- Executive Summary

- Global Clinical Trial Management System Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Component Adoption Analysis

- Recent Component Launches

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Component Prices

- Pricing Analysis, By Component Modality

- Regional Prices and Component Preferences

- Global Clinical Trial Management System Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

- Global Clinical Trial Management System Market Outlook: Component

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis and Volume (Units) Analysis, By Component, 2020 - 2025

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Attractiveness Analysis: Component

- Global Clinical Trial Management System Market Outlook: Modality

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Modality, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Attractiveness Analysis: Modality

- Global Clinical Trial Management System Market Outlook: System Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By System Type, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Attractiveness Analysis: System Type

- Global Clinical Trial Management System Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End User, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms Others

- Others

- Market Attractiveness Analysis: End User

- Key Highlights

- Global Clinical Trial Management System Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Clinical Trial Management System Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Component

- By Modality

- By System Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms

- Others

- Market Attractiveness Analysis

- Europe Clinical Trial Management System Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Component

- By Modality

- By System Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms

- Others

- Market Attractiveness Analysis

- East Asia Clinical Trial Management System Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Component

- By Modality

- By System Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms

- Others

- Market Attractiveness Analysis

- South Asia & Oceania Clinical Trial Management System Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Component

- By Modality

- By System Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms

- Others

- Market Attractiveness Analysis

- Latin America Clinical Trial Management System Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Component

- By Modality

- By System Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms

- Others

- Market Attractiveness Analysis

- Middle East & Africa Clinical Trial Management System Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Component

- By Modality

- By System Type

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Component, 2026 - 2033

- Hardware

- Software

- Services

- Market Size (US$ Bn) Analysis and Forecast, By Modality, 2026 - 2033

- Cloud-based

- Web-based

- On-premises

- Market Size (US$ Bn) Analysis and Forecast, By System Type, 2026 - 2033

- Enterprise-based

- Site-based

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Pharmaceutical and Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Medical Device Firms

- Others

- Market Attractiveness Analysis

- Competition Landscape

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Recent Developments)

- Oracle Corporation

- Overview

- Segments and Component & End User

- Key Financials

- Market Developments

- Market Strategy

- Merative US L.P.

- Medidata Solutions, Inc.

- Parexel International Corporation

- Clario

- MedNet Solutions, Inc.

- Advarra, Inc.

- DSG, Inc.

- eClinPro, LLC

- RealTime Software Solutions, LLC

- Simbec-Orion Group Limited

- Veeva Systems Inc.

- IQVIA Holdings Inc.

- SimpleTrials

- Ennov

- Others

- Oracle Corporation

- Market Structure

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Healthcare IT

- Clinical Trial Management System Market

Clinical Trial Management System Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Clinical Trial Management System Market by Component (Hardware, Software, and Services), by Modality (Cloud-based, Web-based, and On-premises), by System Type (Enterprise-based and Site-based) by End User (Pharmaceutical and Biopharmaceutical Companies, Clinical Research Organizations (CROs), Medical Device Firms, and Others), and Regional Analysis from 2026 - 2033

Key Industry Highlights:

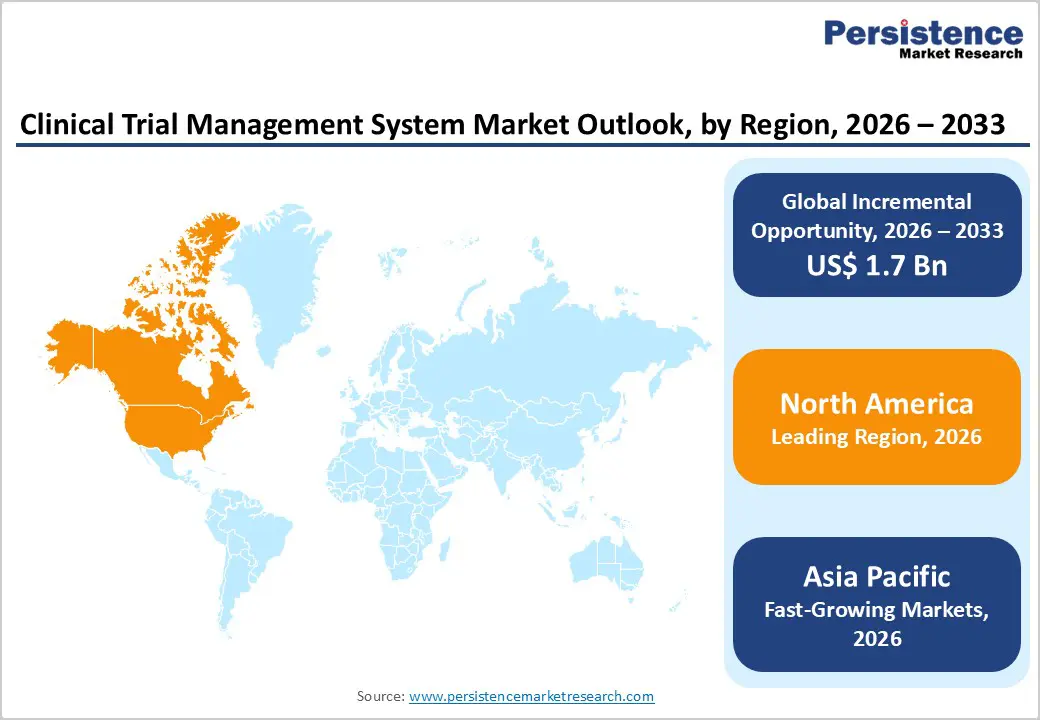

- Leading Region: North America accounts for the largest share at 48.5%, supported by a mature clinical research ecosystem, strong pharmaceutical R&D investment, advanced regulatory frameworks, and early implementation of integrated eClinical technologies.

- Fastest-Growing Region: Asia Pacific is expanding most rapidly due to increasing clinical trial outsourcing, large treatment-naïve patient populations, improving regulatory processes, and expanding research infrastructure across major economies.

- Leading Component Segment: Software dominates the market owing to its central role in protocol management, site monitoring, budgeting, compliance tracking, and integration with other digital clinical systems.

- Fastest-Growing Component Segment: Services are witnessing accelerated growth as organizations require implementation support, system validation, integration, and ongoing platform optimization.

- Leading Modality Segment: Cloud-based solutions lead adoption as they enable scalable deployment, remote access, faster updates, and improved collaboration across global trial networks.

- Fastest-Growing Modality Segment: Site-based systems are expanding quickly as investigator sites and research hospitals increasingly digitize study management to improve operational efficiency and data accuracy.

| Key Insights | Details |

|---|---|

|

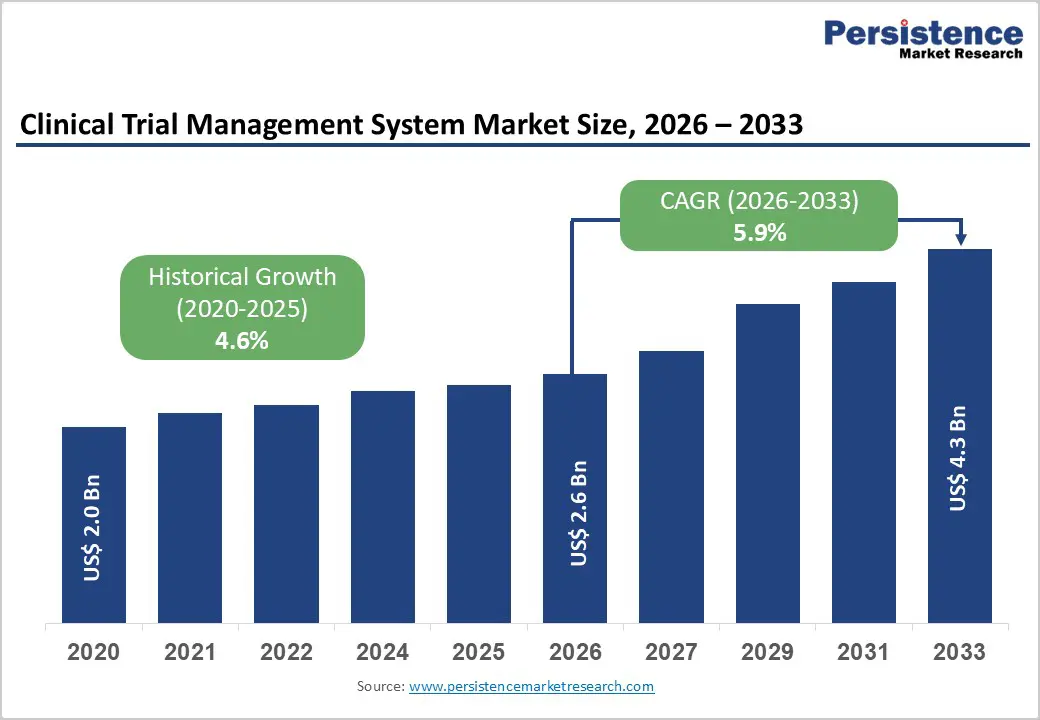

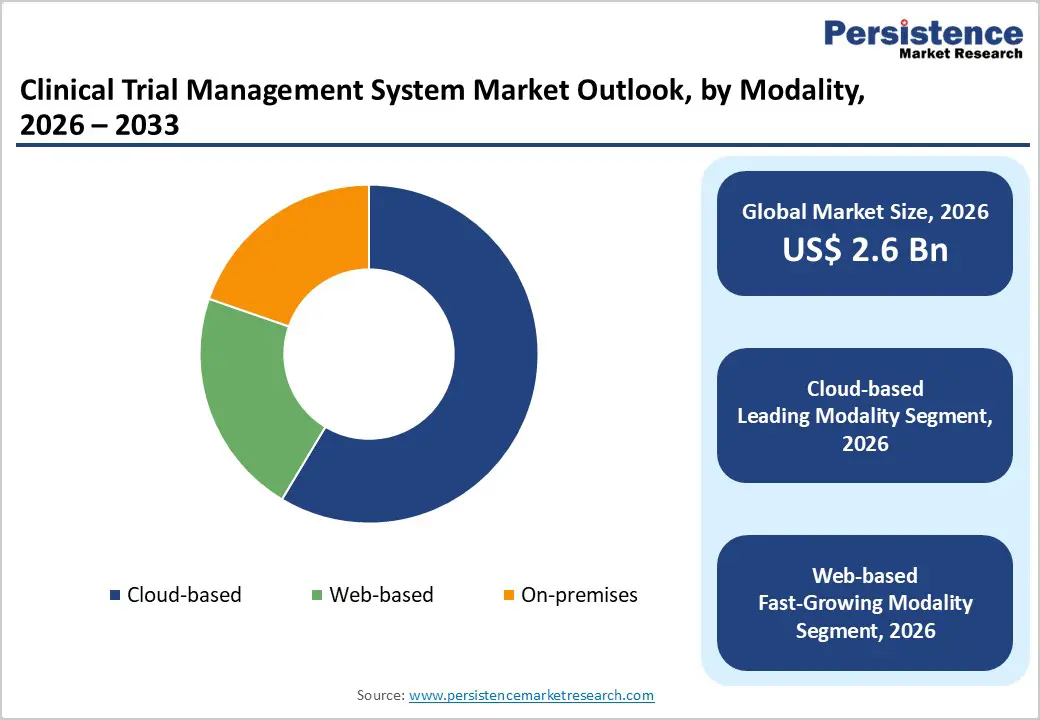

Clinical Trial Management System Market Size (2026E) |

US$ 2.6 Bn |

|

Market Value Forecast (2033F) |

US$ 4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.6% |

Market Dynamics

Driver - Increasing Clinical Trial Complexity and Digital Transformation Accelerating Platform Adoption

The rapid expansion of global clinical research activity, combined with growing protocol complexity, is a major factor supporting adoption of advanced trial management platforms. Modern clinical studies increasingly involve multi-country operations, diverse patient populations, adaptive trial designs, and extensive regulatory documentation requirements, making manual coordination inefficient and risk-prone. Pharmaceutical and biotechnology companies are conducting larger volumes of oncology, rare disease, and biologics trials, all of which require structured oversight of site performance, patient enrollment, budgeting, and compliance tracking. As development pipelines expand, organizations are prioritizing centralized systems that improve operational visibility and reduce delays across trial phases.

Digital transformation initiatives across life sciences are further strengthening demand. Integration of CTMS with electronic data capture, safety monitoring, and remote patient engagement tools enables real-time decision-making and improved collaboration among sponsors, CROs, and investigators. The rise of decentralized and hybrid clinical trials has amplified the need for cloud-enabled systems capable of supporting remote monitoring and distributed workflows. Automation of reporting, audit readiness, and risk-based monitoring processes helps reduce administrative burden while improving regulatory compliance. Continuous advancements in analytics, artificial intelligence, and predictive trial planning are enabling more efficient study execution, reinforcing sustained market expansion.

Restraints - High Implementation Costs and Organizational Transition Challenges Slowing Adoption

Despite strong growth momentum, adoption barriers remain linked to financial and operational challenges associated with system deployment. Implementation of enterprise-grade trial management platforms often requires substantial upfront investment involving licensing, customization, validation, and staff training. Smaller biotechnology firms, academic research centers, and emerging-market sponsors may face budget constraints that delay modernization initiatives. In addition, integration with legacy IT infrastructure and existing clinical data systems can be technically complex, requiring specialized expertise and extended deployment timelines.

Organizational change management also presents a significant hurdle. Transitioning from spreadsheet-based or fragmented tracking processes to centralized digital platforms demands workflow restructuring and user training across multiple departments. Resistance to change among clinical teams and investigators can slow adoption, particularly when new systems alter established operational practices. Data migration risks, cybersecurity concerns, and strict regulatory validation requirements further increase implementation complexity. Variability in global regulatory standards adds another layer of operational burden for multinational sponsors attempting standardized deployment. Limited digital maturity among certain research sites and inconsistent technology infrastructure in developing regions can also restrict full utilization of advanced system capabilities, moderating near-term adoption despite clear long-term efficiency benefits.

Opportunity - Growth of Decentralized Trials, AI Integration, and Emerging Research Markets Creating Expansion Potential

Significant growth opportunities are emerging as clinical research shifts toward more patient-centric and technology-driven models. Decentralized and hybrid trial approaches are gaining momentum, enabling remote participation through telemedicine, wearable devices, and home-based data collection. These evolving models require sophisticated coordination tools capable of managing distributed investigators, virtual visits, and real-time performance tracking, creating strong demand for advanced management platforms. As sponsors aim to accelerate recruitment and improve patient retention, integrated solutions that combine operational oversight with analytics-driven insights are becoming increasingly valuable.

Artificial intelligence and advanced analytics represent another important opportunity area. Predictive modeling for site selection, enrollment forecasting, and risk identification allows sponsors to optimize trial execution and reduce costly delays. Expansion of biotechnology innovation across the Asia Pacific, Latin America, and parts of Eastern Europe is also increasing demand for scalable digital infrastructure as new sponsors enter global research ecosystems. Partnerships between technology providers and CROs are enabling bundled eClinical offerings, improving accessibility for mid-sized organizations. Additionally, regulatory agencies are encouraging digital data standardization and transparency, supporting broader system adoption. Continuous innovation in interoperability, automation, and patient engagement technologies is expected to unlock substantial long-term growth potential across the evolving clinical research landscape.

Category-wise Analysis

By Component Insights

Software is expected to remain the dominant component in the global clinical trial management system market in 2026, accounting for 61.8% of total revenue. Its leadership stems from the essential role CTMS software plays in protocol planning, site management, budgeting, subject tracking, and regulatory documentation throughout the clinical development lifecycle. Sponsors and CROs increasingly rely on integrated digital platforms to manage multi-country trials and complex study designs efficiently. The shift toward real-time analytics, automated reporting, and interoperability with EDC, ePRO, and safety systems has strengthened software adoption across organizations of all sizes. In addition, regulatory pressure for transparent audit trails and standardized workflows has accelerated platform modernization. Continuous upgrades involving AI-assisted forecasting, risk-based monitoring tools, and workflow automation are improving operational efficiency, reducing trial timelines, and supporting sustained dominance of the software segment.

By Modality Insights

Cloud-based deployment is projected to hold the largest share of 58.6% in 2026, driven by growing demand for flexible and remotely accessible trial infrastructure. Pharmaceutical sponsors and CROs increasingly favor cloud environments to enable centralized oversight across geographically dispersed study sites. Cloud architecture supports faster system deployment, lower upfront IT investment, and seamless updates aligned with evolving regulatory requirements. The expansion of decentralized and hybrid clinical trials has further accelerated adoption, as investigators, monitors, and sponsors require secure remote access to trial data and performance dashboards. Enhanced cybersecurity frameworks, data backup capabilities, and compliance certifications have improved confidence among regulated users. Furthermore, cloud platforms enable easier integration with digital health technologies and patient engagement tools, improving collaboration and operational visibility while supporting faster study execution timelines across global research programs.

By End-user Insights

Pharmaceutical and biopharmaceutical companies are anticipated to account for 44.6% of the CTMS market in 2026, reflecting their central role as primary trial sponsors. Increasing R&D investments, rising biologics and specialty drug development, and growing clinical trial complexity are driving adoption of advanced trial management platforms. These organizations require centralized systems capable of coordinating large investigator networks, managing regulatory submissions, tracking enrollment milestones, and controlling trial budgets across multiple regions. As development pipelines expand into oncology, rare diseases, and personalized medicine, operational coordination has become more data-intensive, strengthening reliance on CTMS solutions. Additionally, outsourcing strategies involving CRO partnerships necessitate unified platforms that enhance transparency and collaboration. Automation of monitoring activities, financial tracking, and compliance management helps sponsors reduce operational inefficiencies while accelerating time-to-market, reinforcing segment leadership.

Regional Insights

North America Clinical Trial Management System Market Trends

North America is expected to dominate the global clinical trial management system market with a value share of 48.5% in 2026, led primarily by the United States. The region benefits from a highly structured clinical research environment supported by advanced healthcare infrastructure, strong regulatory frameworks, and substantial pharmaceutical R&D expenditure. A large concentration of biopharmaceutical sponsors, CROs, and academic research institutions generates continuous demand for sophisticated trial management technologies. Adoption of decentralized trial methodologies, digital endpoints, and real-time monitoring solutions is particularly high, encouraging rapid migration toward cloud-enabled CTMS platforms. Regulatory expectations around data integrity, patient safety, and audit readiness further promote system standardization.

Additionally, widespread integration of CTMS with broader eClinical ecosystems enhances operational visibility and efficiency. Ongoing investments in precision medicine, oncology trials, and rare disease research continue to increase study volumes, sustaining long-term regional dominance while encouraging innovation in analytics-driven trial oversight and automated compliance management solutions.

Europe Clinical Trial Management System Market Trends

The Europe clinical trial management system market is projected to grow steadily, supported by coordinated research initiatives and strong public healthcare systems across major countries including Germany, the U.K., France, and Italy. Increasing implementation of harmonized regulatory frameworks and cross-border clinical studies is encouraging adoption of centralized digital trial platforms. European sponsors and academic institutions emphasize standardized protocols, data transparency, and cost-efficient research execution, all of which favor CTMS deployment. Growth is also supported by rising clinical activity in oncology, neurology, and rare disease research programs funded through public-private collaborations. The region demonstrates increasing reliance on cloud-based infrastructure to streamline investigator coordination and regulatory reporting requirements.

Moreover, expansion of mid-sized biotechnology firms is contributing to new system adoption as organizations transition from manual tracking to automated trial oversight. Continued investment in digital health integration, patient recruitment optimization, and real-world evidence generation is expected to sustain consistent market progression across the region.

Asia Pacific Clinical Trial Management System Market Trends

The Asia Pacific clinical trial management system market is anticipated to register a CAGR of around 7.9% between 2026 and 2033, reflecting rapid expansion of clinical research capabilities across China, India, Japan, South Korea, and Southeast Asia. Increasing attractiveness of the region for global trials driven by large patient pools, diverse disease profiles, and comparatively lower operational costs is accelerating CTMS adoption among sponsors and CROs. Governments are investing in healthcare digitization, regulatory modernization, and research infrastructure development, enabling faster trial approvals and improved data management practices. Growth in domestic pharmaceutical innovation and biosimilar development is further increasing demand for structured trial oversight tools.

Additionally, rising collaborations between global sponsors and regional research institutions are promoting technology transfer and adoption of standardized eClinical platforms. Improvements in investigator training, site connectivity, and digital data capture capabilities are strengthening operational efficiency, positioning Asia Pacific as a key long-term growth engine for the CTMS market.

Competitive Landscape

- In April 2025, Veeva Systems introduced Veeva SiteVault CTMS, a site-focused clinical trial management solution integrated with SiteVault eISF and eConsent, enabling research sites to manage studies within a unified platform while supporting seamless bidirectional data exchange with sponsors to streamline workflows and improve operational efficiency.

- In November 2025, Tata Consultancy Services launched the next-generation TCS ADD™ Risk-Based Quality Management (RBQM) platform, an AI-enabled integrated solution designed to provide pharmaceutical, MedTech, CROs, and research organizations with proactive, compliant oversight and intelligent monitoring across the entire clinical trial lifecycle.

- In November 2025, Medidata Solutions, Inc. announced that Caidya expanded its adoption of Medidata Experiences, adding Clinical Trial Management System (CTMS) and Clinical Data Studio solutions to enhance connected workflows, improve data integration, and enable more data-driven decision-making across its global clinical trial operations.

Companies Covered in Clinical Trial Management System Market

- Oracle Corporation

- Merative US L.P.

- Medidata Solutions, Inc.

- Parexel International Corporation

- Clario

- MedNet Solutions, Inc.

- Advarra, Inc.

- DSG, Inc.

- eClinPro, LLC

- RealTime Software Solutions, LLC

- Simbec-Orion Group Limited

- Veeva Systems Inc.

- IQVIA Holdings Inc.

- SimpleTrials

- Ennov

- Others

Frequently Asked Questions

The global clinical trial management system market is projected to be valued at US$ 2.6 Bn in 2026.

Rising global clinical trial volume, increasing trial complexity, growing outsourcing to CROs, and strong adoption of cloud-based digital trial management platforms are driving CTMS market growth.

The global clinical trial management system market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Expansion of decentralized and hybrid clinical trials, AI-enabled analytics integration, emerging-market trial activity, and demand for unified eClinical platforms create significant growth opportunities.

Oracle Corporation, Merative US L.P., Medidata Solutions, Inc., Parexel International Corporation, and Clario are some of the key players in the clinical trial management system market.