- Industrial Goods & Service

- Concrete Pump Market

Concrete Pump Market Size, Share, and Growth Forecast 2026 - 2033

Concrete Pump Market by Product Type (Stationary, Truck-Mounted, Others), Pump Type (Boom Pumps, Line Pumps), Power Source (Diesel, Electric, Hybrid), End-Use Industry (Residential, Commercial, Industrial, Infrastructure), by Regional Analysis, 2026 - 2033

Concrete Pump Market Size and Trend Analysis

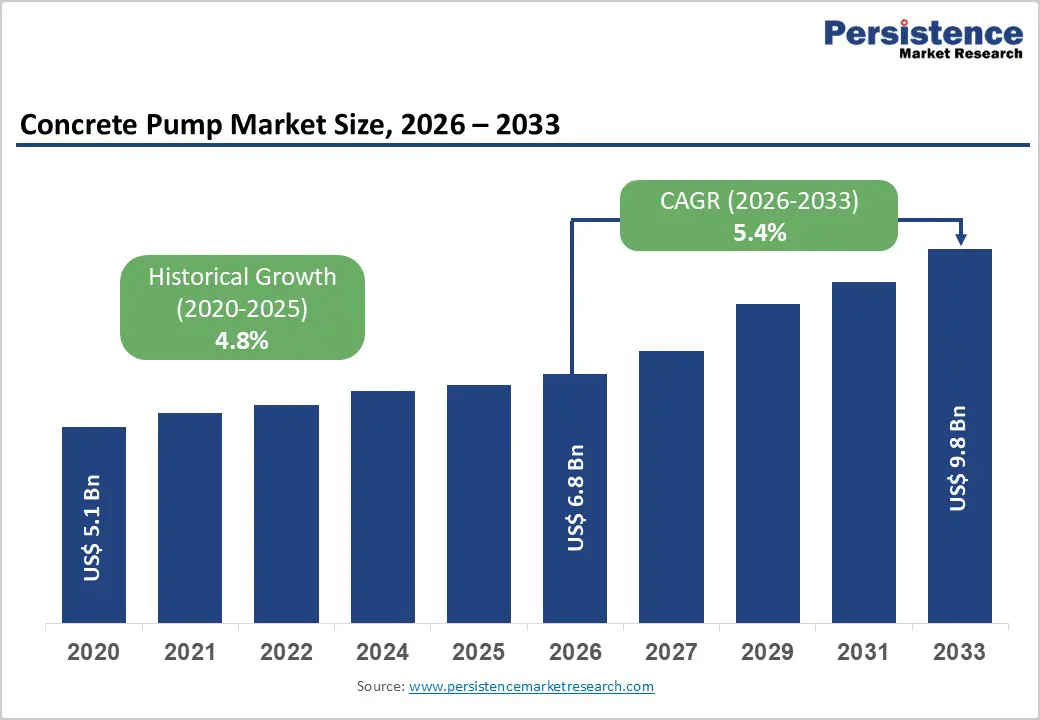

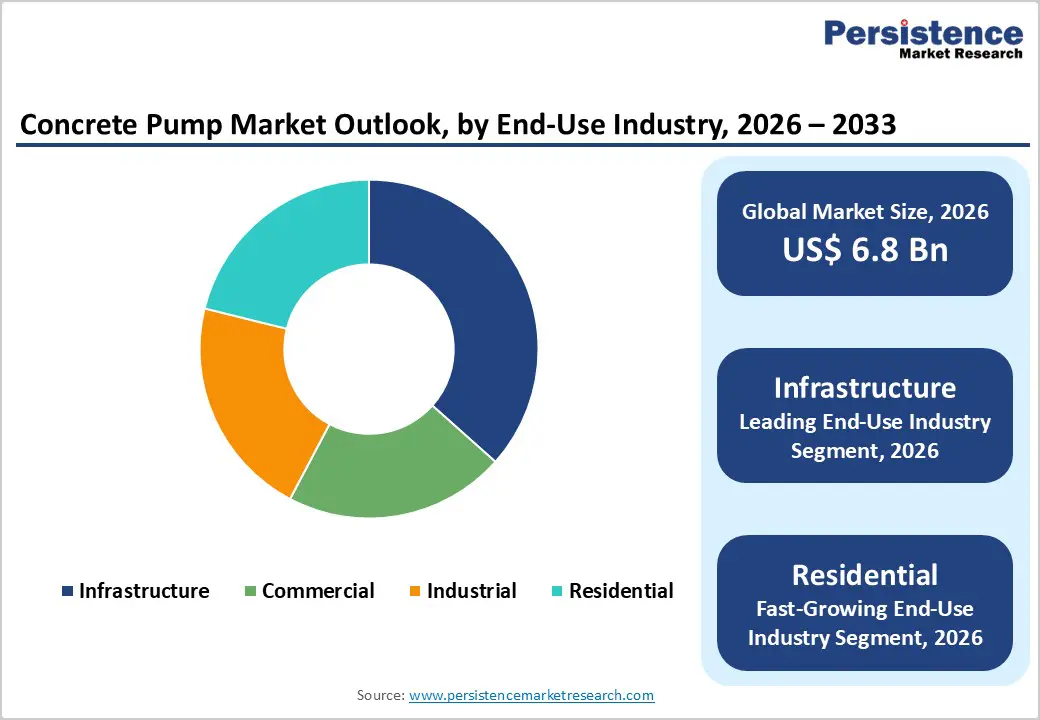

The global concrete pump market size is expected to be valued at US$ 6.8 billion in 2026 and projected to reach US$ 9.8 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Robust global construction activity is the primary catalyst driving the concrete pump market forward. Large-scale investments in infrastructure development, spanning transportation networks, residential housing, and urban renewal projects, are sustaining strong equipment demand. Government-backed stimulus programs across North America, Asia Pacific, and Europe have accelerated project timelines, prompting contractors to invest in high-efficiency concrete pumping equipment. The growing preference for mechanized concrete placement over traditional manual methods, driven by labor cost pressures and quality requirements, further reinforces market momentum.

Key Industry Highlights

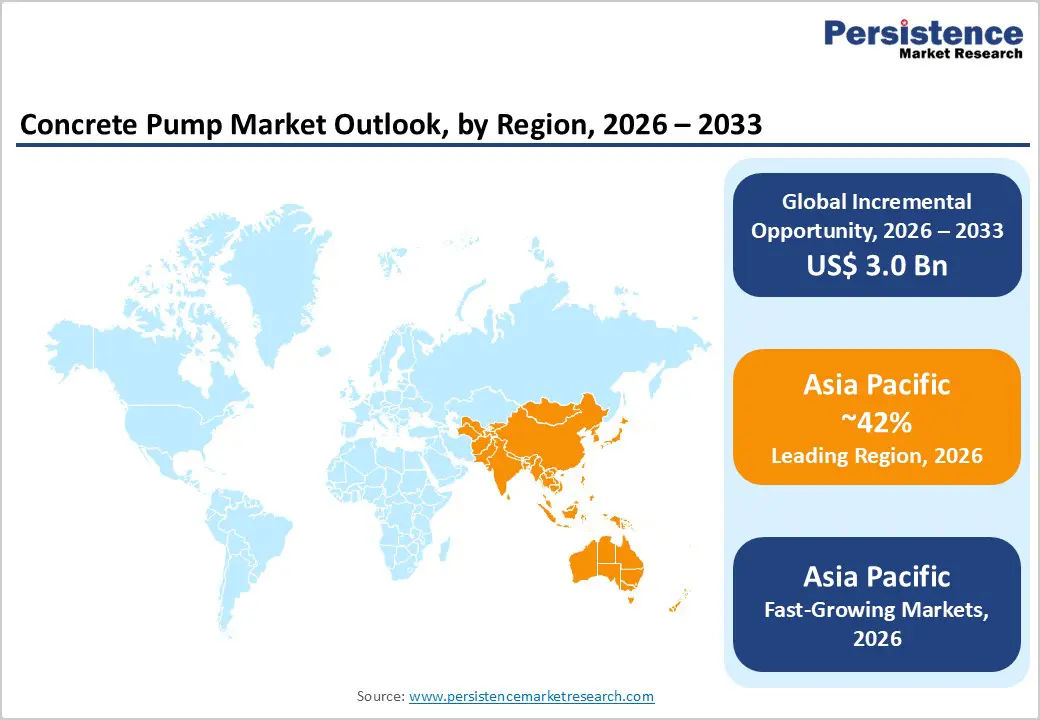

- Leading Region: Asia Pacific dominates the global concrete pump market with approximately 42% share in 2025, driven by China's urbanization mega-projects, India's infrastructure pipeline, and strong ASEAN construction momentum.

- Fastest Growing Region: The Middle East & Africa region is poised as the fastest-growing regional market (CAGR ~7.1%), fueled by Saudi Arabia's Vision 2030 megaprojects and escalating affordable housing demand across Sub-Saharan Africa.

- Dominant Segment: Truck-mounted concrete pumps command approximately 55% market share in 2025, underpinned by mobility advantages, rapid site deployment, and versatility across residential, commercial, and infrastructure applications.

- Fastest Growing Segment: The electric and hybrid concrete pump segment is the fastest growing, propelled by EU Stage V emissions regulations, urban low-emission zone mandates, and major OEM electrification investments targeting a CAGR exceeding 8.5% through 2033.

- Key Market Opportunity: ASEAN's US$ 210 billion+ infrastructure pipeline and Saudi Arabia's Vision 2030 megaprojects represent transformative demand opportunities for global concrete pump manufacturers with localized service capabilities through 2033.

| Key Insights | Details |

|---|---|

| Concrete Pump Market Size (2026E) | US$ 6.8 Billion |

| Market Value Forecast (2033F) | US$ 9.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Surge in Global Infrastructure Investment and Urbanization

One of the most significant drivers propelling the concrete pump market is the unprecedented wave of infrastructure investment globally. The U.S. Infrastructure Investment and Jobs Act, signed in 2021, committed US$ 1.2 trillion toward roads, bridges, rail, and broadband, with construction projects continuing to ramp up through 2026-2033. Similarly, the European Union's €1.8 trillion recovery fund, NextGenerationEU, allocates substantial portions to green and digital infrastructure. In Asia, China's continued Belt and Road Initiative investments and India's National Infrastructure Pipeline (NIP) targeting US$ 1.4 trillion in projects through 2025 are directly fueling demand for concrete pumping equipment, as contractors seek faster and more efficient concrete placement to meet aggressive project deadlines.

Rising Demand for High-Rise Residential and Commercial Construction

The global trend toward vertical urbanization, driven by land scarcity in metropolitan areas, is creating robust sustained demand for concrete pumps. By 2050, approximately 68% of the world's population is projected to live in urban areas, according to the United Nations Department of Economic and Social Affairs (UNDESA). This urban migration is intensifying demand for high-rise residential towers and commercial complexes, both of which require boom and stationary concrete pumps capable of delivering concrete at significant heights and volumes. The global commercial construction market, valued at approximately US$ 4.7 trillion in 2024, underlines the scale of opportunity. Concrete pumps, with their ability to deliver precise volumes at heights exceeding 200 meters, have become indispensable to modern high-rise construction workflows, reducing pour time and labor requirements substantially.

Restraints - High Capital Cost and Maintenance Burden

The significant upfront acquisition cost of concrete pumping equipment remains a material barrier to market expansion, particularly in price-sensitive developing economies. A truck-mounted boom pump can cost between US$ 300,000 and US$ 800,000, while stationary high-pressure pumps may exceed US$ 500,000. Beyond purchase prices, ongoing maintenance, including wear-part replacement for cylinders, pistons, and S-valves, adds considerable lifecycle costs. For small and mid-size contractors, this economics often render equipment ownership unviable, limiting market penetration. While rental models partially offset this barrier, rental fleet availability remains uneven across emerging regions, constraining market growth in high-potential geographies.

Shortage of Skilled Operators and Regulatory Compliance Complexity

Concrete pump operation demands trained professionals capable of managing hydraulic systems, boom positioning, and safety protocols. According to the European Construction Industry Federation (FIEC), the construction sector faces a shortage of approximately 1 million skilled workers across Europe as of 2024. This skills deficit reduces equipment utilization rates and increases accident risk. Furthermore, evolving occupational safety regulations, such as OSHA standards in the U.S. and EN 13000 crane safety standards adapted to pump operations in the EU, require ongoing compliance investment from both manufacturers and contractors, raising operational complexity and costs that dampen equipment adoption among smaller operators.

Opportunities - Electrification of Concrete Pumps: A Green Construction Imperative

The transition to electric and hybrid concrete pumps represents a compelling market opportunity aligned with global decarbonization mandates. The European Green Deal targets climate neutrality by 2050, with construction, accounting for approximately 36% of the EU's total energy consumption, under increasing regulatory scrutiny. Several countries, including Norway, Germany, and the United Kingdom, are actively introducing zero-emission construction equipment zones in urban areas. Major players such as Putzmeister Holding GmbH and Schwing GmbH have introduced electric pump variants, responding to accelerating contractor interest. According to the International Energy Agency (IEA), global spending on clean energy technologies, including electric construction equipment, is expected to exceed US$ 2 trillion annually by 2030, underscoring the scale of structural market shift toward electrification in the concrete pump segment.

Emerging Market Infrastructure Boom: Southeast Asia and the Middle East

Southeast Asia and the Middle East represent high-growth frontiers for concrete pump manufacturers. ASEAN nations collectively committed to over US$ 210 billion in infrastructure spending under their respective national development plans through 2030, spanning transportation, energy, and urban housing. In the Middle East, Saudi Arabia's Vision 2030 program is driving the construction of megaprojects, including NEOM, the Red Sea Project, and Qiddiya, with aggregate contracted construction value exceeding US$ 1.25 trillion. These large-scale, complex projects require advanced concrete pumping solutions, including ultra-high-pressure line pumps and long-reach boom configurations. Manufacturers capable of establishing regional service networks and localized support operations in UAE, Saudi Arabia, Vietnam, and Indonesia stand to capture significant market share as project activity accelerates through 2033.

Category-wise Analysis

Product Type Insights

The Truck-Mounted segment commands the leading position in the concrete pump market by product type, accounting for approximately 55% of total market share in 2025. The dominance of truck-mounted concrete pumps is underpinned by their superior mobility, rapid deployment capability, and operational versatility across diverse construction site conditions. These units, which integrate the pump mechanism directly onto a commercial truck chassis with an extendable boom, eliminate the need for separate towing and enable contractors to service multiple job sites within a single working day. Growing demand for medium-to-high-rise residential and commercial projects across North America, Europe, and Asia Pacific has reinforced adoption, as truck-mounted pumps can effectively deliver concrete at the heights and volumes required by these projects. The integration of telematics and remote monitoring systems in modern truck-mounted models has also enhanced uptime and predictive maintenance, further strengthening their market position.

Pump Type Insights

Boom pumps represent the leading segment within the pump type category, capturing approximately 62% market share in 2025. Boom pumps utilize a remote-controlled articulating robotic arm (boom) to place concrete precisely, significantly reducing labor requirements and enabling concrete delivery at heights and distances not achievable with traditional methods. Their deployment is particularly well-suited to high-rise buildings, large commercial complexes, and infrastructure projects such as bridges and dams. According to the American Concrete Pumping Association (ACPA), concrete pumping now accounts for a majority of ready-mix concrete placement in the United States, with boom pumps constituting the most widely rented and owned equipment class. Advances in remote control systems, carbon fiber boom arms reducing overall unit weight, and increased reach, some models now extending to 72 meters, have made boom pumps the preferred choice for contractors globally.

Power Source Insights

Diesel-powered concrete pumps remain the dominant segment in the power source category, holding approximately 68% of market share in 2025. Diesel's primacy is attributable to its superior energy density, widespread fuel availability, and the proven reliability of diesel hydraulic systems under demanding site conditions, including remote locations without access to grid electricity. Tier 4 Final and Stage V emission-compliant diesel engines have addressed earlier environmental concerns to a degree, prolonging regulatory viability in many markets. In regions such as Sub-Saharan Africa, South Asia, and parts of Southeast Asia, where grid reliability remains low, diesel is effectively the only practical power source. That said, the fastest-growing power source segment is Electric/Hybrid, driven by zero-emission zone regulations in European and major Asian cities, with manufacturers rapidly expanding their electric pump portfolios to capture this emerging demand.

Industry Insights

The Infrastructure segment leads the end-use industry category, accounting for approximately 35% of total concrete pump market share in 2025. Infrastructure projects, including highways, bridges, tunnels, dams, railways, ports, and airports, require large volumes of concrete placed at challenging angles and elevations, making high-capacity pumping equipment essential. National infrastructure stimulus packages have been particularly influential: the U.S. Bipartisan Infrastructure Law (2021) allocated US$ 110 billion for roads and bridges alone, while China's 14th Five-Year Plan (2021-2025) prioritized construction of 30,000 kilometers of new highways and significant high-speed rail expansion. These mega-projects directly drive procurement of stationary and truck-mounted concrete pumps with high-pressure delivery specifications. The fastest-growing end-use segment is Residential, supported by mass affordable housing programs in India, China, and across ASEAN nations.

Regional Insights

North America Concrete Pump Market Trends and Insights

North America accounted for approximately 24% of global concrete pump market share in 2025, with the United States being the dominant national market. The region's strength is anchored by sustained government capital expenditure on transportation infrastructure under the Infrastructure Investment and Jobs Act, which continues to unlock funding for bridge rehabilitation, highway construction, and transit expansion. The American Concrete Pumping Association (ACPA) reports strong equipment rental activity, reflecting contractor preferences for asset-light models. Digital integration, including GPS fleet tracking, telematics, and IoT-enabled pump diagnostics, is rapidly becoming standard among leading North American contractors.

Canada contributes notably through large residential construction programs in Ontario and British Columbia, while Mexico's nearshoring-driven industrial construction boom is expanding demand for concrete pumping equipment across manufacturing corridor states. The growing adoption of green building certifications, including LEED and WELL, is encouraging contractors to explore low-emission electric pump alternatives, positioning North America as a key adopter of next-generation pumping technologies through 2033.

Europe Concrete Pump Market Trends and Insights

Europe is characterized by a mature yet innovation-driven concrete pump market, with Germany, France, Italy, and the United Kingdom forming the core demand centers. Germany, home to globally recognized manufacturers Putzmeister Holding GmbH and Schwing GmbH, leads both in production and domestic deployment, underpinned by robust commercial and infrastructure construction activity. The EU's Renovation Wave Strategy aims to double the annual energy renovation rate of buildings, driving considerable concrete pump utilization in retrofit and deep renovation works.

Stringent Stage V non-road mobile machinery (NRMM) emission regulations enforced across the EU are accelerating the adoption of hybrid and electric pump models. Schwing GmbH and CIFA S.p.A. have both introduced electrically driven pump solutions to capture this regulatory-driven demand shift. The U.K., through its Net Zero Strategy, has set aggressive construction equipment electrification targets, further stimulating market innovation. Across Spain and France, post-pandemic urban renewal and social housing programs continue to sustain concrete pump demand, with public investment projects particularly prominent.

Asia Pacific Concrete Pump Market Trends and Insights

Asia Pacific is the largest and fastest-growing regional market for concrete pumps globally, commanding approximately 42% of global market share in 2025. China is the undisputed regional anchor, driven by massive ongoing urbanization, with the country's urban population expected to reach 1 billion by 2030 according to the National Bureau of Statistics of China. Domestic manufacturers such as Sany Heavy Industry Co., Ltd. and Zoomlion Heavy Industry Science & Technology Co., Ltd. benefit from deep local market penetration and cost-competitive manufacturing, while also expanding aggressively into international markets.

India represents the most dynamic growth frontier, with the government's Pradhan Mantri Awas Yojana (PMAY) targeting construction of 20 million affordable housing units and the National Infrastructure Pipeline driving US$ 1.4 trillion of project investment through 2025. Domestic player Ajax Engineering Private Limited has capitalized on this surge. Across Southeast Asia, rapid urbanization in Vietnam, Indonesia, and the Philippines is generating strong pump rental demand, with governments prioritizing smart city and transit-oriented development (TOD) programs that require high-capacity concrete placing solutions. Japan's market remains technology-forward, with Kyokuto Kaihatsu Kogyo Co., Ltd. advancing automation and remote-operation capabilities in pump design.

Competitive Landscape

The global concrete pump market is characterized by a semi-consolidated structure, where a limited number of large international manufacturers hold significant market share while numerous regional and niche producers compete in local markets. Large players benefit from extensive distribution networks, strong engineering capabilities, and established relationships with construction contractors. Meanwhile, smaller manufacturers often compete through cost-competitive offerings, customized equipment configurations, and localized after-sales service.

Competition in the market is largely driven by technological innovation, product reliability, and service efficiency. Manufacturers are focusing on extending boom reach, improving pumping efficiency, integrating advanced remote-control systems, and incorporating predictive maintenance features through digital monitoring technologies. Sustainability considerations are also influencing product development, including the introduction of electric and low-emission concrete pumps for urban construction environments. In addition, companies are increasingly adopting rental fleet expansion, equipment-as-a-service (EaaS) models, and strategic partnerships with ready-mix concrete suppliers to strengthen market presence and capture recurring revenue streams across construction projects.

Key Developments:

- June, 2025: Putzmeister Holding GmbH unveiled the BSA 1405 D Classic stationary concrete pump through its “Concrete Dastak Roadshow,” designed for reliable performance, easy operation, and low maintenance across residential buildings, bridges, and long-distance pumping applications.

- January, 2026: Ajax Engineering Limited launched UDAAN, a compact mobile concrete mixing solution at EXCON 2025, marking its entry into a new equipment category aimed at improving mobility, efficiency, and on-site concrete production for construction projects.

Companies Covered in Concrete Pump Market

- Putzmeister Holding GmbH

- Sermac S.p.A.

- Schwing GmbH

- Shantui Construction Machinery Co., Ltd.

- Schwing Stetter India Private Limited

- DY Concrete Pumps Inc.

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- Ajax Engineering Private Limited

- Sany Heavy Industry Co., Ltd.

- Kyokuto Kaihatsu Kogyo Co., Ltd.

- Liebherr-International AG

- Everdigm Corporation

- CIFA S.p.A.

- Alliance Concrete Pumps Inc.

- Concord Concrete Pumps Inc.

- KCP Heavy Industries Co., Ltd.

- Bauer Maschinen GmbH

- Junjin CS Co., Ltd.

Frequently Asked Questions

The global concrete pump market is estimated to reach US$ 6.8 billion in 2026 and is projected to grow to around US$ 9.8 billion by 2033 at a CAGR of 5.4%.

Growth is driven by rising infrastructure investments, rapid urbanization, increasing high-rise construction, and growing contractor preference for mechanized concrete placement solutions.

Asia Pacific leads the market with about 42% share in 2025, supported by strong infrastructure development and urbanization across China, India, and Southeast Asia.

A major opportunity lies in the development of electric and hybrid concrete pumps and expansion into fast-growing infrastructure markets in Southeast Asia and the Middle East.

Key players include Putzmeister Holding GmbH, Schwing GmbH, Sany Heavy Industry Co., Ltd., Zoomlion Heavy Industry Science & Technology Co., Ltd., CIFA S.p.A., Liebherr-International AG, Ajax Engineering Private Limited, Kyokuto Kaihatsu Kogyo Co., Ltd., Everdigm Corporation, and Sermac S.p.A.