- Pharmaceuticals

- Acquired Orphan Blood Disease Market

Acquired Orphan Blood Disease Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Acquired Orphan Blood Disease Market by Treatment (Drug Class - Antineoplastic Drugs, Transfusion or Exchange; Bone Marrow Transplant), Disease Type, Distribution Channel, and Regional Analysis, from 2026 - 2033

Acquired Orphan Blood Disease Market Share and Trends Analysis

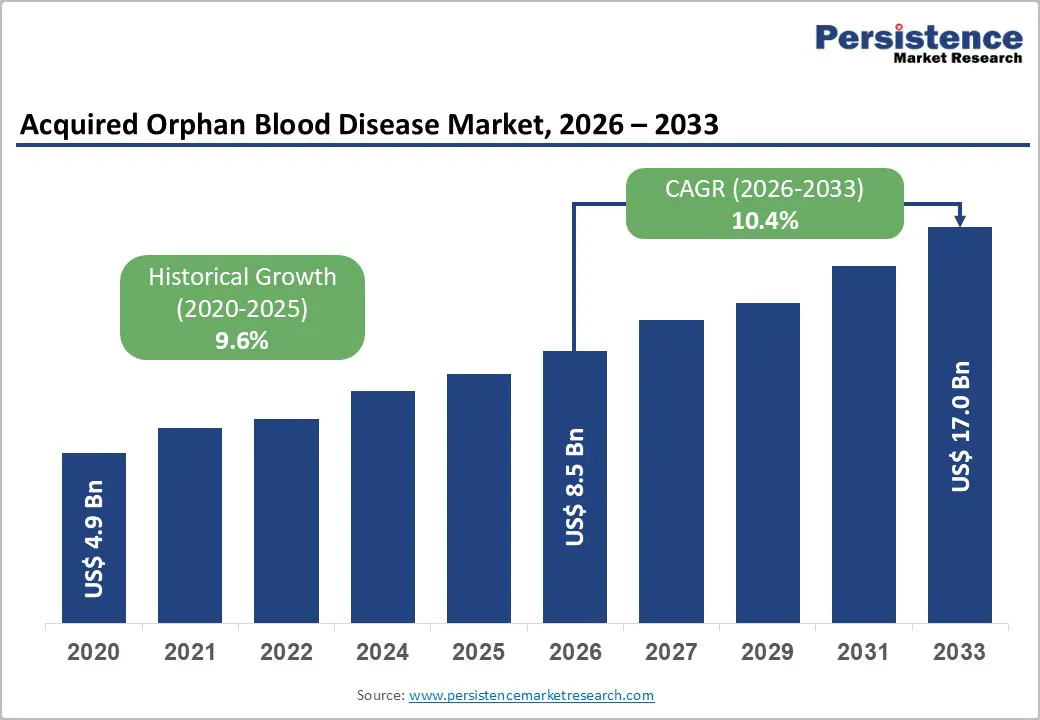

The global acquired orphan blood disease market size is likely to be valued at US$ 8.5 billion in 2026 and reach US$ 17.0 billion by 2033 growing at a CAGR of 10.4% during the forecast period from 2026 to 2033. Blood disorders are caused due to lack of blood components. These components include red blood cells, white blood cells, and platelets. Anemia, leucopenia, and thrombocytopenia are some of the common blood disorders. Some of the common symptoms of blood diseases include fatigue, headache, weakness, fever, infections, and bleeding.

Acquired orphan blood disease is a rare blood disorder characterized by an insufficient number of red blood cells. This disease is characterized by the body’s inability to produce red blood cells. Moreover, improper functioning of the bone marrow also leads to a lack of red blood cells, which in turn results in a decrease in platelet numbers.

Key Industry Highlights:

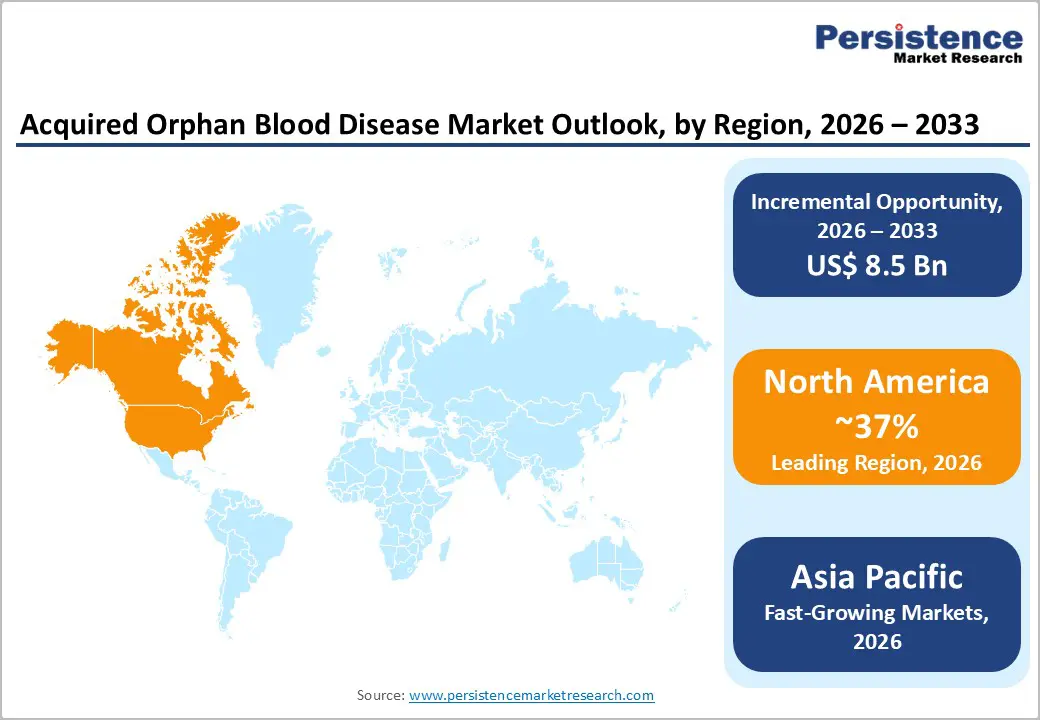

- Leading Region: North America leads the market due to high prevalence of rare blood disorders, advanced healthcare infrastructure, strong reimbursement systems, and established treatment protocols.

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by improving healthcare access, increasing awareness of rare hematologic diseases, and rising adoption of advanced therapies.

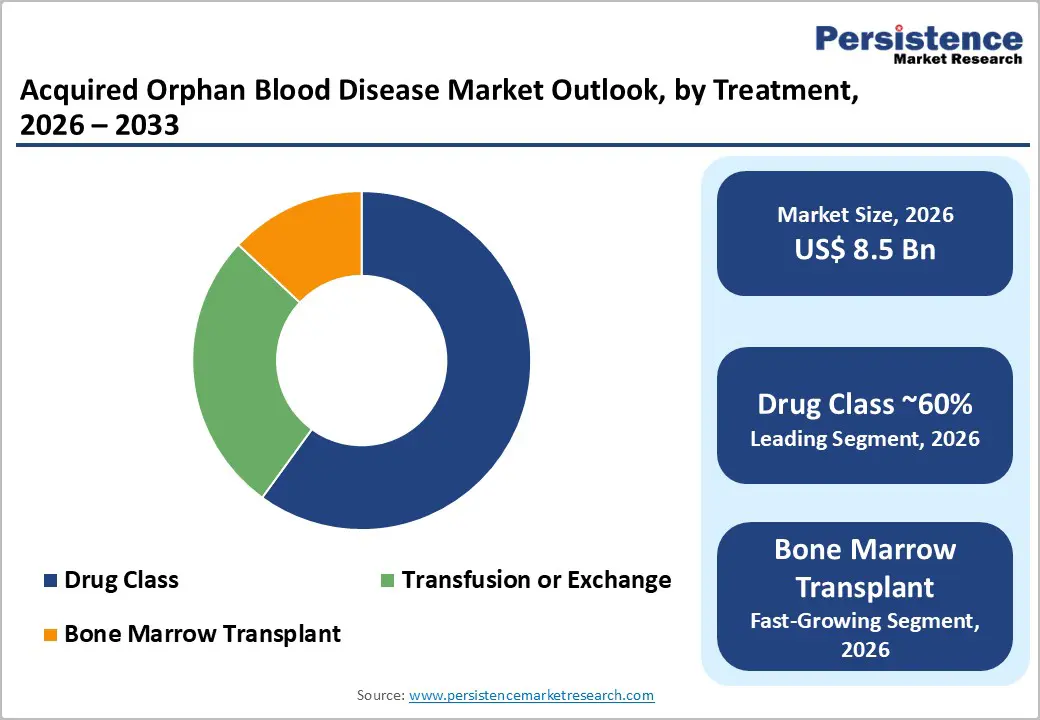

- Dominant Segment: Drug-class therapies dominate the market, fueled by the widespread use of targeted biologics, complement inhibitors, and immunomodulators for conditions such as PNH, aplastic anemia, and MDS.

- Fastest Growing Segment: Bone marrow transplant (BMT) is the fastest growing segment due to curative potential, advances in stem cell technology, improved donor matching, and expanding treatment eligibility.

| Key Insights | Details |

|---|---|

|

Acquired Orphan Blood Disease Market Size (2026E) |

US$ 8.5 Bn |

|

Market Value Forecast (2033F) |

US$ 17.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.6% |

Market Dynamics

Driver - Rising Incidence of Chronic Diseases Across the World

The growing global incidence of chronic diseases is a key driver of the acquired orphan blood disease market. As populations age and lifestyle-related factors such as poor diet, physical inactivity, and environmental exposures increase, the prevalence of chronic conditions such as diabetes, cancer, and autoimmune disorders also rises. These chronic illnesses often lead to complications, including rare blood disorders such as paroxysmal nocturnal hemoglobinuria (PNH), aplastic anemia, and myelodysplastic syndromes (MDS). The connection between chronic diseases and rare blood abnormalities highlights the need for early detection, improved diagnostics, and innovative treatment options, creating heightened demand for specialized healthcare solutions.

This rising burden has encouraged greater investment in research and development of therapies for orphan blood diseases. Healthcare systems are compelled to allocate additional resources, implement policy reforms, and foster collaborations to address the complex requirements of patients with these conditions. Consequently, both public and private stakeholders are increasingly focusing on expanding treatment access, enhancing clinical care, and advancing novel therapeutics. Together, these factors significantly drive growth in the acquired orphan blood disease market, offering opportunities for innovation, improved patient outcomes, and broader adoption of specialized medical interventions worldwide.

Restraints - Longer Duration for Approval of Drugs to Limit Opportunities

One significant restraint limiting opportunities in the acquired orphan blood disease market is the prolonged drug approval process. Orphan drug development often involves complex clinical trials, rigorous safety and efficacy assessments, and stringent regulatory scrutiny, which together extend timelines compared with non-orphan medicines. A study conducted by the Tufts Center for the Study of Drug Development revealed that the time required to transition from first patent filing to product launch for orphan drugs is 18% longer on average than it is for all new drugs, the transition from initial clinical studies to market launch for orphan drugs can take up to 17.2 years on average, significantly longer than standard drug development cycles. This extended timeline is compounded by challenges in patient recruitment due to a small, geographically dispersed population, leading to delays in completing statistically robust trials.

Furthermore, regulatory authorities may require extensive post-market data and long follow-up periods, often spanning several years, before granting full marketing approval, adding additional delays. These protracted approval processes limit the speed at which novel therapies reach patients, reduce the attractiveness of orphan drug investment for some developers, and can slow overall market growth by delaying revenue realization and patient access to innovative treatments.

Opportunity - Advancements in Genomic and Molecular Research

Advancements in genomic and molecular research are creating transformative opportunities in the acquired orphan blood disease market. Technologies such as next-generation sequencing (NGS), whole exome sequencing (WES), and whole genome sequencing (WGS) have dramatically improved the accuracy, speed, and affordability of identifying genetic variants linked to rare hematologic conditions, enabling earlier and more precise diagnosis. For example, WES can analyze ~1.5% of the human genome and captures about 85% of known disease-causing mutations, significantly enhancing rare-disease detection and therapeutic targeting. Moreover, emerging molecular tools, including CRISPR-based gene editing and base-editing platforms, are accelerating the development of curative treatment candidates, with nearly 45% of pipeline therapies in acquired orphan blood diseases involving gene or cell therapy modalities.

These genomic and molecular innovations not only accelerate drug discovery but also enable precision medicine strategies tailored to patient-specific biological profiles, improving clinical outcomes and reducing the length of diagnostic journeys. Continued integration of multi-omics data, computational analytics, and personalized treatment approaches will further expand market potential, attract investor interest and foster collaborations between biotech firms and research institutions focused on rare hematologic disorders.

Category-wise Analysis

By Treatment Insights

In the acquired orphan blood disease market, the drug class segment is expected to dominate, accounting for approximately 60% of the market share in 2025. This segment includes targeted therapies, biologics, and complement inhibitors for the treatment of rare hematologic disorders such as paroxysmal nocturnal hemoglobinuria (PNH), aplastic anemia, and myelodysplastic syndromes (MDS). High efficacy, better safety profiles, and strong clinical outcomes drive the preference for drug-based treatments among healthcare providers and patients. Additionally, ongoing research and the introduction of novel therapies continue to expand the drug class portfolio, reinforcing its dominant position.

Bone marrow transplant (BMT) is the fastest-growing treatment segment within the market due to its curative potential for patients with severe acquired blood diseases. Advances in stem cell technologies, improved donor matching, and reduced-intensity conditioning regimens have increased patient eligibility and success rates. Rising adoption of BMT in emerging markets, combined with growing awareness among healthcare providers and patients, contributes to rapid market expansion. The segment’s growth reflects its increasing role as a definitive treatment option alongside supportive care and pharmacologic therapies.

By Distribution Channel Insights

Hospital pharmacies are projected to remain the leading distribution channel for acquired orphan blood disease treatments in 2025, given the complexity and severity of these conditions. Patients with disorders such as aTTP, severe PNH, CAD crises, and high-risk MDS are primarily managed in tertiary care hospitals or academic medical centers. These settings provide essential services, including plasma exchange, intensive transfusion support, and stem cell transplantation. High-cost biologics, including complement inhibitors and anti-CD20 antibodies, are typically administered in inpatient units or hospital-based outpatient infusion centers under strict medical supervision, with reimbursement contracts negotiated at the institutional level.

Retail and online pharmacies currently serve a secondary role, mainly dispensing maintenance oral therapies, supportive medications, or refills for patients transitioned to home care. Their share is expected to increase gradually as subcutaneous and oral formulations of therapies become more widely available, allowing greater flexibility for patients and supporting the expansion of home-based treatment models alongside hospital-centered care.

Regional Insights

North America Acquired Orphan Blood Disease Market Trends

North America, led by the U.S., is projected to hold the largest regional share, around 37% in 2025, supported by strong diagnostic capabilities, high treatment affordability, and a robust orphan-drug regulatory framework. The U.S. Food and Drug Administration’s Orphan Drug Act has granted numerous designations and approvals for therapies targeting PNH, CAD, and aTTP, incentivizing innovation through market exclusivity, tax credits, and fee waivers. Extensive ADAMTS13 testing infrastructure, national hemovigilance programs, and large academic hematology networks enable rapid identification and management of immune-mediated thrombotic microangiopathies.

Innovation is particularly strong in North America, where several biotech and pharmaceutical companies are advancing proximal complement inhibitors, gene-editing strategies, and long-acting monoclonal antibodies aimed at reducing infusion frequency and overall treatment burden. Real-world data platforms and rare-disease registries are deeply integrated into clinical practice, supporting outcomes-based reimbursement and post-marketing safety surveillance. In Canada, national rare-disease funding initiatives and health technology assessment frameworks are gradually improving access to high-cost therapies, although timelines can be longer than in the U.S., leading to cross-border treatment flows for some patients.

Asia and Pacific Acquired Orphan Blood Disease Market Trends

Asia Pacific is expected to be the fastest-growing region in the Acquired Orphan Blood Disease market, supported by large under-diagnosed patient populations, expanding healthcare infrastructure, and rising adoption of advanced hematology therapies in China, Japan, India, and ASEAN countries. Japan and South Korea have long-established rare-disease and transplant programs, with national insurance systems increasingly covering complement inhibitors and other high-cost biologics for PNH and related disorders. In China, rapid build-out of tertiary hospitals, increasing availability of ADAMTS13 and flow cytometry testing, and inclusion of selected orphan therapies in national reimbursement lists are driving higher recognition and treatment of PNH, aTTP, and MDS.

India and several ASEAN markets are in earlier stages but are experiencing rapid growth in bone marrow transplant capacity, with an increasing number of centers performing allogeneic procedures for hematologic malignancies and severe aplastic anemia that overlap with PNH and MDS indications. Local and regional pharmaceutical companies are beginning to develop or license biosimilars and more affordable biologic alternatives, which could significantly expand access over the forecast period. Manufacturing-cost advantages in the region also make Asia Pacific an attractive base for large multinationals seeking to supply complement inhibitors, monoclonal antibodies, and supportive drugs globally, reinforcing its role as both a demand and supply hub.

Competitive Landscape

The acquired orphan blood disease market is highly competitive, with key players including Alexion Pharmaceuticals, Amgen, Celgene, Eli Lilly, Sanofi, GlaxoSmithKline, and Cyclacel Pharmaceuticals. These companies focus on developing innovative therapies, expanding pipelines, and strategic collaborations to strengthen market presence. Other notable participants include Onconova Therapeutics, Incyte Corporation, and CTI BioPharma, contributing to product diversification and technological advancements. Intense competition drives continuous research, improved treatment options, and broader access to therapies for rare blood disorders, enhancing overall market growth and innovation.

Key Industry Developments:

- In January 2024, Sanofi and Inhibrx, Inc. (“Inhibrx”), a publicly traded clinical-stage biopharmaceutical company focused on developing a broad pipeline of novel biologic therapeutic candidates, have entered into a definitive agreement under which Sanofi agreed to acquire Inhibrx following the spin-off of non-INBRX-101 assets into New Inhibrx.

- In November 2024, Cumberland Pharmaceuticals Inc., a specialty pharmaceutical company, announced that the U.S. Food and Drug Administration (FDA) had granted Ifetroban both Orphan Drug Designation and Rare Pediatric Disease Designation for treating cardiomyopathy linked to Duchenne muscular dystrophy (DMD).

Companies Covered in Acquired Orphan Blood Disease Market

- Sanofi S.A.

- Intas Pharmaceuticals Ltd.

- Bristol-Myers Squibb Company

- Celgene Corporation

- Dr. Reddy’s Laboratories

- Jiangsu Hengrui Medicine Co., Ltd

- Astex Pharmaceuticals, Inc.

- MGI Pharma Inc.

- SuperGen Inc.

- Johnson & Johnson

- Sanofi

- AstraZeneca

- Apellis Pharmaceuticals, Inc.

- Novartis AG

- Others

Frequently Asked Questions

The orphan blood disease market is projected to be valued at US$ 8.5 Bn in 2026.

Rising rare blood disorder diagnoses, regulatory orphan incentives, advanced targeted therapies, and growing patient awareness drive global market growth.

The global market is expected to witness a CAGR of 10.4% between 2026 and 2033.

Expansion of gene and cell therapies, emerging market access improvements, and precision medicine innovation present major opportunities.