- Advanced Materials

- Bio LPG Market

Bio LPG Market Size, Share, and Growth Forecast 2026 - 2033

Bio LPG Market by Feedstock (Bio-oil, Sugar-based, Biogas, Agricultural Residue, Industrial and Household Waste), Application (Transportation, Aviation, Power Generation, Residential & Commercial Cooking, Other), End Use (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

Bio LPG Market Size and Trend Analysis

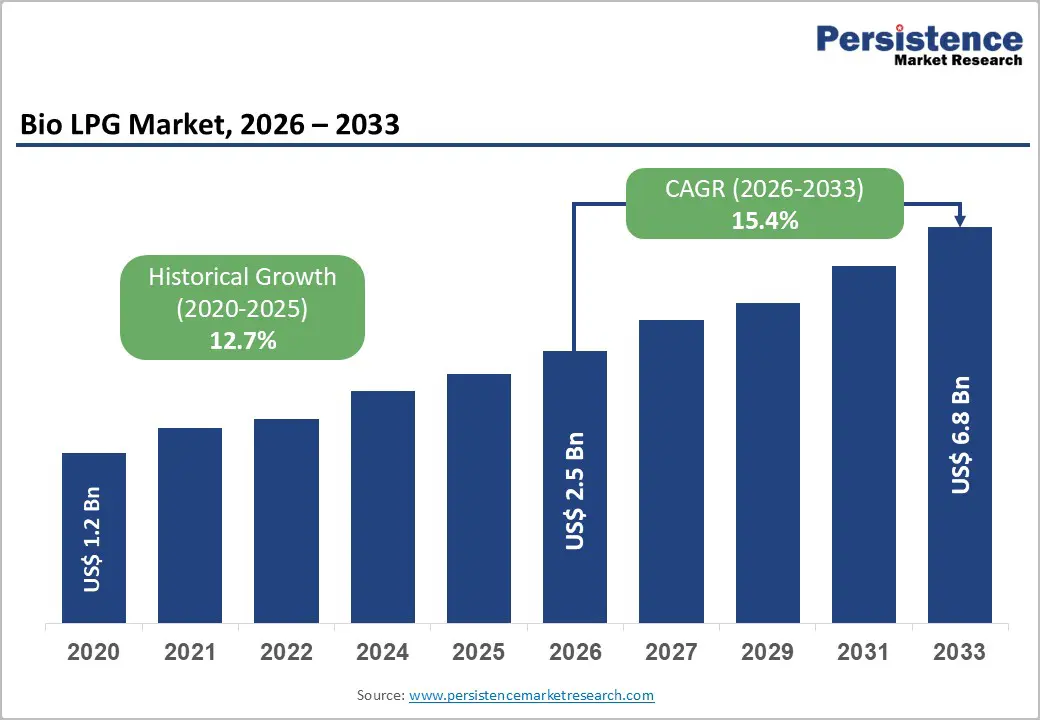

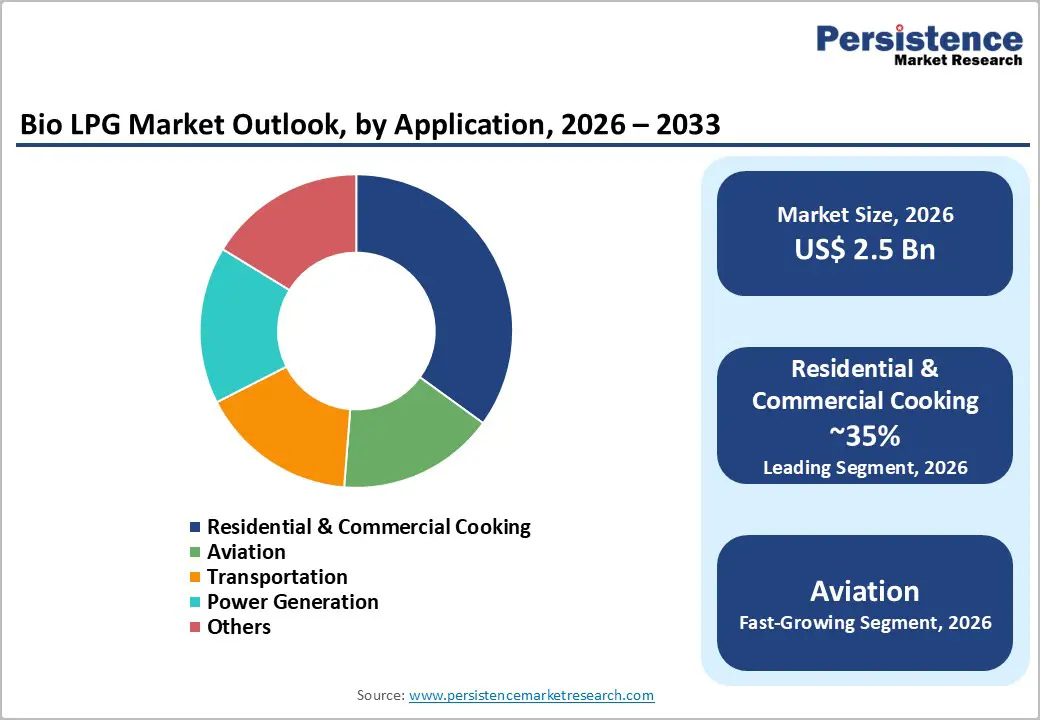

The global bio LPG market is valued at US$ 2.5 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, growing at a CAGR of 15.4% between 2026 and 2033.

This robust growth is primarily driven by accelerating global decarbonization mandates, the rapid expansion of biofuel blending requirements across the European Union, the United States, and major Asia-Pacific economies, and Bio LPG's unique advantage as a chemically identical, drop-in substitute for conventional LPG requiring no infrastructure modifications.

The International Energy Agency (IEA) has confirmed that EU biogas and biomethane production grew 14% year-on-year in 2024, underpinning feedstock availability for Bio LPG synthesis. Furthermore, the ongoing U.S.-Iran conflict, which has disrupted 1.5 mb/d of LPG exports through the Strait of Hormuz as of March 2026 per IEA data, is structurally accelerating the urgency of renewable LPG alternatives across import-dependent regions.

Key Market Highlights

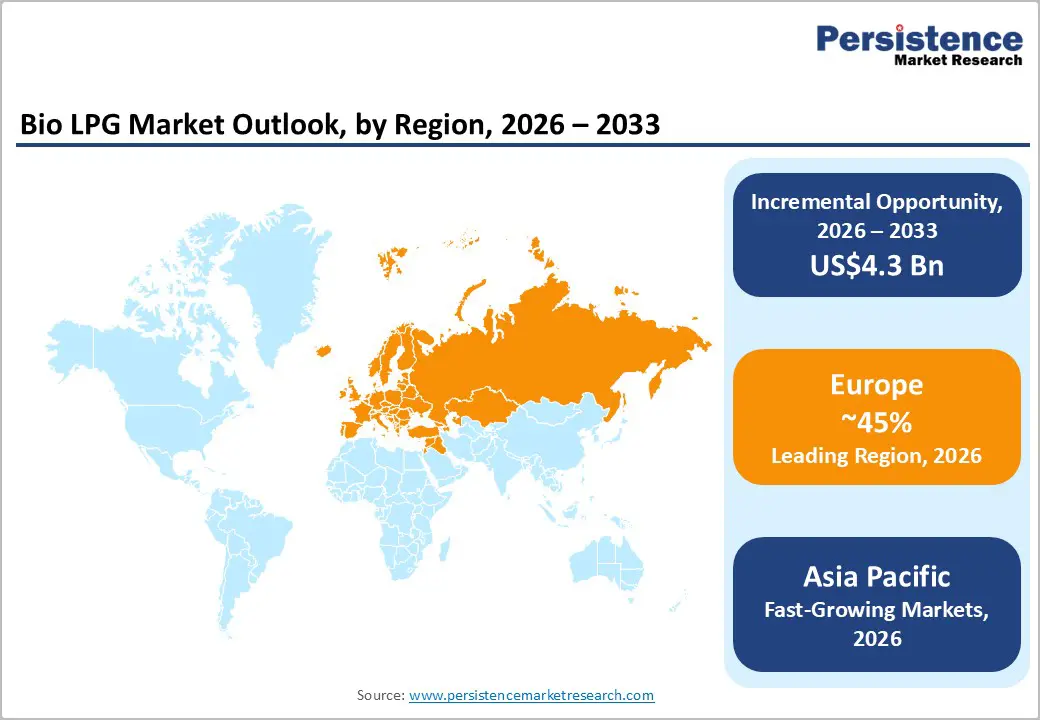

- Leading Region: Europe dominates the Bio LPG market with over 45% share in 2025, driven by RED III mandates, EU Fit for 55 targets, and production facilities across France, Sweden, Italy, Spain, and the Netherlands.

- Fastest Growing Region: Asia-Pacific is the fastest-growing Bio LPG region, with Strait of Hormuz supply disruptions (March 2026, IEA) driving emergency policy shifts in India, China, Japan, and ASEAN toward domestically produced renewable LPG.

- Dominant Segment: Bio-oil is the leading feedstock segment, with 38% market share, underpinned by established HEFA hydroprocessing at Neste's Rotterdam refinery and TotalEnergies' bio-refineries, where Bio LPG is co-produced with renewable diesel.

- Fastest Growing Segment: Aviation-grade Bio LPG is the fastest-growing application segment, catalyzed by ReFuelEU Aviation mandating SAF blending from 2% in 2025 to 70% by 2050, with Neste pioneering aviation-grade Bio LPG commercialization.

- Key Market Opportunity: Asia-Pacific's off-grid and rural residential LPG dependence, with India spending US$ 24 Bn annually on LPG subsidies (New Lines Institute, 2026), represents the largest addressable growth opportunity for Bio LPG market expansion.

| Key Insights | Details |

|---|---|

| Bio LPG Market Size (2026E) | US$ 2.5 Bn |

| Market Value Forecast (2033F) | US$ 6.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 15.4% |

| Historical Market Growth (2020 - 2025) | 12.7% |

Market Dynamics

Market Growth Drivers

Stringent Global Decarbonization Policies and Renewable Energy Directives

The most powerful catalyst for the Bio LPG market is the binding regulatory framework established by the European Union's Renewable Energy Directive III (RED III), which mandates a 42% renewable energy share by 2030. Complementing this, the EU's Fit for 55 package targets a 55% net reduction in greenhouse gas emissions by 2030 compared to 1990 levels. According to the European Biogas Association (EBA), Bio LPG production capacity in Europe is expected to triple by 2030, driven by biorefinery conversions and circular economy investments.

Simultaneously, ReFuelEU Aviation and ReFuelEU Maritime directives are mandating rapid scale-up of renewable fuels, including Bio LPG in hard-to-electrify transport sectors. The REPowerEU Plan further commits to a non-binding biomethane target of 35 Bn cubic meters by 2030, creating additional upstream feedstock supply that directly supports Bio LPG co-production.

Escalating Fossil LPG Supply Disruptions Reinforcing Renewable Alternatives

The geopolitical landscape of early 2026 has delivered a structural shock to conventional LPG markets. According to the IEA's Oil Market Report (March 2026), Gulf producers exported 1.5 mb/d of LPG in 2025, with over 3 mb/d of regional refining capacity shut following the escalation of the U.S.-Iran conflict and closure of the Strait of Hormuz. Brent crude prices surged over 25% within the first eight days of the conflict, with natural gas markets rising over 40% (New Lines Institute, 2026). These disruptions have compelled governments and energy companies to urgently accelerate the deployment of domestically produced renewable fuels, with Bio LPG emerging as the most practical drop-in substitute given its compatibility with existing LPG infrastructure, distribution networks, and appliances across residential, commercial, and industrial segments worldwide.

Market Restraints

High Production Costs and Feedstock Supply Constraints

Despite favorable policy tailwinds, Bio LPG production costs remain significantly higher than conventional fossil LPG, representing a formidable barrier to mass-market adoption. According to CME Group's Argus Media analysis (2025), conventional and waste-oil feedstock availability in 2030 could reach approximately 43 million tons, but this will be surpassed by combined renewable diesel, sustainable aviation fuel, and biodiesel demand competing for the same feedstocks, leading to structural tightness and price escalation that erodes Bio LPG margins. Renewable diesel and SAF capacity in Europe reached 4.5 million tons and 2.4 million tons, respectively, in 2025, intensifying competition for limited waste-based and bio-oil feedstocks that are also critical for Bio LPG synthesis.

Limited Production Scale and Geographic Concentration

Bio LPG production remains geographically concentrated primarily in France, Italy, Spain, Sweden, and the Netherlands, with limited commercial-scale facilities outside Europe. This concentration constrains global supply availability and limits the market's ability to serve growing demand in Asia-Pacific and North America at competitive cost structures. The EBA Statistical Report 2025 warns that regulatory fragmentation, market harmonization gaps, and investment uncertainty are slowing deployment at a decisive moment. Germany accounts for 53% of EU biogas production, creating upstream supply concentration risks that can cascade into Bio LPG feedstock availability constraints.

Market Opportunities

Aviation-Grade Bio LPG and Sustainable Aviation Fuel Integration

The aviation sector presents a transformational growth opportunity for Bio LPG producers. The EU's ReFuelEU Aviation directive mandates sustainable aviation fuel blending from 2% in 2025 to over 70% by 2050. SAF capacity in Europe is already expected to reach 2.4 million tons in 2025, according to Argus Media estimates cited by CME Group. Aviation-grade Bio LPG, first commercially developed by Neste, offers airlines a certified, low-lifecycle-emission propellant that integrates directly into existing aircraft fuel systems without engine modifications.

The U.S.-Iran conflict's widespread flight cancellations across the Middle East and disruptions to conventional jet and LPG supply chains are accelerating airline operators' and fuel procurement desks' interest in domestically sourced, geopolitically insulated renewable alternatives, presenting a long-term structural demand catalyst for aviation-oriented Bio LPG producers.

Asia-Pacific Off-Grid and Rural Energy Transition

Asia-Pacific's massive LPG-dependent residential and agricultural base represents the single largest untapped opportunity for Bio LPG market expansion. India alone has budgeted approximately 2 trillion rupees (US$ 24 Bn) in LPG cooking gas subsidies for fiscal year 2025-26 (New Lines Institute, 2026), while the ongoing Strait of Hormuz disruption has forced India to invoke emergency powers to redirect LPG supplies from industrial users to households. This acute fossil LPG supply vulnerability, compounded by India's import of more than 80% of its crude oil, creates powerful policy incentives to accelerate domestic Bio LPG production. According to the IEA's Renewables 2025 report, China's combined biogas and biomethane production is forecast to rise 23% between 2025 and 2030, establishing a credible feedstock base to support Asia-Pacific Bio LPG manufacturing scale-up.

Category-wise Insights

Feedstock Analysis

The Bio-oil segment dominates the Bio LPG feedstock landscape, accounting for approximately 38% of the market share in 2025. Bio-oil's leadership is underpinned by its established hydroprocessing pathway, the same technology used by leading producers such as Neste at its Rotterdam refinery and TotalEnergies at its French and Belgian bio-refineries, which co-produces Bio LPG as a direct by-product of renewable diesel and hydroprocessed esters and fatty acids (HEFA) production.

According to Argus Media estimates cited by CME Group (2025), renewable diesel capacity in Europe reached approximately 4.5 million tons in 2025, representing a substantial and growing source of Bio LPG co-product. The Biogas segment ranks as the second-largest feedstock category, reinforced by EU biomethane production growing 14% year-on-year in 2024 per IEA data, with Germany, France, Italy, Denmark, and the Netherlands collectively accounting for the majority of EU biomethane output.

Application Analysis

The Residential & Commercial Cooking segment represents the leading application for Bio LPG, commanding approximately 35% of total market demand. This dominance is driven by Bio LPG's chemically identical properties to fossil LPG, enabling seamless drop-in deployment across the 60 million European households that rely on LPG for domestic heating and cooking per Eurostat data, particularly in rural and off-grid areas where natural gas infrastructure is absent. Companies such as Calor Gas (UK) and SHV Energy's Futuria brand have commercially marketed Bio LPG as a 100% renewable drop-in replacement for residential customers.

The Transportation segment follows as the second-largest application, gaining significant traction as Bio LPG autogas offers up to 80% lifecycle greenhouse gas emission reductions versus conventional LPG, aligning with increasingly stringent vehicle emission standards across the EU and Asia-Pacific.

End Use Analysis

The Residential end-use segment leads the Bio LPG market with approximately 40% market share, reflecting the segment's large addressable base and ease of adoption. Over 60 million households in Europe alone use LPG for heating and cooking per Eurostat, representing a deeply penetrable market for Bio LPG substitution, given the zero-infrastructure-modification requirement. Rural off-grid residential consumers are particularly compelling adopters, as Bio LPG provides a low-carbon heating solution in markets where heat pump electrification remains economically or technically unfeasible.

The European LPG Association (AEGPL) has recognized Bio LPG as a viable short-to-medium-term decarbonization solution for residential sectors where grid-based electrification cannot be rapidly deployed. The Commercial segment follows, with hospitality, food services, and office heating sectors progressively adopting Bio LPG under corporate ESG and sustainability reporting mandates.

Regional Insights

North America Bio LPG Trends

North America represents a pivotal and rapidly advancing market for Bio LPG, supported by the United States’ status as the world’s largest oil and gas producer. This strong domestic production base has partially shielded the region’s LPG supply chain from the disruptions caused by the 2026 Strait of Hormuz crisis. Despite this insulation, the more than 25% surge in global oil prices following the onset of the U.S.-Iran conflict has reinforced the economic rationale for expanding domestically produced Bio LPG across the U.S. and Canada.

On the policy front, the U.S. Renewable Fuel Standard (RFS) and state-level low-carbon fuel standards continue to create incentives for Bio LPG production and blending. Additionally, U.S. biomethane output, estimated at 136 PJ, remains one of the fastest-growing renewable gas streams, strengthening future feedstock availability for Bio LPG pathways.

Europe Bio LPG Trends

Europe remains the leading global market for Bio LPG, holding over 45% of the total share due to its advanced and comprehensive biofuel regulatory framework. The EU Renewable Energy Directive III targets a 42% renewable energy share by 2030, with major economies, including Germany, France, Italy, the Netherlands, and Sweden, driving both production and consumption. EU biomethane output increased by 14% in 2024, supported by France’s new biomethane blending mandate effective in 2026.

The geopolitical instability arising from the U.S.-Iran conflict has further intensified Europe’s commitment to expand domestic Bio LPG capacity. Initiatives such as the REPowerEU Plan, the UK’s decarbonization efforts for off-grid heating, Spain’s Bio LPG investments through Repsol, and Preem AB’s expansion in Sweden collectively reinforce a robust, integrated Bio LPG ecosystem across the region.

Asia Pacific Bio LPG Trends

Asia-Pacific is the fastest-growing regional market for Bio LPG, driven by severe fossil fuel supply disruptions arising from the U.S.-Iran conflict. With nearly 80% of the region’s oil imports traditionally routed through the Strait of Hormuz, its closure in late February 2026 triggered significant energy constraints across multiple economies. India implemented emergency measures to divert LPG toward residential use, while Bangladesh and Myanmar enforced fuel rationing, and the Philippines introduced a four-day workweek to reduce demand. These vulnerabilities are accelerating policy-led support for domestic Bio LPG production.

China’s biogas and biomethane output is projected to expand by 23% between 2025 and 2030, and India’s substantial LPG subsidy burden is reinforcing the case for renewable alternatives. Concurrently, Japan, South Korea, and ASEAN countries are investing in bio-refineries and agricultural waste valorization to strengthen regional feedstock availability.

Competitive Landscape

The global Bio LPG market exhibits a moderately consolidated competitive structure, with SHV Energy and Neste together commanding over 50% of the global production share. Market leaders are pursuing capacity expansion through strategic joint ventures, feedstock diversification into cellulosic and waste-based pathways, and geographic expansion into Asia-Pacific and North America. Key differentiators include proprietary hydroprocessing technology, established long-term waste feedstock supply agreements, and direct integration into LPG distribution infrastructure. Emerging business model trends include dedicated Bio LPG brand launches, aviation-grade Bio LPG product lines by Neste, and joint ventures specifically designed for Bio LPG scale-up, such as Dimeta.

Key Market Developments

- February 2025: TotalEnergies announces the commissioning of BioNorrois, its 8th biomethane production unit-1 in France, located in Fontaine-le-Dun (Normandy). It will inject 153 GWh of biomethane per year into the natural gas transport network operated by NaTran, equivalent to the average annual gas consumption of more than 30,000 inhabitants.

- September 2024: SHV Energy’s Polish business, Gaspol, welcomed its first delivery of bioLPG at the port of Gdansk, introducing this important sustainable fuel to the country for the first time. This came just a year after Gaspol had introduced hybrid systems combining liquefied gas with heat pumps, demonstrating the company's continued push at the frontier of renewable energy in Poland.

- February 2026: Eni and Q8 Italy announce a major strategic investment in the ongoing project for the construction of a new biorefinery in Priolo, Sicily. The transformation plan for the Versalis site in Priolo received formal approval from Eni and the Kuwait Petroleum Corporation Board of Directors, which follows the official binding offer submitted by Q8.

Top Companies in the Bio LPG Market

- SHV Energy (Netherlands) is the global market leader in Bio LPG distribution, operating under brands including Calor, Primagaz, and its dedicated renewable brand Futuria Fuels. The company commands the largest distribution network for off-grid LPG globally and has pioneered commercial Bio LPG supply in Europe. Its November 2023 partnerships with Japanese energy and industrial conglomerates position SHV Energy as the leader in next-generation feedstock diversification toward livestock-derived renewable propane, reinforcing its dominant competitive position across production, distribution, and retail dimensions of the Bio LPG value chain.

- Neste (Finland) is the world's largest producer of renewable diesel and a foundational pioneer of commercial Bio LPG synthesis. It's Rotterdam and Finnish refineries that co-produce Bio LPG through the HEFA pathway at an industrial scale. The 2024 expansion, adding 30% new production capacity and the launch of aviation-grade Bio LPG, demonstrates Neste's strong portfolio diversification strategy. The company's technological leadership in renewable hydroprocessing, extensive feedstock procurement networks across Europe, Asia, and North America, and deep integration with aviation sector sustainability commitments make it the most technologically differentiated player in the Bio LPG market.

- TotalEnergies (France) leverages its integrated energy conglomerate structure and bio-refinery operations across France and Belgium to produce and commercialize Bio LPG at scale. The company's 2024 introduction of an industrial heating-specific Bio LPG blend delivering 80% carbon reduction demonstrates its focus on high-value industrial applications. TotalEnergies' global distribution infrastructure, significant R&D investment in advanced biofuel pathways, and strategic alignment with EU decarbonization targets establish it as a major commercial force across European and emerging Bio LPG markets.

Companies Covered in Bio LPG Market

- SHV Energy

- Neste

- TotalEnergies

- Eni S.p.A

- Repsol

- Preem AB

- Renewable Energy Group, Inc.

- Global Bioenergies

- Calor Gas Ltd.

- Irving Oil

- Alkcon Corporation

Frequently Asked Questions

The global Bio LPG market is valued at US$ 2.5 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, expanding at a CAGR of 15.4% over the forecast period. Historically, the market grew at a CAGR of 12.7% between 2020 and 2025, with the 2026-2033 acceleration driven by binding EU decarbonization mandates, global fossil LPG supply disruptions, and expanding renewable energy infrastructure investments.

The primary demand drivers are binding regulatory mandates, including the EU's RED III (42% renewable energy by 2030), Fit for 55 (55% GHG reduction by 2030), and ReFuelEU Aviation directives. The driver also includes geopolitical fossil LPG supply disruptions, specifically the March 2026 Strait of Hormuz closure that suspended 1.5 mb/d of LPG exports per IEA, structurally reinforcing renewable alternative deployment urgency.

The Bio-oil segment leads the Bio LPG feedstock category with approximately 38% market share, driven by its established HEFA hydro processing production pathway where Bio LPG is co-produced alongside renewable diesel at industrial-scale bio-refineries operated by Neste and TotalEnergies. Biogas ranks second, supported by 14% EU biomethane production growth in 2024 per IEA.

Europe leads the global Bio LPG market with over 45% of global market share, anchored by the world's most comprehensive biofuel regulatory framework (RED III, Fit for 55, REPowerEU), established bio-refinery infrastructure in France, Sweden, Italy, Spain, and the Netherlands, and market leaders SHV Energy and Neste collectively commanding over 50% of global Bio LPG production share.

The single most significant market opportunity is Asia-Pacific's off-grid and rural residential energy transition. With 80% of Asia's oil imports historically transiting the Strait of Hormuz (TIME, March 2026), and India allocating US$ 24 Bn annually to LPG subsidies, the structural imperative to develop domestic Bio LPG supply chains in India, China, Japan, and ASEAN markets represents the largest addressable growth frontier for market participants over the 2026-2033 forecast period.

The leading companies in the global Bio LPG market include SHV Energy, Neste, TotalEnergies, Eni S.p.A, Repsol, Preem AB, Renewable Energy Group, Inc., Global Bioenergies, Calor Gas Ltd., Irving Oil, and Alkcon Corporation. SHV Energy and Neste together hold over 50% of the global production share.