- Sporting Goods & Equipment

- Aqua Gym Equipment Market

Aqua Gym Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Aqua Gym Equipment Market by Equipment Type (Aqua Bikes, Aqua Treadmills, Aqua Dumbbells and Barbells, Aqua Step Platforms, Balance & Core Training Equipment, Others), End-user (Fitness Centers and Health Clubs, Rehabilitation & Physiotherapy Centers, Hotels & Resorts, Sports Training Facilities, Residential Users), Distribution Channel (Online, Specialty Store, Institutional Sales), and Regional Analysis, 2026 - 2033

Aqua Gym Equipment Market Size and Trend Analysis

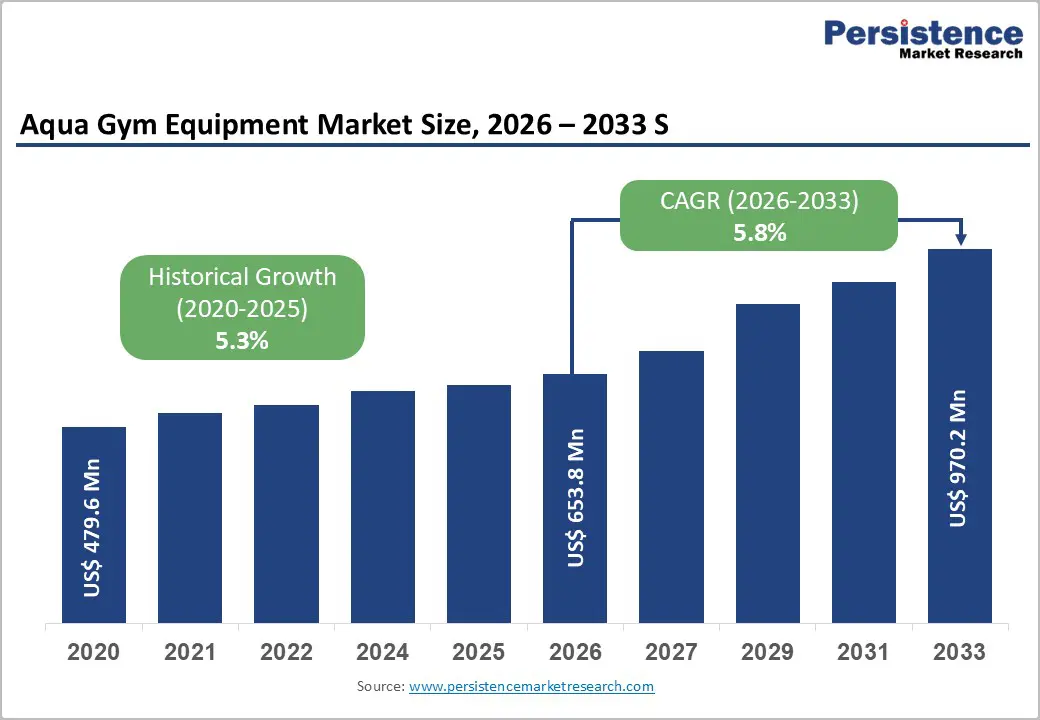

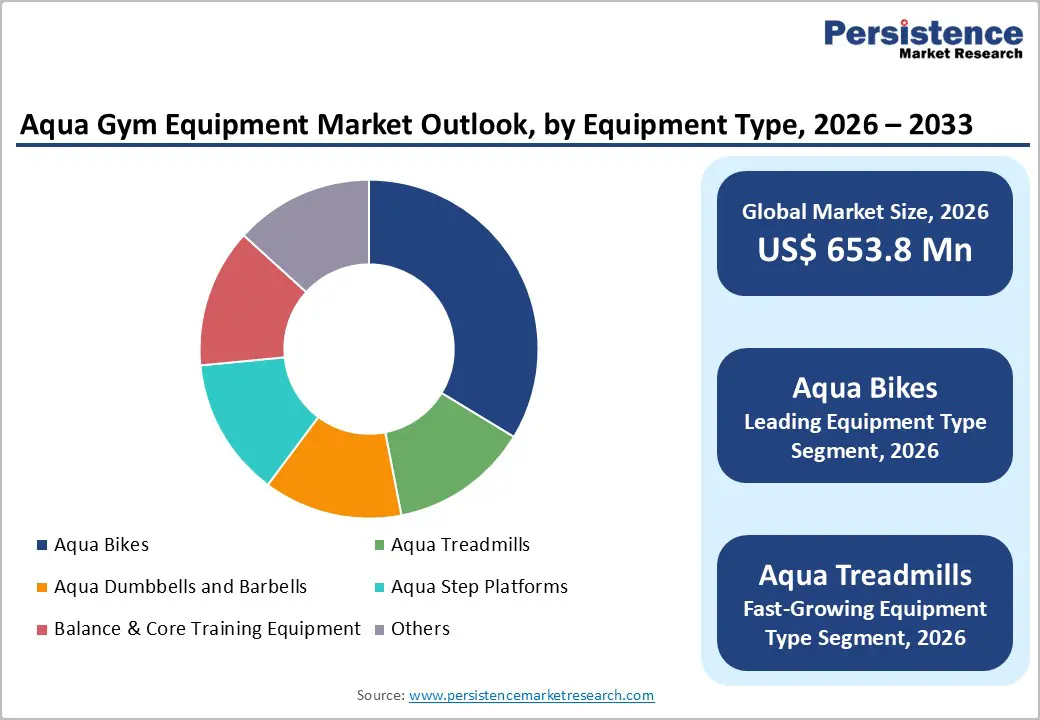

The global aqua gym equipment market size is expected to be valued at US$ 653.8 million in 2026 and projected to reach US$ 970.2 million by 2033, growing at a CAGR of 5.8% between 2026 and 2033. The market is experiencing sustained growth, driven by a powerful convergence of an aging global population seeking low-impact fitness solutions, rising incidence of chronic musculoskeletal conditions, and expanding health and wellness infrastructure across gyms, rehabilitation centers, and luxury resorts. The World Health Organization (WHO) reports that insufficient physical activity is one of the leading risk factors for global mortality, affecting over 1.4 billion adults worldwide, compelling healthcare providers and fitness operators to invest in low-impact alternatives such as aqua fitness.

The growing integration of smart technologies, including IoT-enabled resistance systems, waterproof wearables, and digital performance tracking platforms, is further elevating product differentiation and driving demand from fitness centers, rehabilitation clinics, hotels & resorts, and increasingly tech-savvy home users.

Key Industry Highlights:

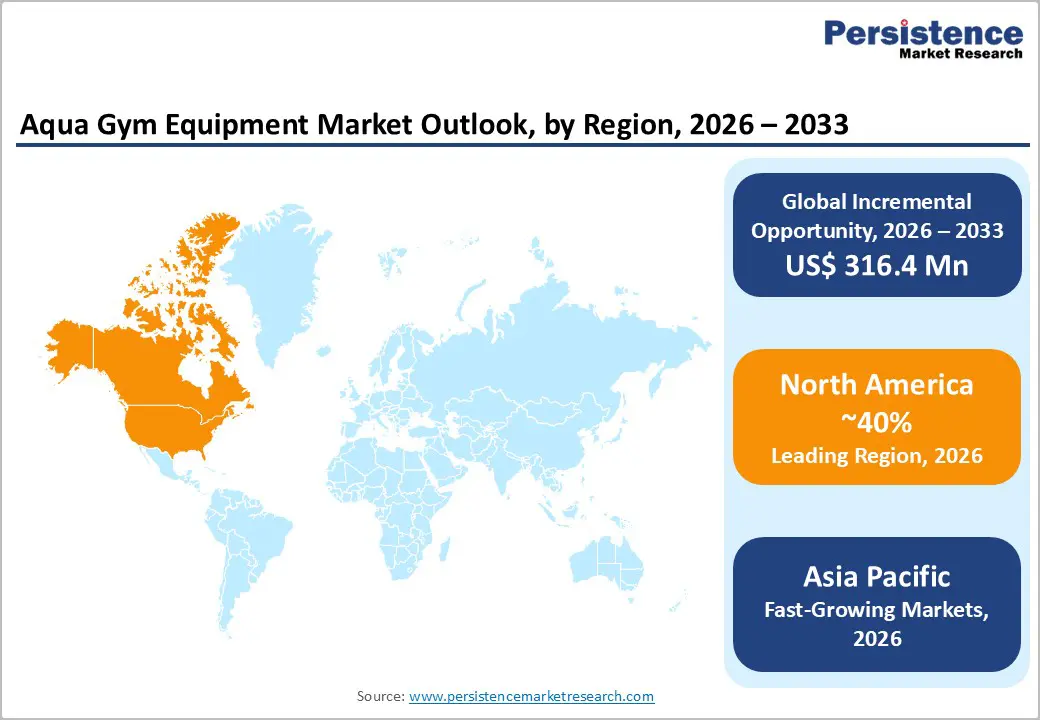

- Leading Region: North America leads the global Aqua Gym Equipment market with approximately 40% market share in 2025, anchored by the U.S.'s highly developed fitness infrastructure, clinical hydrotherapy adoption across professional sports and rehabilitation, and over 200,000 health clubs globally served by leading suppliers such as HydroWorx International.

- Fastest Growing Region: Asia Pacific is the fastest-growing region in the Aqua Gym Equipment market, driven by China's fitness center expansion, Japan's rapidly aging 29%+ elderly population, India's clinical hydrotherapy adoption (Sri Ramakrishna Hospital, 2023), and ASEAN luxury wellness resort proliferation, fueling sustained equipment procurement.

- Dominant Segment: Aqua Bikes are the dominant equipment type, holding approximately 35% market share in 2025, supported by the global popularity of aqua cycling group fitness classes, cardiovascular health benefits, joint-friendly accessibility, and strong OEM commercial product portfolios from BECO Beermann GmbH & Hydrorider across Europe and North America.

- Fastest Growing Distribution Channel: Online distribution channels are the fastest-growing segment, expanding at approximately 7.5% CAGR through 2033, driven by e-commerce growth for consumer aqua fitness accessories (aqua dumbbells, flotation belts, resistance bands) and direct-to-consumer digital marketing by specialty aqua equipment brands targeting home fitness users.

- Key Opportunity: Smart IoT-enabled aqua gym equipment integration represents a transformative market opportunity, validated by £500k investment in UK aqua rehab technology (November 2024), with connected aqua fitness platforms commanding significant price premiums and unlocking subscription-based coaching and analytics revenue streams through 2033.

| Key Insights | Details |

|---|---|

|

Aqua Gym Equipment Market Size (2026E) |

US$ 653.8 Million |

|

Market Value Forecast (2033F) |

US$ 970.2 Million |

|

Projected Growth CAGR (2026–2033) |

5.8% |

|

Historical Market Growth (2020–2025) |

5.3% |

Market Dynamics

Drivers - Rising Prevalence of Chronic Disease and an Aging Global Population Accelerating Aquatic Rehabilitation Demand

The growing global burden of chronic diseases and musculoskeletal disorders is a decisive driver of the Aqua Gym Equipment market. According to the WHO, musculoskeletal conditions affect over 1.71 billion people globally, with osteoarthritis, lower back pain, and rheumatoid arthritis representing the most prevalent conditions. Aquatic exercise is clinically validated for these populations, water buoyancy reduces body weight by up to 90% when submerged to the neck, enabling effective therapeutic movement without joint stress. The United Nations projects that the global population aged 65 and above will double to approximately 1.6 billion by 2050, creating a structurally expanding base of users for rehabilitation-oriented aqua gym equipment. Rehabilitation & physiotherapy centers across North America, Europe, and the Asia Pacific are increasingly adopting hydrotherapy pools equipped with aqua treadmills, resistance jets, and buoyancy-assisted training devices, as studies published in the Journal of Aging and Physical Activity confirm that aquatic exercise significantly improves functional capacity and reduces fall risk in older adults.

Expanding Health Club Infrastructure and Growing Popularity of Aqua Fitness Classes

The global fitness industry's post-pandemic recovery and ongoing expansion of aqua fitness programming across health clubs are providing powerful tailwinds for equipment demand. According to the International Health, Racquet & Sportsclub Association (IHRSA), there are over 200,000 health clubs globally with an estimated 184 million members, and a growing proportion of these facilities are integrating dedicated aqua fitness pools and programs. Aqua cycling, water aerobics, aqua HIIT, and aqua yoga are among the fastest-growing group fitness formats, according to the American College of Sports Medicine (ACSM) in its annual fitness trends surveys. The CDC reports that only 24.2% of U.S. adults meet combined aerobic and muscle-strengthening physical activity guidelines, representing a substantial untapped market for fitness solution providers. Hotels and luxury wellness resorts are also investing in aqua gym equipment as a differentiating amenity, with segment-specific demand growing particularly across the Middle East, Europe, and Asia Pacific wellness tourism corridors.

Restraints - High Equipment Cost and Requirement for Dedicated Aquatic Infrastructure

The adoption of premium aqua gym equipment, particularly underwater treadmills, resistance jets, and aqua bikes, requires significant upfront investment. High-end units from providers such as HydroWorx International, Inc. can cost between US$ 20,000 and US$ 100,000+, placing commercial-grade aqua fitness equipment beyond the reach of smaller fitness centers, community pools, and individual consumers. Additionally, installing such equipment requires specialized aquatic pools or therapy tanks, adding construction and retrofitting costs that can amount to hundreds of thousands of dollars, limiting adoption to well-capitalized fitness operators and institutional healthcare facilities.

Maintenance Complexity and Regulatory Compliance Challenges in Aquatic Environments

Aqua gym equipment operates in chemically demanding aquatic environments with constant exposure to chlorinated water, humidity, and mechanical stress from buoyancy forces. Maintenance requirements are substantially higher than for land-based fitness equipment, requiring corrosion-resistant materials, frequent inspection protocols, and specialized servicing expertise. Ensuring compliance with international safety standards for water-based exercise equipment, including those set by ASTM International and European EN standards, adds to the regulatory burden for manufacturers and imposes certification costs that can disproportionately affect smaller market entrants, limiting product variety in price-sensitive market segments.

Opportunities - Smart and IoT-Enabled Aqua Fitness Equipment Creating a New Premium Product Category

The integration of smart technologies into aqua gym equipment represents the most transformative growth opportunity for market participants between 2026 and 2033. Consumer demand for data-driven fitness experiences, driven by the broader wearables and digital health revolution, is driving investment in IoT-enabled aqua bikes, smart resistance systems, and waterproof fitness trackers that provide real-time performance analytics, personalized coaching, and progress monitoring. In November 2024, a Bristol-based startup secured £500,000 in funding to develop what it claims is the world's first aqua rehabilitation technology with integrated clinical validation capabilities. In August 2023, AquaTrainer launched a new line of customizable aqua fitness solutions for commercial gyms and homes. The global digital fitness equipment market is growing at a CAGR exceeding 8%, creating adjacent demand for digitally integrated aqua fitness products. Manufacturers that successfully deliver connected aqua gym platforms, compatible with mobile apps, wearable devices, and virtual training environments, are positioned to command significant price premiums and build recurring revenue through subscription-based coaching content and performance analytics services.

Rehabilitation and Physiotherapy Centers as a High-Growth Institutional End User

Rehabilitation and physiotherapy centers represent one of the most compelling institutional growth opportunities for aqua gym equipment suppliers, driven by clinical evidence validating hydrotherapy's effectiveness for post-surgical recovery, neurological rehabilitation, and chronic pain management. HydroWorx International, Inc.'s underwater treadmill systems are already widely deployed in NFL, NBA, MLB, and NHL team rehabilitation facilities, and the clinical adoption model is increasingly being replicated across hospital-based outpatient rehabilitation programs. In 2023, Sri Ramakrishna Hospital in India introduced its first aquatic treadmill for rehabilitation, reflecting growing clinical adoption in Asian markets. The American Physical Therapy Association (APTA) estimates that over 50 million Americans receive physical therapy annually, with aquatic therapy protocols increasingly integrated into standard care pathways for joint replacement, neurological recovery, and pediatric rehabilitation. This expanding clinical validation base, combined with reimbursement approvals for hydrotherapy in key markets including the U.S., Germany, and Japan, positions the rehabilitation segment as the fastest-growing end user through 2033.

Category-wise Analysis

Equipment Type Insights

Aqua Bikes are the leading equipment type in the Aqua Gym Equipment market, commanding approximately 35% of total market share in 2025. Their dominance is anchored in versatility, accessibility for users across all fitness levels, and proven cardiovascular benefits in a zero-impact aquatic environment. Aqua bikes are among the most popular formats for group fitness classes, and aqua cycling sessions are now offered across thousands of health clubs globally, with the format gaining mainstream momentum, particularly in France, Germany, Spain, and the United States. Cardiovascular aqua gym equipment broadly (including aqua bikes) held approximately 60% of the product segment in 2024, reflecting the dominance of cardio-focused aquatic training. BECO Beermann GmbH & Co. KG and Hydrorider are leading European manufacturers of commercial-grade aqua bikes. Aqua Treadmills are the fastest-growing equipment type, with expanding adoption in clinical and athletic performance driving a CAGR exceeding 6.5% through 2033.

End-user Insights

Fitness Centers and Health Clubs represent the leading end-user segment in the Aqua Gym Equipment market, accounting for approximately 38% of total market share in 2025. The segment's dominance is driven by the global proliferation of health club memberships, exceeding 184 million worldwide, per IHRSA, and the competitive differentiation premium that aqua fitness programs provide for member acquisition and retention. Fitness center operators are actively investing in aqua gym equipment to offer diverse programming, including aqua cycling, water aerobics, aqua HIIT, and hydrotherapy-adjacent wellness services. The ACSM consistently identifies aquatic exercise as a top fitness trend for mature adults, reinforcing institutional procurement priorities. Rehabilitation & Physiotherapy Centers are the fastest-growing end-user segment, with clinical adoption of aquatic therapy protocols accelerating across hospital systems, sports medicine clinics, and outpatient physiotherapy practices globally, projected to grow at above 7% CAGR through 2033.

Distribution Channel Insights

Specialty Stores are the leading distribution channel in the Aqua Gym Equipment market, capturing approximately 49% of the total market share in 2025. Specialty stores, encompassing dedicated aquatic fitness equipment retailers, sports goods specialists, and physiotherapy supply distributors, maintain their leadership by offering personalized consultation, in-person product demonstrations, expert guidance on equipment selection, and post-purchase installation and servicing support. These value-added services are particularly important for institutional buyers, such as fitness centers, rehabilitation clinics, and hotels, that procure high-value equipment, including aqua bikes and underwater treadmills. Sprint Aquatics and Texas Recreation Corporation leverage specialty retail and institutional distribution channels to serve these commercial buyers. The Online channel is the fastest-growing distribution segment, expanding at a CAGR of approximately 7.5% through 2033, driven by growing e-commerce penetration for residential and lighter-weight aqua fitness accessories, including aqua dumbbells, barbells, flotation belts, and resistance bands.

Regional Insights

North America Aqua Gym Equipment Market Trends and Insights

North America leads the global Aqua Gym Equipment market with approximately 40% market share in 2025, driven by a highly developed fitness infrastructure, strong health and wellness culture, high per-capita healthcare expenditure, and a rapidly aging population with growing demand for therapeutic aquatic solutions. The U.S. accounts for the majority of regional demand, with the CDC noting that only 24.2% of adults meet combined aerobic and muscle-strengthening physical activity guidelines, underscoring broad public health need for accessible fitness formats such as aqua exercise. The U.S. hosts thousands of aquatic therapy clinics, public pools, YMCAs, and resort spas actively equipped with aqua fitness gear. HydroWorx International, Inc. serves professional sports teams across the NFL, NBA, and NHL with its underwater treadmill systems, while AquaJogger and HYDRO-FIT, Inc. maintain strong consumer and institutional positions.

In December 2024, The Amenity Collective, North America's leader in full-service facilities management across the fitness, aquatics, and recreation industries, announced the acquisition of Advantage Sport & Fitness Inc., creating North America's largest fitness equipment distributor and servicer in partnership with LIVunLtd. This consolidation strengthens the commercial aqua fitness equipment supply chain across the region. Regulatory initiatives such as the Americans with Disabilities Act (ADA) requirements for accessible pool facilities and growing Medicare reimbursement recognition of aquatic physical therapy are further institutionalizing aqua gym equipment procurement across healthcare and public sector facilities in North America.

Europe Aqua Gym Equipment Market Trends and Insights

Europe is the second-largest regional market for aqua gym equipment, with strong demand anchored in a mature aquatic fitness culture, an aging population, and well-developed rehabilitation infrastructure. France is particularly notable as a hotbed for aqua cycling, a fitness format popularized by the Waterflex brand, and a key market for specialty aqua fitness studios that are proliferating across major cities. Germany's health-conscious consumer base and rising smartphone-connected wellness behavior are fueling demand for smart aqua gym equipment. BECO Beermann GmbH & Co. KG's 2023 launch of an innovative aqua treadmill with adjustable water resistance exemplifies European OEM innovation leadership. In Spain, the growing wellness tourism and spa resort sector is driving premium aqua equipment procurement.

In 2023, Speedo International Ltd. collaborated with Intersport Sello and the Finnish Swimming Association to expand its Nordic market presence, demonstrating the broader European trend of cross-sector aquatic fitness collaboration. In February 2025, Waterland Private Equity partnered with WellNess to drive the expansion of France's top premium fitness club chain, indicating strong institutional investor confidence in European aqua fitness infrastructure growth. The UK is also witnessing growth, with the NHS increasingly supporting hydrotherapy for musculoskeletal conditions and with approximately 20 million adults classified as physically inactive.

Asia Pacific Aqua Gym Equipment Market Trends and Insights

Asia Pacific is the fastest-growing region with the projected positive CAGR between 2026 and 2033, propelled by rising health consciousness, expanding middle-class disposable incomes, government-backed wellness initiatives, and a growing aquatic sports and rehabilitation sector. China, the world's second-largest economy by GDP, is seeing rapid expansion of commercial fitness centers and hotel wellness facilities, with aqua fitness programs gaining traction in Tier 1 and Tier 2 cities driven by government health initiatives and the National Fitness Program. Japan, one of the world's most rapidly aging societies, with over 29% of its population aged 65+, represents a natural and structurally large market for therapeutic aqua gym equipment in rehabilitation and senior wellness facilities.

In 2023, Sri Ramakrishna Hospital in India introduced the country's first clinical aquatic treadmill for rehabilitation, signaling the beginning of systematic hydrotherapy equipment adoption in Indian healthcare. India's Ayushman Bharat health infrastructure expansion is further incentivizing investment in therapeutic equipment across hospital networks. The ASEAN region, particularly Thailand, Singapore, and Australia, is also emerging as a significant market, with luxury resort aqua fitness facilities and growing physiotherapy center networks driving consistent equipment procurement. Australia's New Parramatta Aquatic Centre, inaugurated in 2023, exemplifies the region's commitment to premium aquatic fitness infrastructure.

Competitive Landscape

The global Aqua Gym Equipment market exhibits a moderately fragmented structure, with numerous specialized manufacturers operating across different equipment categories such as aquatic bikes, treadmills, and resistance accessories. The absence of a dominant global supplier allows both established aquatic fitness brands and smaller niche manufacturers to compete effectively. Market participants typically focus on specific customer segments including rehabilitation centers, fitness clubs, sports training facilities, and wellness resorts.

Competitive strategies in the industry increasingly emphasize product differentiation through ergonomic design, corrosion-resistant materials, and equipment optimized for underwater resistance training. Companies are also strengthening partnerships with physiotherapy clinics, rehabilitation facilities, and aquatic fitness centers to expand institutional adoption. Customization of equipment for commercial facilities as well as compact solutions for residential pools is becoming an important strategy. In addition, manufacturers are exploring the integration of smart technologies such as connected resistance systems, digital training platforms, and performance tracking features. Investments in sustainable materials, improved durability, and user-friendly designs for elderly and rehabilitation patients are also shaping innovation and long-term market competitiveness.

Key Developments

- February, 2026: Apa Wellness unveiled a modular “water-native” smart aquatic training system designed to transform standard swimming pools into intelligent gyms for rehabilitation and fitness, integrating sensors, AI, and app connectivity to track and guide aquatic workouts.

- February, 2025: Waterland Private Equity partnered with WellNess to drive the expansion of France's leading premium fitness club chain, signaling strong investor confidence in European aqua fitness infrastructure growth and specialty equipment demand.

Companies Covered in Aqua Gym Equipment Market

- Aqua Lung International

- WaterGym LLC

- Speedo International Ltd.

- Theraquatics

- HydroWorx International, Inc.

- BECO Beermann GmbH & Co. KG

- Acquapole S.A.S.

- N-Fox Company

- AquaJogger

- Texas Recreation Corporation

- Sprint Aquatics

- Aqua Creek Products

- HYDRO-FIT, Inc.

- Aqualogix Fitness

- Aqua Sphere

- Hydrorider International

- AquaTrainer

- Waterflex SAS

Frequently Asked Questions

The global Aqua Gym Equipment market is estimated to reach US$ 653.8 million in 2026, driven by increasing demand from fitness centers, rehabilitation clinics, and hospitality facilities.

Key demand drivers include rising aging populations, growing prevalence of musculoskeletal disorders, expanding health club infrastructure, and increasing adoption of aquatic therapy and fitness programs.

North America leads the Aqua Gym Equipment market, supported by strong aquatic fitness infrastructure, widespread hydrotherapy adoption, and growing use in rehabilitation and sports training facilities.

A key growth opportunity lies in smart IoT-enabled aqua fitness equipment and increasing adoption of aquatic therapy in rehabilitation and physiotherapy centers.

Key players include HydroWorx International, BECO Beermann GmbH & Co. KG, Sprint Aquatics, Aqua Creek Products, AquaJogger, Speedo International Ltd., Aqualogix Fitness, HYDRO-FIT Inc., Acquapole S.A.S., and Aqua Sphere.