- Advanced Materials

- Carbon Prepreg Market

Carbon Prepreg Market Size, Share, and Growth Forecast 2026 - 2033

Carbon Prepreg Market by Resin Type (Thermoset Resins, Thermoplastic Resins), by Product Form (Rolls, Sheets, Tapes), by End-Use (Aerospace & Defense, Automotive & Transportation, Wind Energy, Sports & Leisure, Marine, Industrial), by Regional Analysis, 2026 - 2033

Carbon Prepreg Market Size and Trend Analysis

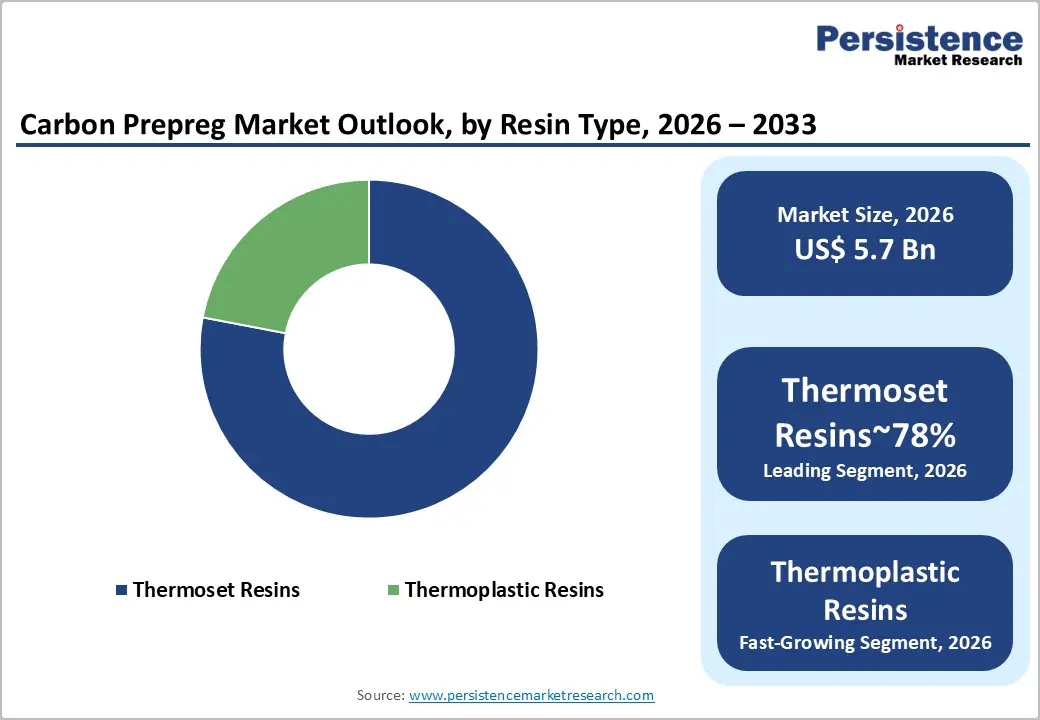

The global carbon prepreg market size is likely to be valued at US$ 5.7 Billion in 2026 and is expected to reach US$ 9.1 Billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033.

This growth trajectory is underpinned by escalating demand for lightweight, high-strength composite materials across aerospace and defense manufacturing, the accelerating transition to electric vehicles, and the expansion of global wind energy infrastructure.

Key Industry Highlights:

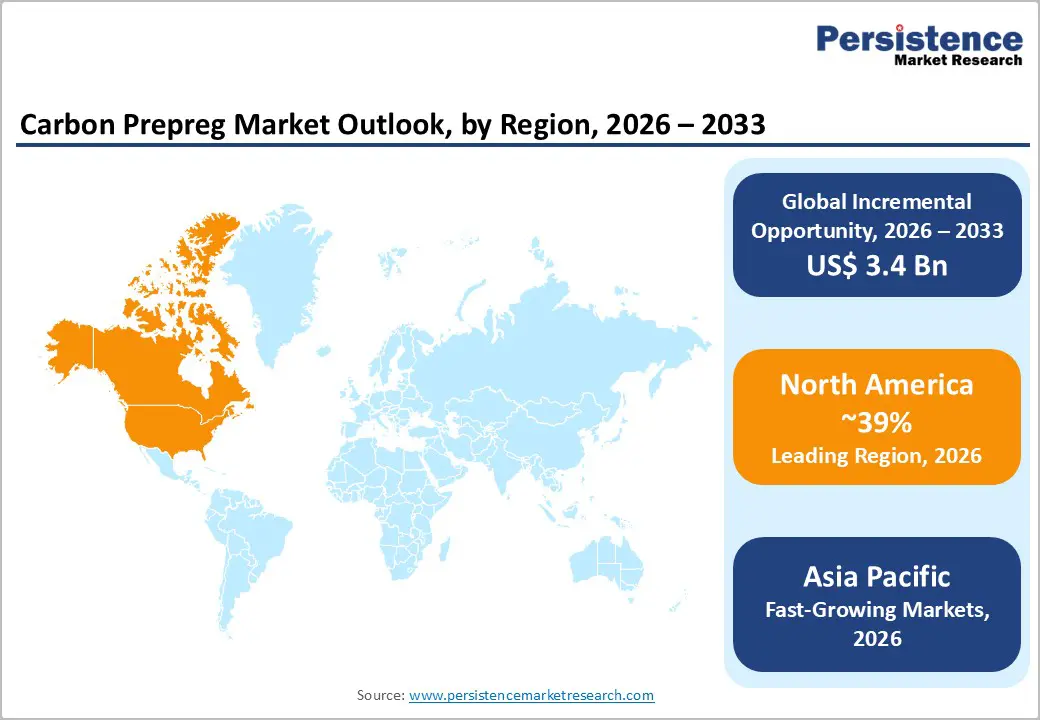

- Leading Region: North America leads the global Carbon Prepreg Market holding 39% share, anchored by the world's highest concentration of aerospace and defense composite manufacturers, including Boeing, Lockheed Martin, and Northrop Grumman, with U.S. DoD advanced materials spending reaching US$ 2.1 billion in 2024.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 9.7%, led by China's record 75.9 GW wind energy installation in 2023, Japan's tier-1 prepreg manufacturing leadership through Toray Industries and Teijin Limited, and India's expanding aerospace and defense composite programs through HAL.

- Leading Segment: Aerospace & Defense is the dominant end-use segment at approximately 44% of 2026 revenue, sustained by Boeing 787, Airbus A350, and F-35 Lightning II program prepreg consumption, with IATA projecting the global fleet to nearly double to 47,000 aircraft by 2043.

- Fastest-Growing Segment: Thermoplastic Resins represent the fastest-growing Resin Type segment, driven by EU ELV Directive recyclability requirements and Airbus Clean Aviation program commitments to thermoplastic welding in next-generation aircraft structures, with PEEK, PEKK, and PPS matrix systems gaining qualification traction.

- Key Opportunity: The key market opportunity lies in offshore wind energy expansion, where turbine blades exceeding 80 meters require carbon prepreg spar caps, supported by GWEC's reported 117 GW of installations in 2023 and REPowerEU's commitment to 510 GW of renewable capacity by 2030.

| Key Insights | Details |

|---|---|

| Carbon Prepreg Market Size (2026E) | US$ 5.7 Billion |

| Market Value Forecast (2033F) | US$ 9.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 5.4% |

Market Dynamics

Drivers - Aerospace and Defense Procurement Expansion Anchoring Structural Prepreg Demand

The aerospace and defense sector continues to be the most important driver for the Carbon Prepreg Market. This is mainly due to the growing need to reduce aircraft weight while meeting strict safety, durability, and fire-resistance standards set by regulators such as the FAA and EASA. The recovery of commercial aviation after the pandemic has increased aircraft production rates.

Airbus, for example, plans to produce 75 A320-family aircraft per month by 2026, with each aircraft requiring large volumes of thermoset prepreg in key structural components. On the defense side, the U.S. Department of Defense invested around US$ 2.1 billion in advanced materials research in 2024, supporting programs like the F-35 and next-generation aircraft. These combined commercial and military demands are creating steady and long-term growth opportunities for prepreg manufacturers across global markets.

Automotive Lightweighting Mandates and Electric Vehicle Architecture Accelerating Prepreg Adoption

Strict emission regulations are pushing automotive manufacturers to reduce vehicle weight and improve energy efficiency, increasing the use of carbon fiber prepreg in structural components. The European Union’s target of 93.6 g CO2/km by 2030 is forcing automakers to adopt lightweight materials across their vehicle platforms. Carbon fiber prepreg, once limited to luxury and sports cars, is now expanding into broader vehicle segments due to advancements in manufacturing technologies such as out-of-autoclave processing and high-pressure resin transfer molding.

These technologies reduce production time and cost, making prepreg more accessible. Additionally, electric vehicles create further demand, as heavy batteries require lightweight materials to maintain performance and range. Leading companies like BMW and Toyota are actively developing carbon fiber-based designs, demonstrating the growing importance of prepreg materials in the future of automotive manufacturing.

Restraints - High Raw Material and Processing Costs Limiting Adoption Beyond Premium Segments

High production costs remain a major challenge for the widespread adoption of carbon prepreg materials. The manufacturing process involves expensive raw materials such as polyacrylonitrile (PAN)-based carbon fiber, along with energy-intensive processing stages like oxidation and carbonization. In addition, thermoset prepregs require controlled cold storage, which adds to logistics and operational costs.

According to the National Renewable Energy Laboratory (NREL), carbon fiber can cost eight to twelve times more per kilogram than steel, making it less attractive for cost-sensitive industries. As a result, industries such as construction, consumer goods, and mass-market automotive applications often prefer cheaper alternatives such as aluminum or glass fiber. This cost barrier slows down the expansion of the Carbon Prepreg Market into high-volume applications, limiting its growth mainly to premium and performance-driven sectors where cost is less of a concern.

Recyclability Limitations and End-of-Life Regulatory Pressure on Thermoset Systems

Recycling challenges associated with thermoset prepreg materials are becoming a growing concern for the industry. Thermoset resins such as epoxy, bismaleimide, and cyanate ester cannot be remelted or reshaped once cured, making recycling difficult. This creates issues in meeting increasing environmental regulations, especially in Europe, where policies like the End-of-Life Vehicles Directive are becoming stricter.

New frameworks such as the Carbon Border Adjustment Mechanism are also increasing pressure on manufacturers to improve sustainability. Although recycling methods like solvolysis and pyrolysis exist, they are not yet commercially viable at a large scale. As a result, companies face challenges in managing production waste and end-of-life composite materials. These limitations are encouraging some manufacturers to consider thermoplastic alternatives, which are easier to recycle, thereby slowing the growth of thermoset prepreg demand in certain applications.

Opportunities - Offshore Wind Energy Infrastructure Expansion Creating Large-Scale Prepreg Demand

The rapid growth of offshore wind energy is creating a strong opportunity for the Carbon Prepreg Market. Modern wind turbine blades are becoming larger, often exceeding 80 meters in length, and require carbon prepreg materials to ensure strength, durability, and lightweight performance. Leading companies such as Vestas, Siemens Gamesa, and GE Renewable Energy rely on carbon prepreg for critical blade components like spar caps.

According to the Global Wind Energy Council, global wind capacity additions reached 117 GW in 2023, with offshore wind growing quickly. Government policies such as the U.S. Inflation Reduction Act and the EU’s REPowerEU plan are supporting large-scale renewable energy investments. Each turbine requires significant amounts of prepreg material, creating consistent demand. As countries continue to expand clean energy infrastructure, prepreg manufacturers with strong wind energy product offerings can benefit from long-term, policy-driven growth opportunities.

Thermoplastic Prepreg Technology Unlocking Automated Manufacturing and Recyclable Composite Architectures

Thermoplastic prepreg technology is emerging as a key growth opportunity for the market. Unlike thermoset systems, thermoplastic materials can be reshaped, welded, and recycled, making them more sustainable and compliant with evolving environmental regulations. Advanced thermoplastic resins such as PEEK, PPS, and PEKK are gaining attention across aerospace and automotive industries. Airbus is actively developing thermoplastic composite structures under its Clean Aviation program, aiming to reduce weight and production costs.

The automotive companies like BMW and Toyota are investing in thermoplastic-based components. Large research initiatives such as Clean Sky 2 have already demonstrated the effectiveness of these materials in aircraft structures. Major industry players, including Toray, Solvay, and Teijin, are expanding their thermoplastic prepreg portfolios to capture this growing demand. This shift toward recyclable and automated composite solutions is expected to significantly transform the future of the Carbon Prepreg Market.

Category-wise Analysis

Resin Type Insights

Within the Resin Type segment, Thermoset Resins hold the leading position, accounting for around 78% of total segment revenue in 2026. This strong share reflects their long-standing use in aerospace applications, where epoxy, bismaleimide, and cyanate ester systems have built decades of certified performance under strict regulatory standards set by the FAA and EASA. Thermoset carbon prepreg offers high out-of-plane strength, excellent bonding between fiber and resin, and proven durability under mechanical and thermal stress, making it ideal for primary aircraft structures.

Major manufacturers such as Boeing and Airbus continue to rely on thermoset epoxy prepregs for key components like fuselage skins, wing covers, and tail sections. Although thermoplastic prepregs are growing quickly due to recyclability and faster processing benefits, thermoset systems are expected to maintain their dominance, as aerospace material qualification cycles remain long and complex.

Product Form Insights

Among Product Form categories, Rolls account for the largest share, contributing about 52% of total segment revenue in 2026. Roll-format carbon prepreg is widely preferred for automated manufacturing processes such as Automated Fiber Placement (AFP) and Automated Tape Laying (ATL), which are used by leading aerospace companies including Boeing, Airbus, Leonardo, and Safran.

These automated systems require materials with consistent roll structure, uniform resin distribution, and stable handling properties to ensure efficient and high-quality production. Equipment manufacturers like Electroimpact and MTorres highlight that AFP systems can achieve deposition rates of over 100 kg per hour, making roll-format prepreg essential for large-scale composite manufacturing. As aircraft production rates recover and increase, particularly for programs like the 737 MAX and A320neo families, demand for roll-format prepreg is expected to remain strong and continue supporting high-volume aerospace manufacturing.

End-user Insights

In the End-Use segment, Aerospace & Defense leads the market, accounting for approximately 44% of total revenue in 2026. This dominance is driven by the sector’s need for materials that offer high strength while minimizing weight, a requirement that carbon prepreg fulfills effectively. Programs such as the F-35 Lightning II, produced by Lockheed Martin, are among the largest consumers of advanced carbon prepreg in military applications.

In the commercial sector, Boeing’s 787 Dreamliner stands out, with over 50% of its structure made from composite materials, including extensive use of carbon prepreg in fuselage and wing components. According to the International Air Transport Association (IATA), the global aircraft fleet is expected to grow to over 47,000 by 2043. This projected expansion indicates a long-term and steady demand for aerospace-grade carbon prepreg materials across both commercial and defense aviation sectors.

Regional Insights

North America Carbon Prepreg Market Trends

North America continues to lead the global Carbon Prepreg Market, supported by a well-established aerospace and defense manufacturing base. The United States is home to major industry players such as Boeing, Lockheed Martin, Northrop Grumman, and Raytheon Technologies, all of which are key consumers of high-performance carbon prepreg materials. In addition, companies like Hexcel Corporation and Cytec Solvay Group operate major prepreg production facilities in the region, ensuring a stable domestic supply for critical programs.

Government support further strengthens the market, with initiatives like the U.S. Department of Energy’s Composites Manufacturing for Energy Applications program funding research in advanced composites for automotive and energy sectors. The National Science Foundation also supports innovation through funding at leading institutions such as MIT, Georgia Tech, and the University of Michigan. These combined efforts create a strong pipeline for advanced material development and sustained market growth.

Europe Carbon Prepreg Market Trends

Europe is the second-largest market for carbon prepreg, driven by a strong and integrated aerospace manufacturing ecosystem centered around Airbus operations in France, Germany, Spain, and the United Kingdom. Germany plays a key role as a hub for composite production, hosting major companies like SGL Carbon and Solvay, while also supporting demand from automotive leaders such as BMW, Daimler, and Volkswagen focused on lightweight materials to meet emission targets.

Policy support is also a major growth driver, with initiatives like Clean Aviation, Clean Sky 2, and REPowerEU promoting innovation in aerospace and renewable energy sectors. Airbus aims to increase composite content in future aircraft, reinforcing prepreg demand. At the same time, Europe’s push for renewable energy, including offshore wind targets of up to 300 GW by 2050, is expected to drive long-term demand for prepreg materials used in wind turbine components.

Asia Pacific Carbon Prepreg Market Trends

Asia Pacific is the fastest-growing region in the Carbon Prepreg Market, supported by rapid expansion in aerospace, electric vehicles, and renewable energy sectors. Japan plays a leading role in advanced material production, with companies like Toray Industries, Teijin, and Mitsubishi Chemical supplying globally qualified carbon prepreg systems to major aerospace manufacturers. China is expanding its domestic aerospace capabilities through programs like COMAC’s C919 and C929, while also promoting advanced materials under its “Made in China 2025” initiative.

The country’s strong growth in wind energy, with record installations, is further driving prepreg demand. India is also emerging as a key market, supported by government initiatives such as the UDAN scheme and defense programs like HAL’s Tejas aircraft. Additionally, ASEAN countries, including Malaysia and Singapore are attracting aerospace manufacturing and maintenance investments, contributing to regional market expansion.

Competitive Landscape

The global carbon prepreg market is moderately consolidated, with leading players such as Hexcel Corporation, Toray Industries, Solvay, Teijin, and Mitsubishi Chemical accounting for a significant share of total revenue. These companies maintain their competitive advantage through advanced resin technologies, long-term aerospace certifications, and integrated carbon fiber supply chains that help control costs and ensure quality.

Their strategic focus includes expanding thermoplastic prepreg offerings, developing out-of-autoclave processing methods, and increasing production capacity, especially in Asia Pacific. Mid-sized players like SGL Carbon, Gurit, and Chomarat Group compete by specializing in applications across wind energy, marine, and industrial sectors. The market is also witnessing the emergence of new business models, including prepreg-as-a-service and digital tracking systems that improve material traceability and production efficiency, making the competitive landscape increasingly dynamic and innovation-driven.

Key Developments:

- In August 2024: Teijin introduced the Tenax Ultra-light carbon fiber prepreg series designed for advanced aerospace structures, enabling significant weight reduction and improved fuel efficiency. The product targets next-generation aircraft platforms by enhancing mechanical performance beyond conventional thermoset prepreg systems.

- In April 2024: Toray commercialized an advanced carbon fiber prepreg featuring improved thermal conductivity and superior resin infusion properties, enhancing manufacturing efficiency and component quality. The innovation supports aerospace and industrial composite applications requiring faster processing and better heat management performance.

- In January 2023: Hexcel expanded its U.S. prepreg manufacturing capacity to strengthen supply chain reliability for aerospace customers like Boeing and Airbus. The move supports rising aircraft production rates and ensures consistent availability of high-performance composite materials for critical structural programs.

Companies Covered in Carbon Prepreg Market

- Hexcel Corporation

- Toray Industries, Inc.

- Solvay S.A.

- Teijin Limited

- Mitsubishi Chemical Group Corporation

- SGL Carbon

- Gurit Holding AG

- Chomarat Group

- Advanced Composites Group Ltd.

- Park Aerospace Corp.

- Arvind Composite

- Bharat Composites

- FIBERMAX

- ACP COMPOSITES, INC.

- Bhor Chemicals and Plastics Pvt. Ltd.

Frequently Asked Questions

The global Carbon Prepreg Market is valued at US$ 5.7 Billion in 2026 and is forecast to reach US$ 9.1 Billion by 2033, registering a forecast period CAGR of 6.9%. The market recorded a historical CAGR of 5.4% between 2020 and 2025, reflecting consistent structural demand from aerospace and industrial end-use sectors.

The principal demand drivers are accelerating aerospace and defense aircraft procurement, with Airbus targeting 75 A320-family aircraft per month by 2026, and stringent vehicle emissions regulations such as the EU's 93.6 g CO₂/km fleet target by 2030, which are compelling automotive OEMs to integrate carbon fiber prepreg for structural lightweighting in both conventional and electric vehicle platforms.

The Aerospace & Defense segment leads with approximately 44% of End-Use segment revenue in 2026, driven by carbon prepreg's critical role in Boeing 787 Dreamliner, Airbus A350, and F-35 Lightning II structures. The International Air Transport Association (IATA) projects the global aircraft fleet to nearly double to 47,000 aircraft by 2043, ensuring sustained long-term segment leadership.

North America leads the global Carbon Prepreg Market, driven by the concentration of leading aerospace and defense manufacturers including Boeing, Lockheed Martin, and Northrop Grumman, and supported by U.S. Department of Defense advanced materials investment of US$ 2.1 billion in 2024. Domestic prepreg leaders Hexcel Corporation and Cytec Solvay Group maintain U.S. production facilities serving these strategic customers.

Offshore wind energy infrastructure expansion represents the most high-value structural opportunity, with modern turbine blades exceeding 80 meters requiring carbon prepreg spar caps and the Global Wind Energy Council (GWEC) reporting 117 GW of global wind capacity additions in 2023. Policy support from the U.S. Inflation Reduction Act and EU REPowerEU's 510 GW renewable target by 2030 secures a durable, policy-backed demand pipeline.

The leading companies in the global Carbon Prepreg Market include Hexcel Corporation, Toray Industries, Inc., Solvay S.A., Teijin Limited, Mitsubishi Chemical Group Corporation, SGL Carbon, Gurit Holding AG, Chomarat Group, Park Aerospace Corp., Advanced Composites Group Ltd., Arvind Composite, Bharat Composites, FIBERMAX, ACP COMPOSITES, INC., and Bhor Chemicals and Plastics Pvt. Ltd., among others operating across global aerospace, automotive, wind energy, and industrial composite applications.