and expansion of foodservice and meal-kit channels.

- Investment Plans: Expansion of manufacturing facilities, joint ventures, and technology upgrades; notable examples include Lee Kum Kee’s plant expansions in China and Southeast Asia and Kikkoman’s joint venture in India to enhance local production capabilities.

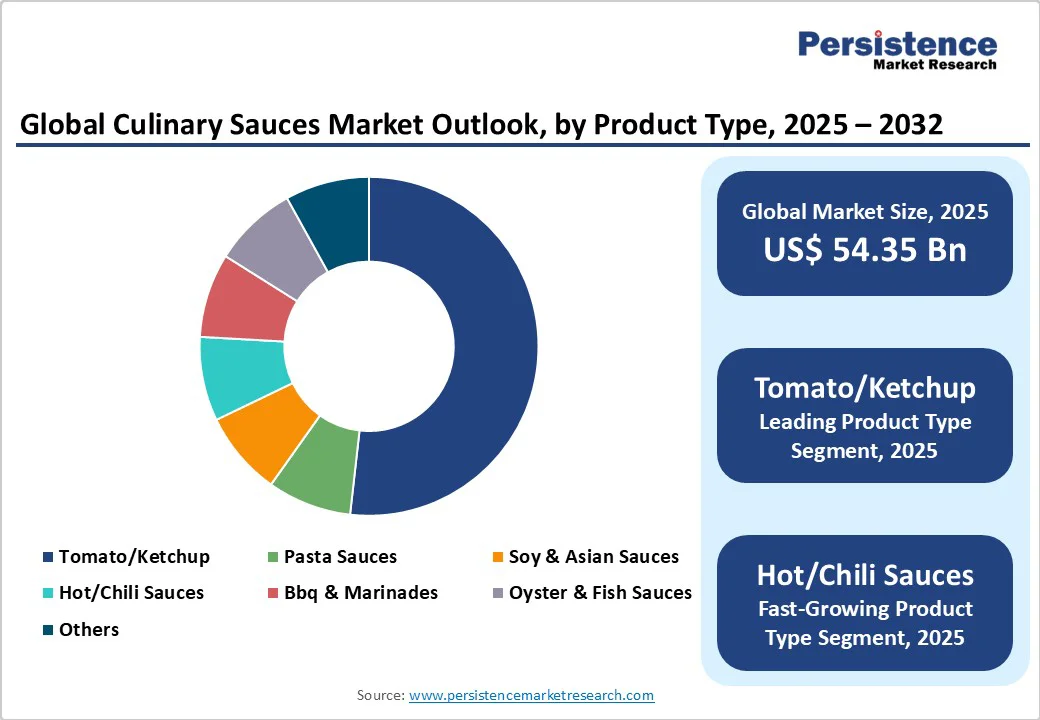

- Dominant Product Type: Tomato-based sauces and ketchup leading retail rotation and household penetration with examples such as Heinz Tomato Ketchup, Del Monte Tomato Sauce, and Prego Pasta Sauces, representing 58.4% of market share.

- Leading End-user: Household segment accounts for 63% of revenue in 2025, with consistent repeat purchases, strong brand loyalty, and distribution across supermarkets, hypermarkets, and e-commerce platforms, while foodservice and industrial channels are the fastest-growing sub-segments.

| Key Insights | Details |

|---|---|

|

Culinary Sauces Market Size (2025E) |

US$54.35 Bn |

|

Market Value Forecast (2032F) |

US$69.92 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Convenience and At-Home Premiumization

Consumer behavior demonstrates sustained growth in at-home meal occasions, driving demand for ready-to-use sauces. The increase in retail and e-commerce penetration has made sauces widely accessible and boosted household penetration. Between 2019 and 2025, the market expanded, reflecting the rising appeal of convenient and premium products. Manufacturers are responding with shelf-stable, refrigerated, and dry concentrate formats, raising average selling prices and supporting steady mid-single-digit growth.

Clean-Label, Health, and Plant-Based Innovation

Consumers increasingly prefer sauces with reduced sodium, no artificial preservatives, organic certification, and plant-based positioning. Clean-label and nutrient-enriched products are commanding premium pricing and securing retailer shelf space. Health initiatives in key markets, such as voluntary sodium reduction programs, drive reformulation, increasing R&D investment while providing competitive differentiation for early movers.

Foodservice Recovery and Cross-Border Flavors

The foodservice channel, including restaurants, QSRs, and HoReCa, is a high-value segment for sauces. Its recovery post-pandemic has driven demand for industrial and culinary-grade sauces. Additionally, global migration and cross-cultural dining trends have increased adoption of Asian, Latin American, and Middle Eastern sauces in Western retail. These trends boost volume and premium SKU penetration, enhancing both retail and foodservice revenues.

Barrier Analysis - Raw Material Price Volatility

Sauce production relies on commodities such as tomatoes, oils, and spices. Supply disruptions, crop failures, or tariff changes can increase production costs and compress margins. Smaller processors face margin erosion during such periods, while companies with long-term contracts or vertical integration remain more resilient.

Regulatory and Labeling Complexities

Evolving labeling requirements, allergen declarations, and nutrition regulations increase compliance costs. Differences across countries force SKU proliferation and raise supply-chain complexity. Non-compliance can lead to recalls, posing reputational and financial risks that constrain rapid product launches.

Opportunity Analysis - Premium and Ethnic Flavor Portfolios

Premiumization through authentic regional sauces and artisanal products presents a significant growth opportunity. Ethnic sauces from Korea, India, and Latin America command price premiums of 10–30% over commodity products. If penetration continues, premium and ethnic extensions could add US$5–10 Billion in global retail value by 2030.

B2B and Ready-Meal Integration

Industrial demand from food processors, frozen meals, and meal-kit producers requires scalable, functional sauces. Concentrated and dry formats are particularly appealing for cost efficiency and shelf life. B2B sauce demand could account for 20–30% of production volumes in mature markets over the next five to eight years, providing a stable, high-volume revenue source.

Category-wise Analysis

Product Type Insights

Tomato-based sauces and ketchup remain the backbone of the culinary sauces market due to ubiquity in households and consistent consumption patterns, holding a market share of 58.4% in 2025. Products such as Heinz Tomato Ketchup, Del Monte Tomato Sauce, and Prego Pasta Sauces illustrate the scale and popularity of these products. Their production benefits from economies of scale, allowing companies to maintain competitive pricing while ensuring wide distribution. These sauces are often considered pantry staples, with strong rotation in supermarkets, convenience stores, and e-commerce channels. Retailers often promote tomato-based sauces through bundle offers and multipacks, further boosting sales volumes. Beyond traditional ketchup, innovations such as organic, low-sugar, or herb-infused variants support premiumization trends within this leading category.

The fastest growth is observed within hot/chili sauces and related spicy formats, which include traditional hot sauces, chili pastes, and flavored spicy condiments. Examples include Tabasco, Huy Fong Sriracha, Nando’s Peri-Peri, and regional chili-garlic sauces from companies such as Lee Kum Kee. Growth drivers include taste-seeking, social media-led food trends, QSR menu innovation, and penetration into the frozen meals and meal kit market. End-uses extend beyond household retail into foodservice and industrial supply (bulk tubs for QSRs, inclusion in ready meals), which amplifies volumes and margin opportunities. Ethnic” or fusion is a cross-cutting innovation theme rather than a distinct product-type in the taxonomy; fusion variants. For example, Korean-style BBQ glazes or chili-garlic marinades are typically recorded under existing categories such as Hot/Chili, BBQ & Marinades, or Soy & Asian sauces.

End-user Insights

Household consumption remains the largest segment with a market share of 63% in 2025, supported by repeat purchases, brand loyalty, and the presence of major supermarket chains. Products such as Kraft Heinz sauces, Unilever’s Knorr culinary bases, and Campbell’s pasta sauces dominate retail shelf space. Supermarkets, hypermarkets, and online grocery platforms serve as the main distribution channels. This segment benefits from strong promotional activity, seasonal bundling (pasta meal kits or barbecue packs), and in-store sampling campaigns. The household segment also increasingly favors convenience-driven innovations, including re-sealable bottles, squeezable pouches, and ready-to-heat sauces, which encourage trial and repeat purchases.

The foodservice and industrial channels are experiencing the fastest growth, fueled by dining-out recovery, growth of QSRs, and the expansion of ready-meal manufacturing. Bulk sauces for institutional use, such as large-format ketchup, soy sauce, or pasta sauce tubs, are increasingly popular. Companies such as McCormick, Conagra, and Kikkoman have tailored industrial formats for foodservice operators and meal-kit companies. The segment also benefits from private-label contracts, where sauces are supplied directly to food processors under customized formulations. Industrial adoption not only increases sales volume but also ensures consistent contracts and margin stability, making it a strategic focus for manufacturers targeting long-term growth.

Regional Insights

North America Culinary Sauces Market Trends - Clean-Label, and Strategic Expansion Drive the U.S. Culinary Sauces Market

North America, led by the U.S., is driven by increasing consumer demand for convenience, diverse global flavors, and clean-label products. Retailers respond with extensive stock keeping unit (SKU) variety, including premium, organic, and low-sodium options. Regulatory frameworks such as FDA labeling requirements and voluntary sodium reduction programs influence product formulation and innovation.

The U.S. market features a strong presence of major CPG players, including Kraft Heinz, Conagra, Campbell, and McCormick, which dominate both retail and foodservice channels. Recent developments include McCormick’s expansion of its North American plant in 2024, enhancing production capacity for dry and concentrated sauces, and Kraft Heinz’s targeted acquisitions to strengthen its organic and ethnic sauce portfolio. Foodservice and meal-kit channels are emerging as significant growth drivers, with partnerships between large sauce manufacturers and QSRs or online meal-kit companies enabling broader distribution and higher-volume sales.

Europe Culinary Sauces Market Trends - Mature Market Focused on Premiumization, Regulation, and Sustainability

Europe represents a mature culinary sauces market characterized by high per-capita spend and strict regulatory oversight. Leading markets include Germany, the U.K., France, and Spain, each with distinct consumption patterns. Germany emphasizes premium and organic sauces, while the U.K. and France are highly innovative in supermarkets with ready-to-use meal solutions and ethnic sauce options. Harmonized EU labeling standards and nutrition targets, such as sodium and sugar regulations, increase reformulation costs but also provide opportunities for differentiation and premium positioning.

Retail consolidation, private-label penetration, and investment in sustainable packaging are shaping competitive strategies. Notable developments include Unilever’s 2025 launch of low-sodium Knorr sauces in the U.K. and Campbell’s expansion of premium pasta sauces in Germany, reflecting ongoing efforts to meet evolving consumer preferences. France’s robust foodservice sector, combined with cross-border trading, further enhances the region’s strategic relevance in both retail and industrial channels.

Asia Pacific Culinary Sauces Market Trends - Rapid Growth Fueled by Traditional Flavors and Manufacturing Hubs

Asia Pacific is the largest and fastest-growing region, accounting for approximately 37.6% of the market share in 2025. Growth is supported by strong domestic consumption of soy, chili, and fermented sauces, alongside the rapid expansion of modern retail formats and e-commerce platforms. China and Japan serve as key manufacturing hubs, providing cost advantages and advanced R&D capabilities. India is experiencing rapid retail growth driven by urbanization, a young population, and increasing awareness of global flavors.

Recent developments include Lee Kum Kee’s expansion of its China and Southeast Asia manufacturing plants in 2025 and Kikkoman’s joint venture in India to produce local soy and chili sauces, enhancing regional production and distribution efficiency. Key country insights highlight China’s dominance in volume due to traditional dietary patterns, Japan’s focus on premium and export-oriented sauces, and India’s growing market for ready-to-use and packaged ethnic sauces. Investment trends include plant expansions, joint ventures, and technology upgrades, positioning the region as a critical growth engine for global sauce manufacturers.

Competitive Landscape

The global culinary sauces market is fragmented, with numerous regional and artisanal brands alongside global leaders. Leading players such as Kraft Heinz, Unilever, Nestlé, McCormick, Kikkoman, and Conagra dominate branded revenues. Core SKUs are concentrated among top players, while premium and ethnic niches remain fragmented.

Key strategies include product innovation (clean label, ethnic flavors), capacity expansion, channel digitalization, and acquisitions for market access. Leaders emphasize R&D, co-packing partnerships, and private-label defense to maintain competitive advantage.

Key Industry Developments

- In March 2025, Kraft Heinz launched its Organic Tomato Ketchup and Reduced-Sodium BBQ Sauce lines in the U.S., targeting health-conscious consumers and strengthening its position in the North American retail segment.

- In May 2025, Lee Kum Kee expanded production at its China and Southeast Asia plants to scale up Premium Soy Sauce, Oyster Sauce, and Chili Garlic Sauce lines for both domestic and export markets.

Companies Covered in Culinary Sauces Market

- Kraft Heinz Company

- Unilever PLC

- Nestlé S.A.

- McCormick & Company, Inc.

- Kikkoman Corporation

- Conagra Brands, Inc.

- Del Monte Foods, Inc.

- Campbell Soup Company

- Hormel Foods Corporation

- General Mills, Inc.

- B&G Foods, Inc.

- Lee Kum Kee

- McIlhenny Company (Tabasco)

- Ajinomoto Co., Inc.

- Yamasa Corporation

- Hain Celestial Group, Inc.

- Mizkan Holdings Co., Ltd.

- Otafuku Sauce Co., Ltd.

- Tilda Foods Limited

- Goya Foods, Inc.

Frequently Asked Questions

The culinary sauces market size is estimated at US$54.35 Billion in 2025.

The culinary sauces market is projected to reach US$69.92 Billion by 2032, reflecting stable but moderate growth.

Key trends include premiumization and ethnic flavor adoption, clean-label and reduced-sodium products, dry/concentrate sauce formats for convenience and longer shelf life, and the growth of online and foodservice channels.

Tomato-based sauces and ketchup remain the leading product type globally, supported by high household penetration, strong retail rotation, and widespread brand recognition.

The culinary sauces market is expected to grow at a CAGR of 3.7% between 2025 and 2032.

Major players include Kraft Heinz Company, Unilever PLC, Nestlé S.A., McCormick & Company, Inc., and Kikkoman Corporation.