- Automotive

- Automotive Smart Antenna Market

Automotive Smart Antenna Market Size, Share, and Growth Forecast 2026 – 2033

Automotive Smart Antenna Market by Frequency Type (High, Very High, Ultra-High), Vehicle Type (Passenger Cars [SUV, Hatchbacks], Commercial Vehicles [Light Commercial Vehicle, Heavy Commercial Vehicles]), Antenna Type (Shark Fin, Fixed Mast), and Regional Analysis for 2026–2033

Automotive Smart Antenna Market Size and Trend Analysis

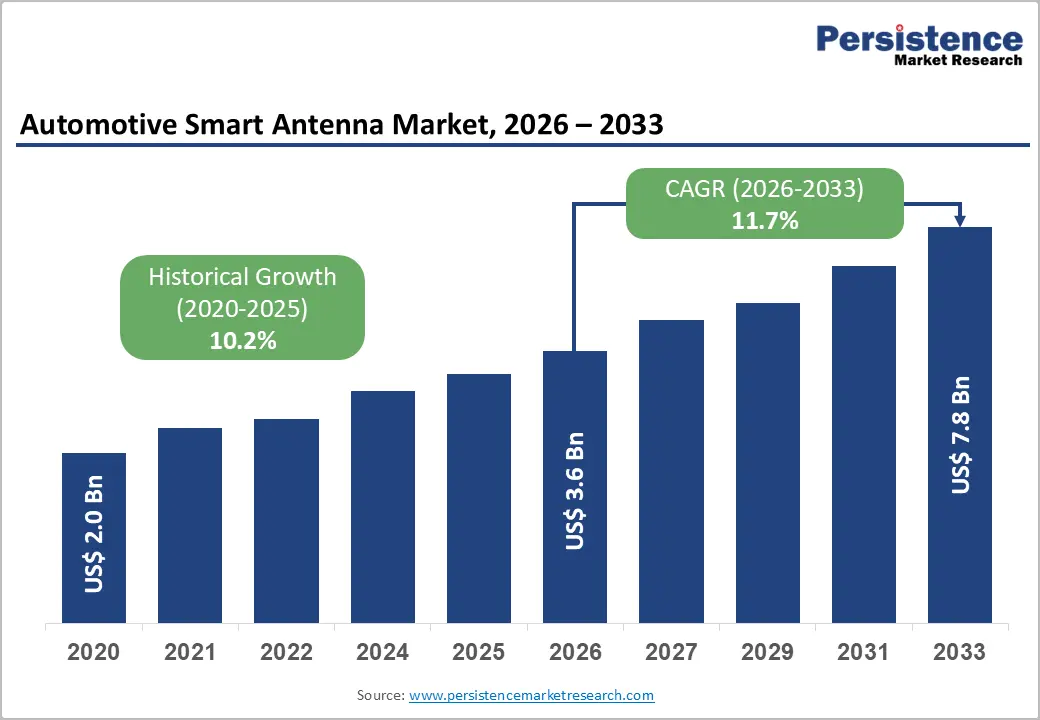

The global Automotive Smart Antenna market size is valued at US$ 3.6 billion in 2026 and is projected to reach US$ 7.8 billion by 2033, growing at a CAGR of 11.7% between 2026 and 2033.

The market's robust expansion is primarily driven by the accelerating integration of advanced connectivity technologies in modern vehicles, including 5G, V2X (Vehicle-to-Everything), and GNSS systems. Stringent government mandates worldwide, such as the European Union's eCall regulation requiring emergency call systems in all new vehicles, are compelling automakers to embed multi-band antenna systems.

Key Industry Highlights:

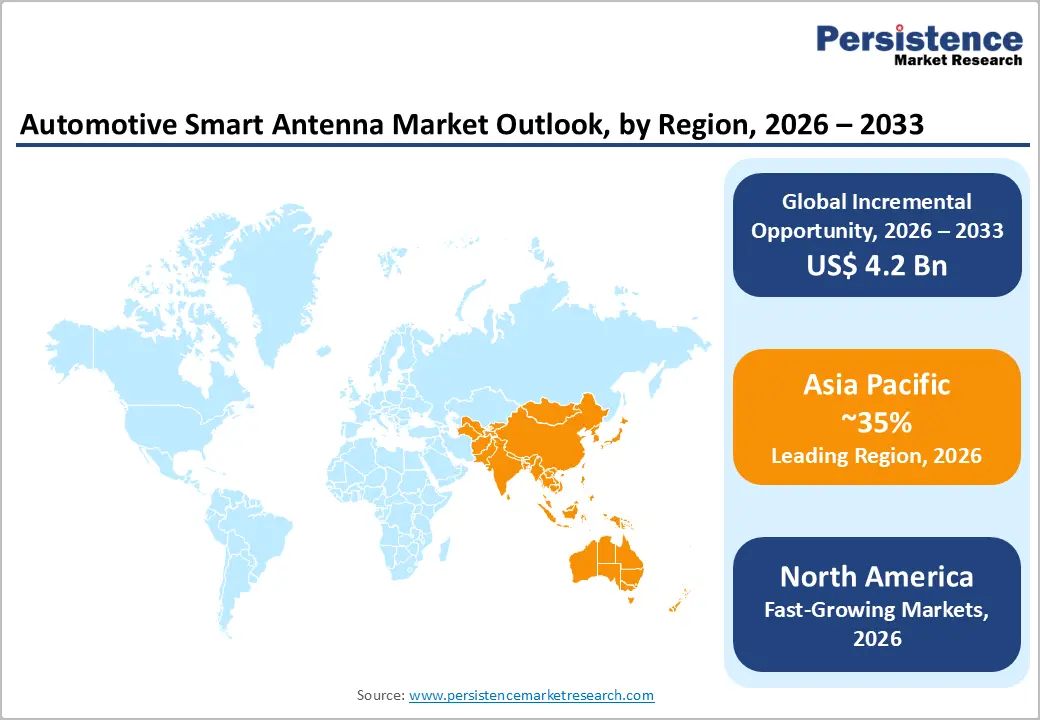

- Leading Region - Asia Pacific dominates the global automotive smart antenna market, accounting for approximately 34% of global revenue, underpinned by China's C-V2X mandate, mass-scale vehicle production surpassing 56% of global output (OICA, 2023), and rapid 5G infrastructure expansion.

- Fastest Growing Market- North America represents a mature yet dynamically evolving market for automotive smart antennas, accounting for approximately 28% of global market revenue. The region's growth is driven by strong OEM adoption of connected vehicle technologies, supported by robust 5G infrastructure rollouts by carriers such as Verizon, AT&T, and T-Mobile.

- Dominant Antenna Type Segment - The shark fin antenna type leads with approximately 72% market share, driven by OEM preference for aerodynamic, multi-band integration capabilities, and alignment with fuel efficiency directives from the EPA and EU Green Deal across global vehicle platforms.

- Fastest Growing Frequency Type- The UHF segment is the fastest growing, propelled by mass deployment of 5G NR (bands n77/n78), V2X communication protocols, and the surge in autonomous vehicle platforms requiring simultaneous multi-band antenna operation in the 300 MHz–3 GHz spectrum.

- Key Opportunity - With global EV sales reaching 14 million units in 2023 (IEA) and projected to surpass 300 million EVs by 2030, suppliers offering integrated 5G, V2X, GNSS, and mmWave antenna modules for autonomous EV platforms represent the highest-value opportunity in the market.

DRO Analysis

Drivers - Rapid Proliferation of Connected Vehicles and 5G Adoption

The global automotive industry is undergoing a paradigm shift toward connected mobility, making high-performance antenna systems indispensable. According to the International Telecommunication Union (ITU), global 5G subscriptions surpassed 1.6 billion in 2023 and are projected to exceed 5 billion by 2027. This connectivity revolution is directly impacting the automotive sector, as vehicles now require multi-band smart antennas capable of simultaneously supporting LTE, 5G NR, Wi-Fi 6, GNSS, and DSRC (Dedicated Short-Range Communications).

The European Automobile Manufacturers' Association (ACEA) reported that over 60% of new passenger vehicles sold in Europe in 2023 were equipped with some form of connected services, a figure expected to reach nearly 90% by 2030. Smart antennas consolidate multiple frequency bands into compact, aerodynamic modules, directly enabling this next-generation connectivity and creating sustained demand across all vehicle segments.

Regulatory Mandates for Vehicle Safety and Emergency Communication Systems

Global regulatory frameworks are compelling automotive original equipment manufacturers (OEMs) to integrate advanced communication antennas as standard equipment. The European Commission's eCall regulation (Regulation (EU) 2015/758) has mandated emergency call systems in all new passenger cars and light commercial vehicles since April 2018, creating an irreversible baseline demand for embedded antenna solutions.

Similarly, Russia enforces the ERA-GLONASS standard, and China's Ministry of Industry and Information Technology (MIIT) has mandated Beidou-based telematics in commercial vehicles. Additionally, the U.S. National Highway Traffic Safety Administration (NHTSA) proposed rules requiring V2X communication capabilities in light vehicles by 2026–2027. These mandates collectively generate a non-discretionary demand pipeline for smart antenna systems, significantly supporting market growth.

Restraints - High Development and Integration Costs for Multi-Band Smart Antennas

The design and integration of multi-band smart antenna systems involve considerable research, development, and manufacturing costs that can challenge adoption, particularly in the price-sensitive entry-level vehicle segment. Multi-band smart antennas must simultaneously accommodate frequencies ranging from 700 MHz to 6 GHz for 5G sub-6GHz bands, plus 1.5 GHz GNSS and 76–77 GHz radar, requiring sophisticated RF engineering and signal isolation techniques.

According to the SAE International, adding a fully integrated smart antenna module can increase a vehicle's electronics bill of materials by USD 80–200 per unit, which manufacturers struggle to absorb in mass-market models. This cost burden restrains the speed of adoption in emerging markets and among budget automakers, creating a notable barrier to the uniform global proliferation of automotive smart antenna technology.

Electromagnetic Interference and Integration Complexity in Modern Vehicle Architectures

Modern vehicles are increasingly dense with electronic systems, creating a challenging electromagnetic environment for smart antenna performance. Electric vehicles (EVs) and hybrid platforms introduce high-voltage power electronics that generate significant electromagnetic interference (EMI), which can degrade antenna sensitivity and communication reliability.

The International Electrotechnical Commission (IEC) standard IEC 61000 highlights that EMI mitigation in automotive-grade electronics demands additional shielding and filtering, adding weight and cost. With the rapid evolution toward software-defined vehicles and zonal electrical architectures, antenna placement and integration face compounding complexity, potentially limiting performance optimization and slowing the deployment cycle of next-generation smart antenna platforms.

Opportunity - Expansion of Electric and Autonomous Vehicles as High-Bandwidth Antenna Platforms

The accelerating global transition toward electric and autonomous vehicles represents a transformative opportunity for smart antenna manufacturers. Autonomous vehicles at SAE Level 3 and above require a dense array of communication modalities: 5G V2X, LiDAR-assisted GNSS, DSRC, and radar (76–81 GHz) all integrated seamlessly within the vehicle's antenna system. The International Energy Agency (IEA) reported that global electric vehicle sales reached 14 million units in 2023, with the fleet expected to surpass 300 million EVs by 2030.

Each autonomous or connected EV is projected to generate 4–5 terabytes of data per day (per Intel's estimates), necessitating ultra-high-frequency antenna arrays. Antenna suppliers that develop ultra-compact, multi-function modules supporting millimetre-wave bands will be exceptionally positioned to capture value in this rapidly expanding EV and autonomous vehicle ecosystem.

Surge in Smart Infrastructure and V2X Communication Deployments

Government investments in Intelligent Transportation Systems (ITS) and Vehicle-to-Everything (V2X) infrastructure are creating substantial new demand streams for automotive smart antennas. The U.S. Infrastructure Investment and Jobs Act (2021) allocated over USD 110 billion for transportation infrastructure, including USD 1 billion specifically for advanced transportation technologies such as V2X deployments.

China's Ministry of Transport has committed to deploying C-V2X (Cellular V2X) infrastructure along 90% of national highways by 2025. As smart city initiatives proliferate across Europe, North America, and the Asia Pacific, automotive antenna manufacturers that can deliver ultra-high-frequency modules supporting simultaneous C-V2X, GNSS, and 5G NR connectivity will unlock significant growth opportunities in both aftermarket and OEM channels.

Category-wise Analysis

Frequency Type Insights

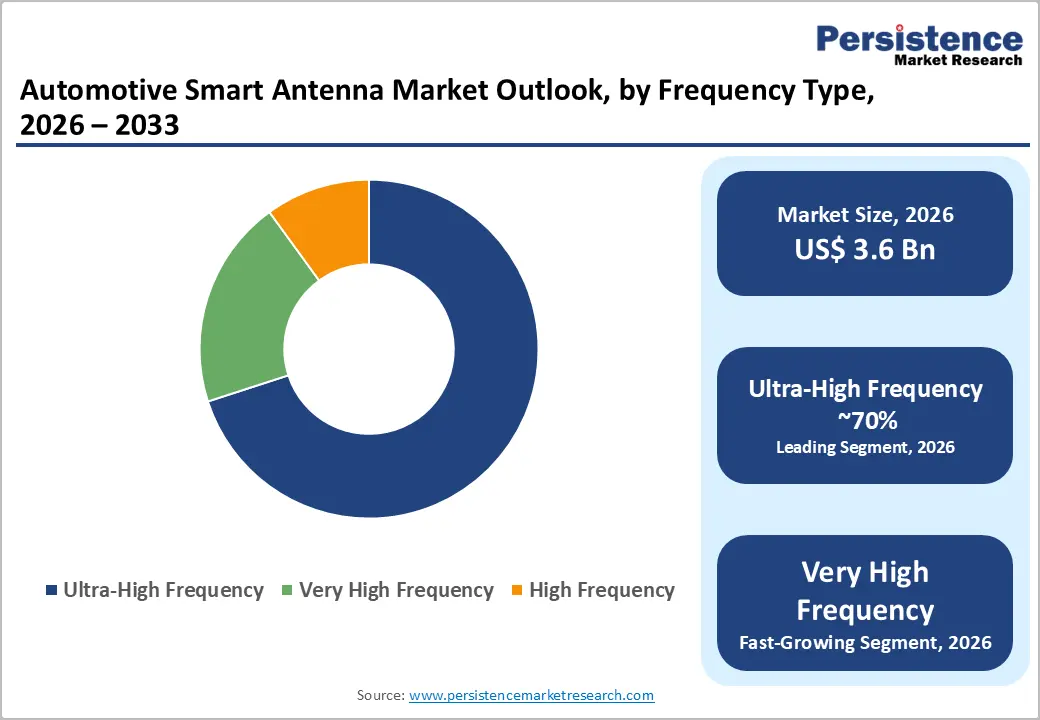

Among frequency type segments, the Ultra-High Frequency (UHF) segment commands the leading position in the automotive smart antenna market, accounting for approximately 48% of total market share. Ultra-high frequency antennas, operating in the 300 MHz to 3 GHz range, serve as the backbone for modern in-vehicle connectivity, supporting 4G LTE, 5G sub-6GHz, Wi-Fi, and GNSS applications simultaneously.

The widespread deployment of cellular telematics and V2X communication modules in modern vehicles necessitates UHF-capable antenna systems. According to the 3rd Generation Partnership Project (3GPP) standards, 5G NR bands n77 and n78 (operating at 3.3–4.2 GHz) are the primary deployment bands for automotive 5G globally, further reinforcing UHF antenna demand. The segment's technical versatility and its alignment with global connectivity mandates underpin its dominant market position.

Vehicle Type Insights

The passenger cars account for a dominant share in the automotive smart antenna market, representing approximately 65% of the total revenue. This dominance is underpinned by the sheer volume of global passenger car production and the high penetration of connectivity features in consumer vehicles. According to the Organisation Internationale des Constructers automobiles (OICA), global passenger car production reached 67.1 million units in 2023, representing a significant installed base for smart antenna integration.

Within passenger cars, the SUV sub-segment is particularly influential, with SUVs accounting for over 46% of all new passenger car registrations globally in 2023 (ACEA data). Premium and mid-range SUVs are increasingly equipped with advanced infotainment, ADAS (Advanced Driver-Assistance Systems), and connectivity packages, all requiring integrated multi-band smart antenna modules.

Antenna Type Insights

The shark fin antenna segment leads the antenna type category, accounting for approximately 72% share in 2026. The shark fin antenna's dominance reflects its superior ability to house multiple antenna elements: AM/FM, GPS, LTE/5G, Wi-Fi, and SiriusXM/DAB within a single, aerodynamically optimized form factor.

Unlike traditional fixed mast antennas, shark fin designs reduce aerodynamic drag and enhance vehicle aesthetics, aligning with modern automotive styling trends. The U.S. Environmental Protection Agency (EPA) and European Green Deal fuel efficiency directives are prompting OEMs to minimize drag coefficients, accelerating the shift from fixed mast to shark fin designs. Major global automakers, including Toyota, Volkswagen Group, and Stellantis, have standardized shark fin antennas across most of their new vehicle platforms, cementing the segment's market leadership.

Regional Analysis

North America Automotive Smart Antenna Market Trends & Analysis

North America represents a mature yet dynamically evolving market for automotive smart antennas, accounting for approximately 28% of global market revenue. The region's growth is driven by strong OEM adoption of connected vehicle technologies, supported by robust 5G infrastructure rollouts by carriers such as Verizon, AT&T, and T-Mobile. The NHTSA's V2X rulemaking initiative and the U.S. Department of Transportation's ITS Strategic Plan 2020–2025 are pivotal regulatory catalysts. Investments under the Bipartisan Infrastructure Law, allocating USD 550 billion for transportation modernization, further support antenna integration across commercial fleets.

U.S. Automotive Smart Antenna Market Size

The United States is the single largest national market in North America, contributing approximately 80% of the regional revenue. The country's advanced automotive manufacturing base, combined with regulatory push from the NHTSA for V2X readiness, positions the U.S. as a critical demand centre. Estimated at ~US$ 700 Mn in 2026, the U.S. market is forecasted to grow at a healthy pace through 2033, driven by a high concentration of premium and semi-autonomous vehicle sales.

Europe Automotive Smart Antenna Market Trends, Drivers, & Insights

Europe holds the second-largest share of the global automotive smart antenna market at approximately 26%, supported by stringent connectivity and safety mandates from the European Commission. The EU eCall mandate, active since April 2018, has been foundational in embedding GSM/UMTS antennas as standard in all new vehicles. The region is further propelled by the European Green Deal and the EU's Cooperative ITS (C-ITS) deployment framework, which promotes V2X communication across trans-European transport networks.

Germany Automotive Smart Antenna Market Size

Germany, home to BMW, Mercedes-Benz, Volkswagen Group, and Audi, is the dominant European market, accounting for approximately 22% of European regional revenue. The country's emphasis on premium connected vehicles and sophisticated ADAS platforms makes it a consistent high-value market for smart antenna systems, with an estimated market size of approximately ~US$ 180 Mn in 2026.

U.K. Automotive Smart Antenna Market Size

The United Kingdom represents a significant portion of European demand, supported by its Connected and Automated Mobility (CAM) Roadmap 2025 and ambitious autonomous vehicle testing programs. The U.K. market is estimated at approximately ~US$ 95 Mn in 2026, with notable growth expected as post-Brexit vehicle safety standards continue to align with EU frameworks and as EV penetration accelerates.

France Automotive Smart Antenna Market Size

France's market is anchored by Renault and Stellantis (PSA Group) production volumes and a government-backed EV adoption agenda. The French Ministry of Ecological Transition's electrification incentives are driving a generational upgrade in vehicle electronics. The French automotive smart antenna market is estimated at approximately ~US$ 75 Mn in 2026, expanding in line with growing connected vehicle mandates across the EU.

Asia Pacific Automotive Smart Antenna Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market, accounting for approximately 34% of global revenue and expanding at the highest regional CAGR. China's government-mandated C-V2X rollout and Japan's ITS Connect program are pivotal growth enablers. India's vehicle production boom and the Bharat NCAP crash test mandate (2023) requiring enhanced telematics are further catalysts. According to the OICA, Asia accounted for approximately 56% of global vehicle production in 2023, making it the foundational demand engine for automotive components globally.

China Automotive Smart Antenna Market Size

China is the world's largest automotive market and a dominant force in smart antenna adoption. The China Association of Automobile Manufacturers (CAAM) reported vehicle sales exceeding 30 million units in 2023. Backed by MIIT's Beidou telematics mandate for commercial vehicles and C-V2X infrastructure deployment targets, China's national market is estimated at approximately ~US$ 550 Mn in 2026 and is expected to see the strongest absolute growth over the forecast period.

India Automotive Smart Antenna Market Size

India is an emerging but rapidly growing market, driven by the Society of Indian Automobile Manufacturers (SIAM) reporting production volumes surpassing 5.8 million vehicles in FY2023–24. Regulatory catalysts including the AIS 140 mandate for vehicle tracking and growing 4G/5G penetration are accelerating smart antenna integration in commercial and passenger vehicles. India's market is estimated at approximately ~US$ 130 Mn in 2026, with an above-average regional CAGR driven by fleet modernization and EV policy support.

Japan Automotive Smart Antenna Market Size

Japan is a technologically advanced market with a strong focus on ITS and autonomous driving R&D. The Japan Automobile Manufacturers Association (JAMA) and the government's Strategic Innovation Promotion Program (SIP) for automated driving have driven consistent antenna technology upgrades across domestic OEMs like Toyota, Honda, and Nissan. Japan's market is estimated at approximately ~US$ 180 Mn in 2026, with steady growth in premium antenna modules for autonomous vehicle prototypes.

Competitive Landscape

The global automotive smart antenna market exhibits a moderately consolidated structure, with a handful of Tier-1 suppliers, including Laird Connectivity, Harada Industries, Kathrein Automotive, Continental AG, and TE Connectivity collectively commanding significant revenue shares. The market is characterized by intensive R&D investment in multi-band integration, miniaturization, and 5G mmWave compatibility. Key differentiators include the ability to integrate diverse frequency bands in a single antenna unit, partnership depth with major OEMs, and compliance with regional safety certifications such as UNECE R-155 for cybersecurity.

Key Developments

- In January 2025, Harada Industries announced the launch of its next-generation MIMO 5G shark fin antenna module for passenger cars, developed in collaboration with a leading Japanese OEM, designed to simultaneously support 5G NR, GNSS, V2X, and Wi-Fi 6E in a single compact unit.

- In December 2024, FORVIA HELLA began mass-producing fifth-generation 77 GHz radar in China. The unit achieves 360° detections, suggesting synergies between radar cooling and antenna packaging.

Companies Covered in Automotive Smart Antenna Market

- Mitsumi Electric Co., Ltd.

- Continental AG

- Harada Industry Co., Ltd.

- Molex

- INFAC Corporation

- Ficosa International SA

- Huf Group

- Harman International Inc.

- Fuba Automotive Electronics GmbH

- Laird Connectivity

Frequently Asked Questions

The global Automotive Smart Antenna Market is valued at approximately US$ 3.6 Bn in 2026 and is projected to reach US$ 7.8 Bn by 2033, growing at a compound annual growth rate (CAGR) of 11.7% during the forecast period from 2026 to 2033.

The primary demand drivers include the rapid proliferation of 5G-connected vehicles and V2X (Vehicle-to-Everything) communication systems, as well as stringent regulatory mandates such as the EU eCall regulation (Regulation (EU) 2015/758) and NHTSA V2X rulemaking in the U.S., which require embedded multi-band antenna systems in all new vehicles.

The Shark Fin Antenna segment is the clear leader, holding approximately 72% of the antenna type market share. Its dominance stems from its ability to accommodate multiple frequency bands within a single aerodynamic form factor, aligned with global OEM preferences and fuel efficiency directives from regulatory bodies including the EPA and the EU Green Deal.

Asia Pacific is the leading regional market, commanding approximately 34% of global revenue. The region's dominance is anchored by China's government-mandated C-V2X deployment, the region's share of over 56% of global vehicle production (OICA, 2023), and accelerating 5G network rollouts across key automotive markets.

Leading companies operating in the global Automotive Smart Antenna Market include Harada Industries Co., Ltd., Continental AG, TE Connectivity, Laird Connectivity (Aptiv), Kathrein Automotive GmbH, Yokowo Co., Ltd., and UFI Filters, among others.