- Pharmaceuticals

- Colorectal Cancer Screening Market

Colorectal Cancer Screening Market Size, Share, and Growth Forecast 2026 - 2033

Colorectal Cancer Screening Market by Test Type (Colonoscopy, Stool-based Tests, Others), by End-user (Hospitals & Clinics, Clinical Laboratories, Diagnostic Imaging Centers, and Others), by Regional Analysis, 2026 - 2033

Colorectal Cancer Screening Market Size and Trend Analysis

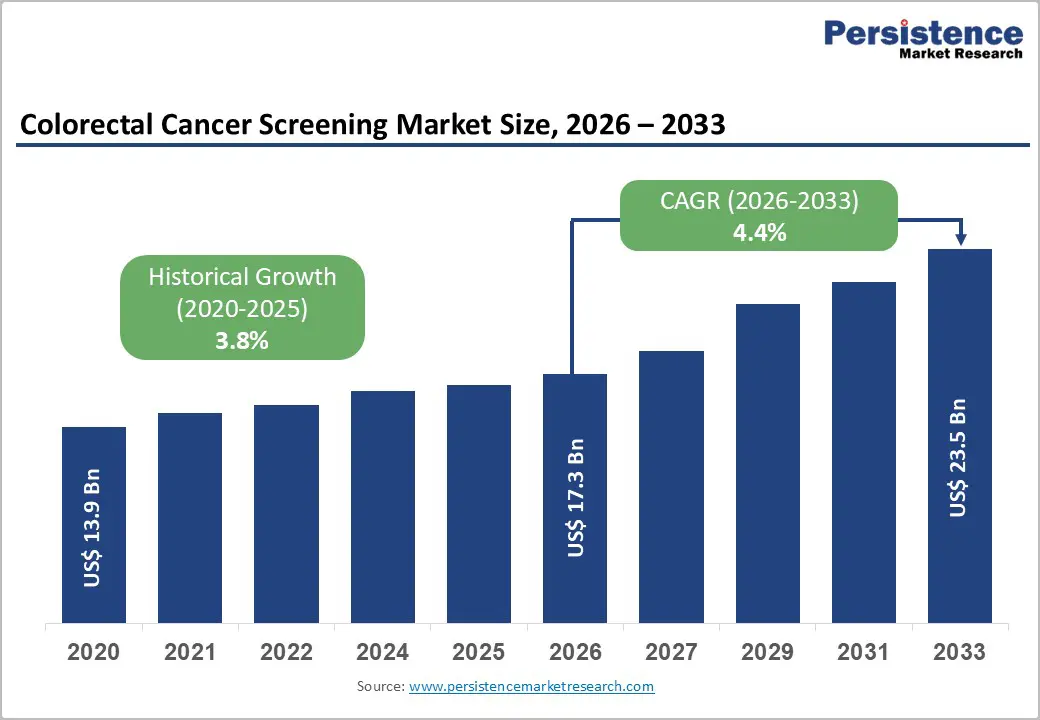

The global colorectal cancer screening market size is expected to be valued at US$ 17.3 billion in 2026 and projected to reach US$ 23.5 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

The global market is growing steadily due to the increasing global burden of colorectal cancer and the rising emphasis on early detection and preventive healthcare. Screening methods such as colonoscopy, fecal immunochemical tests (FIT), stool DNA tests, and imaging techniques are widely used to identify precancerous polyps and early-stage tumors. According to data published by the National Center for Biotechnology Information (NCBI) in April 2023, over 15.0 million colonoscopies are performed annually in the U.S., highlighting the strong adoption of screening procedures. Expanding screening guidelines, technological advancements, and growing awareness about early diagnosis are further driving market growth worldwide.

Key Industry Highlights:

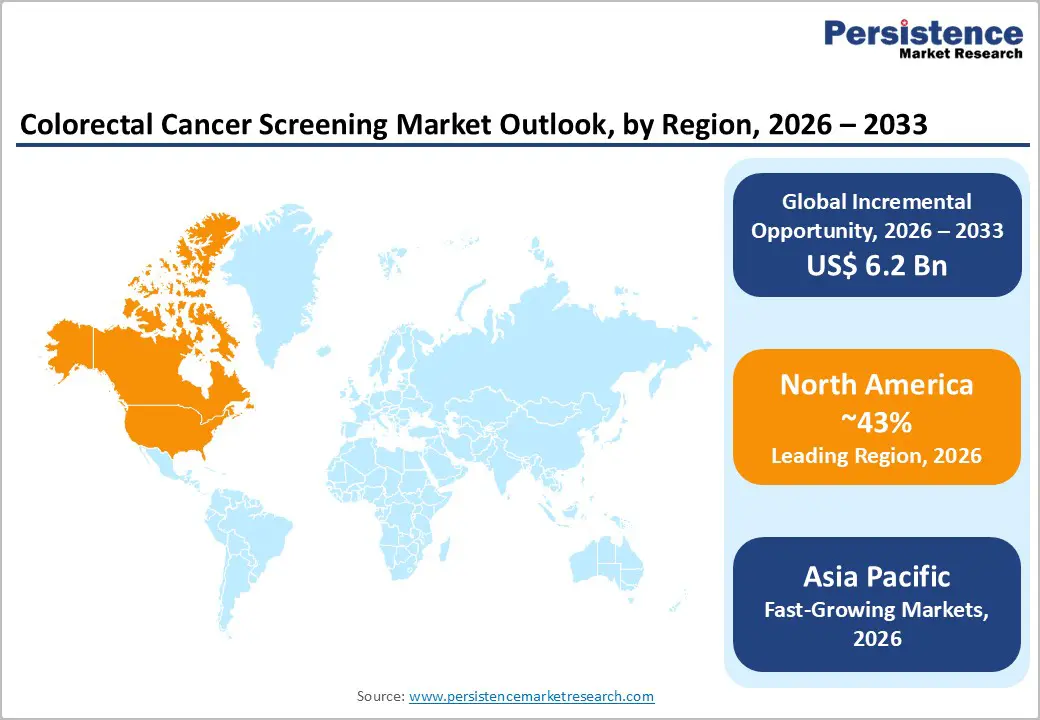

- North America leads colorectal cancer screening due to strong guidelines, widespread insurance coverage, high awareness, and early adoption of advanced screening technologies.

- Asia Pacific is the fastest-growing region due to ageing populations, rising colorectal cancer incidence, and expanding FIT-based population screening programs.

- Colonoscopy dominates screening test types because it provides both diagnosis and treatment, supported by strong guideline recommendations and follow-up after positive tests.

- Stool-based tests, including FIT, FOBT, and stool DNA assays, are fastest growing due to home sampling convenience and higher participation rates.

- Key opportunity lies in expanding blood-based and next-generation stool DNA screening tests with digital tools to improve adherence and early detection.

| Key Insights | Details |

|---|---|

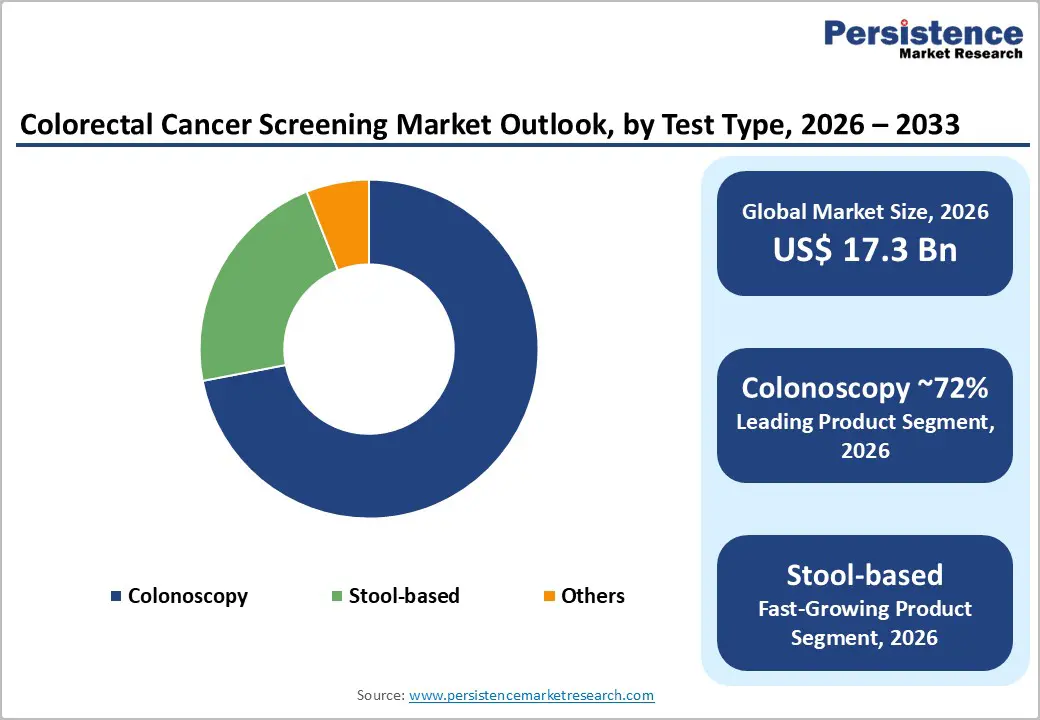

| Colorectal Cancer Screening Market Size (2026E) | US$ 17.3 billion |

| Market Value Forecast (2033F) | US$ 23.5 billion |

| Projected Growth CAGR (2026 - 2033) | 4.4% |

| Historical Market Growth (2020 - 2025) | 3.8% |

Market Dynamics

Drivers - Rising global colorectal cancer burden and shift to earlier screening

The foremost growth driver for the colorectal cancer screening market is the steadily increasing incidence and mortality burden of colorectal cancer worldwide, particularly in transitioning economies and younger cohorts. GLOBOCAN-based analyses estimate over 1.9 million new colorectal cancer cases and nearly 930,000 deaths in 2020, making the disease the third most diagnosed cancer and accounting for around 9-10% of all cancer deaths. In response to the rising incidence among adults under 50, guidelines from the U.S. Preventive Services Task Force (USPSTF) and the American College of Gastroenterology (ACG) now recommend routine screening for average-risk adults starting at 45 years, rather than 50, greatly expanding the eligible screening population. This policy shift, combined with national screening programs in Europe and Asia Pacific, is structurally increasing procedure volumes for colonoscopy and stool-based tests over the forecast period.

Restraints - Suboptimal screening uptake and access disparities

Despite strong evidence and national recommendations, screening participation remains below desired levels in many countries, constraining the full revenue potential of the colorectal cancer screening market. European studies show that, in numerous member states, fewer than 65% eligible adults have undergone recommended stool testing or colonoscopy, falling short of uptake targets set in the EU guidelines. Barriers such as limited public awareness, fear of invasive procedures, cultural stigma, and logistical challenges (time off work, travel to endoscopy centres) all reduce participation, particularly in lower-income and rural communities. In low- and middle-income regions, weaker primary-care systems and constrained colonoscopy capacity further limit program reach, slowing broader market penetration despite high disease burden.

Opportunities - Accelerated adoption of non-invasive stool DNA and blood-based assays

A major opportunity for market players lies in scaling next-generation non-invasive screening modalities that address adherence barriers and improve early detection. Multi-target stool DNA tests such as Cologuard®, developed by Exact Sciences Corporation, have demonstrated colorectal cancer sensitivities above 90% and specificities close to 90%, substantially outperforming traditional FIT for cancer detection while retaining at-home convenience. Recent clinical data on a second-generation stool-DNA test and the BLUE-C trial underpinning regulatory approvals for enhanced multitarget stool tests show sensitivities of 94-96% for colorectal cancer and improved detection of advanced precancerous lesions compared with FIT. In parallel, companies such as NOVIGENIX SA are advancing blood-based immune-transcriptomic assays (for example, the Colox® test and next-generation NGS-based versions) that have reported areas under the curve around 0.90 and sensitivities above 80% in early clinical studies, opening a pathway for high-acceptance, blood-draw-based screening solutions in primary care and occupational health settings.

Category-wise Analysis

Test Type Insights

By Test Type, colonoscopy remains the dominant modality, accounting for roughly 72% of the colorectal cancer screening market in 2025, reflecting its dual role as both a diagnostic and therapeutic procedure. Clinical guidelines from the USPSTF and ACG position colonoscopy every 10 years as a preferred screening option for average risk adults, given its ability to directly visualize the entire colon, remove precancerous polyps, and biopsy suspicious lesions in a single session. Studies consistently show colonoscopy’s high sensitivity for advanced adenomas and cancers and its association with substantial reductions often 50-60% in colorectal cancer incidence and mortality among screened populations. Although non-invasive stool-based tests are gaining traction, positive results still require follow up colonoscopy, sustaining procedure volumes. As health systems work through post pandemic backlogs and expand screening to younger age groups, colonoscopy is expected to maintain its leading share, particularly in North America and parts of Europe and Asia Pacific with robust endoscopy infrastructure.

End-user Insights

Among end-users, hospitals & clinics constitute the leading segment of the colorectal cancer screening market, capturing a substantial share of test ordering and procedure revenues. Large hospitals, academic medical centres, and integrated clinic networks typically house endoscopy suites where screening and diagnostic colonoscopies are performed, and they often coordinate follow-up care after positive stool tests. In many countries, hospital-based gastroenterology and oncology departments lead implementation of national screening programs, manage outreach to primary care physicians, and host multidisciplinary tumour boards that interpret findings and guide treatment pathways. As a result, hospitals and clinics are central nodes in the screening ecosystem, handling higher-value colonoscopy volumes and complex high-risk individuals, while clinical laboratories and diagnostic imaging centres play complementary roles by processing high-throughput FIT and stool-DNA tests and providing CT colonography and other alternative imaging modalities. Growing consolidation of healthcare delivery and the spread of integrated delivery networks are expected to strengthen the influence of hospital and clinic systems on technology selection and vendor partnerships.

Regional Insights

North America Colorectal Cancer Screening Market Trends and Insights

North America is the leading regional market for colorectal cancer screening, supported by high disease awareness, well established guidelines, and broad insurance coverage. In the U.S., the USPSTF and major professional societies recommend routine screening for average risk adults aged 45-75 years using colonoscopy, FIT, stool DNA tests, CT colonography, or flexible sigmoidoscopy, with coverage mandated for recommended options under federal health policy. National cancer trends reports indicate that more than 70% of adults aged 50-75 is up to date with colorectal cancer screening, one of the highest rates globally, underpinning strong procedural and test volumes.

The region also serves as an innovation hub for advanced screening technologies and data-driven care models. The U.S. Food and Drug Administration (FDA) has approved multi-target stool DNA tests, such as Cologuard®, and has recently cleared next-generation stool DNA assays with sensitivities near 94% for colorectal cancer and improved performance for advanced precancerous lesions compared with FIT. Health systems and vendors increasingly deploy electronic reminders, mailed FIT kits, telehealth counselling, and population health analytics to improve adherence and close gaps among underserved groups. With an advanced reimbursement framework and strong presence of leading players such as Exact Sciences Corporation, bioMérieux, Inc., and major endoscopy equipment manufacturers, North America is expected to retain its market leadership during the forecast period.

Asia Pacific Colorectal Cancer Screening Market Trends and Insights

Asia Pacific is the fastest-growing regional market for colorectal cancer screening, driven by rapid population ageing, westernization of diets and lifestyles, and increasing governmental recognition of colorectal cancer as a major public-health priority. Many countries in the region have experienced rising colorectal cancer incidence, particularly in urban populations, with incidence rates in Australia/New Zealand and parts of East Asia now comparable to those in high-income Western countries. In response, several governments have launched or expanded organized screening programs based on FIT, sometimes combined with risk-scoring tools such as the Asia Pacific Colorectal Screening (APCS) score to optimize colonoscopy referrals.

Japan pioneered FIT-based population screening in 1992, followed by South Korea, Taiwan, and Australia in the 2000s, and more recently New Zealand and Hong Kong, with participation rates gradually improving as awareness grows. Regional consensus guidelines recommend quantitative FIT every 1-2 years or colonoscopy every 10 years as preferred options, while also acknowledging emerging roles for stool-DNA and blood-based tests as evidence accumulates. As large countries such as China and India explore scaling up CRC screening within broader non-communicable disease strategies, vendors that provide cost-effective FIT kits, automated analyzers, colonoscopy solutions, and novel blood-based assays are expected to see above-average growth in this region.

Competitive Landscape

The global colorectal cancer screening market is moderately competitive, with a mix of diagnostics companies, biotechnology firms, and medical device manufacturers. Major players such as Exact Sciences, Olympus, and Fujifilm hold significant market positions through advanced screening tests and endoscopy technologies. Companies are increasingly investing in research and development to launch innovative non-invasive screening methods, including stool DNA and blood-based tests. Strategic partnerships, acquisitions, and expansion of laboratory networks are also common competitive strategies. The market is witnessing rising competition from emerging biotech companies developing molecular diagnostics and AI-enabled screening tools aimed at improving early detection and patient compliance.

Key Developments:

- In March 2026, Guardant Health, Inc. announced that its Shield™ blood-based colorectal cancer screening test became widely available for physician ordering through Quest Diagnostics’ nationwide network, expanding access to innovative blood-based CRC screening across the United States.

- In March 2025, Apollo Cancer Centres launched ColFit, a nationwide colorectal cancer screening program aimed at improving survival outcomes and lowering treatment costs across Apollo Hospitals in India.

- In July 2024, Guardant Health received FDA approval for its Shield™ blood test as a primary colorectal cancer screening option, paving the way for Medicare reimbursement and expanding non-invasive screening access.

Companies Covered in Colorectal Cancer Screening Market

- NOVIGENIX SA

- EIKEN CHEMICAL CO., LTD.

- Clinical Genomics Technologies Pty Ltd.

- Exact Sciences Corporation

- Epigenomics AG

- bioMérieux, Inc.

- Olympus Corporation

- KARL STORZ SE & Co. KG

- FUJIFILM Holdings America Corporation

- Cerner Corporation

- Others

Frequently Asked Questions

The global colorectal cancer screening market is expected to reach around US$ 17.3 billion in 2026.

Key drivers include rising colorectal cancer incidence, screening eligibility expansion to age 45, strong guideline support, and growing FIT and colonoscopy-based screening programs.

North America leads the colorectal cancer screening market due to strong awareness, favorable reimbursement policies, advanced endoscopy infrastructure, and innovation in screening technologies.

Key opportunity lies in expanding non-invasive stool DNA and blood-based liquid biopsy screening tests, alongside digital engagement tools, improving early detection.

Key companies include Novigenix, Eiken Chemical, Clinical Genomics, Exact Sciences, Epigenomics, bioMérieux, Olympus, Karl Storz, Fujifilm, Roche Diagnostics, Abbott, Guardant Health.