- Automotive Components & Materials

- Automotive Air Intake Manifold Market

Automotive Air Intake Manifold Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Air Intake Manifold Market by Vehicle Type (Passenger Cars, Heavy Commercial Vehicles (HCV), Light Commercial Vehicles (LCV), Sports Car), Material (Aluminum, Magnesium, Plastic/Other Composites, Iron), Manifold Type (Single Plane, Dual Plane, EFI, Hi-RAM, Supercharger Intake), Distribution Channel (OEM, Aftermarket), and Regional Analysis for 2026 - 2033

Automotive Air Intake Manifold Market Size and Trend Analysis

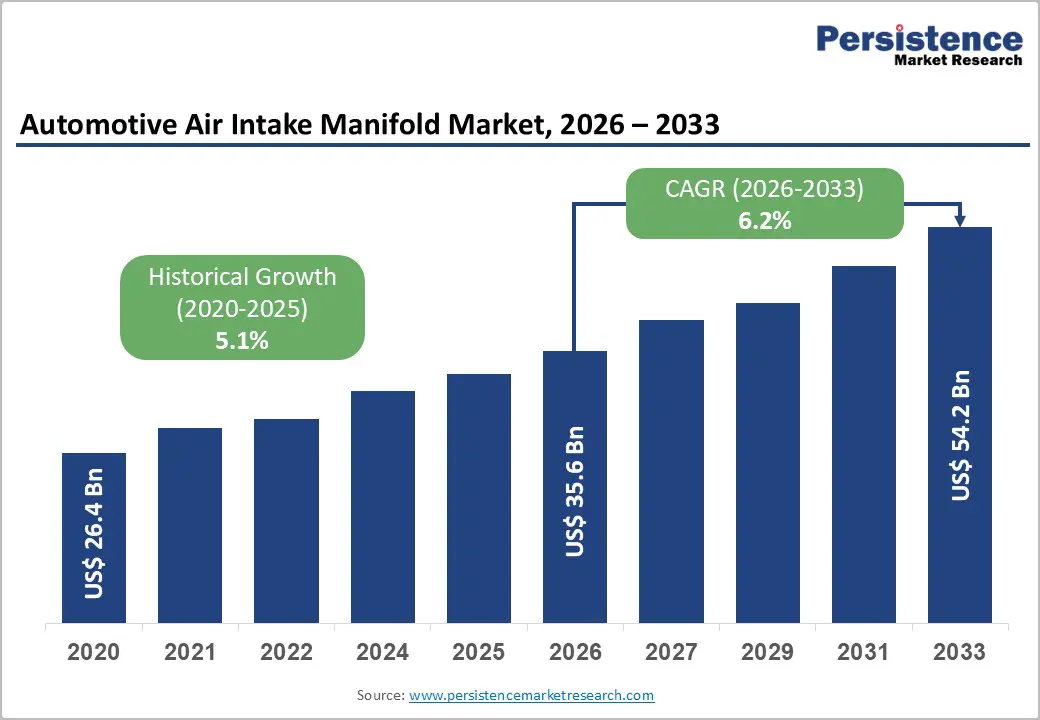

The global Automotive Air Intake Manifold market size is valued at US$ 35.6 billion in 2026 and is projected to reach US$ 54.2 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This robust growth trajectory is anchored by the continued dominance of internal combustion engine (ICE) vehicles globally, the intensifying push for lightweighting and fuel efficiency, and tightening emission regulatory frameworks across major automotive markets.

Stringent standards such as the U.S. EPA's Phase 3 Greenhouse Gas Emissions Standards for heavy-duty vehicles and the Euro 7 regulation in Europe are compelling manufacturers to develop more advanced, aerodynamically optimized, and lightweight intake manifold assemblies.

Key Highlights:

- Leading Region – North America leads the global automotive air intake manifold market with approximately 35% revenue share, driven by high vehicle production volumes, robust EPA emission regulation frameworks, and a mature high-performance aftermarket ecosystem across the U.S. and Mexican automotive hubs.

- Fastest Growing Region – Asia Pacific is the fastest-growing region, propelled by China's massive ICE and hybrid vehicle production, India's BS-VI compliance-driven upgrades, Japan's precision manufacturing capabilities, and ASEAN automotive sector expansion, driving consistent manifold procurement growth.

- Dominant Segment – Passenger Cars hold approximately 55% market share, supported by global production of over 70 million units annually, widespread adoption of turbocharged engines requiring advanced manifold assemblies, and growing hybrid vehicle demand, which sustains per-vehicle intake manifold content value.

- Fastest Growing Segment – The EFI manifold segment is the fastest-growing design type, driven by universal EFI adoption across new vehicle platforms, tightening Euro 7 and China 6 emission compliance, and OEM integration of variable geometry and sensor-embedded manifold technologies for advanced engine management.

- Key Opportunity – Purpose-designed air intake manifolds for hydrogen internal combustion engines represent a transformational growth opportunity, validated by MAHLE's MAN hTGX contract and Alpine's Alpenglow Hy6 hydrogen concept, as governments globally accelerate H2 infrastructure investment.

| Key Insights | Details |

|---|---|

|

Automotive Air Intake Manifold Market Size (2026E) |

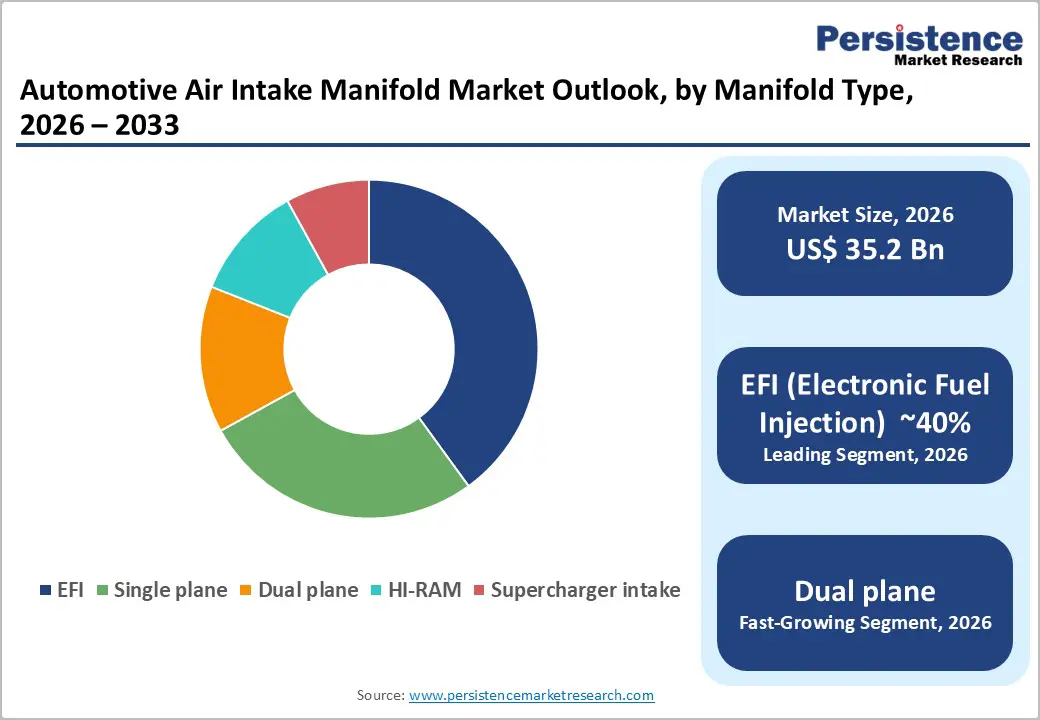

US$ 35.6 Billion |

|

Market Value Forecast (2033F) |

US$ 54.2 Billion |

|

Projected Growth CAGR (2026–2033) |

6.2% |

|

Historical Market Growth (2020–2025) |

5.1% |

DRO Analysis

Drivers - Stringent Emission Regulations Driving Advanced Manifold Development

Escalating global emission standards are among the most powerful demand catalysts for the automotive air intake manifold market. In March 2024, the U.S. Environmental Protection Agency (EPA) finalized its Phase 3 Greenhouse Gas Emissions Standards for heavy-duty vehicles, mandating CO2 reductions of up to 60% for vocational trucks and 40% for tractor trucks by model year 2032 compared to Phase 2 levels. In parallel, Europe's Euro 7 standard is imposing tighter limits on pollutant emissions from both light-duty and heavy-duty vehicles.

Air intake manifolds play a pivotal role in optimizing the air-fuel mixture for combustion, and compliance with these standards requires more precisely engineered manifold geometries, variable-length intake runners, and the integration of advanced flow management technologies. These regulatory pressures are compelling automotive OEMs and Tier-1 suppliers to invest significantly in next-generation manifold R&D.

Rising Demand for Lightweight Vehicles and Fuel Efficiency Improvements

The global automotive industry's sustained focus on lightweighting and fuel-economy improvements is driving consistent demand for advanced air intake manifold materials and designs. According to the U.S. Department of Energy, a 10% reduction in vehicle weight translates to a 6–8% improvement in fuel economy, making material substitution in components such as intake manifolds a strategic imperative for vehicle manufacturers.

The transition from cast iron and aluminum manifolds to advanced polymer composites and thermoplastics has enabled weight reductions of up to 30% per unit while maintaining structural integrity and thermal resistance. In July 2024, an air intake manifold made entirely from 100% recycled nylon won the Society of Plastics Engineers (SPE) Automotive Innovation Award in the Powertrain category, underscoring the convergence of sustainability and performance objectives driving innovation in this component segment.

Restraints - Structural Threat from Electric Vehicle Adoption

The accelerating global transition to battery-electric vehicles (BEVs) represents a structural headwind for the automotive air intake manifold market in the long term. Since fully electric powertrains do not require air intake manifolds, sustained growth in BEV penetration will progressively reduce the total addressable market for this component. The International Energy Agency (IEA) reported that global electric car sales surpassed 14 million units in 2023, with BEVs and plug-in hybrids collectively accounting for over 18% of total new car sales.

While hybrid vehicles continue to require intake manifold components, the trajectory of electrification in leading markets such as China, Europe, and the United States creates a medium- to long-term structural constraint on demand growth that manufacturers must proactively address through product diversification.

Raw Material Price Volatility and Supply Chain Disruptions

Significant volatility in raw material prices, including aluminum, magnesium, and engineering-grade polymers, continues to pose a margin challenge for air intake manifold manufacturers. Global supply chain disruptions stemming from geopolitical tensions, energy cost inflation, and constraints on raw material availability have intermittently elevated input costs for key manifold materials.

According to the London Metal Exchange (LME), aluminum prices have exhibited considerable volatility, with spot prices fluctuating by more than 30% over certain periods between 2021 and 2024. For Tier-1 suppliers operating under long-term fixed-price supply contracts with OEMs, such cost fluctuations directly compress profitability and constrain investment capacity for product innovation.

Opportunities - Hydrogen Internal Combustion Engine Vehicles Creating New Manifold Demand

The emergence of hydrogen-fueled internal combustion engine (H2-ICE) vehicles represents a compelling near- to medium-term growth opportunity for specialized air intake manifold manufacturers. Hydrogen-combustion engines require purpose-designed intake manifold systems capable of managing the unique combustion characteristics and pressure dynamics of hydrogen fuel delivery. In October 2024, Alpine unveiled the Alpenglow Hy6 concept, featuring a 6-cylinder hydrogen engine that requires a modified intake manifold to deliver an optimal hydrogen-air mixture.

In November 2024, MAHLE GmbH secured a contract from commercial vehicle manufacturer MAN Truck & Bus to supply components for the hydrogen engine of its MAN hTGX truck, signaling real-world commercial traction for hydrogen powertrain applications. As government investments in hydrogen infrastructure accelerate across Europe, Japan, and South Korea, demand for hydrogen-compatible intake manifold solutions is poised to create meaningful new revenue streams.

Aftermarket Segment Growth Fueled by Performance Tuning and Fleet Replacement

The automotive aftermarket segment offers a highly attractive growth opportunity for air intake manifold suppliers, driven by a combination of vehicle aging, fleet expansion in emerging markets, and the thriving performance tuning culture in North America and Europe. According to the Automotive Aftermarket Suppliers Association (AASA), the global automotive aftermarket was valued at over US$ 500 Bn and continues to expand as average vehicle age increases across major markets.

In June 2024, Wilson Manifold launched a billet aluminum intake manifold for the LT2 engine, targeting high-performance and forced-induction applications, illustrating sustained demand for performance-oriented aftermarket manifold products. With plug-and-play modular intake kits gaining traction in the enthusiast segment and fleet operators requiring periodic manifold replacement in aging commercial vehicle inventories, the aftermarket distribution channel is expected to grow at a premium to the overall market rate through 2033.

Category-wise Analysis

Vehicle Type Insights

Within the vehicle type category, the passenger cars segment holds a dominant position, accounting for approximately 55% of total market revenue. The primacy of passenger cars is driven by the sheer volume of global passenger vehicle production and the continued reliance on internal combustion and hybrid powertrains in this segment. According to the International Organization of Motor Vehicle Manufacturers (OICA), global passenger vehicle production exceeded 70 million units in 2023, with the vast majority incorporating gasoline or diesel intake manifold systems.

The widespread adoption of downsized turbocharged engines in passenger cars, which require specialized intake manifold designs to manage higher boost pressures and airflow dynamics, has further elevated the average per-vehicle content value of air intake manifold assemblies, reinforcing the segment's revenue leadership within the overall market.

Material Insights

Aluminum is the leading material segment in the automotive air intake manifold market, accounting for approximately 38% of overall revenue. Aluminum’s dominance is attributable to its superior strength-to-weight ratio, excellent thermal conductivity, corrosion resistance, and established manufacturability via die casting and sand-casting processes that are deeply integrated into automotive Tier-1 supply chains. Aluminum manifolds are widely preferred for performance-oriented passenger vehicles, sports cars, and commercial vehicle platforms where thermal management and structural rigidity under high-temperature engine conditions are critical.

While plastic and composite materials are gaining share in fuel-economy-focused passenger car applications due to cost and weight advantages, aluminum retains leadership in premium, commercial, and performance segments. Ongoing investments in advanced aluminum alloys with improved heat resistance are further extending the material's competitive relevance through the forecast period.

Manifold Type Insights

Among manifold design types, the EFI (Electronic Fuel Injection) segment holds the dominant market share, estimated at approximately 40%. The EFI manifold's leadership reflects the near-universal adoption of electronic fuel injection systems in modern gasoline and diesel passenger vehicles, which have largely displaced carbureted systems across virtually all new vehicle platforms globally. EFI manifolds are engineered to enable precise control of air distribution to individual cylinders, optimizing combustion efficiency, reducing emissions, and improving throttle response across a wide operating range.

The progressive tightening of global emission standards, including Euro 7, China 6, and BS-VI in India, is compelling manufacturers to adopt increasingly sophisticated EFI manifold designs integrated with intake air temperature sensors, tumble flap actuators, and variable geometry runners for comprehensive engine management compliance.

Distribution Channel Insights

The OEM (Original Equipment Manufacturer) channel represents the dominant distribution segment for automotive air intake manifolds, holding approximately 72% of the overall market share. OEM dominance reflects the structural nature of the automotive supply chain, wherein Tier-1 suppliers such as MAHLE GmbH, MANN+HUMMEL, and Aisin Seiki maintain long-term supply contracts with vehicle manufacturers to deliver intake manifold assemblies as part of integrated engine build programs.

The high degree of component customization, precision engineering specifications, and quality certification requirements associated with OEM supply effectively create high barriers to entry and sustain the channel's dominance. Automakers' increasing adoption of modular engine platforms spanning multiple vehicle lines also creates volume-scale advantages for established OEM manifold suppliers, enabling cost-competitive pricing and robust supply chain integration across vehicle model cycles.

Regional Analysis

North America Automotive Air Intake Manifold Market Insights

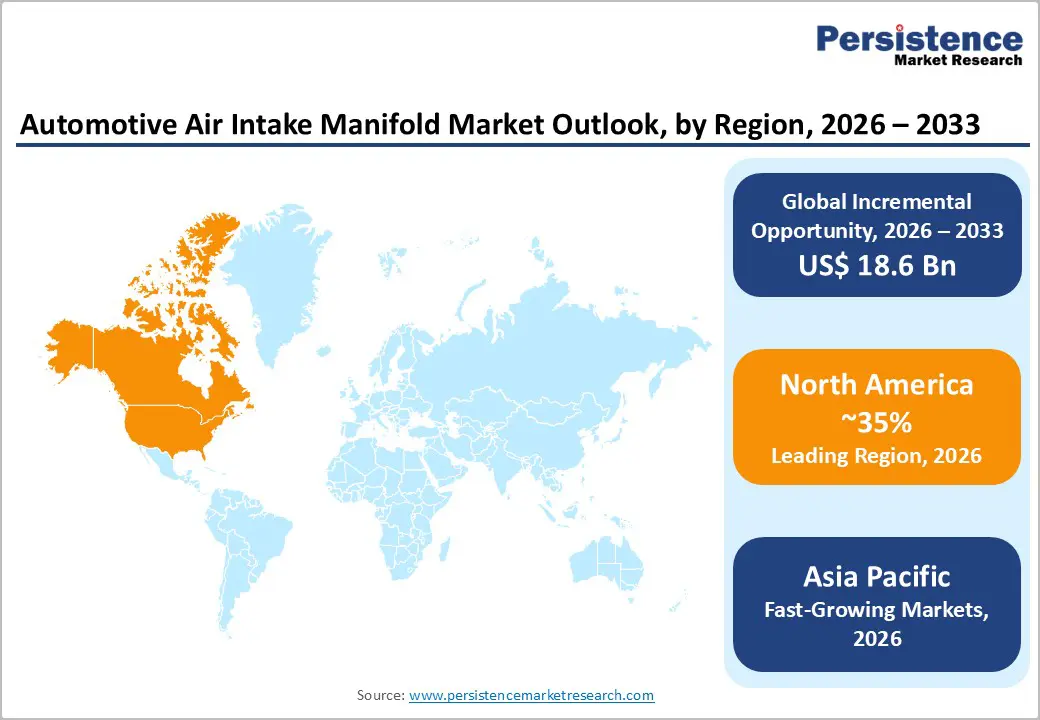

North America is the leading regional market for automotive air intake manifolds, holding approximately 35% of global revenue share. The region's market leadership is underpinned by its large and established automotive production base, particularly in the United States and Mexico, which together host significant manufacturing operations for major global OEMs, including General Motors, Ford Motor Company, Stellantis, and international transplants. The region's strong regulatory framework, anchored by the U.S. EPA's Phase 3 Greenhouse Gas Standards finalized in March 2024, is actively stimulating innovation in high-efficiency manifold designs for both light-duty and heavy-duty vehicle platforms.

The performance aftermarket segment is also exceptionally robust in North America, with the Specialty Equipment Market Association (SEMA) estimating the U.S. specialty automotive equipment market at over US$ 47 Bn annually. This includes significant demand for high-performance intake manifold products for V8 and turbocharged platforms from companies such as Edelbrock and Holley Performance.

Asia Pacific Automotive Air Intake Manifold Market Insights

Asia Pacific is the fastest-growing regional market for automotive air intake manifolds, driven by the region's enormous vehicle production volumes, rapidly expanding middle-class vehicle ownership, and significant government-backed automotive sector investments. China dominates the region as the world's single largest automotive market, with annual vehicle production exceeding 30 million units as of 2023 per OICA data. Despite the rapid uptake of battery electric vehicles in China, internal combustion engine and hybrid vehicles continue to account for most new vehicle production, sustaining robust demand for intake manifold systems.

India is emerging as one of the region's most dynamic growth markets, fueled by the rollout of the Bharat Stage VI (BS-VI) emission norms, record-high passenger vehicle sales, and the government's Production Linked Incentive (PLI) scheme for automotive components that is attracting foreign Tier-1 investments. ASEAN nations particularly Thailand, Indonesia, and Vietnam are benefiting from automotive manufacturing relocations and growing domestic vehicle demand, adding further momentum to regional intake manifold procurement activity.

Europe Automotive Air Intake Manifold Market Insights

Europe represents the second-largest regional market, with demand shaped by some of the world's most stringent automotive emission regulations and the region's legacy of precision engineering manufacturing. Germany leads European market activity, driven by the concentrated presence of premium automotive OEMs, including Volkswagen Group, BMW, and Mercedes-Benz, all of which are investing in advanced downsized turbocharged engine platforms requiring sophisticated intake manifold solutions. France, Spain, and the United Kingdom contribute meaningfully through vehicle assembly operations and Tier-1 supplier networks, including Sogefi Group and Magneti Marelli (now Marelli Holdings).

The imminent implementation of the Euro 7 emission standard is a decisive force in European market dynamics, compelling manufacturers to adopt more advanced EFI and variable-geometry intake manifold solutions across petrol and diesel platforms. In Q1 2025, Nexans announced a €100 million manufacturing investment in Germany, reflecting broader European industrial reinvestment in advanced automotive components.

Competitive Landscape

The global automotive air intake manifold market exhibits a moderately concentrated structure, with the top ten manufacturers collectively accounting for approximately 80% of total revenue. Leading Tier-1 suppliers, including MAHLE GmbH, MANN+HUMMEL, Aisin Seiki, Sogeti Group, and Toyota Boshoku Corporation, compete through proprietary material technologies, integrated engine management capabilities, global manufacturing footprints, and long-term OEM supply relationships.

Key competitive differentiators include precision polymer melding expertise, lightweighting innovation through composite and recycled-material designs, and the development of variable-geometry manifold platforms compatible with multiple engine families. Emerging business model trends include collaborative engineering with OEM engine development teams, additive manufacturing for rapid prototyping, and the integration of embedded air temperature sensors within manifold assemblies to support advanced engine control unit (ECU) functionality.

Key Market Developments

- In August 2025, Cummins' newly introduced intake manifold design gained attention due to its resemblance to advanced side-draft manifolds pioneered by Banks Power. Earlier, Banks Power had developed a side-draft intake system for the Cummins 5.9L engine, enhancing airflow efficiency and delivering significant horsepower improvements, including applications in record-setting high-performance trucks.

- June 2025, MAHLE GmbH entered a partnership with TecMotive GmbH to expand its workshop equipment service network in Germany and Austria, doubling service capacity and strengthening its Tier-1 component support infrastructure across European automotive markets.

Companies Covered in Automotive Air Intake Manifold Market

- Aisin Seiki

- BorgWarner

- Dana Incorporated

- Donaldson Company

- Lear Corporation

- Magneti Marelli

- MAHLE GmbH

- MANN+HUMMEL

- Sogefi Group

- Toyota Boshoku Corporation

Frequently Asked Questions

The global Automotive Air Intake Manifold market is valued at US$ 35.6 Bn in 2026 and is projected to reach US$ 54.2 Bn by 2033, at a forecast CAGR of 6.2%.

Key growth drivers include tightening global emission standards such as the U.S. EPA's Phase 3 Greenhouse Gas Standards and Euro 7, rising demand for lightweight and fuel-efficient vehicles, and the widespread adoption of turbocharged and downsized engine platforms in both passenger and commercial vehicles that require advanced intake manifold assemblies.

The OEM (Original Equipment Manufacturer) channel dominates with approximately 72% market share, supported by long-term supply contracts between Tier-1 manifold suppliers and vehicle manufacturers, high customization requirements, and the integration of intake manifold assemblies into modular engine build programs across global automotive production platforms.

North America leads the market with approximately 35% revenue share, underpinned by high-volume vehicle production in the U.S. and Mexico, robust EPA emission regulation activity, active Tier-1 supplier networks, and a mature high-performance automotive aftermarket ecosystem that sustains diverse intake manifold demand across vehicle segments.

The leading companies include MAHLE GmbH, MANN+HUMMEL GmbH, Aisin Seiki Co., Ltd., Toyota Boshoku Corporation, Sogefi Group, Magneti Marelli S.p.A., BorgWarner Inc., Röchling Automotive, Novares Group, and Keihin Corporation.