- Automotive Components & Materials

- Automotive Lubricant Market

Automotive Lubricant Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Lubricant Market by Product Type (Engine Oil, Transmission Fluid, Gear Oil, Greases, Hydraulic Fluids, Brake Fluids, Coolants & Antifreeze, Others), Base Oil Type (Mineral Oil Lubricants, Synthetic Lubricants, Semi-Synthetic Lubricants, Bio-based Lubricants), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers, Three-Wheelers, Off-Highway Vehicles, Electric Vehicles), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Automotive Lubricant Market Size and Trend Analysis

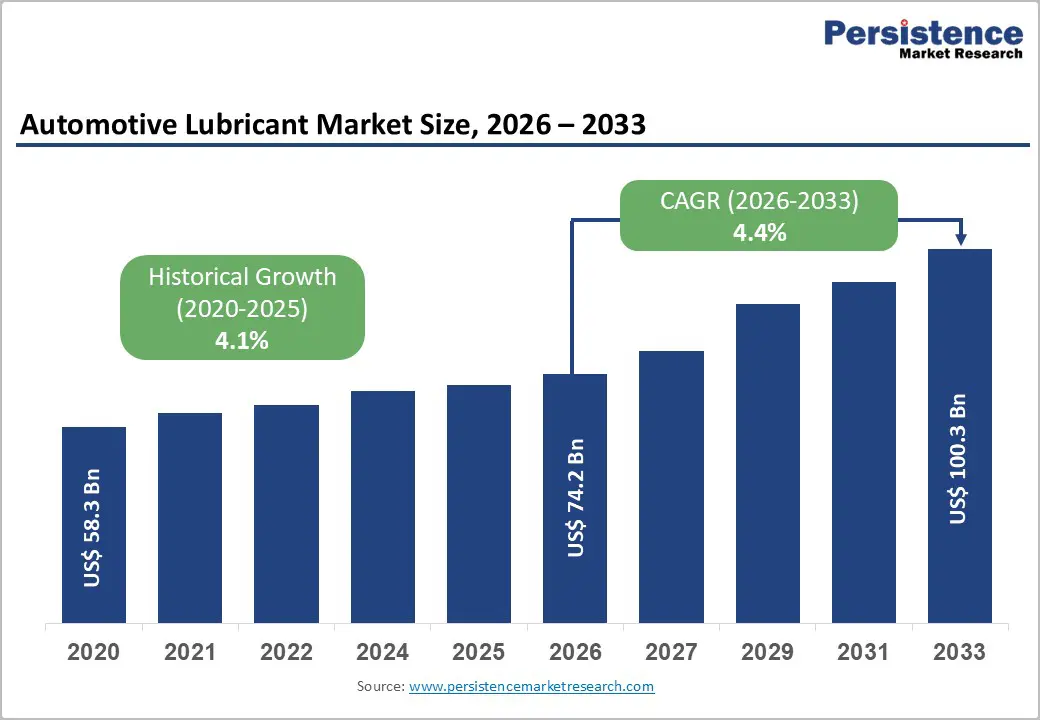

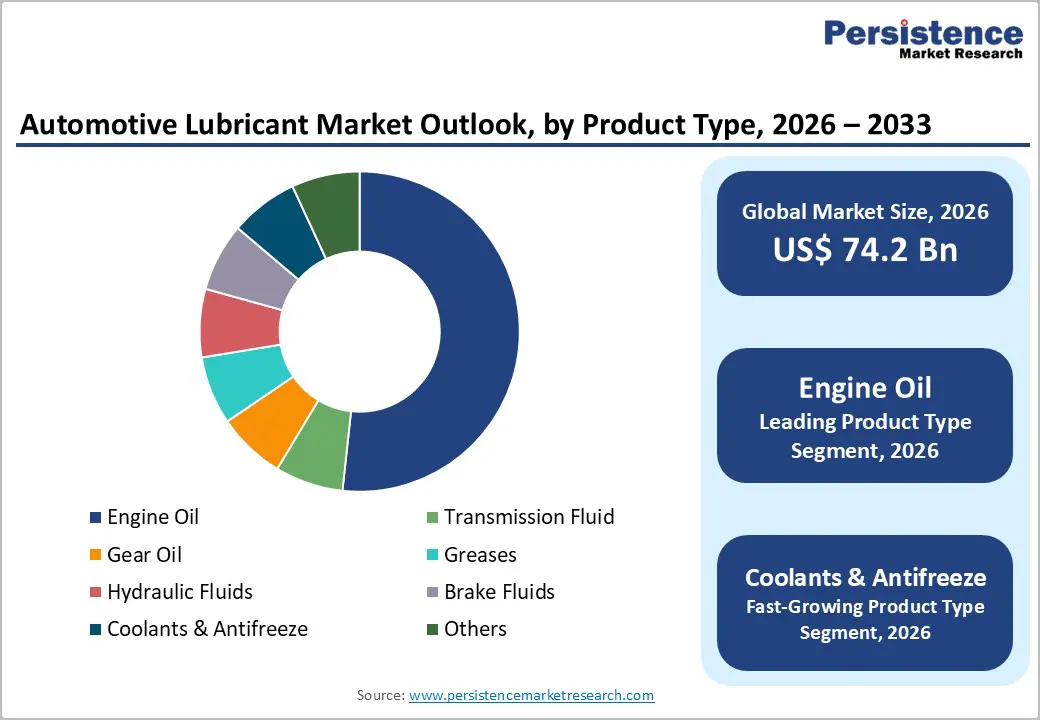

The global Automotive Lubricant market size is expected to be valued at US$ 74.2 billion in 2026 and projected to reach US$ 100.3 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033 Robust global vehicle fleet expansion, tightening engine emission and fuel efficiency regulations, and the progressive shift from mineral to high-performance synthetic and semi-synthetic lubricants are the structural pillars propelling the automotive lubricant market forward.

The International Organization of Motor Vehicle Manufacturers (OICA) reports global vehicle production surpassing 90 million units in 2023, with the in-use vehicle fleet exceeding 1.4 billion units globally, each requiring periodic lubricant maintenance. Concurrently, the proliferation of turbocharged, downsized engines and extended oil drain interval specifications mandated by OEMs and regulatory bodies, including the American Petroleum Institute (API) and the European Automobile Manufacturers' Association (ACEA) is driving a premium product mix shift, sustaining revenue growth above pure volume growth rates across the forecast period.

Key Industry Highlights:

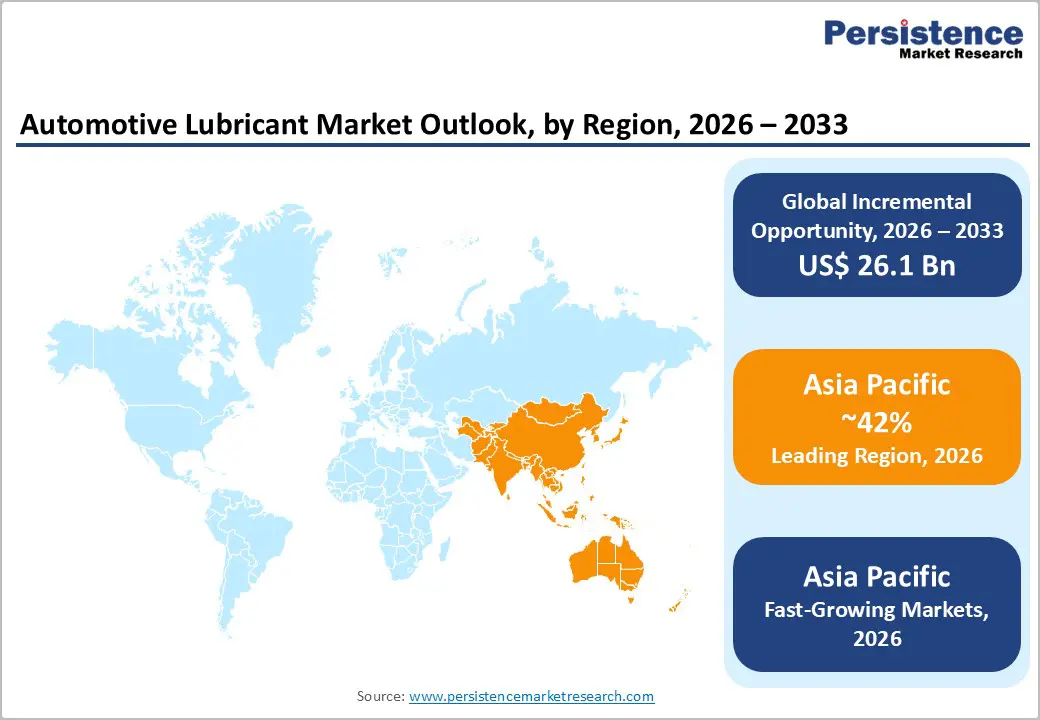

- Leading Region: Asia Pacific leads the global Automotive Lubricant market with approximately 42% consumption share in 2025, driven by China's world-scale vehicle production, India's rapidly expanding vehicle fleet exceeding 300 million registered units, and robust ASEAN two-wheeler and commercial vehicle growth.

- Fastest Growing Region: Asia Pacific is also the fastest growing region at approximately 5.3% CAGR through 2033, underpinned by India's middle-class motorization surge, China's NEV transition creating EV-fluid demand, and expanding industrial and off-highway vehicle lubricant consumption across Indonesia, Thailand, and Vietnam.

- Dominant Segment: Engine Oil dominates the Product Type category with approximately 57% market share in 2025, reflecting its universal application across all ICE vehicle categories and continuous premiumization driven by API SP, ILSAC GF-6, and ACEA specification upgrades mandating advanced synthetic formulations globally.

- Fastest Growing Segment: Synthetic Lubricants are the fastest growing Base Oil Type segment, propelled by OEM extended drain interval mandates, Euro 7 and EPA CAFE low-viscosity requirements, and the emergence of purpose-engineered EV e-fluids and battery thermal management products commanding 2–3x conventional lubricant price premiums.

- Key Opportunity: The key market opportunity is purpose-engineered EV lubricants and thermal management fluids, with the global EV fleet projected to reach 250 million units by 2030 per the IEA, offering lubricant manufacturers a high-margin, high-growth specialty segment offsetting conventional ICE lubricant volume displacement through 2033.

| Key Insights | Details |

|---|---|

|

Automotive Lubricant Market Size (2026E) |

US$ 74.2 Billion |

|

Market Value Forecast (2033F) |

US$ 100.3 Billion |

|

Projected Growth CAGR (2026–2033) |

4.4% |

|

Historical Market Growth (2020–2025) |

4.1% |

Market Dynamics

Drivers - Expanding Global Vehicle Fleet and Rising Demand for Extended Drain Interval Lubricants

The relentless expansion of the global motorized vehicle fleet, now exceeding 1.4 billion in-use vehicles per OICA data, creates a structurally massive and recurring aftermarket demand base for automotive lubricants that grows independently of new vehicle sales cycles. In emerging economies, vehicle ownership rates remain far below developed market saturation levels: India surpassed 300 million registered vehicles in 2024 per the Ministry of Road Transport and Highways (MoRTH), while ASEAN motorization rates continue to accelerate. Equally significant is the automotive industry's transition to extended oil drain interval specifications: modern API SP and ILSAC GF-6-certified engine oils now deliver drain intervals of 10,000–15,000 miles versus 3,000–5,000 miles for conventional oils, driving consumers and fleet operators toward premium synthetic and semi-synthetic products that carry significantly higher per-unit revenues, sustaining market value growth even as volume consumption per vehicle moderates in mature markets.

Stringent Emission Regulations Driving Premium Lubricant Adoption

Global tightening of vehicular emission norms is compelling automotive manufacturers to reformulate engines for improved fuel economy and lower tailpipe emissions, directly increasing technical requirements for engine oils and transmission fluids. The European Union's Euro 7 emission standard, formally adopted in 2024, imposes the strictest particulate matter and NOx limits to date on passenger cars and commercial vehicles, requiring low-viscosity, low-SAPS (Sulfated Ash, Phosphorus, and Sulfur) engine oils compatible with advanced after-treatment systems including Diesel Particulate Filters (DPF) and Selective Catalytic Reduction (SCR) catalysts. In the United States, the Environmental Protection Agency (EPA) and National Highway Traffic Safety Administration (NHTSA) finalized the most stringent ever CAFE fuel economy standards for 2027–2032 model year vehicles in 2024, mandating fleetwide average fuel economy improvements that necessitate advanced low-friction lubricant formulations. The API's ongoing PC-12 engine oil category development, targeting combustion efficiency and hybrid vehicle compatibility, exemplifies how regulatory pressure continuously elevates lubricant performance specifications and average selling prices across the automotive lubricant value chain.

Restraints - Electric Vehicle Proliferation and Structural Lubricant Demand Displacement

The accelerating transition to battery electric vehicles (BEVs) presents the most structurally significant long-term restraint on automotive lubricant demand, as BEVs require no conventional engine oil, transmission fluid, or coolant in the traditional sense. The International Energy Agency (IEA) reported global EV sales surpassing 14 million units in 2023, representing over 18% of total new car sales, up from near-zero a decade earlier. While EVs still require specialized e-fluids, thermal management fluids, and greases, the per-vehicle lubricant consumption is estimated at 30–60% lower versus comparable internal combustion engine (ICE) vehicles, creating a structural volume displacement in markets with rapid EV adoption trajectories including China, Norway, and Germany.

Base Oil Price Volatility and Feedstock Dependency

Automotive lubricant margins remain acutely sensitive to base oil price fluctuations; as base oils constitute 70–90% of finished lubricant formulation costs. Both Group I/II mineral base oils and Group III/IV synthetic base oils are derived from or co-produced with petroleum refining, making their pricing highly correlated with crude oil benchmarks and refinery utilization rates. The Brent crude price range of US$ 70–100/bbl experienced during 2022–2024 translated into significant raw material cost volatility for lubricant manufacturers, compressing blending margins and constraining the ability to pass through cost increases to price-sensitive aftermarket consumers. According to the American Chemistry Council (ACC), specialty chemicals producers, including lubricant additive manufacturers, experienced feedstock cost escalations of 15–25% during peak commodity inflation periods, limiting profitability across the value chain.

Opportunities - Specialized E-Fluids and Thermal Management Lubricants for Electric Vehicles

While BEV proliferation constrains conventional lubricant volumes, it simultaneously unlocks a rapidly growing premium specialty opportunity in EV-specific lubricants and thermal management fluids. Electric drivetrains require purpose-engineered transmission fluids compatible with copper and electrical components; conventional lubricants containing sulfur or phosphorus additives can degrade motor windings and cause insulation failure. Battery thermal management fluids, critical for maintaining lithium-ion battery cells within the optimal 15–35°C operating window for range and longevity, represent an entirely new, high-value product category.

Shell plc, TotalEnergies SE, ExxonMobil Corporation, and Fuchs SE have all launched dedicated EV fluid portfolios between 2022 and 2025. According to the IEA, the global EV fleet is projected to reach 250 million units by 2030, creating a structural addressable market for specialized e-fluids and thermal management products that did not exist a decade ago. The premium pricing of EV-grade fluids, typically 2–3x conventional ICE lubricant pricing, offers lubricant manufacturers a compelling margin-accretive transition pathway aligned with the automotive industry's electrification trajectory.

Bio-based and Sustainable Lubricants Under Circular Economy Regulations

The global regulatory push toward circular economy principles and sustainable chemistry is creating a meaningful commercial opportunity for bio-based and re-refined lubricant producers. The European Union's Regulation (EU) 2023/1542 on batteries and the broader EU Green Deal industrial strategy explicitly prioritize bio-based and recycled-content materials in automotive components, a framework increasingly extending to fluid maintenance products. The U.S. Environmental Protection Agency's (EPA) Significant New Alternatives Policy (SNAP) program and BioPreferred® initiative, operated by the U.S. Department of Agriculture (USDA), mandate bio-based product procurement preferences in federal vehicle fleets, catalyzing commercial adoption. The European Lubricating Grease Institute (ELGI) and the European Lubricants Industry Association (UEIL) document growing demand for vegetable oil-based greases and bio-synthetic esters across forestry, agricultural, and urban fleet applications where environmental contamination risk is regulated. The re-refined base oil segment, where used motor oil is re-processed to Group II+ specification through hydrotreatment, is attracting investment from Safety-Kleen (a Clean Harbors company) and Avista Oil AG, aligning with EU end-of-life vehicle and waste oil recovery targets under the Waste Framework Directive.

Category-wise Analysis

Product Type Insights

Engine Oil is the dominant product type in the global automotive lubricant market, commanding approximately 57% of total share in 2025. The American Petroleum Institute (API) and the International Lubricant Standardization and Approval Committee has (ILSAC) maintained rigorous and regularly updated specification categories, currently API SP and ILSAC GF-6A/B, that define minimum performance requirements for passenger car motor oils in the U.S., while the ACEA sets equivalent European standards. The transition toward lower-viscosity engine oils (0W-20, 0W-16, and emerging 0W-8 grades) mandated by OEMs seeking fuel economy improvements is consistently driving consumers toward higher-specification, premium-priced fully synthetic formulations, sustaining revenue growth above volume trends and reinforcing engine oil's market value leadership.

Base Oil Type Insights

Mineral Oil Lubricants retain market leadership in the Base Oil Type category, accounting for approximately 46% of global automotive lubricant consumption by volume in 2025. This dominance is anchored by mineral oil lubricants' cost competitiveness, extensive established supply chain infrastructure, and continued widespread use across high-volume, price-sensitive vehicle segments, particularly two-wheelers, commercial fleet vehicles in developing economies, and the vast in-use fleet of older passenger cars in Africa, Latin America, and parts of Asia that do not require premium synthetic specification. Group I and Group II mineral base oils are produced by the majority of global petroleum refiners, ensuring reliable supply availability at competitive pricing. While Synthetic Lubricants represent the fastest-growing base oil segment, driven by OEM factory fill specifications, extended drain intervals, and EV fluid requirements, mineral base oils will maintain significant volume share through the forecast period given the sheer scale and longevity of the global ICE vehicle fleet in emerging and developing markets.

Vehicle Type Insights

Passenger Cars constitute the dominant vehicle type segment, accounting for approximately 44% of global Automotive lubricant consumption in 2025. This dominance mirrors the passenger car's position as the world's most numerous motorized vehicle category, with OICA documenting global passenger car production of approximately 67 million units in 2023 and an in-use fleet estimated at over 1 billion vehicles. Passenger car motor oils (PCMO) are subject to the most stringent and frequently updated OEM and API/ACEA specifications, driving continuous product upgrades and premium mix enrichment that sustain average revenue per liter above other vehicle categories. The growth of turbocharged gasoline direct injection (TGDI) engines, now standard across most new passenger car platforms, including those from Volkswagen AG, Toyota Motor Corporation, and General Motors, requires engine oils with enhanced thermal stability and deposit control properties, reinforcing the shift toward premium and synthetic formulations and the segment's continued market revenue leadership.

Sales Channel Insights

The aftermarket sales channel commands approximately 68% of global Automotive Lubricant market share in 2025, reflecting the fundamental economics of vehicle maintenance: while OEM factory-fill lubricants are specified at the point of vehicle manufacture, the far larger replacement maintenance market over a vehicle's 10–15 year service life is served through independent workshops, quick-lube chains, automotive parts retailers, and e-commerce channels.

The aftermarket channel is characterized by significant brand loyalty to recognized premium labels including Shell Helix, Mobil 1, Castrol (BP plc), and Total Quartz (TotalEnergies SE), as well as intense competition from private-label and economy-tier brands in price-sensitive markets. The proliferation of e-commerce automotive parts and lubricant platforms, including Amazon, Alibaba, and regional platforms, is reshaping aftermarket distribution, enabling consumers to compare specifications and pricing across brands with unprecedented transparency. In India, the Motor Industry of India (ACMA) documents the organized aftermarket growing faster than the overall lubricant market, driven by expanding service networks and increasing consumer awareness of recommended oil change intervals.

Regional Insights

North America Automotive Lubricant Market Trends and Insights

North America leads the global Automotive Lubricant market with approximately 26% share in 2025, anchored by the United States' position as the world's second-largest vehicle market and the most technologically advanced lubricant consumer. The U.S. market is characterized by high synthetic lubricant penetration, with Mobil 1 (ExxonMobil), Shell Pennzoil, and Valvoline commanding significant brand equity, and progressive regulatory requirements from the EPA and NHTSA mandating fuel economy improvements that necessitate low-viscosity, premium-specification engine oils. The API's PC-12 next-generation engine oil category, under active development with ILSAC, is expected to further elevate baseline lubricant specifications across the U.S. passenger car fleet from 2026 onwards.

The quick-lube service channel, dominated by Jiffy Lube (Shell), Valvoline Instant Oil Change, and Firestone, provides a highly accessible mass-market distribution infrastructure for premium branded lubricants. Canada's market mirrors U.S. trends with additional emphasis on low-temperature performance specifications given its extreme winter climate, driving higher 0W-xx grade penetration. The North American commercial vehicle sector, particularly long-haul trucking in the Permian Basin and Midwest logistics corridors, sustains robust demand for API CK-4 and FA-4 certified heavy-duty engine oils, with Shell, ExxonMobil, and Chevron's Delo brand leading fleet lubricant supply.

Europe Automotive Lubricant Market Trends and Insights

Europe represents a premium, specification-driven automotive lubricant market, where the ACEA's engine oil sequences, ACEA A/B for passenger cars and ACEA E for heavy-duty engines, define minimum performance requirements that are among the world's most technically demanding. Germany leads regional consumption, home to major lubricant producers Fuchs SE and headquarters of OEM groups Volkswagen AG, BMW Group, and Mercedes-Benz Group AG, all of which mandate proprietary OEM-approval lubricant specifications (VW 508.00/509.00, BMW Longlife-04, MB 229.52) that effectively segment the premium aftermarket and drive consumers toward approved products. France hosts TotalEnergies SE's lubricants headquarters, while Shell's European operations serve U.K. and broader Western European markets.

The EU Green Deal and Euro 7 emission standard are reshaping the European lubricant landscape toward ultra-low-viscosity, low-SAPS formulations and bio-based lubricant alternatives. Spain and Italy, with their large two-wheeler and light commercial vehicle segments, contribute significant mid-tier lubricant demand. The European Union's End-of-Life Vehicles Directive revision (proposed 2023) and Waste Oils Directive are reinforcing re-refined base oil and bio-lubricant adoption, with UEIL reporting growing recycled content mandates in national public procurement frameworks across Germany, France, and the Netherlands. The European Chemicals Agency (ECHA) is also reviewing PAH restrictions in mineral-based lubricants, potentially accelerating the shift to Group III synthetic base stocks across the European aftermarket.

Asia Pacific Automotive Lubricant Market Trends and Insights

Asia Pacific is both the largest and fastest growing automotive lubricant market globally, accounting for approximately 42% of global consumption in 2025 and projected to register a CAGR of approximately 5.3% through 2033. China, the world's largest vehicle market, producing over 30 million vehicles in 2023 per OICA data, is the epicenter of regional and global lubricant demand, served by Sinopec Corporation, China National Petroleum Corporation (CNPC), and multinational majors including Shell, ExxonMobil, and TotalEnergies. China's aggressive NEV push, with New Energy Vehicle (NEV) penetration exceeding 35% of new car sales in 2024 per the China Passenger Car Association (CPCA), is simultaneously displacing conventional lubricant volumes and driving rapid growth in EV-specific e-fluid demand.

India is the region's most dynamic growth market, with MoRTH reporting over 300 million registered vehicles as of 2024 and the Society of Indian Automobile Manufacturers (SIAM) documenting robust two-wheeler and passenger car production growth supported by expanding middle-class vehicle ownership. Petronas Lubricants International, IDEMITSU, and Indian Oil Corporation's SERVO brand are active in this high-growth market. Japan's advanced lubricant market, driven by ENEOS Corporation, Idemitsu Kosan, and Toyota's proprietary fluid specifications, emphasizes ultra-low-viscosity 0W-16 and 0W-8 grades pioneered by Toyota Motor Corporation for its hybrid powertrains. ASEAN nations, particularly Indonesia, Thailand, and Vietnam, provide high-volume growth through expanding two-wheeler and commercial vehicle fleets, benefiting from low-cost domestic mineral lubricant production and growing access to international branded products.

Competitive Landscape

The global automotive lubricant market exhibits a moderately consolidated structure at the premium branded segment, where a limited group of multinational oil and lubricant producers command a substantial share of global revenue. At the same time, the broader market remains highly fragmented due to the presence of numerous regional blenders and state-owned enterprises, particularly across Asia, the Middle East, and Latin America, serving domestic demand and price-sensitive aftermarket segments.

Market participants primarily compete through extensive OEM approval portfolios, advanced additive and base oil technologies, and strong brand positioning within the automotive aftermarket. Leading suppliers also leverage global distribution networks, strategic partnerships with vehicle manufacturers, and investments in high-performance synthetic formulations. Emerging business strategies include the development of specialized EV fluids, expansion into bio-based lubricants, and the use of digital platforms for predictive maintenance and oil condition monitoring. In addition, acquisitions of regional lubricant blenders and expansion of localized blending facilities are becoming common strategies to strengthen presence in fast-growing emerging automotive markets.

Key Developments:

- August, 2025: Valvoline Cummins Private Limited announced a four-year strategic collaboration with Mahindra & Mahindra Ltd. to supply high-performance engine, transmission, and axle lubricants under the Maximile brand across Mahindra’s dealership and aftermarket networks, strengthening supply chain efficiency and sustainability initiatives.

- October, 2025: Repsol announced a strategic partnership with MotoGP organizer Dorna Sports to become the exclusive lubricant supplier for Moto2 and Moto3 categories from 2026 to 2030, strengthening its global lubricants expansion strategy and motorsport technology development.

- October, 2025: ExxonMobil secured a potential US$954 million U.S. Navy contract to supply marine lubricants and engineering support services under the Military Sealift Command’s Worldwide Lubrication Program, covering products such as engine oils, turbine oils, hydraulic fluids, and technical shipboard support.

Companies Covered in Automotive Lubricant Market

- Shell plc

- ExxonMobil Corporation

- BP plc (Castrol)

- TotalEnergies SE

- Chevron Corporation

- Valvoline Inc.

- Fuchs SE

- Idemitsu Kosan Co., Ltd.

- ENEOS Corporation

- LUKOIL

- SK Lubricants

- Sinopec Corporation

- China National Petroleum Corporation (CNPC)

- Petronas Lubricants International

- Phillips 66

- Indian Oil Corporation (SERVO)

- Kluber Lubrication (Freudenberg Group)

- Repsol S.A.

Frequently Asked Questions

The global Automotive Lubricant market is estimated at US$ 74.2 billion in 2026 and is projected to reach US$ 100.3 billion by 2033, growing at a CAGR of 4.4%.

Demand is driven by the expanding global vehicle fleet, tightening emission and fuel-efficiency regulations, increasing adoption of synthetic lubricants, and the emergence of EV-specific e-fluids.

Asia Pacific leads the market with around 42% consumption share, supported by large vehicle fleets and high automotive production in China, India, and ASEAN countries.

The biggest opportunity lies in EV-specific lubricants and thermal management fluids, which offer higher margins and rising demand with global EV adoption.

Major players include Shell plc, ExxonMobil Corporation, BP plc, TotalEnergies SE, Chevron Corporation, and Valvoline Inc., along with several regional lubricant producers.