- Pharmaceuticals

- Cervical Cancer Vaccines Market

Cervical Cancer Vaccines Market Size, Share, and Growth Forecast 2026 - 2033

Cervical Cancer Vaccines Market by Vaccine Type (Bivalent Vaccines, Quadrivalent Vaccines, Nonavalent Vaccines), by Age Group (9-14 Years, 15-26 Years, Above 26 Years), End-user (Hospitals, Clinics, Vaccination Centers, Others), and Regional Analysis, 2026 - 2033

Cervical Cancer Vaccines Market Share and Trends Analysis

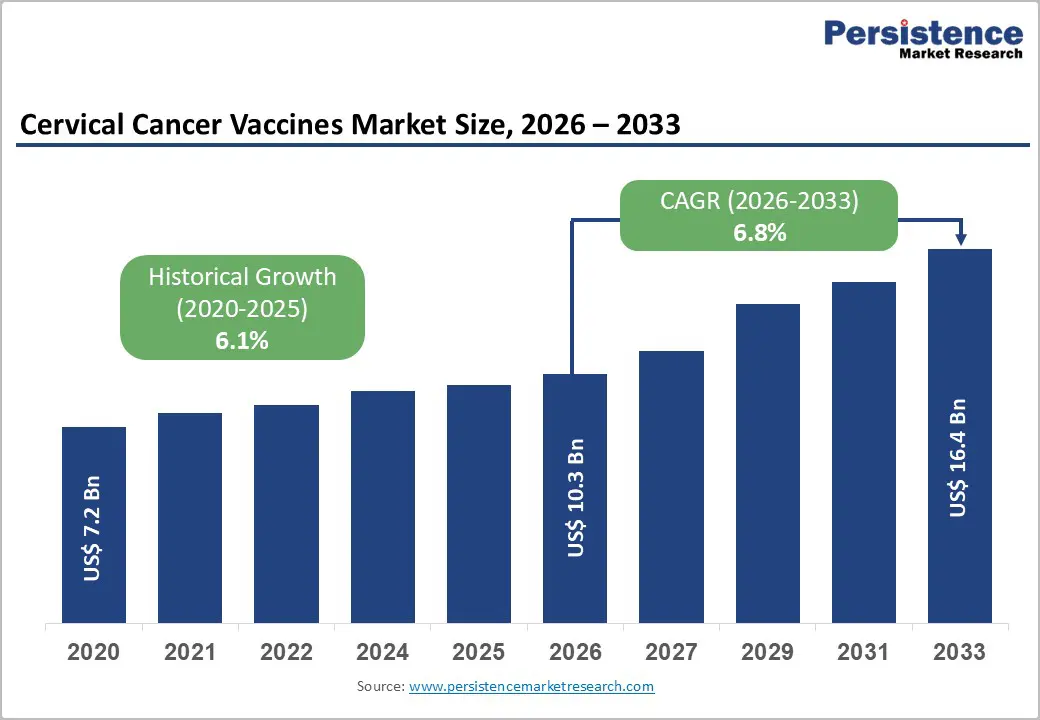

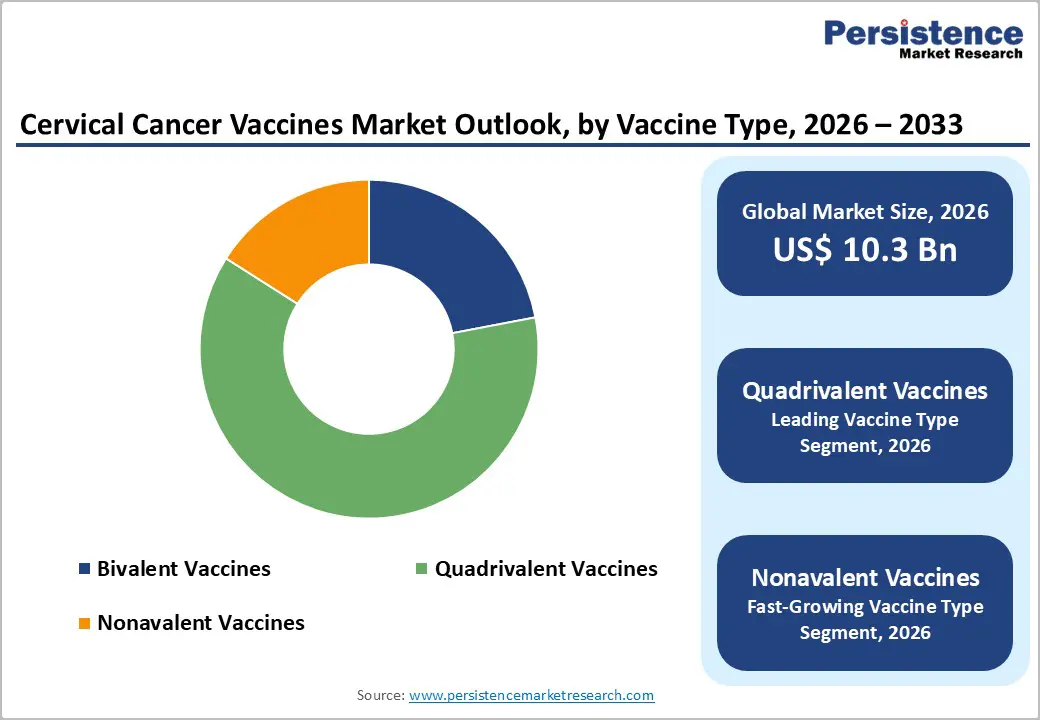

The global cervical cancer vaccines market size is expected to be valued at US$ 10.3 billion in 2026 and projected to reach US$ 16.4 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

Market growth is anchored in the high global burden of cervical cancer, strong evidence for human papillomavirus (HPV) vaccination effectiveness, and the expansion of national immunization programs supported by organizations such as WHO and Gavi, the Vaccine Alliance. WHO reports that cervical cancer is the fourth most common cancer among women, with around 660,000 new cases and 350,000 deaths in 2022, more than 90% of which occur in low- and middle-income countries. At the same time, Gavi estimates that scaled-up HPV vaccination campaigns have already protected 86 million girls and prevented over 1 million cervical cancer deaths in lower-income countries, underscoring both the life-saving potential of vaccines and the growing demand for bivalent, quadrivalent, and nonavalent HPV products.

Key Industry Highlights:

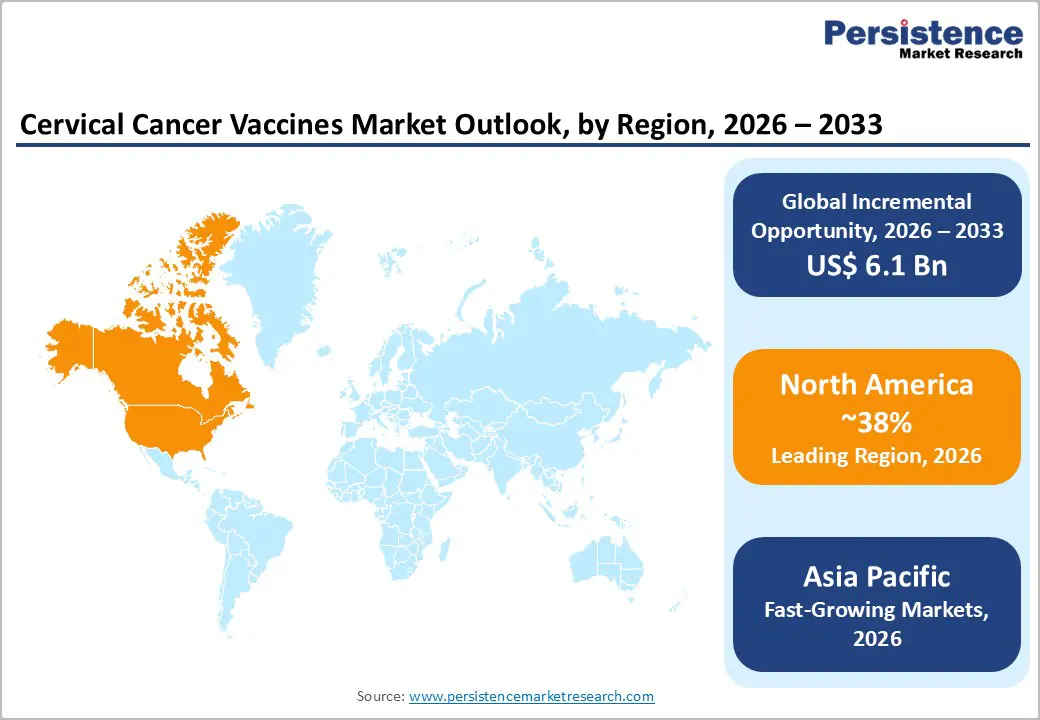

- North America leads the cervical cancer vaccines market, with around 38% share in 2025, supported by strong ACIP-aligned recommendations, broad reimbursement, and continued innovation around nonavalent HPV vaccination.

- The Asia Pacific region is the fastest-growing market, propelled by high cervical cancer burden, large adolescent cohorts, national immunization initiatives in India and China, and the rise of domestic vaccine manufacturers offering more affordable quadrivalent and nonavalent products.

- By Vaccine Type, Quadrivalent Vaccines dominate with an estimated 62% share in 2025, reflecting long-standing use of products like GARDASIL and CERVAVAC in national immunization programs and Gavi-supported campaigns worldwide.

- Nonavalent Vaccines are the fastest-growing segment, as broader genotype coverage and strong clinical efficacy data for products like GARDASIL 9 and Cecolin 9 support preferential guideline recommendations and increasing adoption across both high-income and emerging markets.

- Key market opportunities include expansion of single-dose HPV vaccination strategies, increased inclusion of boys and older age groups, and leveraging regional manufacturing hubs in India and China to improve affordability and coverage in high-burden, low-resource settings.

| Key Insights | Details |

|---|---|

| Cervical Cancer Vaccines Size (2026E) | US$ 10.3 billion |

| Market Value Forecast (2033F) | US$ 16.4 billion |

| Projected Growth CAGR (2026 - 2033) | 6.8% |

| Historical Market Growth (2020 - 2025) | 6.1% |

Market Dynamics

Drivers - High global burden of cervical cancer and WHO elimination initiative

A central growth driver for the cervical cancer vaccines market is the substantial and persistent global burden of cervical cancer and the concerted push by WHO and partner organizations to eliminate the disease as a public health problem. Cervical cancer is the fourth most common cancer in women, with approximately 660,000 new cases and 350,000 deaths recorded in 2022, and about 90% of these deaths occur in low- and middle-income countries where screening and treatment services remain limited. In response, WHO’s elimination strategy sets ambitious 90-70-90 targets by 2030, including 90% of girls fully vaccinated with HPV vaccine by age 15. Modelling studies suggest that achieving these targets could avert up to 74 million new cases and 62 million deaths by 2120, highlighting the critical role of vaccines and supporting long-term growth in vaccine demand across both high-income and Gavi-supported countries.

Robust clinical efficacy and expanded use of nonavalent and quadrivalent vaccines

Another important driver is the strong clinical efficacy profile of licensed HPV vaccines, especially nonavalent and quadrivalent products, and their increasingly broad use among girls, boys, and young adults. Clinical trials show that GARDASIL 9 (Human Papillomavirus 9-valent Vaccine, Recombinant) from Merck & Co., Inc. can prevent around 90% of cervical cancers caused by HPV by providing coverage against seven high-risk genotypes (including HPV 16, 18, 31, 33, 45, 52, 58) and two low-risk genotypes (6, 11). Efficacy analyses report over 96% protection against high-grade cervical, vulvar, and vaginal disease associated with the additional five oncogenic HPV types beyond those included in earlier quadrivalent formulations. Recent global guideline reviews also consistently recommend HPV vaccination often with nonavalent vaccines, as a cornerstone of cervical cancer prevention for girls and, increasingly, for boys, strengthening clinical and policy support for market expansion.

Restraints - Unequal access, low coverage in many low- and middle-income countries

Despite strong evidence and policy support, the cervical cancer vaccines market is constrained by unequal access and relatively low coverage in many low- and middle-income countries (LMICs). As of 2023, only about 27% of girls aged 9-14 years worldwide had received at least one dose of an HPV vaccine, with coverage especially low in some regions due to funding gaps, weak health systems, and competing health priorities. Challenges include reaching adolescent girls who are not routinely served by immunization programs, ensuring cold-chain capacity, training health workers, and addressing logistical barriers in school- and community-based campaigns. While Gavi and partners are helping to close these gaps, persistent inequities in coverage limit the near-term revenue potential in certain high-burden markets and slow progress toward global elimination goals.

Vaccine hesitancy, misinformation, and historical program setbacks

Vaccine hesitancy and misinformation surrounding HPV vaccines remain significant obstacles, particularly in some high-income and emerging markets where early controversies have undermined trust. Concerns about adverse events, often unrelated to vaccination but amplified by media and social networks, have led to temporary suspensions or sharp declines in uptake in countries such as Japan and in early programs in India, where a controversial pilot in 2008 triggered a nearly 10-year ban on HPV vaccination before more recent policy reversals. Although extensive safety monitoring by the WHO, CDC, and national regulatory agencies has consistently affirmed the strong safety profile of licensed HPV vaccines, lingering public concerns can dampen demand, disrupt national rollouts, and require sustained investment in communication and community engagement to rebuild confidence.

Opportunities - Shift to single-dose schedules and expansion of age and gender indications

One of the most promising opportunities for the cervical cancer vaccines market is the shift toward simplified dosing schedules and expanded target populations. In 2022, WHO’s Strategic Advisory Group of Experts (SAGE) endorsed a single-dose HPV vaccination schedule as an alternative to the traditional two- or three-dose regimens for girls aged 9-20 years, based on emerging evidence of non-inferior protection. Single-dose schedules significantly reduce programmatic complexity and costs, making it easier for countries, especially Gavi-supported LMICs to introduce and scale up HPV vaccination. At the same time, regulators such as the FDA and EMA continue to broaden label indications, with GARDASIL 9 now approved for use in females 9-45 years and males 9-45 years for the prevention of HPV-related cancers and disease. These developments create opportunities for manufacturers to expand volumes in both adolescent and adult segments and across genders.

Emergence of new manufacturers and high-valency vaccines in emerging markets

A second key opportunity arises from the entry of new vaccine manufacturers and the development of high-valency HPV vaccines in emerging markets such as India and China. The Serum Institute of India Pvt. Ltd. launched CERVAVAC, India’s first indigenously developed quadrivalent HPV vaccine, in January 2023, with strong backing from the Government of India and international partners, and plans for nationwide rollout targeting the country’s approximately 700 million women and girls. In China, Xiamen Innovax Biotech, Beijing Wantai BioPharm, and Walvax Biotechnology have developed domestic bivalent and, more recently, nonavalent vaccines such as Cecolin 9, which received approval from the National Medical Products Administration (NMPA) in 2025, making China the second country after the United States capable of independently supplying 9-valent HPV vaccines. These initiatives are expected to improve regional access and affordability, stimulate price competition, and support large-scale immunization in high-burden markets, thereby expanding overall market volume.

Category-wise Analysis

Vaccine Type Insights

Within the vaccine type, quadrivalent vaccines currently hold the leading position, representing an estimated 62% share of the cervical cancer vaccines market in 2025. Quadrivalent formulations such as GARDASIL and newer quadrivalent products like CERVAVAC from the Serum Institute of India target HPV types 6, 11, 16, and 18, thereby preventing both high-grade cervical lesions caused by oncogenic types 16 and 18 and genital warts caused by low-risk types 6 and 11. These vaccines have been widely deployed in national immunization programs since the late 2000s, with substantial post-marketing evidence demonstrating significant reductions in cervical intraepithelial neoplasia (CIN), genital warts, and HPV infections among vaccinated cohorts. Large-scale procurement by Gavi and high-income countries alike, combined with established cold-chain and dosing protocols, underpins the continued dominance of quadrivalent vaccines, even as Nonavalent Vaccines, which offer broader type coverage, are expected to post the fastest growth over 2025-2032.

End-user Insights

Across end-user segments, Hospitals constitute the leading channel in 2025, particularly in high- and middle-income countries, where hospital-based outpatient departments, affiliated clinics, and specialist gynecology and oncology centers serve as key vaccination points. In regions such as North America and Europe, hospitals and large integrated health systems play a central role in administering catch-up HPV doses to older adolescents and adults, integrating vaccination into broader sexual and reproductive health services and cancer prevention programs. Hospitals also act as hubs for public health campaigns and serve as referral centers for women identified through cervical screening initiatives who may benefit from vaccination as part of comprehensive care. While dedicated Vaccination Centers and primary care Clinics are vital in school-based and community-based programs, especially in LMICs, the concentration of specialized staff, cold-chain infrastructure, and record-keeping systems in hospitals ensures that they retain the largest revenue share among end users in the current market.

Regional Insights

North America Cervical Cancer Vaccines Market Trends and Insights

North America dominates the Cervical Cancer Vaccines market due to strong immunization programs, high healthcare spending, and early adoption of advanced vaccines. Countries such as the United States and Canada have well-established HPV vaccination initiatives supported by public health authorities, which significantly contribute to high vaccination coverage among adolescents and young adults. Government organizations such as the Centers for Disease Control and Prevention actively promote HPV vaccination through national immunization schedules and awareness campaigns aimed at preventing cervical cancer. Additionally, strong reimbursement policies and insurance coverage encourage widespread vaccine adoption across hospitals, clinics, and community vaccination centers. The region also benefits from the presence of major vaccine manufacturers and ongoing research activities focused on improving vaccine efficacy and expanding protection against multiple HPV strains. Increasing awareness about HPV-related cancers, along with rising screening programs and preventive healthcare initiatives, continues to support market growth. Furthermore, strong regulatory frameworks and rapid approval processes for innovative vaccines strengthen the region’s leadership in the cervical cancer vaccines market.

Asia Pacific Cervical Cancer Vaccines Market Trends and Insights

The Asia Pacific Cervical Cancer Vaccines market is emerging rapidly, driven by growing awareness of HPV-related cancers and expanding government vaccination initiatives in countries like India, China, and Australia.

The increasing incidence of cervical cancer, coupled with improving healthcare infrastructure and rising disposable incomes, is fueling vaccine adoption in urban and semi-urban areas. Governments and public health organizations are gradually integrating HPV vaccines into national immunization programs, particularly targeting adolescents and young women. Market growth is also supported by partnerships between local pharmaceutical companies and global vaccine manufacturers to improve supply and reduce costs. Awareness campaigns through schools, clinics, and social media platforms are educating the population about the benefits of early vaccination. Additionally, expanding cold-chain logistics and favorable regulatory approvals for new HPV vaccines are enabling broader reach. With increasing acceptance and affordability, the region is poised to witness significant growth in cervical cancer vaccine uptake over the next decade.

Competitive Landscape

The cervical cancer vaccines market is highly competitive, characterized by intense innovation and strategic collaborations. Key players focus on expanding product portfolios, developing next-generation vaccines, and improving multivalent coverage to address a broader range of HPV strains. Competition also revolves around pricing strategies, government tenders, and participation in national immunization programs. Companies are increasingly investing in clinical trials, regulatory approvals, and awareness campaigns to enhance market penetration.

Key Developments:

- In February 2026, the Government of India prepared and launched a nationwide Human Papillomavirus (HPV) vaccination programme to prevent cervical cancer among adolescent girls as a major public health initiative. The programme targeted girls aged 14 years, aiming to vaccinate around 1.15 crore girls annually under designated government health facilities.

- In October 2025, Vidal Health and the Serum Institute of India entered a strategic collaboration to improve access to the HPV vaccine as part of national cervical cancer prevention efforts. The partnership enabled Vidal Health’s digital platform to offer an end-to-end, cashless HPV vaccination experience, including digital appointment booking, consent processes, and certification without paperwork.

- In September 2025, Sunflower Therapeutics received its first milestone payment from its collaboration with SK bioscience after completing and demonstrating a technology transfer package covering multiple HPV serotypes, marking a key step in the commercialization of a 10-valent HPV vaccine.

Companies Covered in Cervical Cancer Vaccines Market

- Merck & Co., Inc.

- GlaxoSmithKline plc

- Serum Institute of India Pvt. Ltd.

- Walvax Biotechnology Co., Ltd.

- Beijing Wantai BioPharm

- Shanghai Zerun Biotechnology

- Xiamen Innovax Biotech

- Sanofi, Pfizer Inc.

- INOVIO Pharmaceuticals

- Astellas Pharma

- Emergent BioSolutions

Frequently Asked Questions

The global Cervical Cancer Vaccines Market is projected to reach approximately US$ 10.3 billion in 2026, reflecting continued expansion of HPV vaccination programs and broader use of quadrivalent and nonavalent vaccines worldwide.

A major demand driver is the high global burden of cervical cancer, around 660,000 new cases and 350,000 deaths in 2022 combined with WHO’s elimination strategy and strong evidence that HPV vaccines can prevent the vast majority of HPV-related cervical cancers.

North America currently leads the market with an estimated 38% share of global revenues in 2025, supported by robust ACIP-aligned recommendations, high coverage, and the extensive use of GARDASIL 9 across adolescent and adult populations.

Key opportunities include scaling single-dose HPV vaccination strategies, expanding coverage to boys and older age groups, and leveraging new domestic manufacturing capacity in India and China to increase access and affordability in high-burden markets.

Leading companies include Merck & Co., Inc., GlaxoSmithKline plc, Serum Institute of India Pvt. Ltd., Walvax Biotechnology Co., Ltd., Beijing Wantai BioPharm, Shanghai Zerun Biotechnology, Xiamen Innovax Biotech, Sanofi, Pfizer Inc., INOVIO Pharmaceuticals, Astellas Pharma, and Emergent BioSolutions.