- Executive Summary

- Global Automotive Plastic Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Automotive Plastic Market: Value Chain

- List of Raw Material Supplier

- List of Manufacturers

- List of Distributors

- List of End-users

- Profitability Analysis

- Forecast Factors - Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Global Parent Market Overview

- Other Macro-Economic Factors

- Price Trend Analysis, 2019 - 2032

- Key Highlights

- Key Factors Impacting Polymer Type Prices

- Prices by Polymer Type/Process/Application/

- Regional Prices and Polymer Type Preferences

- Global Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Market Volume (Unit) Projections

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size Analysis, 2019-2024

- Current Market Size Forecast, 2025-2032

- Global Automotive Plastic Market Outlook: Polymer Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Polymer Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Market Attractiveness Analysis: Polymer Type

- Global Automotive Plastic Market Outlook: Process

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By End-user, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Market Attractiveness Analysis: Process

- Global Automotive Plastic Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Application, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Market Attractiveness Analysis: Application

- Global Automotive Plastic Market Outlook: Process

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Process, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Market Attractiveness Analysis: Process

- Global Automotive Plastic Market Outlook: Sales Channel

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Sales Channel, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis: Sales Channel

- Key Highlights

- Global Automotive Plastic Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Region, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Region, 2025 - 2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa (MEA)

- Market Attractiveness Analysis: Region

- North America Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Polymer Type

- By End-user

- By Application

- By Process

- By Sales Channel

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025 - 2032

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Sales Channel, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis

- Europe Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Polymer Type

- By End-user

- By Application

- By Process

- By Sales Channel

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025 - 2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Sales Channel, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis

- East Asia Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Polymer Type

- By End-user

- By Application

- By Process

- By Sales Channel

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025 - 2032

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Sales Channel, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis

- South Asia & Oceania Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Polymer Type

- By End-user

- By Application

- By Process

- By Sales Channel

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025 - 2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Sales Channel, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis

- Latin America Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Polymer Type

- By End-user

- By Application

- By Process

- By Sales Channel

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025 - 2032

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Sales Channel, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis

- Middle East & Africa Automotive Plastic Market Outlook: Historical (2019 - 2024) and Forecast (2025 - 2032)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2019 - 2024

- By Country

- By Polymer Type

- By End-user

- By Application

- By Process

- By Sales Channel

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2025 - 2032

- GCC

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Polymer Type, 2025 - 2032

- Polypropylene (PP)

- Polyurethane (PU)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA / Nylon)

- Polycarbonate (PC)

- Polyethylene (PE)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Others (Acrylic (PMMA), PS, TTPEs)

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End-user, 2025 - 2032

- Commercial Vehicle

- Passenger Vehicle

- Compact

- Mid-Size

- SUVs

- Luxury

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Application, 2025 - 2032

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Process, 2025 - 2032

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Sales Channel, 2025 - 2032

- OEMs

- Aftermarket

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- BASF SE

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- SABIC

- Dow Inc.

- LyondellBasell Industries

- Covestro AG

- DuPont de Nemours, Inc.

- LG Chem

- Mitsubishi Chemical Holdings Corporation

- Evonik Industries AG

- Solvay S.A.

- Teijin Limited

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Sumitomo Chemical Co., Ltd.

- Lanxess AG

- Royal DSM N.V.

- Borealis AG

- Lear Corporation

- Magna International, Inc.

- Adient plc

- Grupo Antolin

- Hanwha Azdel Inc.

- Owens Corning

- Momentive Performance Materials, Inc.

- Quadrant AG

- Akzo Nobel N.V.

- BASF SE

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Plastic Market

Automotive Plastic Market Trends, Size, Share, Growth, Forecasts, 2025 - 2032

Automotive Plastic Market By Polymer Type (Polypropylene (PP), Polyurethane (PU), Polyvinyl Chloride (PVC), Others), Application (Interior Components, Others), Sales Channel (OEM, Aftermarket), End-user (Commercial Vehicle, Others), and Regional Analysis for 2025 - 2032

Automotive Plastic Market Share and Trends Analysis

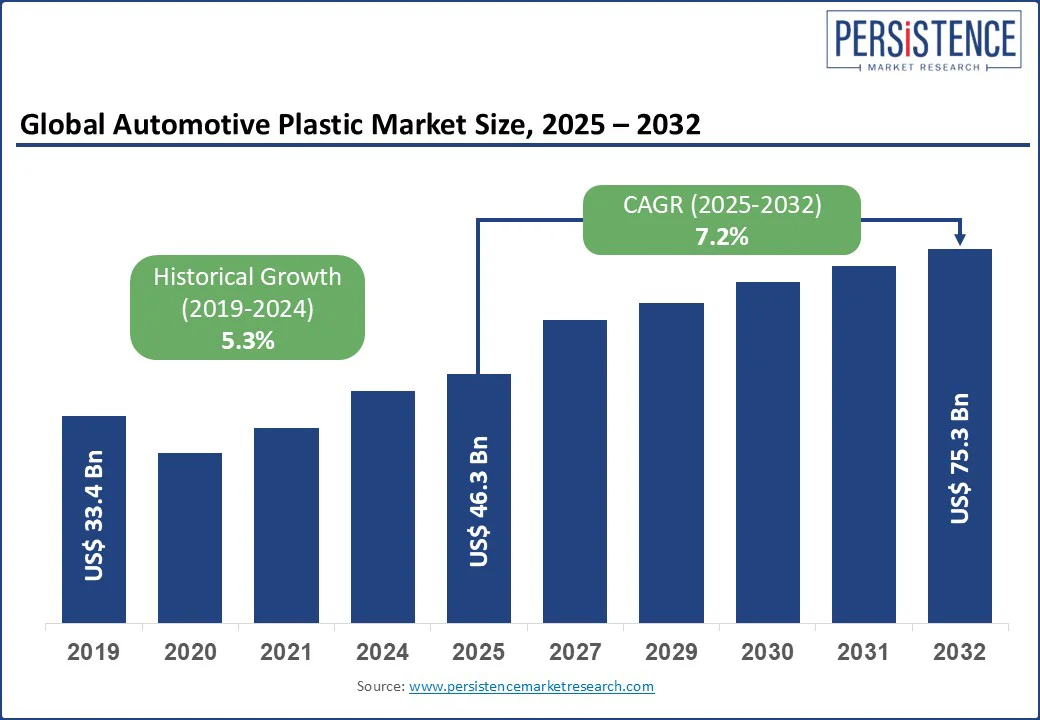

The global automotive plastic market size is likely to be valued at US$ 46.3 Bn in 2025, and is estimated to reach US$ 75.3 Bn by 2032, growing at a CAGR of 7.2% during the forecast period 2025 - 2032.

The automotive plastic market growth is driven by the rising demand for lightweight, cost-effective, and durable materials in vehicle production. Automakers across regions including the U.S., China, India, Germany, and the U.K. are actively integrating plastic components into interiors, exteriors, and under-the-hood applications to improve fuel efficiency and meet evolving safety and design expectations.

Plastics continue to replace heavier materials such as metals, helping to lower vehicle weight and support EV adoption. Applications such as dashboard panels, door trim components, seat backs, glove compartments, and center consoles rely heavily on specialty compounds such as polyamide and PP-based blends. Manufacturers have started using recycled feedstocks for interior trims and buckle covers. As sustainability becomes a major concern, companies are scaling up innovations in recycled and bio-based plastics.

Key Industry Highlights

- EV sales crossing 17 million globally in 2024 fuel surging demand for lightweight, safety-focused plastic battery components.

- Polypropylene dominates with 38.9% share in 2025, driven by widespread use in fascias, hoods, and interior trims across China, Germany, and the U.S.

- BASF’s rPCF plastics, produced with renewable energy, position the company as a frontrunner in low-emission automotive material solutions.

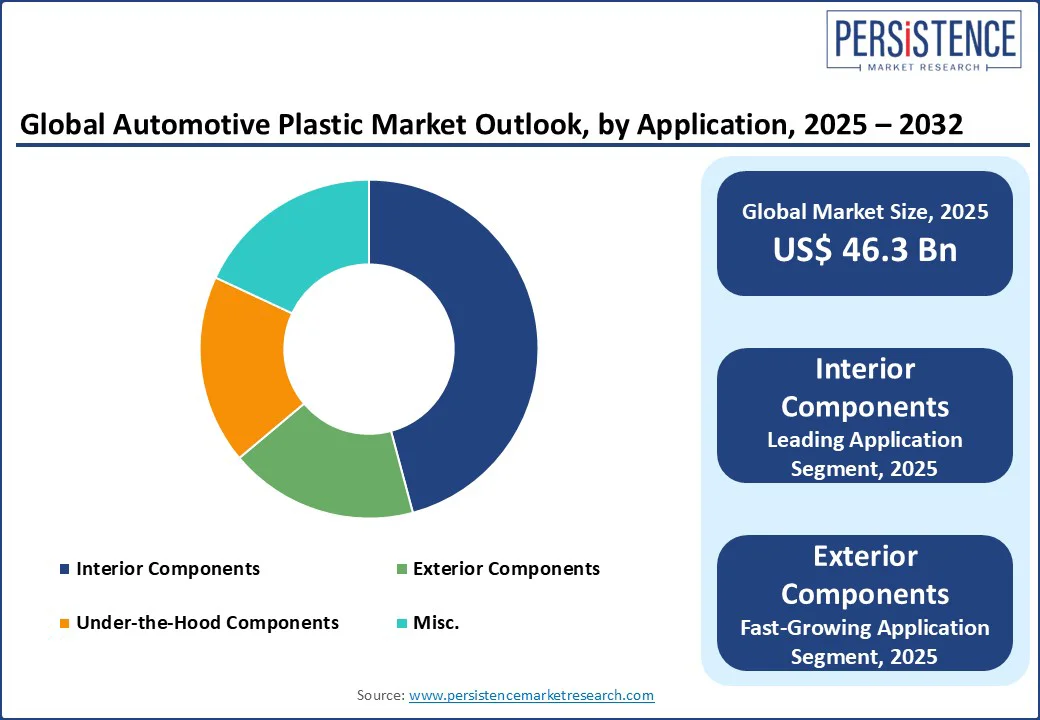

- Interior components are anticipated to command 45.5% of the automotive plastic market share in 2025, powered by demand for soft-touch, recyclable, and scratch-resistant compounds.

- Trade uncertainties and subsidy rollbacks in the U.S. and Europe disrupt near-term demand forecasts for automotive plastics.

- SABIC’s BLUEHERO™ platform drives next-gen plastic adoption in EV batteries with enhanced thermal and fire safety capabilities.

- Circular plastics and ISCC+ certified materials redefine OEM sustainability strategies across Germany, Japan, and the U.K.

| Global Market Attribute | Key Insights |

| Estimated Market Size (2025E) | US$ 46.3 Bn |

| Projected Market Value (2032F) | US$ 75.3 Bn |

| Value CAGR (2025 to 2032) | 7.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.3% |

Market Dynamics

Driver - Surge in Sustainable Plastics Reshaping Mobility Across the U.S., Europe, and Asia

The global shift toward lightweight, eco-conscious vehicles is driving significant demand for advanced plastic solutions, especially in North America, Europe, and Asia.

Companies such as BASF are leading this transition, introducing engineering plastics with reduced product carbon footprints (rPCF), using renewable electricity and steam during production. This not only meets OEMs' rising need to comply with Scope 3 emissions targets but also enables lighter vehicle structures that boost fuel efficiency.

With the U.S. automakers doubling down on fuel economy and sustainability mandates and German OEMs pushing for lifecycle emissions reductions, this transition is becoming integral to modern automotive design. Engineering plastics such as polyamides and polypropylene are now being adopted for interiors, under-the-hood, and structural components, reflecting their growing performance capabilities.

The growing availability of these materials across manufacturing hubs in the U.S., Germany, India, and China shows the convergence of sustainability and function. With pressure from end-consumers and regulators, the adoption of advanced plastics will continue to accelerate steadily.

Restraint - Volatile Regulatory and Trade Dynamics Cloud Market Consistency

While demand for high-performance automotive components continues to rise, the market faces disruptions from shifting regulatory and trade policies. In Europe, inconsistent subsidy programs and phased-out incentives across countries such as Germany and France slowed EV sales in 2024, curbing immediate demand for EV-related plastic components.

In the U.S., while the Clean Vehicle Tax Credit initially boosted interest, eligibility constraints limited its impact, creating uncertainty in EV production forecasts and indirectly impacting plastic component sourcing.

Increasing tariffs and geopolitical tensions have disrupted the supply chains for raw material and component flows between China, the U.S., and the EU. For instance, several Southeast Asian and Latin American countries, including Brazil and Thailand, began reinstating tariffs on imported EVs, particularly from China. Such moves impact the supply chain for automotive plastics, which often relies on cross-border trade of resins, additives, and tooling.

Opportunity - EV Boom Across Regions Opening New Frontiers for Advanced Plastics

With EV sales surpassing 17 million globally in 2024 and projected to exceed 20 million by 2025, the EV boom becomes a key growth catalyst for the plastic components market.

In China, EVs accounted for nearly half of all car sales in 2024, and this share is set to reach 60% in 2025, driving massive demand for lightweight plastic-intensive components such as battery enclosures, power electronics housings, and underbody covers.

Companies including SABIC have seized this momentum, offering advanced thermoplastics that enhance safety and reduce weight in EV batteries, directly responding to this global EV surge. Emerging markets such as Brazil, India, and Southeast Asia are also experiencing an electrification wave.

In Thailand and Vietnam, sales jumped nearly 50% in 2024, while Brazil more than doubled its EV sales. These vehicles require a new class of thermally stable, flame-retardant, and recyclable plastics. North America is also catching up, with the U.S. EV sales growing steadily and production expanding across Mexico.

Trend - Integration of Circular and High-Performance Plastics Reshaping OEM Strategy

OEMs and Tier 1 suppliers in Germany, Japan, and the U.S., are adopting circular plastics and next-gen composites as strategic priorities. The move goes beyond just compliance; it reflects a growing shift in brand value tied to sustainability.

Automakers in Europe, including in the U.K. and France, are actively seeking ISCC+ certified polymers and high-recycled content materials, a trend accelerated by companies such as SABIC and BASF who are ramping up their global footprint with greener materials. North American players are also embracing this change. Major events such as The Battery Show North America showcased plastic innovations tailored for EVs with a strong focus on recyclability and thermal performance.

Asia, led by Chinese EV makers, is increasingly adopting lightweight thermoplastics to boost vehicle range and affordability. This cross-regional move toward circularity and performance is defining the long-term evolution of vehicle architecture, creating a new standard where automotive plastic is both functional material and sustainability enabler.

Category-wise Analysis

Polymer Type Insights

By polymer type, the polypropylene segment is expected to capture a market share of around 38.9% in 2025, driven by its strong compatibility with automotive design needs and the global push for lighter, fuel-efficient vehicles. Its chemical resistance, heat tolerance, and ease of molding allow manufacturers to create complex components such as bumper fascias, engine covers, and instrument panels with both durability and design flexibility.

China, Germany, and the U.S. are leading the trend, with initiatives such as LyondellBasell’s 2024 partnership in China demonstrating how polypropylene continues to replace traditional metals in critical parts such as the launch of the first lightweight plastic engine hood for NEVs using Hifax compounds.

As automakers focus on optimizing vehicle performance while keeping costs in check, polypropylene stands out for its ability to deliver strength without added weight. Its application stretches across both electric and conventional vehicles, with widespread use seen in countries including South Korea, Japan, and Italy.

Interior trims, battery casings, and cable insulation built with PP showcase how the material enhances safety, thermal performance, and efficiency. With global investments backing lightweighting strategies and a growing demand for smart manufacturing, polypropylene will continue to shape the future of automotive plastic innovations.

Application Insights

By application, the interior components segment is projected to hold a market share of around 45.5% in 2025, driven by the rising focus on comfort, lightweight design, and sustainability in vehicle cabins. From center consoles and glove boxes to pillar trims and door panels, interior components are evolving as a focal point for OEMs across North America, Germany, and China.

Materials such as LyondellBasell’s Hostacom and Softell are setting a new benchmark with their scratch resistance, soft-touch finishes, and low emissions making them ideal for both mass-market and premium vehicles. In the U.S., companies are shifting to alternatives such as MIRUM® leather and foamable compounds that support weight reduction, thereby diminishing carbon emissions and enhancing the user experience.

Globally, automakers are investing in closed-loop systems and greener feedstocks for interior applications. In countries including Germany and the U.S., new compounds made from recycled plastics, such as those developed by LyondellBasell and used by Audi, are now replacing virgin materials in visible cabin parts. Recycled maritime waste, repurposed into trim components is a growing standard.

Regional Insights

East Asia Automotive Plastic Market Trends

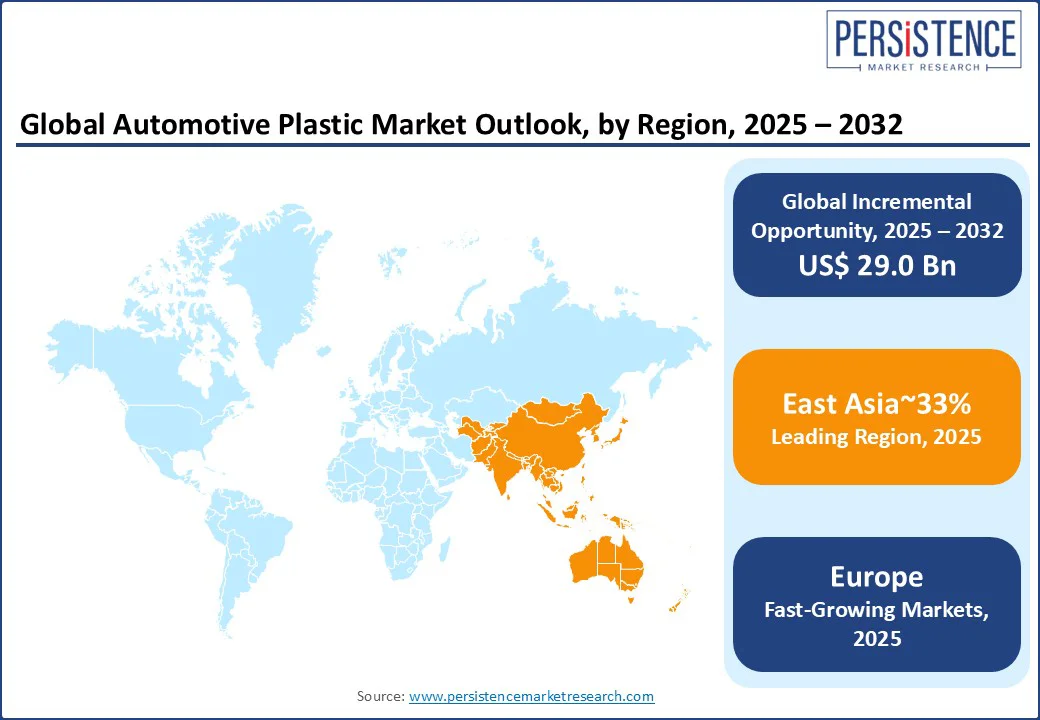

East Asia is anticipated to capture a market share of approximately 33% in the automotive plastic market, driven by strong vehicle production, rising EV adoption, and growing demand for lightweight, sustainable components. China continues to lead with massive output and supportive policies such as tax incentives and EV subsidies. The shift toward electric and autonomous vehicles is accelerating material innovation, with companies such as SABIC launching advanced plastics that enhance safety and performance, especially in battery and sensor applications. Japan and South Korea’s robust manufacturing base supports consistent demand for engineering plastics across interiors, structural parts, and lightweight body panels.

Automotive plastic trends in East Asia also reflect a major transition to circularity and bio-based materials. Dow’s collaboration with Guangdong Delian and Covestro’s closed-loop pilot program highlight the region’s move toward recycled and recyclable plastic use in vehicles. Companies such as LG Chem are pushing the envelope with bio-nylon and flame-retardant compounds for EVs, reinforcing the market’s focus on low-emission and high-performance materials. These developments open growth opportunities in both sustainable product lines and localized plastic supply chains, keeping East Asia central to the evolving automotive plastics ecosystem.

Europe Automotive Plastic Market Trends

Europe region is expected to exhibit the fastest growth in 2025, driven by strong environmental policies, rising demand for electric vehicles, and the growing adoption of lightweight materials across key markets including Germany, France, and Italy. Automotive plastics play a major role in this shift, reducing vehicle weight and emissions. In France and Portugal, for instance, Teijin Automotive Technologies is producing composite panels that are 43% lighter than traditional materials, signaling how innovation is reshaping vehicle design in Europe.

The Global Impact Coalition’s 2025 initiative to recycle plastics from end-of-life vehicles reflects a turning point toward circularity, especially in markets including Germany and the U.K. Italy and Spain are boosting their manufacturing capacity for advanced polymers, aligning with the EU’s long-term roadmap to achieve net-zero emissions by 2050. With manufacturers across Europe integrating Solvay’s fast-curing carbon fiber prepregs and expanding lightweight component production, the region is positioned to lead the global transition to cleaner, smarter mobility powered by next-generation automotive plastic solutions.

North America Automotive Plastic Market Trends

The market growth in North America region is driven by the strong presence of auto production hubs in the U.S. and Canada, along with increasing use of lightweight materials to meet evolving fuel economy and emission norms.

With around 15.8 million vehicles produced across the region in 2023, the U.S. leads the shift toward advanced material integration, especially in electric and hybrid vehicles. Automakers in the U.S. continue to use plastics across bumpers, instrument panels, and battery systems to bring down vehicle weight while boosting performance. Vehicles today carry 426 pounds of plastics and composites on average, an indicator of how deeply integrated these materials have become in vehicle design. The demand pattern shows a steady increase in the use of polymer composites as a long-term strategy to reduce emissions and enhance design flexibility.

Competitive Landscape

The global automotive plastic market reflects a consolidated competitive landscape, with key players such as BASF SE, SABIC, Dow Inc., LyondellBasell Industries, Covestro AG, DuPont, LG Chem, Mitsubishi Chemical Holdings Corporation, and Evonik Industries AG dominating the value chain. These companies are adopting strategies focused on lightweighting, sustainability, and advanced material innovation, driven by the shift toward EVs and stricter global emission standards.

Manufacturers are deepening collaborations with OEMs and integrating recycled and bio-based content into their product lines to keep up with the demand. Leading manufacturers are aggressively investing in circularity and closed-loop recycling systems, particularly in regions including Europe, North America, and China, where regulations and consumer expectations are accelerating the push for eco-friendly solutions. Advanced polyamides, polycarbonates, and PBT blends are replacing metals in structural parts to reduce vehicle weight and emissions, especially in electric vehicles.

The market is expected to see stable long-term growth, with top players expanding production capacity and technological capabilities to maintain their competitive edge across global automotive hubs such as the U.S., Germany, India, and China.

Key Developments

- In June 2025, BASF introduced its rPCF portfolio aimed at the automotive industry, offering plastics produced using renewable electricity and steam. This move supported automakers’ goals to reduce Scope 3 emissions aligning with industry demand for sustainable material solutions.

- In April 2025, SABIC launched its BLUEHERO™ platform focusing on advanced plastic materials for electric vehicle battery components. These materials aim to improve thermal management, fire safety, and structural integrity in EVs.

Companies Covered in Automotive Plastic Market

- BASF SE

- SABIC

- Dow Inc.

- LyondellBasell Industries

- Covestro AG

- DuPont de Nemours, Inc.

- LG Chem

- Mitsubishi Chemical Holdings Corporation

- Evonik Industries AG

- Solvay S.A.

- Teijin Limited

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Sumitomo Chemical Co., Ltd.

- Lanxess AG

Frequently Asked Questions

The global automotive plastic market is projected to be valued at US$ 46.3 Bn in 2025.

Polypropylene (PP) polymer type is expected to hold approximately 38.9% market share in 2025, driven by its lightweight, cost-effective, and high-performance properties ideal for complex automotive components across electric and conventional vehicles.

The automotive plastic market is poised to witness a CAGR of 7.2% from 2025 to 2032.

The growing adoption of sustainable plastics is transforming vehicle design strategies across the U.S., Europe, and Asia to meet emission and circularity goals.

The rapid expansion of the EV market worldwide is unlocking significant demand for high-performance, lightweight plastic components.

Prominent players include BASF SE, SABIC, Dow Inc., LyondellBasell Industries, Covestro AG, DuPont, LG Chem, Mitsubishi Chemical Holdings Corporation, and Evonik Industries AG.