- Specialty & Fine Chemicals

- Copper Scrap Market

Copper Scrap Market Size, Share, and Growth Forecast 2026 - 2033

Copper Scrap Market by Scrap Type (Copper Wire Scrap, Copper Tubing Scrap, Copper Sheets & Plates Scrap, Copper Radiators Scrap, Copper Turnings/Shavings, Others), Material Composition (Pure Copper Scrap, Alloyed Copper Scrap), Purity Level (High Purity, Medium Purity, Low Purity), End-userr, and Regional Analysis, 2026 - 2033

Copper Scrap Market Size and Trend Analysis

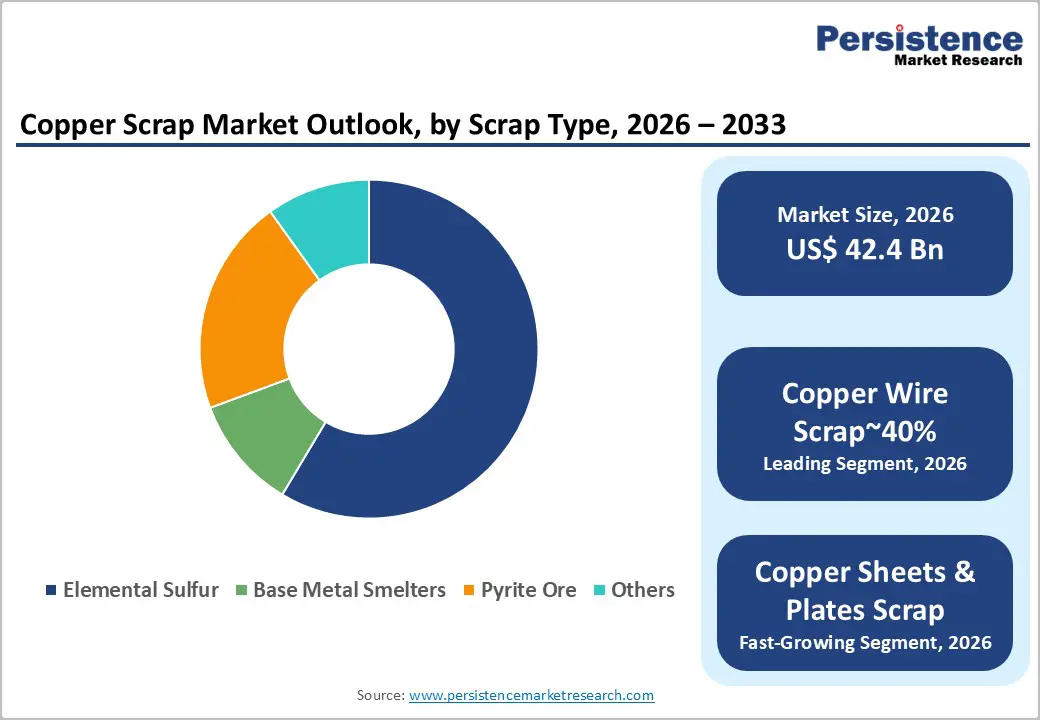

The global copper scrap market size is likely to be valued at US$ 42.4 billion in 2026 and is expected to reach US$ 67.6 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033.

The copper scrap market is on an accelerating growth trajectory, driven by the global energy transition, creating volumes of demand for copper in EV charging infrastructure, wind and solar power systems, and grid modernization, applications where recycled copper is increasingly favored for its lower carbon footprint and cost advantages over primary production.

Key Market Highlights

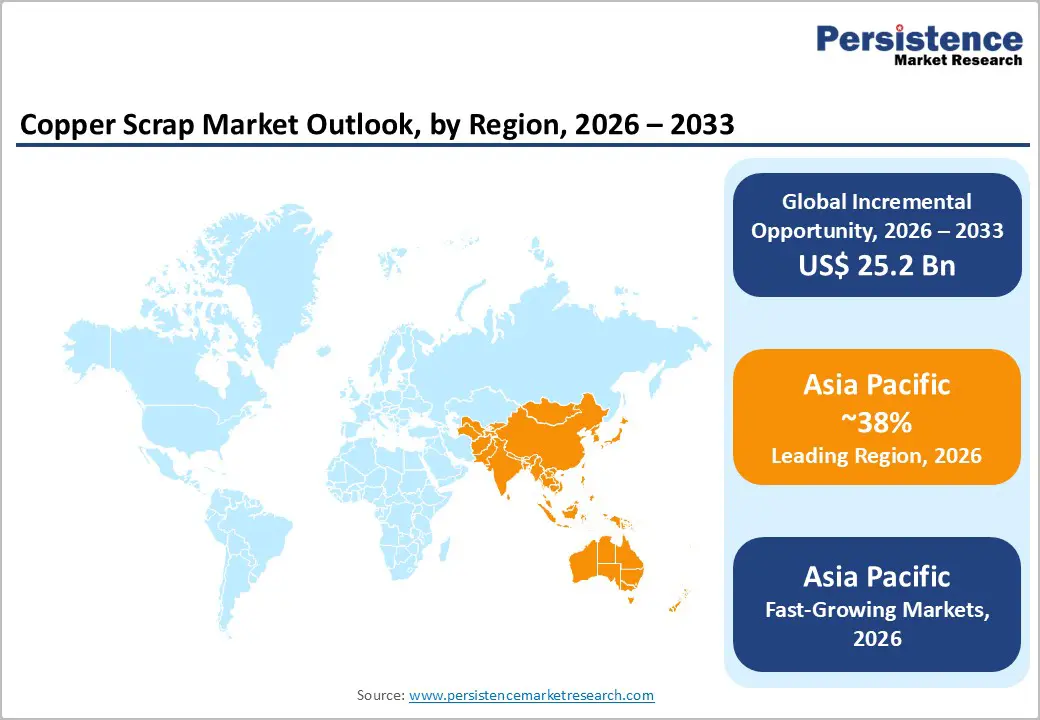

- Leading Region: Asia Pacific is likely to lead the copper scrap market, accounting for 38% share in 2026, driven by China's position as the world's largest copper consumer with growing domestic scrap generation, India's expanding manufacturing and EV sector, Japan's world-class urban mining infrastructure, and ASEAN's rapidly growing electronics manufacturing scrap base.

- Fastest Growing Region: North America is the fastest growing region, propelled by the US$ 65 billion Bipartisan Infrastructure Law grid upgrade, generating legacy copper scrap, IRA clean energy investments driving copper demand, and ISRI-structured formal scrap collection networks enabling efficient high-purity copper recovery.

- Dominant Segment: Copper wire scrap dominates the scrap type category with 40% share, reflecting the International Copper Association's finding that electrical applications consume 65% of global copper demand, making wire and cable the largest and most homogeneous end-of-life copper recovery stream globally.

- Fastest Growing End-userr Segment: Renewable energy is the fastest growing end-user segment, driven by IEA projections of four-times copper demand growth by 2040 under net-zero scenarios and IRENA's 10,000+ GW renewable capacity additions by 2030, both requiring massive copper input increasingly sourced from secondary recycling.

- Opportunity: Advanced urban mining and AI-powered scrap sorting technologies enable profitable processing of previously uneconomic mixed and electronic scrap, with Aurubis AG achieving 98%+ copper recovery from complex WEEE under EU Circular Economy mandates, representing high-margin processing expansion for leading recyclers.

Market Dynamics

Drivers - Global Energy Transition Driving Volumes of Copper Demand

The worldwide energy transition to renewable power, electric vehicles, and grid modernization is the most powerful structural growth catalyst for the copper scrap market. The IEA's Critical Minerals Report estimates that a single offshore wind turbine requires up to 25 tonnes of copper, an EV contains approximately 83 kg of copper, roughly four times that of a conventional ICE vehicle, and grid-scale battery storage systems require substantial copper wiring.

Global EV sales exceeding 14 million units in 2023 per the IEA, combined with the International Renewable Energy Agency (IRENA)'s projection of 10,000+ GW of renewable energy capacity additions by 2030, creates a structural demand surge that primary mining supply cannot fully satisfy. Copper scrap recycling, requiring only 85% less energy than primary smelting per the Copper Alliance, is positioned as a critical supply gap-filling source for energy transition copper demand.

Circular Economy Policies and Extended Producer Responsibility Mandates

Government circular economy mandates and extended producer responsibility (EPR) regulations are structurally increasing copper scrap supply and formalizing recycling flows. The European Union's Circular Economy Action Plan targets a 70% recycling rate for electronics waste and mandates design-for-recyclability standards that increase recoverable copper content from end-of-life products. The EU's Battery Regulation (EU 2023/1542) mandates minimum recycled copper content thresholds in new battery packs from 2031.

In the United States, the EPA's National Recycling Strategy targets a 50% recycling rate for municipal solid waste by 2030, creating supportive policy conditions for expanded copper recovery infrastructure. These regulations collectively stimulate scrap availability, legitimize secondary copper supply chains, and incentivize investment in advanced scrap sorting and processing technology across major markets.

Restraints - Copper Scrap Supply Volatility and Collection Infrastructure Gaps

The copper scrap market faces persistent challenges in securing consistent, predictable feedstock volumes, particularly high-purity clean scrap suitable for direct melting. Informal and fragmented scrap collection networks, dominant in developing markets, result in supply quality variability, delayed collection cycles, and loss of recoverable copper to non-formal channels.

The Bureau of International Recycling (BIR) estimates that globally, significant volumes of end-of-life copper-containing products are inadequately processed for metal recovery, representing both a supply constraint and an environmental challenge. Supply-side volatility also correlates with copper price fluctuations on the London Metal Exchange (LME), creating procurement uncertainty for secondary copper processors.

Trade Restrictions and Export Bans on Copper Scrap

Government-imposed trade restrictions and export bans on copper scrap are creating significant market fragmentation. China, historically the world's largest copper scrap importer, introduced GB/T 38470-2019 solid waste import standards and Category 7 scrap reclassification regulations that effectively banned low- and medium-grade copper scrap imports from 2021.

The World Trade Organization (WTO) has documented multiple trade policy disputes related to scrap metal export controls among major economies. These restrictions disrupt established global copper scrap trade flows, force exporters to seek alternative markets at lower premiums, and compel importers to pay higher prices for domestic scrap, collectively reducing market efficiency.

Opportunities - Renewable Energy Infrastructure Build-Out Creating New Scrap Generation Streams

The massive renewable energy infrastructure build-out is simultaneously creating new high-quality copper scrap generation streams that will feed recyclers through the forecast period and beyond. As first-generation wind farms and solar installations constructed in the 2000s reach end-of-life, wind turbine lifespans are typically 20-25 years, they will generate significant volumes of copper wire, transformer scrap, and cable assemblies.

IRENA estimates that wind turbine decommissioning globally could generate millions of tonnes of recyclable materials annually by the early 2030s. Aurubis AG and Boliden AB have specifically invested in renewable energy scrap processing capabilities. Recyclers who establish collection and processing infrastructure for decommissioned renewable energy components, including copper-rich transformers, generators, and cabling, will be positioned to capture a new, structurally growing, and geographically predictable scrap supply stream.

Advanced Scrap Sorting and Urban Mining Technology

Investment in advanced copper scrap sorting, separation, and urban mining technologies represents a significant commercial opportunity to unlock copper value from previously uneconomic low- and medium-grade scrap streams. Technologies, including AI-powered optical sorting, X-ray fluorescence (XRF) analyzers, eddy current separation, and hydrometallurgical processing, are enabling recyclers to process mixed and contaminated scrap more efficiently, recovering higher copper yields from feedstocks previously sent to landfill.

The European Commission's WEEE Directive mandating the collection and treatment of electrical and electronic waste is expanding the urban mining opportunity base. Companies including Aurubis AG and Glencore plc have invested in proprietary hydrometallurgical and pyrometallurgical technologies capable of processing complex electronic scrap with copper recovery rates exceeding 98%, enabling premium margins from high-complexity feedstocks.

Category-wise Analysis

By Scrap Type Insights

Copper wire scrap is the dominant scrap type, commanding approximately 40% of the copper scrap market. Copper wire, drawn from the electrical and telecommunications sectors, including power cables, building wiring, motor windings, and telecommunications cables, represents the single largest and most homogeneous copper scrap stream globally.

The International Copper Association (ICA) estimates that electrical applications consume approximately 65% of all global copper demand, making wire and cable the primary end-of-life copper recovery source. Wire scrap's relatively high purity, particularly Bare Bright copper wire and No. 1 copper wire grades, makes it the most commercially valuable and directly recyclable scrap category, commanding premium pricing and enabling direct use as secondary copper smelting feedstock.

By Material Composition Insights

Pure copper scrap is the dominant material composition segment, accounting for approximately 62% of the market. Pure copper scrap, classified under ISRI (Institute of Scrap Recycling Industries) grades including Bare Bright, No. 1 Copper, No. 2 Copper, and Insulated Copper, commands the highest secondary market premiums due to its direct usability in copper rod mills and refineries without complex alloy separation processing.

The London Metal Exchange (LME) copper price serves as the primary pricing benchmark, with pure copper scrap typically trading at 98% of the LME Grade A cathode price, depending on grade and contamination levels. Processors, including Aurubis AG and Boliden AB prioritize pure copper scrap procurement for their low-cost secondary smelting and rod production operations.

By Purity Level Insights

High Purity copper scrap is the dominant purity level segment, representing approximately 48% of the market. High-purity grades, including Bare Bright copper wire (99.9%+ Cu) and No. 1 Copper, command premium pricing and can be directly charged into copper rod mills and fire-refined copper (FRHC) furnaces without extensive pre-processing.

The ISRI Scrap Specifications Circular, the industry standard reference for scrap classification in North America, defines precise purity and contamination thresholds for each grade. Growing demand from renewable energy applications requiring high-conductivity copper wire and EV motor windings is sustaining premium demand for high-purity scrap, specifically, as contaminated or alloyed copper cannot meet the conductivity requirements of these applications without additional refining.

By End-user Insights

The electrical & electronics end-user segment is the dominant application for copper scrap, accounting for approximately 45% of total end-user demand. The fundamental role of copper as the preferred electrical conductor, underpinned by its unique combination of high conductivity, formability, and corrosion resistance, makes electrical and electronics applications the largest and most consistent copper scrap consumer.

Secondary copper processed from scrap is widely used in power cable manufacturing, electrical wire rod production, transformer windings, and PCB interconnects. The International Copper Association notes that electrical applications consume approximately 65% of global copper demand. As the energy transition electrifies transportation, buildings, and industry, this end-user segment's copper consumption is set to grow faster than any other application category through 2033.

Regional Insights

North America Copper Scrap Market Trends & Analysis

North America’s copper scrap market is driven by strong industrial recycling ecosystems, high collection efficiency, and export-oriented trade flows. The U.S. dominates regional supply, supported by infrastructure modernization and clean energy investments. Replacement of aging grid systems and EV expansion are expected to steadily increase scrap generation and domestic processing demand.

- U.S. Copper Scrap Market Size

The United States accounts for over 80% of North America’s copper scrap market, valued at approximately USD 18 billion in 2026. Growth is supported by federal infrastructure spending and renewable energy expansion, with a projected CAGR of 6.5% through 2033, driven by both domestic consumption and strong export demand.

Europe Copper Scrap Market Trends, Drivers & Insights

Europe’s copper scrap market is highly mature, driven by stringent recycling regulations and circular economy initiatives. Policies such as the Circular Economy Action Plan and WEEE Directive ensure high recovery rates. Advanced smelting and recycling infrastructure, combined with cross-border scrap movement, supports efficient material utilization and long-term sustainability goals.

- Germany Copper Scrap Market Size

Germany leads Europe’s copper scrap market, accounting for nearly 30% of regional value, estimated at USD 8.9 billion in 2026. Strong industrial output, robust recycling laws, and major players like Aurubis AG support consistent growth, with increasing scrap generation from automotive electrification and renewable energy infrastructure.

- U.K. Copper Scrap Market Size

The U.K. copper scrap market is valued at approximately USD 3.4 billion in 2026. Growth is driven by construction sector recovery, the decommissioning of legacy infrastructure, and strong export activity. Recycling industry consolidation and sustainability targets are expected to support moderate growth at around 5.6% CAGR through 2033.

- France Copper Scrap Market Size

France represents a mid-sized copper scrap market in Europe, estimated at USD 3.5 billion in 2026. Manufacturing, construction, and renewable energy projects drive the demand. Government-backed circular economy policies and increasing electronic waste recycling are expected to enhance copper recovery rates gradually.

Asia Pacific Copper Scrap Market Drivers & Analysis

Asia Pacific dominates the global copper scrap market, supported by rapid industrialization, high copper consumption, and growing domestic scrap generation. The region benefits from strong electronics manufacturing, urban mining practices, and expanding infrastructure. Regulatory shifts and import restrictions are reshaping supply chains toward increased domestic recycling.

- China Copper Scrap Market Size

China is the largest copper scrap market globally, accounting for over 40% of total demand, valued at approximately USD 16.8 billion in 2026. Domestic scrap generation is rising due to aging infrastructure and electronics, offsetting import restrictions, with steady growth expected at 6.7% CAGR through 2033.

- India Copper Scrap Market Size

India’s copper scrap market is rapidly expanding, estimated at USD 4.5 billion in 2026. Growth is fueled by infrastructure development, rising electrical equipment demand, and EV adoption initiatives. Increasing formalization of recycling and investments in processing capacity are expected to drive a strong CAGR of 7.8% through 2033.

- Japan Copper Scrap Market Size

Japan’s copper scrap market is valued at approximately USD 3.4 billion in 2026, supported by advanced recycling technologies and efficient urban mining systems. High recovery rates from electronic waste and automotive sectors sustain a stable supply, with moderate growth of around 4.5% CAGR driven by technological innovation and sustainability goals.

Competitive Landscape

The Copper Scrap Market is highly fragmented at the collection and aggregation levels, dominated by thousands of small and medium-sized scrap dealers, but moderately consolidated at the large-scale processing tier, where Aurubis AG, Glencore plc, Boliden AB, and Sims Limited command significant share. Key differentiators include proprietary scrap sorting and metallurgical processing technology, global sourcing networks, LME-linked pricing expertise, and strategic locations near major scrap generation hubs.

Competitive strategies include vertical integration into copper rod production, investment in AI-powered scrap sorting infrastructure, acquisition of regional scrap dealers, and development of digital scrap trading platforms. Emerging business model trends include scrap-as-a-service procurement contracts with industrial manufacturers and copper lifecycle management partnerships with renewable energy developers to secure future decommissioning scrap streams.

Key Developments:

- March, 2025: Aurubis AG commissioned its expanded Multi-Metal Recovery (MMR) plant in Hamburg, increasing annual copper scrap processing capacity by 100,000 tonnes, specifically designed to process complex electronic scrap and renewable energy component recyclates.

- June, 2024: Boliden AB invested SEK 800 million in upgrading its Rönnskär smelter in Sweden to increase electronic scrap processing throughput by 30%, targeting the growing WEEE copper recovery stream across Europe as circular economy regulations intensify.

Copper Scrap Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 32.0 Bn |

| Current Market Value (2026) | US$ 42.4 Bn |

| Projected Market Value (2033) | US$ 67.6 Bn |

| CAGR (2026 - 2033) | 6.9% |

| Leading Region | Asia Pacific, 38% share |

| Dominant Scrap Type | Copper Wire Scrap, 40% share |

| Top-ranking End-user | Electrical & Electronics, 45% |

| Incremental Opportunity | US$ 25.2 Bn |

Companies Covered in Copper Scrap Market

- Aurubis AG

- Sims Limited

- Schnitzer Steel Industries, Inc.

- Commercial Metals Company

- European Metal Recycling Ltd.

- Glencore plc

- OmniSource Corporation

- Kuusakoski Group

- HKS Metals

- David J. Joseph Company

- Ames Copper Group

- Jain Resource Recycling Pvt. Ltd.

- KGHM Metraco S.A.

- Boliden AB

- Nucor Corporation

- Stena Recycling AB

- Umicore SA

- Metallix Refining

Frequently Asked Questions

The global copper scrap market is estimated at US$ 42.4 billion in 2026 and is forecast to reach US$ 67.6 billion by 2033, growing at a CAGR of 6.9%. The market grew at a historical CAGR of 4.8% from 2020 to 2025, with the acceleration reflecting intensifying energy transition copper demand and expanding circular economy regulatory mandates driving secondary copper supply chain investment.

Key drivers include the IEA-projected four-times increase in copper demand by 2040 under net-zero scenarios driven by EVs (83 kg copper per vehicle), wind turbines (25 tonnes each), and grid modernization, alongside the EU Circular Economy Action Plan and WEEE Directive mandating higher recycling rates that structurally increase secondary copper availability from electrical and electronic equipment.

Copper wire scrap dominates with approximately 40% market share, reflecting the International Copper Association's finding that electrical applications consume 65% of global copper demand, making end-of-life wire and cable the largest, most homogeneous, and highest-purity scrap stream. Premium grades, including Bare Bright and No. 1 Copper wire, trade at 85-98% of the LME cathode price, underscoring the segment's dominant commercial value.

Asia Pacific leads the market, anchored by China's position as the world's largest copper consumer and its growing domestic scrap generation base, Japan's world-class urban mining infrastructure under its Law for Promotion of Effective Utilization of Resources, and India's rapidly expanding manufacturing and EV-driven copper demand. The region's combined manufacturing output and energy transition ambitions make it the dominant copper scrap consumption and processing market globally.

The highest-value opportunities are in advanced urban mining and AI-powered scrap sorting, enabling 98%+ copper recovery from complex WEEE, and in securing renewable energy decommissioning scrap streams from first-generation wind and solar installations reaching end-of-life. IRENA projects millions of tonnes of decommissioning recyclables annually by the early 2030s, driving the copper scrap supply source for proactive recyclers.

Leading companies include Aurubis AG (Europe's largest copper recycler), Glencore plc, Boliden AB, Sims Limited, Schnitzer Steel Industries, Inc., Commercial Metals Company, European Metal Recycling Ltd., and Jain Resource Recycling Pvt. Ltd. These companies compete on scrap processing technology depth, global sourcing networks, LME pricing expertise, and vertical integration into downstream copper products manufacturing.