1. Executive Summary

1.1. Global Urinary Catheters Market Snapshot, 2025 and 2032

1.2. Market Opportunity Assessment, 2025 – 2032, US$ Bn

1.3. Key Market Trends

1.4. Future Market Projections

1.5. Premium Market Insights

1.6. Industry Developments and Key Market Events

1.7. PMR Analysis and Recommendations

2. Market Overview

2.1. Market Scope and Definition

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Opportunity

2.2.4. Challenges

2.2.5. Key Trends

2.3. Macro-Economic Factors

2.3.1. Global Sectorial Outlook

2.3.2. Global GDP Growth Outlook

2.4. COVID-19 Impact Analysis

2.5. Forecast Factors – Relevance and Impact

3. Value Added Insights

3.1. Product Adoption Analysis

3.2. Regulatory Landscape

3.3. Value Chain Analysis

3.4. Key Deals and Mergers

3.5. PESTLE Analysis

3.6. Porter’s Five Force Analysis

4. Price Trend Analysis, 2019 – 2032

4.1. Key Highlights

4.2. Key Factors Impacting Product Prices

4.3. Pricing Analysis, By Product

4.4. Regional Prices and Product Preferences

5. Global Urinary Catheters Market Outlook:

5.1. Key Highlights

5.1.1. Market Volume (Units) Projections

5.1.2. Market Size (US$ Bn) and Y-o-Y Growth

5.1.3. Absolute $ Opportunity

5.2. Market Size (US$ Bn) Analysis and Forecast

5.2.1. Historical Market Size (US$ Bn) Analysis, 2019-2023

5.2.2. Current Market Size (US$ Bn) Analysis and Forecast, 2025–2032

5.3. Global Urinary Catheters Market Outlook: Product

5.3.1. Introduction / Key Findings

5.3.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product, 2019-2023

5.3.3. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

5.3.3.1. Intermittent Catheter

5.3.3.2. Indwelling (Foley) Catheter

5.3.3.3. External Catheter

5.4. Market Attractiveness Analysis: Product

5.5. Global Urinary Catheters Market Outlook: Type

5.5.1. Introduction / Key Findings

5.5.2. Historical Market Size (US$ Bn) Analysis, By Type, 2019-2023

5.5.3. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

5.5.3.1. Coated

5.5.3.2. Uncoated

5.6. Market Attractiveness Analysis: Type

5.7. Global Urinary Catheters Market Outlook: Application

5.7.1. Introduction / Key Findings

5.7.2. Historical Market Size (US$ Bn) Analysis, By Application, 2019-2023

5.7.3. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

5.7.3.1. Urinary Incontinence

5.7.3.2. Urinary Retention

5.7.3.3. Prostate Gland Surgery

5.7.3.4. Spinal Cord Injury

5.7.3.5. Others

5.8. Market Attractiveness Analysis: Application

5.9. Global Urinary Catheters Market Outlook: End User

5.9.1. Introduction / Key Findings

5.9.2. Historical Market Size (US$ Bn) Analysis, By End User, 2019-2023

5.9.3. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

5.9.3.1. Hospitals

5.9.3.2. Long-term Care Facilities

5.9.3.3. Other

5.10. Market Attractiveness Analysis: End User

6. Global Urinary Catheters Market Outlook: Region

6.1. Key Highlights

6.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2019-2023

6.3. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025–2032

6.3.1. North America

6.3.2. Europe

6.3.3. East Asia

6.3.4. South Asia and Oceania

6.3.5. Latin America

6.3.6. Middle East & Africa

6.4. Market Attractiveness Analysis: Region

7. North America Urinary Catheters Market Outlook:

7.1. Key Highlights

7.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Market, 2019-2023

7.2.1. By Country

7.2.2. By Product

7.2.3. By Type

7.2.4. By Application

7.2.5. By End User

7.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025–2032

7.3.1. U.S.

7.3.2. Canada

7.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

7.4.1. Intermittent Catheter

7.4.2. Indwelling (Foley) Catheter

7.4.3. External Catheter

7.5. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

7.5.1. Coated Catheters

7.5.2. Uncoated Catheters

7.6. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

7.6.1. Urinary Incontinence

7.6.2. Urinary Retention

7.6.3. Prostate Gland Surgery

7.6.4. Spinal Cord Injury

7.6.5. Others

7.7. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

7.7.1. Hospitals

7.7.2. Long-Term Care Facilities

7.7.3. Other

7.8. Market Attractiveness Analysis

8. Europe Urinary Catheters Market Outlook:

8.1. Key Highlights

8.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Market, 2019-2023

8.2.1. By Country

8.2.2. By Product

8.2.3. By Type

8.2.4. By Application

8.2.5. By End User

8.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025–2032

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.3.6. Russia

8.3.7. Türkiye

8.3.8. Rest of Europe

8.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

8.4.1. Intermittent Catheter

8.4.2. Indwelling (Foley) Catheter

8.4.3. External Catheter

8.5. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

8.5.1. Coated Catheters

8.5.2. Uncoated Catheters

8.6. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

8.6.1. Urinary Incontinence

8.6.2. Urinary Retention

8.6.3. Prostate Gland Surgery

8.6.4. Spinal Cord Injury

8.6.5. Others

8.7. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

8.7.1. Hospitals

8.7.2. Long-Term Care Facilities

8.7.3. Other

8.8. Market Attractiveness Analysis

9. East Asia Urinary Catheters Market Outlook:

9.1. Key Highlights

9.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Market, 2019-2023

9.2.1. By Country

9.2.2. By Product

9.2.3. By Type

9.2.4. By Application

9.2.5. By End User

9.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025–2032

9.3.1. China

9.3.2. Japan

9.3.3. South Korea

9.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

9.4.1. Intermittent Catheter

9.4.2. Indwelling (Foley) Catheter

9.4.3. External Catheter

9.5. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

9.5.1. Coated Catheters

9.5.2. Uncoated Catheters

9.6. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

9.6.1. Urinary Incontinence

9.6.2. Urinary Retention

9.6.3. Prostate Gland Surgery

9.6.4. Spinal Cord Injury

9.6.5. Others

9.7. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

9.7.1. Hospitals

9.7.2. Long-Term Care Facilities

9.7.3. Other

9.8. Market Attractiveness Analysis

10. South Asia & Oceania Urinary Catheters Market Outlook:

10.1. Key Highlights

10.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Market, 2019-2023

10.2.1. By Country

10.2.2. By Product

10.2.3. By Type

10.2.4. By Application

10.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025–2032

10.3.1. India

10.3.2. Southeast Asia

10.3.3. ANZ

10.3.4. Rest of South Asia & Oceania

10.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

10.4.1. Intermittent Catheter

10.4.2. Indwelling (Foley) Catheter

10.4.3. External Catheter

10.5. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

10.5.1. Coated Catheters

10.5.2. Uncoated Catheters

10.6. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

10.6.1. Urinary Incontinence

10.6.2. Urinary Retention

10.6.3. Prostate Gland Surgery

10.6.4. Spinal Cord Injury

10.6.5. Others

10.7. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

10.7.1. Hospitals

10.7.2. Long-Term Care Facilities

10.7.3. Other

10.8. Market Attractiveness Analysis

11. Latin America Urinary Catheters Market Outlook:

11.1. Key Highlights

11.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Market, 2019-2023

11.2.1. By Country

11.2.2. By Product

11.2.3. By Type

11.2.4. By Application

11.2.5. By End User

11.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025–2032

11.3.1. Brazil

11.3.2. Mexico

11.3.3. Rest of Latin America

11.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

11.4.1. Intermittent Catheter

11.4.2. Indwelling (Foley) Catheter

11.4.3. External Catheter

11.5. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

11.5.1. Coated Catheters

11.5.2. Uncoated Catheters

11.6. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

11.6.1. Urinary Incontinence

11.6.2. Urinary Retention

11.6.3. Prostate Gland Surgery

11.6.4. Spinal Cord Injury

11.6.5. Others

11.7. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

11.7.1. Hospitals

11.7.2. Long-Term Care Facilities

11.7.3. Other

11.8. Market Attractiveness Analysis

12. Middle East & Africa Urinary Catheters Market Outlook:

12.1. Key Highlights

12.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Market, 2019-2023

12.2.1. By Country

12.2.2. By Product

12.2.3. By Type

12.2.4. By Application

12.2.5. By End User

12.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025–2032

12.3.1. GCC Countries

12.3.2. Egypt

12.3.3. South Africa

12.3.4. Northern Africa

12.3.5. Rest of Middle East & Africa

12.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025–2032

12.4.1. Intermittent Catheter

12.4.2. Indwelling (Foley) Catheter

12.4.3. External Catheter

12.5. Current Market Size (US$ Bn) Analysis and Forecast, By Type, 2025–2032

12.5.1. Coated Catheters

12.5.2. Uncoated Catheters

12.6. Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025–2032

12.6.1. Urinary Incontinence

12.6.2. Urinary Retention

12.6.3. Prostate Gland Surgery

12.6.4. Spinal Cord Injury

12.6.5. Others

12.7. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025–2032

12.7.1. Hospitals

12.7.2. Long-Term Care Facilities

12.7.3. Other

12.8. Market Attractiveness Analysis

13. Competition Landscape

13.1. Market Share Analysis, 2025

13.2. Market Structure

13.2.1. Competition Intensity Mapping By Market

13.2.2. Competition Dashboard

13.3. Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

13.3.1. B. Braun Melsungen AG

13.3.1.1. Overview

13.3.1.2. Segments and Product Types

13.3.1.3. Key Financials

13.3.1.4. Market Developments

13.3.1.5. Market Strategy

13.3.2. Coloplast A/S

13.3.3. Becton, Dickinson and Company

13.3.4. Teleflex Incorporated

13.3.5. Boston Scientific Corporation

13.3.6. Medtronic plc.

13.3.7. Hollister Incorporate

13.3.8. Cook Medical

13.3.9. Cathetrix

13.3.10. UroDev Medical

13.3.11. Stryker Corporation

13.3.12. Consure Medical

13.3.13. J and M Urinary Catherters LLC

13.3.14. Urocare Products Inc.

13.3.15. Wellspect Healthcare

13.3.16. CompactCath

13.3.17. ConvaTec

13.3.18. Cardinal Health, Inc.

13.3.19. Amsino International Inc.

14. Appendix

14.1. Research Methodology

14.2. Research Assumptions

14.3. Acronyms and Abbreviations

- Medical Devices

- Urinary Catheters Market

Urinary Catheters Market Size, Share, and Growth Forecast for 2025 - 2032

Urinary Catheters Market by Product (Intermittent Catheter, Indwelling Catheter, External Catheter), Type (Coated, Uncoated), Application, End User, and Regional Analysis from 2025 to 2032

Urinary Catheters Market Size and Share Analysis

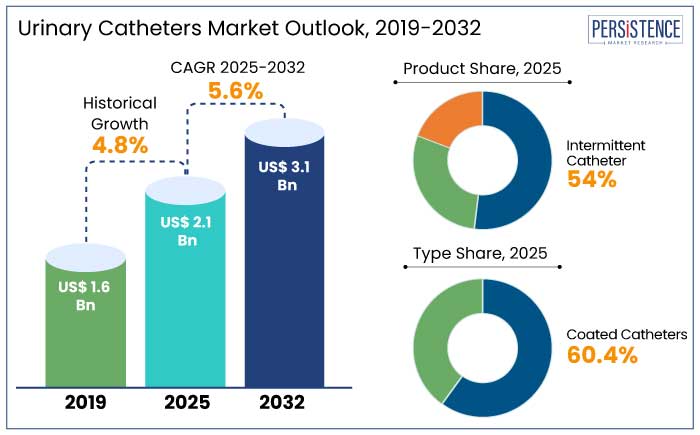

The global urinary catheters market is predicted to reach a size of US$ 2.1 Bn by 2025. It is anticipated to witness a CAGR of 5.6% during the forecast period to attain a value of US$ 3.1 Bn by 2032.

According to the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), around 25% of adults aged 65 and above experience urinary incontinence, leading to a rising need for urinary catheters. Aging population is a significant contributor to growth of the urinary catheter industry. Rise in home healthcare services is bolstering demand for user friendly and portable urinary catheter solutions.

Patients managing chronic conditions prefer self-catheterization, leading to popularity of intermittent urinary catheters. Antimicrobial catheters are witnessing rising demand as they reduce the risk of catheter associated urinary tract infections (CAUTIs). Studies indicate that antimicrobial catheters can decrease infection rates by 30% compared to standard catheters.

Key Highlights of the Industry

- Hydrophilic coatings are witnessing rising demand as these decrease friction while minimizing discomfort during insertion and removal.

- Increased preference for disposable and single-use catheters owing to rising awareness regarding friction control and hygiene is set to boost growth.

- Male external catheters or condom catheters are gaining traction owing to their non-invasive nature and lower risk of infection.

- Closed system catheters are experiencing growth as these are designed to maintain sterility, further minimizing the risk of infections.

- The World Health Organization (WHO) estimates that the population aged 65 and above is estimated to reach 1.5 by 2050, fueling demand for catheters designed for long-term and intermittent use.

- Rising prevalence of bladder dysfunctions and prostate enlargement are the key growth drivers.

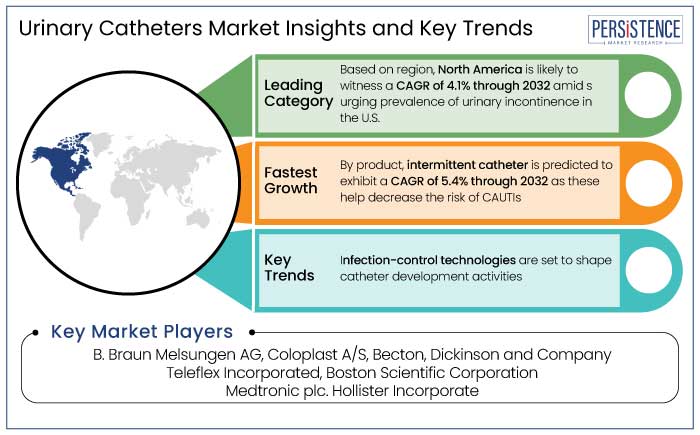

- By product, the intermittent catheter segment is predicted to exhibit a CAGR of 5.4% through 2032 as these help minimize the risk of CAUTIs.

- Based on type, the coated catheters segment is predicted to hold a share of 60.4% in 2025 as these lower the risk of infections.

- The urinary catheters market in North America is set to hold a share of 38.7% in 2025 owing to increasing aging population in the region.

|

Market Attributes |

Key Insights |

|

Urinary Catheters Market Size (2025E) |

US$ 2.1 Bn |

|

Projected Market Value (2032F) |

US$ 3.1 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

4.8% |

Rising Aging Population in North America to Augment Demand

North America urinary catheters market is estimated to hold a share of 38.7% in 2025 and witness a CAGR of 4.1% through 2032. Urological conditions like urinary retention, incontinence, and bladder dysfunction are highly prevalent in the region. For example,

- According to the National Association for Continence (NAFC), nearly 25 million Americans witness urinary incontinence, a significant factor driving demand for urinary catheters.

The aging population of the region is particularly affected with over 30% of men and women aged 65 and above predicted to have some form of urinary incontinence. This fuels the need for intermittent and indwelling catheters.

- According to the U.S. Census Bureau, the population aged 65 and older in the U.S. reached 56 million in 2020 and is predicted to grow to 73 million by 2030.

Older adults are predicted to require long-term catheterization, supporting the growth of urinary catheter market in the region. Availability of skilled healthcare professionals in the region ensures the widespread adoption of catheters in hospitals and clinics.

Hospitals to Recommend Intermittent Catheters as a Safer Alternative

Intermittent catheter is anticipated to hold a share of 54% in 2025. These catheters are designed for temporary use, thereby minimizing the risk of catheter associated urinary tract infections (CAUTIs).

- A study published in the Journal of Urology found that patients using intermittent catheters experienced a 30% lower risk of UTIs compared to those using indwelling catheters.

Hospitals and healthcare providers recommend intermittent catheterization as a safer alternative, driving the demand for clinical and home care settings. Intermittent catheters are user-friendly and designed for self-catheterization, making these ideal for patients managing chronic conditions at home. For instance,

- The National Home Care and Hospice Association reports that over 12 million Americans receive home healthcare annually, and intermittent catheters are among the most commonly used devices.

Coated Catheters are Preferred as these Help Lower the Risk of Infections

Coated catheters are projected to account for a share of 60.4% in 2025. Coated catheters, like antimicrobial-coated and hydrophilic-coated types, lower the risk of infections compared to uncoated catheters. For example,

- The Centers for Disease Control and Prevention (CDC) estimates that 12% to 16% of hospitalized patients undergo urinary catheterization, making them susceptible to CAUTIs. Coated catheters have been shown to decrease this risk by 40% to 70%.

Antimicrobial coatings prevent bacterial adhesion, while hydrophilic coatings decrease friction, lowering irritation and infection risk. Hydrophilic-coated catheters feature a lubricating layer activated by water, minimizing friction during insertion and removal. This makes them particularly suitable for patients requiring frequent catheterization. For instance,

- A study published in the Journal of Clinical Urology found that hydrophilic-coated catheters reduced discomfort in 85% of patients compared to standard catheters.

Urinary Catheters Market Introduction and Trend Analysis

Potential growth in the global urinary catheters industry is predicted to be driven by an emphasis on user-friendly designs and compact products for home based. Smart catheters with IoT enabled monitoring are likely to gain traction in hospitals as well as home care settings. Manufacturers are set to invest in biodegradable and environmentally friendly catheter materials to align with global sustainability goals.

Historical Growth and Course Ahead

The urinary catheters market growth was steady at a CAGR of 4.8% during the historical period from 2019 to 2023. Increased awareness and improved healthcare access in developed as well as emerging markets drove growth. For example,

- According to the World Health Organization (WHO), around 420 million people globally witnessed urinary incontinence or bladder dysfunction in 2023, up from 390 million in 2019.

Growing geriatric population in North America, Europe, and Asia Pacific fueled demand for urinary catheters as older adults are more prone to blood-related conditions. A shift toward self-catheterization for managing chronic conditions contributed to expansion.

Growth during the forecast period is likely to be driven by rising adoption of novel technologies in the field. Development of healthcare infrastructure in emerging markets is likely to augment demand.

Market Growth Drivers

Increased Focus on Homebased Care

Conditions like urinary incontinence, neurogenic bladder, and benign prostatic hyperplasia (BPH) often require long term management using urinary catheters. For example,

- According to the National Association for Continence (NAFC), around 70% of patients with urinary incontinence prefer self-catheterization over relying on healthcare providers for assistance.

Self-catheterization has become a popular option for patients requiring intermittent catheterization owing to convenience and cost-effectiveness. Innovations like hydrophilic coated catheters are easy to use and decrease discomfort, boosting their adoption in home settings. For instance,

- The Agency for Healthcare Research and Quality (AHRQ) reports that home healthcare is 30% to 50% more cost-effective than institutional care.

Favorable Reimbursement Policies

Several countries include intermittent, indwelling, and external urinary catheters in their healthcare reimbursement frameworks. This ensures that patients can access necessary products without incurring substantial out-of-pocket expenses. For example,

- In the U.S., Medicare Part B and private insurance plans cover intermittent catheterization supplies for individuals with permanent urological conditions.

Coverage includes 200 catheters per month for eligible patients. Catheters with sterile packaging or coatings are also reimbursable if deemed medically necessary. For example,

- In Canada, provincial health programs like the Assistive Devices Program (ADP) in Ontario provide coverage for urinary catheters, decreasing the financial burden on patients.

- Hydrophilic-coated catheters, known for decreasing catheter-associated urinary tract infections (CAUTIs), saw a 12% higher adoption rate in regions with comprehensive reimbursement policies.

Market Restraining Factors

High Cost of Innovative Catheters

Cost of unique catheters, like hydrophilic-coated, antimicrobial-coated, and silicone catheters, is higher than traditional catheters. This makes them less accessible in regions with budget constraints, like in emerging economies or underfunded healthcare systems. For example,

- Based on data obtained from prominent manufacturers, advanced catheters can cost up to 50% to 100% more than standard uncoated catheters.

High cost of these products is likely to limit their widespread adoption, especially in cost-sensitive markets.

Market Growth Opportunities

Awareness Campaigns and Educational Initiatives

Campaigns focusing on conditions like urinary incontinence, neurogenic bladder, and prostate issues are educating the public on the importance of timely diagnosis and management. Manufacturers and healthcare providers are organizing workshops, webinars, and tutorials to train patients and caregivers in proper catheter usage. For example,

- Organizations like the World Federation of Incontinence and Pelvic Problems (WFIPP) run global campaigns to address misconceptions and promote the use of medical devices like catheters.

Initiatives targeting healthcare professionals ensure they are equipped to guide patients in choosing the right type of catheter and provide training on its proper use. Training programs also emphasize infection control practices to decrease catheter-associated urinary tract infections (CAUTIs).

- Non-profits and advocacy groups, like the National Association for Continence (NAFC), run annual events and campaigns like "Bladder Health Awareness Month", focusing on the importance of urinary health and the role of catheters in improving quality of life.

Increasing Focus on Infection Prevention

Catheter-associated UTIs are among the most common healthcare associated infections across the globe. For instance,

- According to the Centers for Disease Control and Prevention (CDC), CAUTIs account for 75% of urinary tract infections in hospitals.

The CDC also estimated that 12% to 16% of adult hospitals inpatients will require a urinary catheter during their stay, thereby increasing the risk of infection. In several countries, hospitals may face penalties or decreased reimbursements for avoidable CAUTIs in several countries. For instance,

- Regulatory bodies like the World Health Organization (WHO) and Joint Commission International (JCI) emphasize infection prevention in catheter use.

- Under the Medicare Hospital-Acquired Condition (HAC) Reduction Program, U.S. hospitals may receive decreased reimbursements for CAUTI-related cases.

Competitive Landscape for the Urinary Catheters Market

Companies in the urinary catheters market are focusing on the development of high-performance catheters that offer additional benefits. These features decrease infection risks while improving patient comfort.

Businesses are offering customized solutions to cater to specific requirements. This ensures consumers have a range of choices, thereby increasing satisfaction and demand.

Manufacturers are focusing on disposable catheters owing to the rising need for single use products that decrease the risk of infections. They are focusing on continuous product development of disposable urinary catheters that offer high comfort while decreasing the risk of cross contamination.

Companies are broadening their product portfolio beyond urinary catheters to include complementary products. This includes catheter insertion kits, urinary drainage bags, and continence care products.

Recent Industry Developments

- In January 2024, the California Institute of Technology published a report on how their researchers utilized AI to develop a catheter design that reduced bacterial upstream movement by 100-fold in lab tests. This innovation prevents the use of antibiotics or chemicals, ensuring effective infection prevention.

- In September 2023, the Sage PrimaFit External Urine Management device reduced CAUTI rates by 72%. Clinical Nurse Specialists implemented a quality improvement program to decrease the prevalence and associated harm of catheter-associated urinary tract infections effectively.

- In February 2023, Coloplast launched a male catheter designed to reduce the risk of urinary tract infections. The new product aims to improve patient care by minimizing infection rates associated with catheter use in men.

Companies Covered in Urinary Catheters Market

- B. Braun Melsungen AG

- Coloplast A/S

- Becton, Dickinson and Company

- Teleflex Incorporated

- Boston Scientific Corporation

- Medtronic plc.

- Hollister Incorporate

- Cook Medical

- Cathetrix

- UroDev Medical

- Stryker Corporation

- Consure Medical

- J and M Urinary Catherters LLC

- Urocare Products Inc.

- Wellspect Healthcare

- CompactCath

- ConvaTec

- Cardinal Health, Inc.

- Amsino International Inc.

Frequently Asked Questions

The market is anticipated to reach a value of US$ 3.1 Bn by 2032.

Intermittent, indwelling (foley), and external catheter are the three types.

North America is anticipated to emerge as the leading region with a share of 38.7% in 2025.

Prominent players in the market include B. Braun Melsungen AG, Coloplast A/S, and Becton, Dickinson and Company.

The market is predicted to witness a CAGR of 5.6% throughout the forecast period.