- Advanced Materials

- Bio-based Polyurethane Market

Bio-based Polyurethane Market Size, Share, and Growth Forecast, 2026 - 2033

Bio-based Polyurethane Market by Product Type (Flexible Foams, Rigid Foam, Coatings, Adhesives & Sealants, and Others), End-user (Building & Construction, Automotive, Consumer Goods, Electrical & Electronics, Packaging, and Others), and Regional Analysis for 2026 - 2033

Bio-based Polyurethane Market Size and Trends Analysis

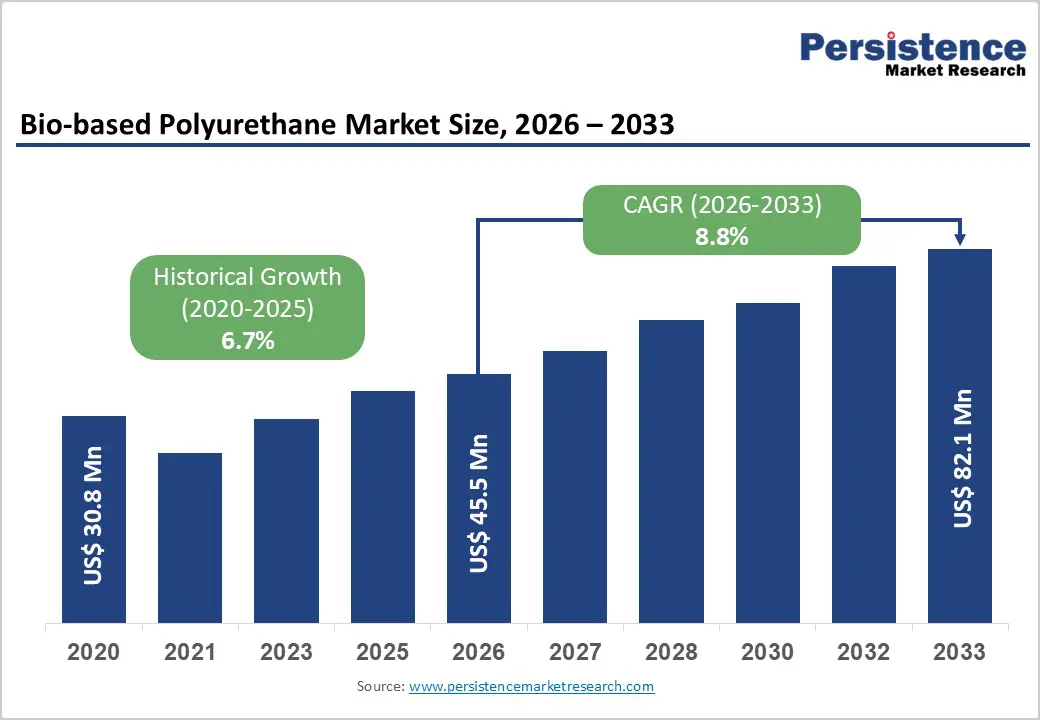

The global bio-based polyurethane market size was valued at around US$ 45.5 million in 2026 and is projected to reach approximately US$ 82.1 million by 2033, growing at a CAGR of 8.8% between 2026 and 2033. The market has expanded from about US$ 30.8 million in 2020, reflecting a historical CAGR of roughly 6.7% driven by sustainability-led substitution of fossil-based polyurethanes in construction, automotive, and consumer applications.

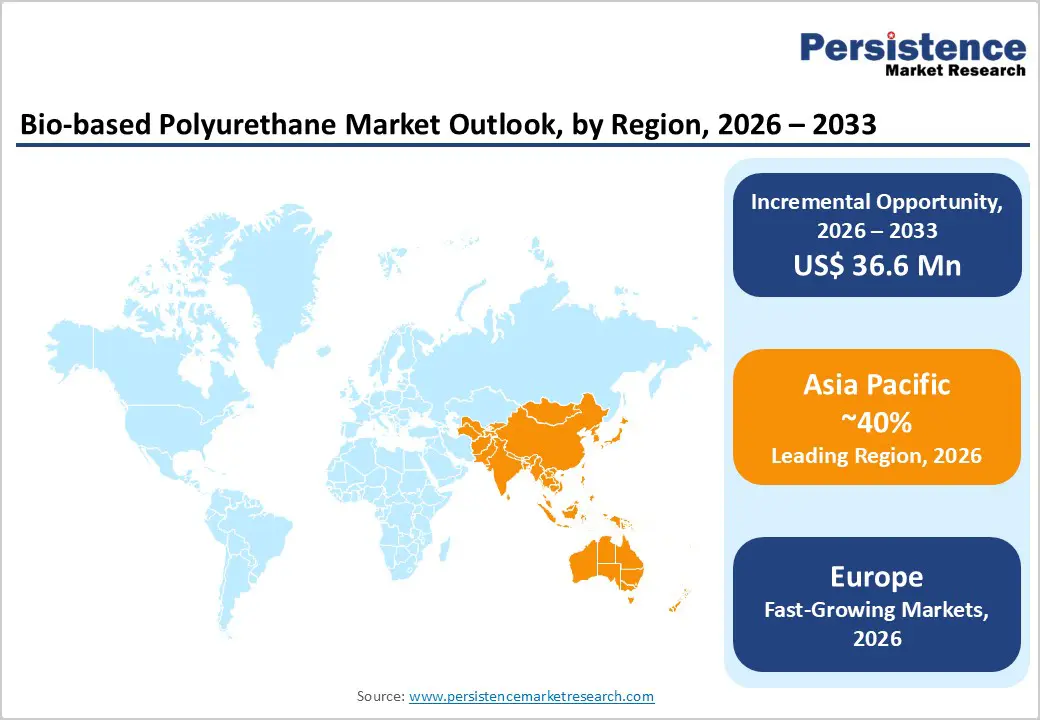

Rising green-building investments, decarbonization targets in transport, and corporate ESG commitments are accelerating the adoption of bio-based foams, coatings, adhesives, and sealants. Asia Pacific already accounts for over 40% of global revenues, underpinned by construction and manufacturing growth, while Europe and North America gain traction through regulatory incentives and circular-economy policies.

Key Industry-Highlights:

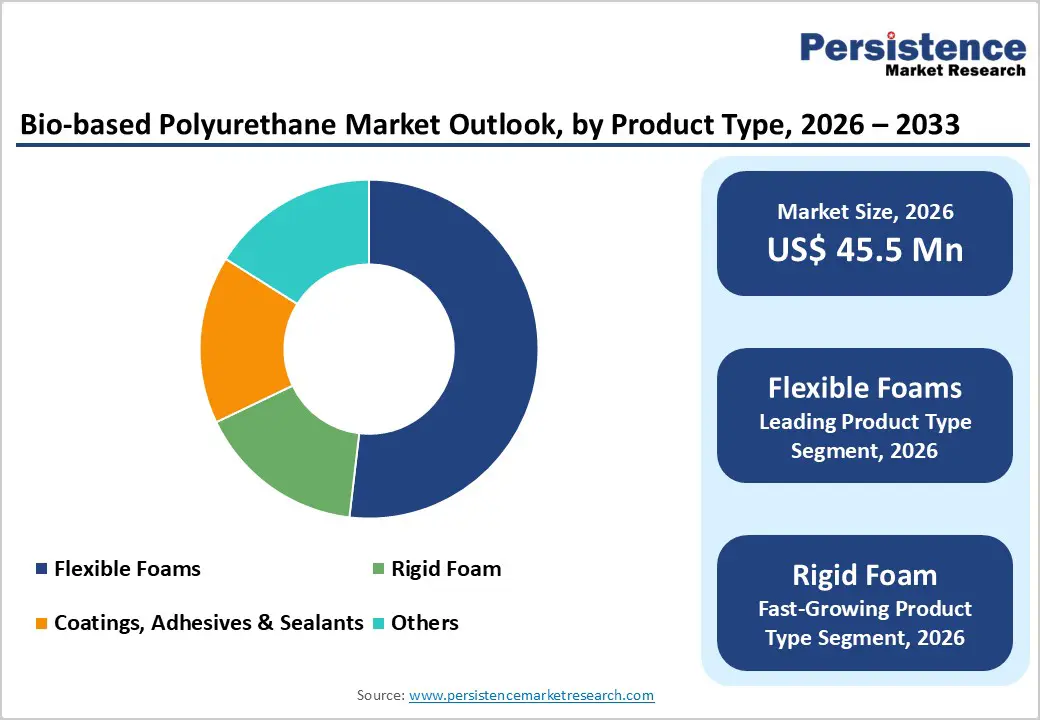

- Leading Product Type: Flexible foams represent over 51% of 2026 revenues, underpinned by cushioning, furniture and automotive seating demand, while rigid foams are projected to grow at approximately 9.5% CAGR on the back of energy-efficient building insulation requirements.

- Rising Crude Oil Prices: Escalating geopolitical tensions in the Middle East have increased global crude oil prices, raising the cost of petrochemical feedstocks used in polyurethane production.

- Higher Polyol and Isocyanate Costs: Key polyurethane intermediates such as polyols, MDI, and TDI are experiencing price pressure due to rising propylene and benzene feedstock costs linked to oil market volatility.

- Supply Chain Disruption Risks: Potential disruptions in the Strait of Hormuz, a critical global oil and chemical shipping route, could delay feedstock supply and increase transportation costs.

- End-user Analysis: Building & construction accounts for above 35% of global revenues, with growth supported by green-building codes and infrastructure investment; the automotive end-use segment is expected to be the fastest-growing, at around 9.6% CAGR, driven by lightweighting and interior sustainability trends.

- Regional Analysis: Asia Pacific holds more than 40% of global market share, benefitting from rapid urbanization, manufacturing scale and access to bio-based feedstocks, while Europe and North America leverage strong regulatory frameworks and innovation ecosystems to expand adoption.

- Technological advances in bio-polyols, bio-fillers and emerging 100% biogenic isocyanates are improving performance parity with fossil-based PU and enabling higher bio-content formulations across flexible and rigid foams, coatings, adhesives, and elastomers.

- Strategic partnerships and R&D programs such as Covestro-Mitsui’s collaboration on bio-based PU, BASF’s biomass-balance MDI deployments, and EU projects like BIOMOTIVE are accelerating the commercialization of bio-based PU solutions in automotive, construction, and specialty applications.

- Despite strong growth prospects, the market faces headwinds from cost premiums, feedstock volatility, and standardization gaps, underscoring the importance for suppliers to combine innovation, supply-chain resilience, and policy engagement to capture long-term value.

Market Dynamics

Drivers - Decarbonization of construction and infrastructure value chains

Global construction is a leading consumer of polyurethane foams and coatings, and policy pressure to cut embodied carbon is pushing asset owners toward bio-based chemistries. Asia Pacific is expected to account for about 50% of global construction output by 2030, with China alone representing roughly 20% of worldwide construction investment, creating sizeable pull for low-carbon insulation materials. Green-building programs and energy-efficiency codes in Europe and North America increasingly reference lifecycle assessment and recycled or bio-based content, making bio-based polyurethane an attractive route to improve building-envelope performance while reducing fossil dependence. This driver directly supports volume growth in rigid foams and coatings for insulation panels, roofing systems and sealants in both new build and retrofits.

Regulatory frameworks and incentives for bio-based materials

Regulators in the European Union and the United States have introduced policy frameworks that favor biobased content, recyclability and reduced carbon footprints for plastics and polymeric materials. The EU’s policy framework on biobased, biodegradable and compostable plastics under the Green Deal’s Circular Economy Action Plan encourages clear biobased-content labeling and radiocarbon-based verification, which benefits polyurethane producers that can certify renewable carbon content. In North America, federal and state programs, including USDA Bio Preferred procurement initiatives and state-level packaging and plastics legislation, create demand signals and, in some cases, economic incentives for bio-based feedstocks in sectors such as packaging, construction, and automotive. Together, these measures lower adoption risk for buyers, support premium pricing relative to conventional PU, and encourage scale-up investments in bio-polyol and bio-isocyanate capacity.

Restraint - Higher cost structure versus conventional polyurethane

Despite improving economics, most bio-based polyurethanes still carry a cost premium over fossil-based analogues, reflecting smaller scale, more complex processing routes and higher prices for certified sustainable feedstocks. Conventional PU benefits from a mature, globally optimized petrochemical supply chain, making price competition difficult in cost-sensitive segments such as commodity insulation or low-spec cushioning. Where buyers are not under regulatory or brand pressure to decarbonize, this premium slows conversion from conventional to bio-based systems and can limit adoption to niche or high-value applications, particularly in emerging markets.

Feedstock availability, standardization, and supply chain complexity

Bio-based PU relies on agricultural oils, biomass residues, and other renewable inputs whose availability and price can fluctuate with crop yields, land-use competition, and policy changes around bioenergy and food security. In addition, there is still no globally harmonized minimum biobased-content standard for polyurethane products, though the EU has begun clarifying measurement methods and labeling expectations. This lack of standardization complicates certification and cross-border trade, while smaller producers may struggle to secure consistent, traceable feedstock volumes that meet OEM sustainability criteria, creating supply-risk perceptions for large buyers.

Opportunities - Next-generation bio-isocyanates and 100% bio-based PU systems

Emerging technologies that enable plant-based or biogenic-carbon isocyanates are opening the possibility of fully bio-based polyurethane systems, not just bio-polyol substitution. For example, pilot-scale plants have demonstrated 100% biogenic isocyanates manufactured without phosgene, validated via ASTM D6866 analysis and targeted initially at thermoplastic polyurethanes and high-performance applications. As these technologies scale and gain regulatory acceptance, they can unlock premium segments where customers are willing to pay for fully renewable, phosgene-free chemistries, expanding market value beyond the current partially bio-based formulations.

Lightweighting and circularity in automotive and transportation

The automotive sector is intensifying efforts to reduce vehicle weight and lifecycle emissions, creating headroom for bio-based polyurethane foams, elastomers and composites in seating, interiors, NVH components and load-bearing structures. EU and Chinese regulations on fleet-average CO- emissions, together with OEM net-zero commitments, are driving evaluation of renewable and recyclable materials in electric and internal-combustion vehicles. As bio-based PU solutions demonstrate mechanical performance parity with conventional materials and integrate with circular models (e.g., recyclability or bio-based feedstock take-back), the addressable automotive market could support high-single-digit to low-double-digit annual growth for relevant grades over the forecast period.

Category-wise Analysis

Product Type Insights

Flexible foams account for above 51% of bio-based polyurethane revenues in 2026, reflecting their entrenched role in cushioning, furniture, automotive seating and packaging applications. Adoption has been supported by advances in bio-polyols derived from lactide, vegetable oils and biomass, which deliver comparable resilience, compression set and durability to petrochemical foams. Academic and industrial studies have validated flexible bio-based PU foams for automotive seats and headrests, with optimized mechanical properties and thermal stability compatible with OEM specifications.

Rigid foams are expected to be the fastest-growing product type, with CAGRs around 9.5%, as energy-efficiency regulations and green-building certifications drive demand for low-thermal-conductivity insulation materials. Bio-based rigid PU foams formulated from lignin, tannin, or vegetable-oil polyols have demonstrated improved fire resistance, compressive strength and lower smoke emissions relative to fossil-based references, making them attractive for sandwich panels, roofing, and cold-chain insulation. This performance profile, coupled with embodied-carbon advantages, positions bio-based rigid foams to outpace overall market growth as building codes tighten and infrastructure pipelines expand.

End-user Insights

Building and construction represents over 35% of global bio-based polyurethane revenues in 2026, underpinned by applications in insulation boards, spray foams, sealants, flooring and coatings for both residential and non-residential assets. Market studies indicate building & construction holds roughly one-third of global bio-based PU demand, with growth supported by green-building certifications, stricter thermal-performance standards and government infrastructure programs. Asia Pacific’s rapid urbanization and infrastructure investment, together with European tax incentives and subsidies for energy-efficient renovations, reinforce this segment’s leadership.

The automotive segment is anticipated to post the highest CAGR, at about 9.6%, reflecting rising use of bio-based PU in seating, interior panels, NVH solutions, coatings, and lightweight composites. EU research programs such as BIOMOTIVE have demonstrated industrial validation of bio-based PU foams and thermoplastic PU in car interiors, while OEM sustainability roadmaps prioritize renewable content and circular material flows. As electric-vehicle platforms seek further weight reduction and improved cabin comfort, bio-based PU materials with improved mechanical properties and lower VOC emissions are well-positioned to capture incremental share from conventional PU and other polymers.

Regional Insights and Trends

Manufacturing scale reinforces Asia Pacific polyurethane leadership

Asia Pacific is the dominant regional market, accounting for over 40% of global bio-based polyurethane revenues in 2026, and is projected to remain the largest and one of the fastest-growing regions through 2033. China, Japan, India, and Southeast Asian economies anchor this position, leveraging large construction pipelines, expanding automotive production, robust consumer-goods manufacturing, and competitive cost structures. Market assessments show Asia Pacific holding close to 38-40% of global revenues in the mid-2020s and growing at CAGRs slightly above the global average, supported by industrialization and rising environmental awareness.

China’s construction market alone accounts for about 20% of global construction investment, and the broader Asia Pacific construction sector is expected to represent roughly half of global output by 2025, fuelling demand for insulation foams, sealants and coatings. Regional governments are progressively tightening building-energy standards and promoting green-building labels, while major automotive OEMs and electronics manufacturers expand capacity in China, India and ASEAN, stimulating use of bio-based PU in interiors, cushioning, and electronics encapsulation. Asia Pacific also benefits from abundant access to vegetable-oil feedstocks and biomass residues, as well as relatively lower labor and land costs, encouraging upstream investments in bio-polyol production and downstream application development. Competition is intensifying as global majors expand local manufacturing and joint ventures, while regional players in China, India and Southeast Asia target cost-competitive bio-based grades for domestic markets.

Regulation-driven innovation underpins steady adoption in North America

North America accounts for a meaningful share of the global bio-based polyurethane market and is projected to grow at mid-single- to high-single-digit CAGRs through 2033, broadly in line with global averages. The United States drives regional demand, supported by a large construction sector, advanced automotive and transportation industries, and active innovation clusters in sustainable materials. Market analyses indicate North America’s bio-based PU market is benefiting from increasing adoption in green buildings and infrastructure rehab projects, as well as expanding use in specialty coatings and adhesives.

Growth is reinforced by a supportive regulatory and incentive environment. Federal procurement preferences under the USDA BioPreferred Program, state-level plastics and packaging regulations, and climate policies encouraging low-carbon building materials all create demand signals for bio-based chemistries. U.S.-based producers and multinationals are investing in biomass-balance isocyanates and biobased binders, exemplified by initiatives such as BASF’s biomass-balance MDI used in polyurethane binders for playground and recreational surfacing, which reduce fossil-carbon footprints without major process changes for converters. The regional competitive landscape is moderately consolidated, with global majors such as BASF, Covestro, Huntsman, and Lubrizol operating R&D centers and production facilities, often partnering with downstream customers to co-develop applications in footwear, construction, and automotive. These collaborations, coupled with venture-backed innovation in bio-isocyanates and recycling technologies, sustain a robust pipeline of commercialization opportunities across flexible and rigid foam, coatings and elastomer applications.

Competitive Landscape

The bio-based polyurethane market exhibits high concentration at the global level, with a handful of multinational chemical companies capturing a significant share of revenues, complemented by regional specialists and system houses. Market analyses consistently identify The Lubrizol Corporation, Covestro, BASF, Mitsui Chemicals, and Huntsman as leading players based on market shares. These companies leverage integrated value chains, strong R&D capabilities, and established customer relationships in construction, automotive, and consumer goods to maintain pricing power and influence on technology standards, while smaller firms focus on niche applications, localized formulation and agile innovation.

Key Developments:

- In 2025, Algenesis Labs commissioned a pilot plant to produce Bio-Iso™, described as the first 100% biogenic carbon isocyanate made from plant-based dicarboxylic acids and manufactured without phosgene. The innovation enables fully bio-based thermoplastic polyurethane when combined with bio-based polyols, supporting downstream manufacturers seeking phosgene-free PU systems aligned with stringent ESG goals.

- In 2024, Covestro and Mitsui Chemicals announced a strategic collaboration to expand the use of bio-based raw materials in polyurethane production. The partnership focuses on reducing fossil-fuel dependence and lowering carbon emissions across key applications including automotive components and industrial materials.

- In October 2024, Mitsubishi Chemical Group announced the adoption of a plant-derived polyurethane raw material called BioPTMG for bio-synthetic applications. The new material aims to reduce reliance on fossil resources and improve sustainability across multiple industries, supporting the development of environmentally friendly products aligned with growing global demand for sustainable materials.

- In 2024, BASF and STOCKMEIER Urethanes USA began commercial production of polyurethane binders for playground and recreational surfacing using BASF’s biomass-balance Lupranate MDI produced at its Geismar facility, supporting lower-carbon polyurethane systems.

- In September 2023, Covestro and Selena Group introduced a new range of bio-attributed polyurethane foams for thermal insulation. Produced using renewable raw materials, these foams help reduce the carbon footprint associated with conventional PU foams and support sustainable construction and building applications.

Companies Covered in Bio-based Polyurethane Market

- BASF SE

- Covestro AG

- Huntsman International LLC

- The Lubrizol Corporation

- Dow Inc.

- Wanhua Chemical Group

- Mitsui Chemicals Inc.

- Recticel NV

- RAMPF Holding GmbH

- Evonik Industries AG

- Cargill, Incorporated

- Mitsubishi Chemical Group

- NIPSEA Group

- UBE Corporation

- Other Market Players

Frequently Asked Questions

The Bio-based Polyurethane market is estimated to be valued at US$ 45.5 Mn in 2026.

The primary demand driver for the bio-based polyurethane market is the increasing global focus on sustainability and the shift toward low-carbon, renewable materials. Industries such as automotive, construction, furniture, footwear, and packaging are actively replacing petroleum-based polyurethane with bio-based alternatives derived from renewable feedstocks like soybean oil, castor oil, and other plant-based polyols.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Bio-based Polyurethane market.

Flexible Foams dominate the product landscape, commanding over 51% of total market revenue in 2026, driven by their extensive use in furniture, bedding, automotive seating, and cushioning applications, where comfort, durability, and lightweight performance are essential.

The key players in the bio-based polyurethane market include BASF SE, Covestro AG, Huntsman Corporation, The Lubrizol Corporation, Dow Inc., Wanhua Chemical Group, and Mitsui Chemicals Inc., which are actively investing in bio-based polyols, sustainable feedstocks, and low-carbon polyurethane technologies to expand their presence in the market.