- Executive Summary

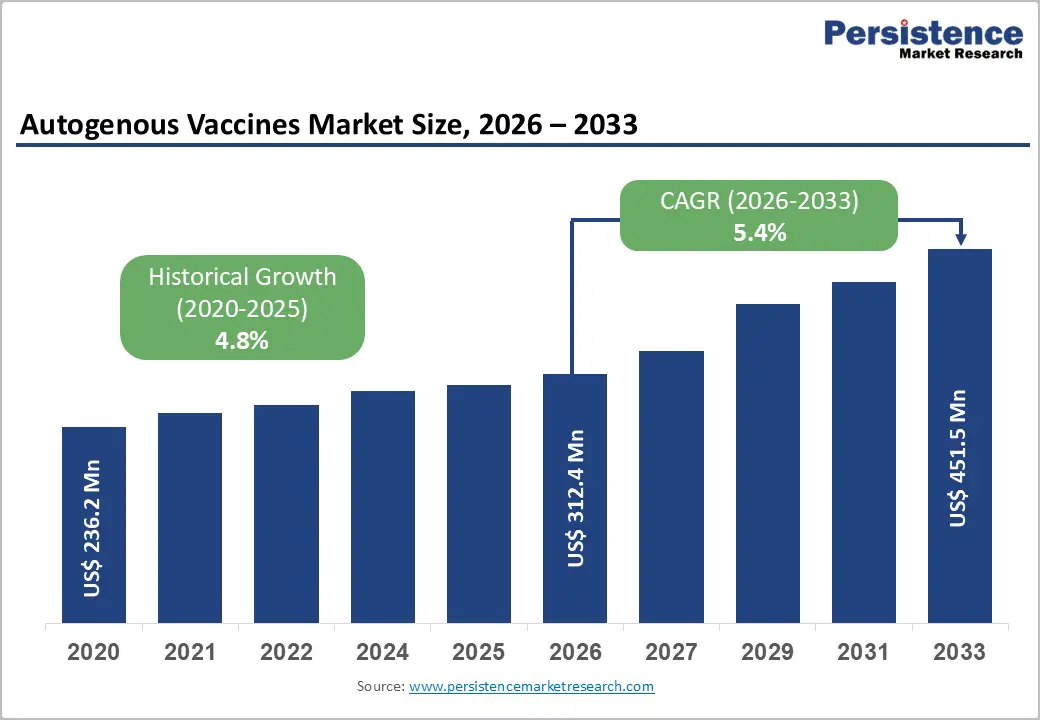

- Global Autogenous Vaccines Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Healthcare Expenditure

- Other Macro-economic Factors

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Disease Epidemiology

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Price Trend Analysis, 2025

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Autogenous Vaccines Market Outlook: Strain Type

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Strain Type, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- Market Attractiveness Analysis: Strain Type

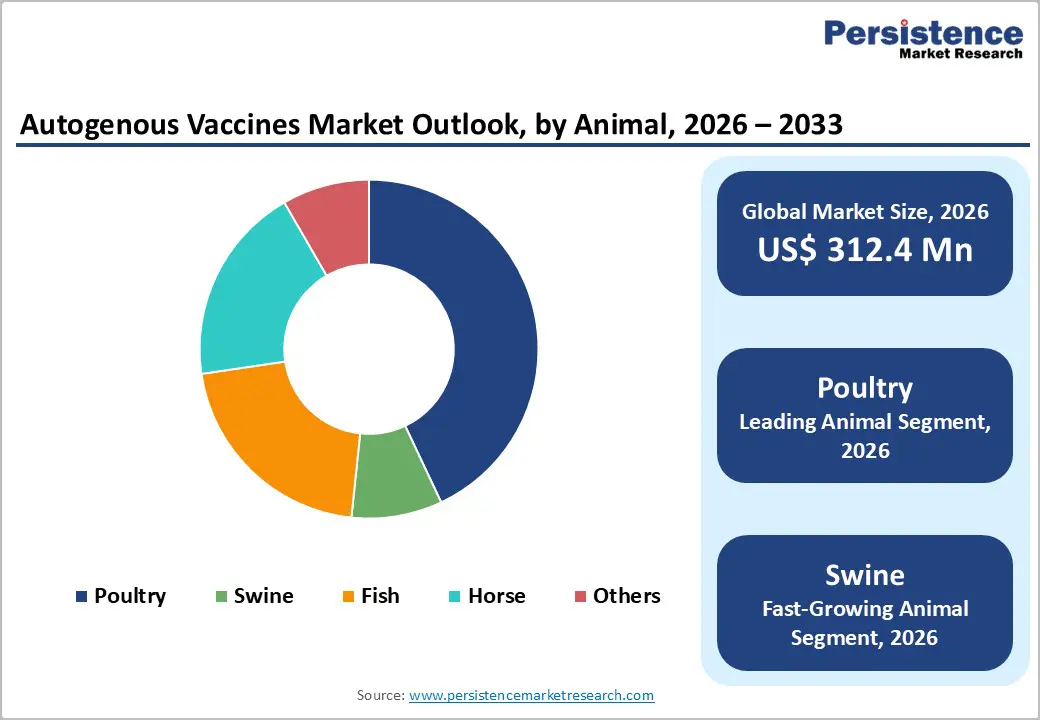

- Global Autogenous Vaccines Market Outlook: Animal

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Animal, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- Market Attractiveness Analysis: Animal

- Global Autogenous Vaccines Market Outlook: End Use

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by End Use, 2020-2025

- Current Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- Market Attractiveness Analysis: End Use

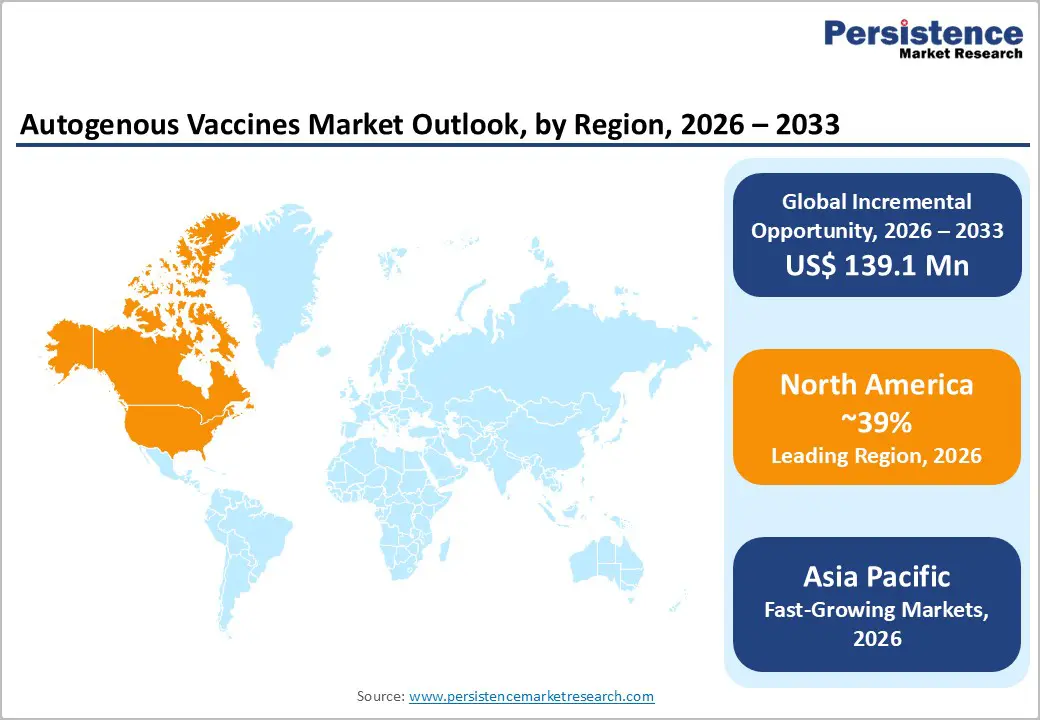

- Global Autogenous Vaccines Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis by Region, 2020-2025

- Current Market Size (US$ Mn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- North America Market Size (US$ Mn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- North America Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- North America Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- Europe Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Europe Market Size (US$ Mn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- Europe Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- Europe Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- East Asia Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- East Asia Market Size (US$ Mn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- East Asia Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- East Asia Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- South Asia & Oceania Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- South Asia & Oceania Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- South Asia & Oceania Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- Latin America Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Latin America Market Size (US$ Mn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- Latin America Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- Latin America Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- Middle East & Africa Autogenous Vaccines Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Mn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Mn) Forecast, by Strain Type, 2026-2033

- Bacterial Strain

- Virus Strain

- Middle East & Africa Market Size (US$ Mn) Forecast, by Animal, 2026-2033

- Poultry

- Swine

- Fish

- Horse

- Others

- Middle East & Africa Market Size (US$ Mn) Forecast, by End Use, 2026-2033

- Veterinary Research Institutes

- Livestock Farming Companies

- Veterinary Clinics and Hospitals

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Ceva

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- HIPRA

- Vaxxinova

- Phibro Animal Health Corporation

- Boehringer Ingelheim Animal Health USA Inc.

- Elanco Animal Health

- Bimeda® Biologicals

- AniCon Labor GmbH (SAN Group Biotech Germany GmbH)

- INVAC International GmbH

- AgriLabs (Huvepharma, Inc.)

- Cambridge Technologies

- Barramundi Asia Pte Ltd. (UVAXX Asia)

- Lohmann Breeders

- IDT Biologika

- Esco Micro Pte. Ltd.

- ARKO Laboratories

- Hygieia Biological Laboratories

- Calier

- ACE Laboratory Services (Apiam Animal Health)

- Dopharma International B.V.

- Others

- Ceva

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Animal Health

- Autogenous Vaccines Market

Autogenous Vaccines Market Size, Share, and Growth Forecast 2026 – 2033

Autogenous Vaccines Market by Strain type (Bacterial Strain, Virus Strain), Animal (Poultry, Swine, Fish, Horse, Others), End-use (Veterinary Research Institutes, Livestock Farming Companies, Veterinary Clinics & Hospitals) and Regional Analysis for 2026 - 2033

Key Industry Highlights:

- North America dominates the autogenous vaccines market, supported by large poultry and swine industries, advanced veterinary diagnostic capabilities, and well-established regulatory systems that allow controlled use of herd-specific vaccines for complex disease management.

- Asia Pacific is anticipated to be the fastest-growing region, driven by rapid expansion of livestock and aquaculture sectors across China, India, Japan, and ASEAN nations, along with rising adoption of advanced biosecurity practices and customized vaccination programs.

- By animal type, poultry represents the largest segment, accounting for around 43% market share in 2025, due to dense farming operations, short production cycles, and frequent demand for flock-specific vaccines to control respiratory and gastrointestinal diseases.

- Swine autogenous vaccines are projected to record the highest growth, fueled by changing respiratory and reproductive disease patterns, the high economic burden of herd-level outbreaks, and producers’ increasing emphasis on reducing antibiotic usage through precision immunization.

- Integration of advanced diagnostics, genomic sequencing, and data analytics with vaccine manufacturing presents a major opportunity, enabling faster response times, improved vaccine effectiveness, and stronger long-term relationships between veterinary biologics suppliers and livestock producers.

| Report Attribute | Details |

|---|---|

|

Autogenous Vaccines Market Size (2026E) |

US$ 312.4 Mn |

|

Market Value Forecast (2033F) |

US$ 451.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

Market Dynamics

Drivers - Limitations of Commercial Vaccines Drive Demand for Tailored Autogenous Solutions in Animal Health

Commercial vaccines, while essential in animal disease prevention, present certain limitations that drive the demand for autogenous vaccines. As outlined in the 2023 HealthforAnimals report, many animal diseases continue to challenge veterinary medicine, with traditional vaccines often failing to offer timely or effective protection against rapidly evolving pathogens.

Most commercial vaccines are based on classical platforms, which, although reliable, lack the flexibility required for fast response to emerging or localized disease threats. They are generally not designed to target specific pathogen strains found within individual herds or regions, limiting their utility during localized outbreaks.

Autogenous vaccines provide a highly targeted solution, using pathogens isolated from the affected animals to create a customized immunization. This precision approach proves invaluable when commercial options are unavailable or inadequate. In December 2024, over 6 million U.S. poultry received an experimental autogenous vaccine for avian metapneumovirus (aMPV) type B developed by Merck Animal Health and Cambridge Technologies demonstrating its value in emergency disease control. This growing reliance on autogenous vaccines highlights their critical role in enabling rapid, localized disease control.

Restraints - Scientific gaps and regulatory hurdles limit the scalability and timely deployment of autogenous vaccines

The limited understanding of veterinary disease epidemiology, especially for region-specific and emerging pathogens is a key factor restraining the global autogenous vaccines market. Rapid genetic mutations, inadequate surveillance, and complex pathogen diversity hinder accurate identification of vaccine targets and slow the development of effective, herd-specific formulations. These challenges are exacerbated by weak collaboration between research institutions and vaccine manufacturers, poor insights into immune responses, and the absence of robust data-sharing systems.

Additionally, stringent regulatory requirements significantly impact the speed and cost of vaccine development. For example, under USDA APHIS Memorandum 800.69, autogenous vaccines must meet rigorous standards such as pathogen isolation, sterility testing, and inactivation validation, which restrict scalability and delay deployment. Their use is often limited to specific flocks or herds, with strict timeframes and mandatory retesting.

These regulatory and scientific constraints collectively limit the market’s ability to respond swiftly and effectively to emerging animal health threats. These multifaceted challenges underscore the need for stronger research frameworks, streamlined regulations, and enhanced industry collaboration to fully realize the potential of autogenous vaccines in global animal health.

Opportunity - Technological innovations open new avenues in autogenous vaccines

Technological advancements present a significant opportunity for the autogenous vaccines market, enabling more efficient and tailored solutions for animal health. Innovations in diagnostic technologies, vaccine formulation, and production processes have enhanced the speed and accuracy of autogenous vaccine development. These advancements help meet the rising demand for customized vaccines, especially in scenarios where commercial vaccines are not effective or unavailable.

A notable example is Vaxxinova’s SRP® (Siderophore Receptor Protein) technology, which represents a breakthrough in bacterial vaccine development. Unlike traditional vaccines, SRP® technology targets iron receptors on the surface of bacteria, which are critical for bacterial survival. By neutralizing these receptors, SRP® vaccines help induce robust immunity in animals without the use of whole bacterial cells. This technology offers a safer and more effective vaccination strategy, particularly against complex bacterial infections in livestock.

Such advancements not only improve the safety and efficacy of autogenous vaccines but also support quicker vaccine production in response to emerging diseases. The integration of novel technologies like SRP® lead to more predictable outcomes, reduce the risk of adverse reactions, and enable a more strategic approach to disease management in animal husbandry.

Category-wise Analysis

Strain Type Insights

The bacterial strain segment is projected to hold a revenue share of nearly 78% in 2025 within the global autogenous vaccines market.

Autogenous vaccines, also referred to as autovaccines, are formulated using bacterial or viral strains isolated directly from specific herds or farms, enabling highly targeted immunity against localized infections. These vaccines serve as vital alternatives when licensed or commercial options are unavailable or ineffective for specific pathogens.

The growing incidence of zoonotic disease outbreaks many of which are linked to multidrug-resistant bacterial strains in livestock has increased the urgency for effective non-antibiotic interventions. As antimicrobial resistance continues to rise, both regulatory authorities and livestock producers are prioritizing preventative strategies that reduce reliance on antibiotics. This shift is driving heightened demand for customized bacterial autogenous vaccines, reinforcing their role as a proactive and sustainable solution for disease management in modern animal health programs.

Animal Insights

The poultry segment is expected to dominate the animal category in 2025, accounting for nearly 42.5% of the global autogenous vaccines market, driven largely by the scale and intensification of commercial poultry farming worldwide. High stocking densities, short production cycles, and continuous exposure to evolving pathogens make poultry operations particularly vulnerable to infectious disease outbreaks, creating strong demand for farm-specific immunization strategies. Frequent occurrences of avian influenza, Newcastle disease, infectious bronchitis, and bacterial infections have heightened reliance on customized vaccines to rapidly control localized strains that may not be adequately covered by conventional commercial products. In 2023, the U.S. Department of Agriculture’s Animal and Plant Health Inspection Service confirmed outbreaks of Highly Pathogenic Avian Influenza in both commercial and backyard flocks, reportedly affecting more than 378.5 million egg-laying chickens, underscoring the scale of biosecurity threats facing the industry. Rising regulatory pressure to curb antibiotic use, combined with growing emphasis on preventive herd health management and surveillance-driven vaccination programs, is further accelerating adoption of autogenous vaccines in poultry, positioning the segment as the cornerstone of market growth over the forecast period.

Regional Insights and Trends

North America Autogenous Vaccines Market Trends

North America currently leads the global autogenous vaccines market, accounting for a significant share of total revenue, supported by advanced veterinary healthcare infrastructure, large-scale livestock operations, and proactive regulatory frameworks that enable rapid development and deployment of tailored vaccine solutions. The United States is at the forefront of this regional dominance, driven by intensive poultry, swine, and cattle farming systems that frequently face localized pathogen challenges requiring customized immunization approaches. Robust disease surveillance programs, widespread use of cutting-edge diagnostics, and strong investments in animal health research further underpin adoption of autogenous vaccines across livestock and companion animal sectors.

In the U.S., stringent oversight by the USDA’s Center for Veterinary Biologics provides a structured pathway for conditional approvals and emergency use of herd-specific vaccines, exemplified by recent conditional clearance for a bird flu vaccine in poultry, which highlights the regulatory support for innovative solutions in response to emerging threats. Farmer preference for precision health management and growing pressure to reduce antibiotic usage are also accelerating demand for autogenous formulations tailored to specific farm-level strains. Canada contributes to regional growth through expanding veterinary services and rising awareness of customized vaccines in both livestock and pet care settings. Strategic collaborations between biotechnology firms, veterinary clinics, and diagnostic laboratories are expected to further enhance product portfolios and market penetration, solidifying North America’s leadership position through the forecast period.

Europe Autogenous Vaccines Market Trends

Europe is estimated to lead the global market, accounting for nearly one-third of the total share in 2025, driven by a strong regulatory framework, evolving legislation, and proactive industry initiatives. The region's diverse legal landscape, as seen in countries such as Germany and the UK, highlights both challenges and opportunities for autogenous vaccine manufacturers.

The UK autogenous vaccines market benefits from advanced veterinary services, precision livestock farming, and growing farmer awareness around herd-specific health management. Notably, Mowi Scotland's 35% reduction in overall biomass mortality across all seawater farms in 2024, aided by autogenous vaccines from Ridgeway Biologicals, underscores their growing impact in aquaculture and livestock health, supporting sustainable disease management across diverse animal production sectors.

Germany autogenous vaccines market is fuelled by its strong veterinary infrastructure, strict antimicrobial resistance regulations, and early adoption of innovative solutions. The launch of the Dopharma-Ripac autogenous vaccine production facility in Potsdam in February 2025, exemplifies this growth, supported by active research collaborations and increasing farmer awareness of targeted, sustainable animal disease prevention.

Combined with rapid response capabilities during outbreaks and supportive legislation, Europe is well-positioned as a key global player in the autogenous vaccines sector.

Asia Pacific Autogenous Vaccines Market Trends

The Asia Pacific region is emerging as the fastest-growing market for autogenous vaccines, driven by rapid expansion of livestock, poultry, and aquaculture production and increasing demand for precision disease management solutions. Rising consumption of animal protein and intensifying farming practices in countries such as China, India, Japan, and Southeast Asian nations are increasing vulnerability to localized disease outbreaks, making customized vaccines an essential tool for herd-specific immunity and improved productivity. Frequent outbreaks of diseases like avian influenza, African swine fever, and other bacterial and viral infections underscore limitations of traditional commercial vaccines and accelerate adoption of tailored immunization strategies in intensive animal production systems.

Regional growth is further supported by expanding veterinary healthcare infrastructure, increased awareness among producers about biosecurity and antimicrobial resistance, and collaborations between livestock companies and diagnostic laboratories for rapid pathogen identification and vaccine development. In aquaculture, where Asia Pacific accounts for over 80% of global production, disease pressure from pathogens in high-density fish and shrimp farms is driving demand for autogenous vaccines to protect valuable stocks and reduce losses. Government initiatives promoting animal health programs, investment in diagnostic facilities, and growing pet ownership in urban areas also contribute to market expansion. As a result, the Asia Pacific autogenous vaccine market is expected to maintain robust momentum through the forecast period.

Competitive Landscape

The competitive landscape of the autogenous vaccines market is moderately consolidated, featuring a mix of established global veterinary biologics firms and specialized regional manufacturers. Market rivalry is shaped by innovation in tailored vaccine solutions, strategic partnerships with diagnostic labs and veterinary networks, and efforts to expand geographic reach to high-growth regions. Companies compete not just on product efficacy, but also on turnaround time for custom formulations, integration of advanced technologies in vaccine development, and compliance with evolving regulatory requirements. Collaborative initiatives that link pathogen surveillance data with rapid vaccine production are increasingly important competitive differentiators. Additionally, firms with strong distribution channels and regional expertise maintain advantage in addressing localized disease outbreaks, while niche players focus on agility and bespoke services for smaller livestock clusters and companion animals.

Key Industry Developments:

- In April 2025, HIPRA launched ICHTIOVAC® ERM, its first inactivated vaccine for Atlantic salmon against Yersiniosis, which was designed to be administered by immersion to combat the disease during the freshwater phase.

- In February 2025, Elanco Animal Health Incorporated entered into an agreement with Medgene to utilize its innovative vaccine platform technology for commercializing a highly pathogenic avian influenza (HPAI) vaccine for dairy cattle.

- In November 2024, Ceva Animal Health announced the construction of a 7,000 m² vaccine manufacturing facility in Hungary with operations commencing by 2026 end. The plant is aimed to produce over 8 billion doses of fermentation-based multicomponent inactivated vaccines for animals annually.

Companies Covered in Autogenous Vaccines Market

- Ceva

- HIPRA

- Vaxxinova

- Phibro Animal Health Corporation

- Boehringer Ingelheim Animal Health USA Inc.

- Elanco Animal Health

- Bimeda® Biologicals

- AniCon Labor GmbH (SAN Group Biotech Germany GmbH)

- INVAC International GmbH

- AgriLabs (Huvepharma, Inc.)

- Cambridge Technologies

- Barramundi Asia Pte Ltd. (UVAXX Asia)

- Lohmann Breeders

- IDT Biologika

- Merck Animal Health

- Zoetis Inc.

Frequently Asked Questions

The global autogenous vaccines market size is projected to reach approximately US$ 312.4 million in 2026, with further growth expected to about US$ 451.5 million by 2033 at a 5.4% CAGR.

Demand is primarily driven by rising livestock disease burdens, the need for herd-specific immunization where commercial vaccines are inadequate, regulatory support for customized veterinary biologics, and global efforts to reduce antimicrobial use through preventive vaccination.

North America leads the autogenous vaccines market, supported by intensive poultry and swine industries, strong diagnostic and veterinary infrastructure, and a mature regulatory framework governing autogenous veterinary biologics.

A major opportunity lies in fast-growing swine and intensive poultry segments, where integrating rapid pathogen sequencing, flexible manufacturing, and data-driven herd health services can deliver highly tailored, high-value vaccination solutions.

Prominent players include Ceva, HIPRA, Vaxxinova, Phibro Animal Health Corporation, Boehringer Ingelheim Animal Health USA Inc., Elanco Animal Health, Bimeda® Biologicals, AniCon Labor GmbH, Cambridge Technologies, IDT Biologika, and regionally active firms such as Barramundi Asia Pte Ltd. (UVAXX Asia).