- Executive Summary

- Global Automotive Glass Fiber Composites Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Automotive Glass Fiber Composites Market Outlook: Composite Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Composite Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- Market Attractiveness Analysis: Composite Type

- Global Automotive Glass Fiber Composites Market Outlook: Manufacturing Process

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Manufacturing Process, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- Market Attractiveness Analysis: Manufacturing Process

- Global Automotive Glass Fiber Composites Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- Market Attractiveness Analysis: Application

- Global Automotive Glass Fiber Composites Market Outlook: Vehicle Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Vehicle Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- Market Attractiveness Analysis: Vehicle Type

- Global Automotive Glass Fiber Composites Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- Europe Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- East Asia Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- South Asia & Oceania Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- Latin America Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- Middle East & Africa Automotive Glass Fiber Composites Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Composite Type, 2026-2033

- Glass Fiber

- Carbon Fiber

- Other

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Manufacturing Process, 2026-2033

- Compression Molding

- Injection Molding

- Resin Transfer Molding (RTM)

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Exterior

- Interior

- Powertrain & Chassis

- Battery Enclosures

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Vehicle Type, 2026-2033

- Electric

- ICE

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Owens Corning

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Johns Manville

- Solvay

- Orbia

- 3B Fiberglass

- SGL Carbon

- PPG Industries

- Jushi Group

- Saint-Gobain

- Chongqing Polycomp International Corporation

- Nippon Electric Glass Co., Ltd.

- AGY Holding Corp.

- Taishan Fiberglass Inc.

- Vetrotex

- LANXESS

- Hexion Inc.

- Teijin Limited

- Toray Industries, Inc.

- Owens Corning

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Glass Fiber Composites Market

Automotive Glass Fiber Composites Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Glass Fiber Composites Market by Composite Type (Glass Fiber, Carbon Fiber, Other), Manufacturing Process (Compression Molding, Injection Molding, Resin Transfer Molding (RTM), Others), Application (Exterior, Interior, Powertrain & Chassis, Battery Enclosures), Vehicle Type (Electric, ICE), by Regional Analysis, 2026 - 2033

Automotive Glass Fiber Composites Market Size and Trend Analysis

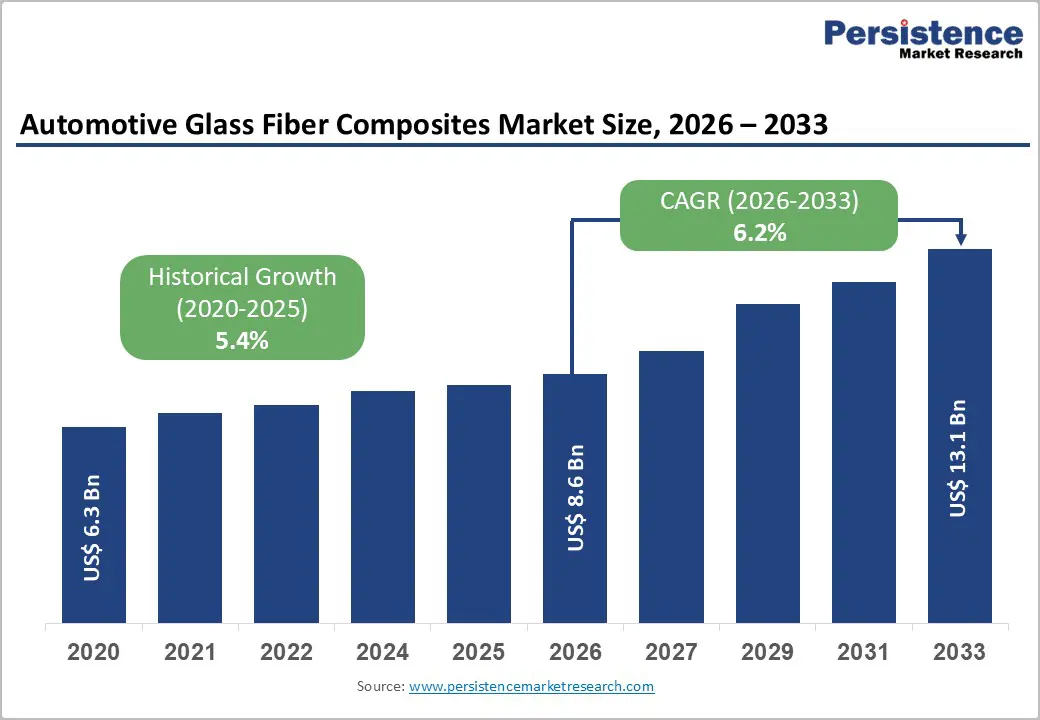

The global automotive glass fiber composites market size is expected to be valued at US$ 8.6 billion in 2026 and projected to reach US$ 13.1 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. The automotive glass fiber composites market is set for robust expansion, driven by the dual imperatives of vehicle lightweighting for fuel-efficiency compliance and the structural demands of electric-vehicle platform development.

Stringent emissions regulations, including the European Union’s CO2 fleet-average targets mandating 95 g/km for passenger cars, are compelling automakers to aggressively replace steel and aluminum with lighter composite materials. Simultaneously, the rapid global scaling of electric vehicle production is creating entirely new application categories, particularly structural battery enclosures and underbody protection panels, where glass fiber reinforced polymers offer a compelling combination of weight savings, electrical insulation, thermal resistance, and cost efficiency compared to metallic alternatives.

Key Industry Highlights:

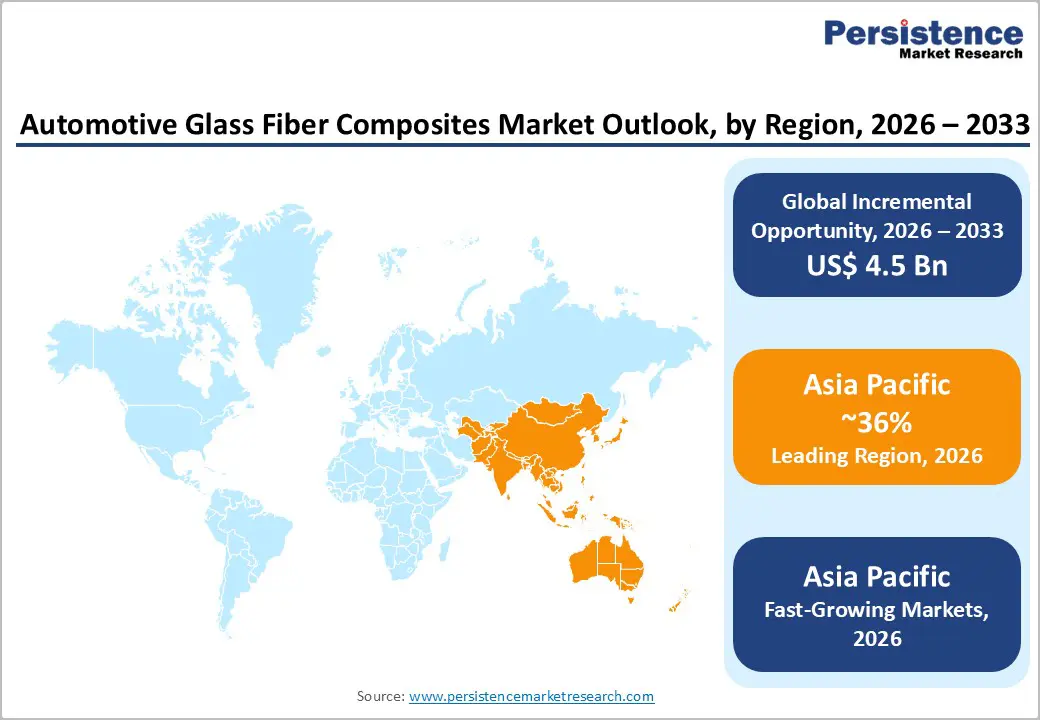

- Leading Region: Asia Pacific leads the global Automotive Glass Fiber Composites market with approximately ~36% revenue share in 2025, anchored by China’s position as the world’s largest vehicle and EV producer, supported by cost-competitive domestic glass fiber producers, including Jushi Group and Taishan Fiberglass Inc.

- Fastest Growing Region: Asia Pacific is also the fastest growing regional market over 2026–2033, propelled by China’s EV manufacturing scale-up, India’s PLI-backed automotive industrialization, and Japan’s thermoplastic composite technology development programs at leading OEMs, including Toyota and Honda.

- Dominant Segment: Glass Fiber composites dominate the Composite Type segment with approximately ~71% market share in 2025, driven by a cost-per-kilogram advantage of 5 to 10 times over carbon fiber, making GFRP the economically viable lightweighting material of choice for mainstream high-volume automotive body and structural applications.

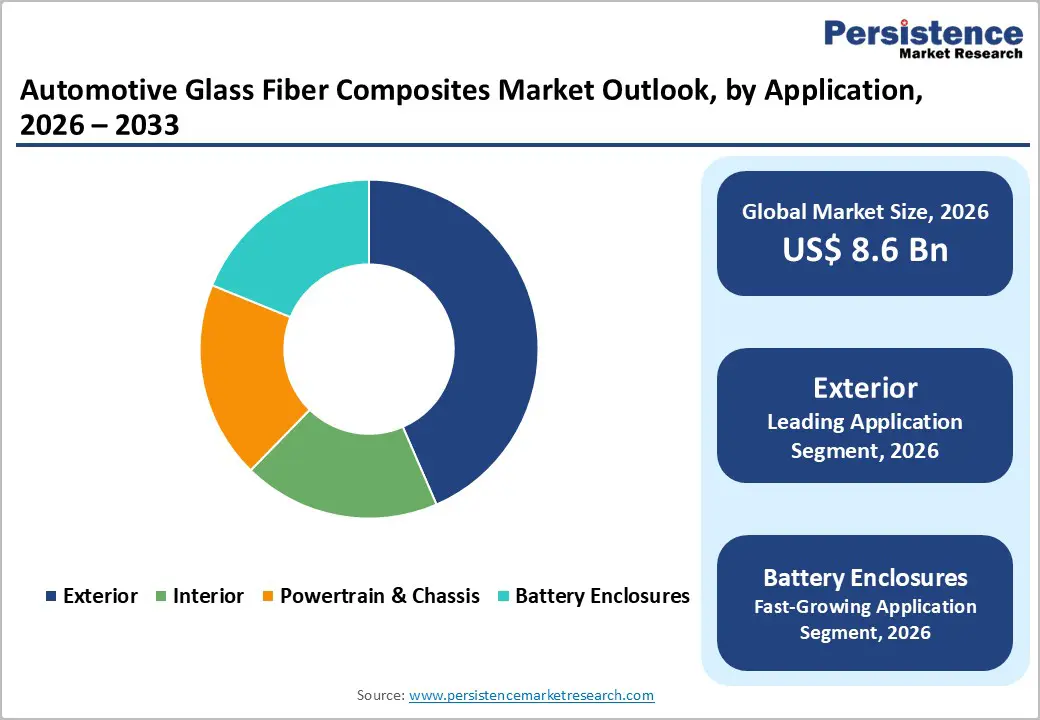

- Fastest Growing Segment: Battery Enclosures are the fastest growing application segment over 2026–2033, with global BEV fleet growth projected to exceed 250 million vehicles by 2030 per the IEA, each requiring GFRP battery enclosures offering structural rigidity, electrical insulation, and thermal resistance in a weight-optimized package.

- Key Opportunity: Thermoplastic GFRP development is the key market opportunity, as forthcoming EU End-of-Life Vehicles Directive recyclability mandates create compelling regulatory and commercial incentives for OEMs and suppliers to transition from thermoset to recyclable thermoplastic glass fiber composite systems across structural vehicle applications.

| Key Insights | Details |

|---|---|

|

Automotive Glass Fiber Composites Market Size (2026E) |

US$ 8.6 Billion |

|

Market Value Forecast (2033F) |

US$ 13.1 Billion |

|

Projected Growth CAGR (2026–2033) |

6.2% |

|

Historical Market Growth (2020–2025) |

5.4% |

Market Dynamics

Drivers - Stringent Vehicle Emission Regulations Accelerating Lightweighting Initiatives

Global regulatory tightening on vehicle greenhouse gas emissions is the single most powerful structural demand driver for automotive glass fiber composites. The European Union has legislated a 100% reduction in CO2 emissions from new passenger cars by 2035, effectively mandating the phase-out of combustion-only powertrains and driving automakers to maximize energy efficiency through every available means, including aggressive mass reduction. In the United States, the Environmental Protection Agency (EPA) finalized revised fuel economy and GHG emissions standards in 2024, targeting significant fleet efficiency improvements through the early 2030s. Every 100 kg of vehicle weight reduction translates to approximately 3–5% improvement in fuel economy according to the U.S. Department of Energy (DOE), providing a quantifiable engineering rationale for glass fiber reinforced plastic (GFRP) adoption in structural body panels, underbody cladding, and load floor systems across both ICE and EV vehicle architectures.

Electric Vehicle Production Surge Creating New Structural and Enclosure Applications

The global electric vehicle transition is generating an unprecedented wave of demand for glass fiber composites in application categories that barely existed a decade ago. Battery enclosures, which must simultaneously provide structural rigidity, impact resistance, electrical insulation, and thermal management properties, represent one of the most technically demanding and highest-volume emerging applications for automotive GFRP. The International Energy Agency (IEA) reported global EV sales of over 14 million units in 2023, a 35% year-on-year increase, and projected the global EV fleet to reach 250 million vehicles by 2030 under stated policy scenarios. Each battery electric vehicle (BEV) platform typically incorporates 30–60% more composite content by weight than comparable ICE vehicles, according to published benchmarking studies from the Society of Automotive Engineers (SAE International). This structural shift in vehicle architecture is creating durable, high-volume incremental demand for glass fiber composite materials and component suppliers.

Restraints - Recycling and End-of-Life Challenges for Thermoset Glass Fiber Composites

A significant barrier to the long-term growth of the automotive glass fiber composites market is the technical and regulatory challenge associated with end-of-life recycling of thermoset GFRP components. Unlike thermoplastic composites or metals, conventional thermoset resin systems, including epoxy and unsaturated polyester, cannot be remelted and reprocessed, making mechanical recycling the primary option and leading to significant degradation of fiber and resin properties. The European Union End-of-Life Vehicles (ELV) Directive, currently under revision, is expected to mandate higher recyclability and recycled content targets for vehicle components, creating compliance risks for automakers and tier suppliers that are heavily reliant on conventional thermoset GFRP. These regulatory and material constraints are dampening adoption rates in some body panel and structural applications where material circularity is a procurement criterion.

High Tooling and Process Investment Requirements

Advanced composite manufacturing processes, including Resin Transfer Molding (RTM) and high-pressure compression molding, require substantial capital investment in precision tooling, press infrastructure, and process-monitoring equipment, which can be prohibitive for smaller automotive tier suppliers. Premium-quality matched-die compression molds for high-volume automotive GFRP components can cost US$500,000 to US$2 million per tool set, and cycle-time optimization for high-volume automotive production remains an ongoing engineering challenge. The European Association of the Machine Tool Industries (CECIMO) notes that capital formation cycles in automotive component tooling typically span 18 to 36 months, creating significant lead-time risk as model-change cycles accelerate. This investment threshold limits the rate at which smaller fabricators can enter the advanced composite automotive supply chain.

Opportunity -Battery Enclosure Composites for Next-Generation EV Platforms

The battery enclosure application represents perhaps the most structurally significant and commercially promising growth opportunity in the automotive glass fiber composites market over the 2026–2033 forecast period. As battery technology evolves toward cell-to-pack and cell-to-body architectures, where the battery pack itself becomes a load-bearing structural element of the vehicle body, the material performance requirements for enclosures are intensifying. Glass fiber reinforced thermoplastics and hybrid GFRP systems offer unique combinations of specific strength, electrical insulation (critical for preventing galvanic corrosion and thermal runaway propagation), and design flexibility that competing materials struggle to match at equivalent cost. Volkswagen Group, BMW AG, and General Motors have each publicly announced composite-intensive roadmaps for next-generation battery platforms. With the IEA projecting the global BEV fleet to grow by over 200 million vehicles between 2024 and 2030, the compound demand for GFRP battery enclosure systems represents a multi-billion dollar incremental revenue opportunity for material suppliers and molding specialists.

Thermoplastic GFRP and Recyclable Composite Development for Circular Economy Compliance

The transition from thermoset to thermoplastic glass fiber composite systems offers a transformative opportunity for material innovators and processors positioned to serve the circular economy requirements that automotive OEMs increasingly face. Thermoplastic GFRP, using polyamide (PA), polypropylene (PP), or polyethylene terephthalate (PET) matrices reinforced with glass fiber, offers genuine recyclability through re-melting and reprocessing, enabling compliance with forthcoming ELV Directive recycled content mandates. Companies including Solvay, LANXESS, and Owens Corning are actively developing advanced thermoplastic composite tape, sheet, and overmolding systems targeting structural automotive applications. The European Commission’s Circular Economy Action Plan and the anticipated revision of the EU End-of-Life Vehicles Directive are creating a regulatory tailwind that will materially elevate the commercial attractiveness of recyclable thermoplastic GFRP in automotive structural and semi-structural applications over the forecast period.

Category-wise Analysis

Composite Type Insights

Glass Fiber Composites Lead the Composite Type Segment with ~71% Market Share in 2025

Glass fiber-reinforced composites dominate the automotive composites market by composite type, holding an estimated ~71% share of total market revenue in 2025. The commanding leadership of glass fiber over carbon fiber and other reinforcement types is fundamentally rooted in the former’s highly favorable cost-to-performance ratio for mainstream automotive applications. E-glass fiber, the most widely used grade in automotive GFRP, is manufactured at commodity scale by producers such as Owens Corning, Jushi Group, 3B Fiberglass, and Taishan Fiberglass Inc., enabling raw material pricing that is typically 5 to 10 times lower per kilogram than carbon fiber. For high-volume vehicle segments, including C-segment and D-segment passenger cars, SUVs, and light commercial vehicles, glass fiber composites deliver sufficient mechanical properties for body panels, structural underbody, and interior load floors while meeting stringent automotive cost-per-part targets.

Manufacturing Process Insights

Compression Molding Leads the Manufacturing Process Segment with ~38% Market Share in 2025

Compression molding is the dominant manufacturing process in the automotive glass fiber composites market, accounting for approximately ~38% of total processing volume in 2025. Its leadership reflects the process’s well-established compatibility with high-volume automotive production schedules. Advanced sheet molding compound (SMC) compression molding systems can achieve cycle times of under 60 seconds for complex, near-net-shape automotive body panel geometries, meeting the throughput requirements of mass-production vehicle assembly lines. Major automotive OEMs, including Stellantis, BMW AG, and General Motors, have industrialized SMC compression molding for exterior components, including hood inners, tailgates, and body side claddings. The process is also well-suited to integrating functional features such as ribs, inserts, and mounting bosses in a single molding step, reducing secondary assembly operations and system costs.

Application Insights

Exterior Application Leads the Application Segment with ~41% Market Share in 2025

The Exterior application segment holds the leading share of the automotive glass fiber composites market, representing approximately ~41% of total demand in 2025. Exterior body panels, including hoods, fenders, front-end modules, bumper systems, tailgates, and roof panels, represent the highest-volume application category for automotive GFRP, leveraging the material’s ability to deliver significant mass savings of 25 to 40% versus equivalent steel stampings while achieving class-A surface finish quality suitable for visible painted surfaces. The widespread adoption of GFRP in pickup truck bed liners, SUV tailgates, and commercial vehicle cab panels, exemplified by components on Ford F-Series, RAM 1500, and Mercedes-Benz Sprinter platforms, underscores the maturity and scale of exterior composite applications. Continuing platform rollouts and the growth of the composite-intensive electric SUV and crossover segments are expected to sustain the exterior segment's leadership through 2033.

Vehicle Type Analysis

ICE Vehicles Lead the Vehicle Type Segment with ~62% Market Share in 2025

Internal Combustion Engine (ICE) vehicles currently account for the leading share of automotive glass fiber composite demand, representing approximately ~62% of total market volume in 2025. Despite the rapid scaling of EV production globally, ICE vehicles, including hybrid electric vehicles (HEVs), continue to constitute the substantial majority of global light vehicle production and sales, with the International Organization of Motor Vehicle Manufacturers (OICA) reporting total vehicle production of approximately 93.5 million units in 2023, of which BEVs accounted for roughly 10%. Established GFRP applications in ICE vehicle exterior panels, underbody shields, engine covers, and intake manifolds represent a large, stable, and high-volume demand base. However, the EV segment is the fastest-growing vehicle type, with structural battery enclosures and new underbody composite systems driving a disproportionately high GFRP intensity per vehicle compared to equivalent ICE platforms.

Regional Insights

North America Automotive Glass Fiber Composites Market Trends and Insights

North America holds a leading position in the global automotive glass fiber composites market, accounting for an estimated ~29% of global revenue share in 2025. The United States is the primary driver, underpinned by its large light-vehicle production base, including the strategically important pickup truck and full-size SUV segments, which have historically adopted GFRP for load beds, tonneau covers, front-end modules, and large body panels at high penetration rates. The U.S. Department of Energy (DOE)’s Vehicle Technologies Office has invested consistently in composite lightweighting research through programs such as the Co-Optimization of Fuels and Engines (Co-Optima) initiative, and the multi-agency Lightweight Materials Consortium supports pre-competitive GFRP technology development for automotive applications.

The North American innovation ecosystem is further strengthened by the presence of global composite material leaders, including Owens Corning (headquartered in Toledo, Ohio) and Johns Manville, as well as a dense network of Tier 1 composite component suppliers. The Inflation Reduction Act (IRA) of 2022, by incentivizing domestic EV manufacturing and battery supply chain investment, is also indirectly accelerating GFRP adoption in battery enclosure and structural EV component manufacturing across the U.S. and Canada, creating a durable demand tailwind for the regional market through the forecast period.

Europe Automotive Glass Fiber Composites Market Trends and Insights

Europe represents the most technologically advanced and regulatory-driven market for automotive glass fiber composites globally, with Germany, France, Italy, and the United Kingdom collectively accounting for the dominant share of regional demand. Germany, home to BMW AG, Volkswagen Group, Mercedes-Benz Group AG, and Stellantis Europe, along with a globally competitive Tier 1 supplier ecosystem, is the epicenter of European automotive composite innovation. The EU’s 2035 zero-emission mandate for new passenger cars and the ongoing revision of the End-of-Life Vehicles (ELV) Directive are compelling German automakers and their supply chains to simultaneously maximize GFRP lightweight content and transition toward recyclable thermoplastic composite systems.

LANXESS, Solvay, and Saint-Gobain are among the European material leaders driving thermoplastic GFRP and hybrid composite development for structural automotive applications, with active collaboration programs with OEM engineering teams across Germany and France. The UK Automotive Council’s Composites Leadership Forum has identified glass fiber composites as a strategic material for the country’s automotive decarbonization roadmap. Spain’s growing EV assembly investments by Volkswagen Group (in Pamplona) and Stellantis (in Zaragoza) are expanding the Iberian composite component supply chain, while Italy’s specialist vehicle and motorsport sectors sustain demand for advanced composite forming technologies.

Asia Pacific Automotive Glass Fiber Composites Market Trends and Insights

Asia Pacific is both the largest and fastest-growing region for the automotive glass fiber composites market, driven by the world’s highest vehicle production volumes, rapidly scaling EV manufacturing ecosystems, and the presence of leading glass fiber raw material producers. China is the unambiguous regional powerhouse, the world’s largest automotive market, producing over 30 million vehicles in 2023 according to the China Association of Automobile Manufacturers (CAAM), and simultaneously the world’s leading EV producer with domestic EV sales of over 9 million units in 2023. Chinese EV manufacturers, including BYD, NIO, and Li Auto are rapidly adopting composite battery enclosure and underbody protection solutions, generating strong domestic demand for the products of glass fiber producers Jushi Group, Taishan Fiberglass Inc., and Chongqing Polycomp International Corporation (CPIC).

Japan remains a critical technology contributor to the region, with Nippon Electric Glass Co., Ltd. and major OEMs including Toyota Motor Corporation and Honda Motor Co. advancing thermoplastic GFRP and glass fiber-carbon fiber hybrid composite systems for next-generation vehicle architectures. India is emerging as a significant growth market, with the Production Linked Incentive (PLI) scheme for Advanced Chemistry Cell batteries and automotive manufacturing incentives catalyzing both EV platform development and composite component supply chain investments. The cost advantage of Asian glass fiber raw material production, where leading producers have achieved manufacturing cost structures significantly below Western counterparts, reinforces the region’s competitive dominance in global composite supply.

Competitive Landscape

The global automotive glass fiber composites market exhibits a two-tier competitive structure. At the upstream level, glass fiber production is moderately consolidated, with a limited number of large-scale multinational manufacturers controlling a significant share of global capacity. These players benefit from economies of scale, integrated melting and fiberizing operations, and strong bargaining power within automotive supply chains. Their strategic focus centers on advanced fiber formulations, proprietary sizing chemistries to improve resin compatibility, and continuous capacity expansion in high-growth automotive regions.

In contrast, the downstream compounding and component fabrication segment is highly fragmented, comprising numerous regional molders and composite processors serving OEM and Tier 1 suppliers. Competitive differentiation at this level emphasizes application engineering expertise, lightweight structural design capabilities, and cost-efficient processing technologies. Across the value chain, companies are increasingly prioritizing recyclable thermoplastic composite systems, regulatory-compliant material innovation, and collaborative co-engineering partnerships with automakers to support EV lightweighting programs and meet evolving sustainability mandates.

Key Developments:

- February 2026: AGY partnered with JPS Composite Materials LLC to begin North American production of the first low-CTE glass fiber fabric for advanced IC substrates, strengthening domestic semiconductor supply chains and enhancing performance in high-end packaging technologies.

- In September 2024: Hexcel Corporation announced the launch of its new lightweight HexForce 1K woven reinforcement fabric, leveraging proprietary 1K carbon fiber to produce high-strength, low-weight composite materials for industrial, automotive, aerospace, and defense applications.

- In June 2024: Navrattan Group announced plans to introduce a new high-efficiency electric bus built using advanced glass fibre composite technology, featuring reduced weight, improved efficiency, and lower maintenance costs.

Companies Covered in Automotive Glass Fiber Composites Market

- Owens Corning

- Johns Manville

- Solvay

- Orbia

- 3B Fiberglass

- SGL Carbon

- PPG Industries

- Jushi Group

- Saint-Gobain

- Chongqing Polycomp International Corporation (CPIC)

- Nippon Electric Glass Co., Ltd.

- AGY Holding Corp.

- Taishan Fiberglass Inc.

- Vetrotex

- LANXESS

- Hexion Inc.

- Teijin Limited

- Toray Industries, Inc.

Frequently Asked Questions

The global Automotive Glass Fiber Composites market is valued at US$ 8.6 billion in 2026 and is projected to reach US$ 13.1 billion by 2033 at a CAGR of 6.2%.

Demand is driven by tightening vehicle CO₂ regulations, EV production growth, and increasing use of lightweight GFRP in battery enclosures and structural components.

Asia Pacific leads with around 36% revenue share in 2025, supported by strong vehicle production and a robust glass fiber manufacturing base.

The key opportunity lies in recyclable thermoplastic GFRP systems aligned with stricter vehicle recyclability mandates and sustainability requirements.

Key players include Owens Corning, Jushi Group, LANXESS, Solvay, and Saint-Gobain, among others competing through advanced composite technologies and OEM partnerships.