- Executive Summary

- Global Silanes Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 – 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Global Parent Market Overview

- Silanes Market: Value Chain

- List of Raw Material Construction Supplier

- List of Manufacturers

- List of Distributors

- List of End User

- Profitability Analysis

- Forecast Factors – Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Material Construction Landscape

- 3.1. Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Other Macro-economic Factors

- Price Trend Analysis, 2020 – 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Product Type /Material Construction/Organization Size

- Regional Prices and Product Preferences

- Global Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast

- Historical Market Size Analysis, 2020-2025

- Current Market Size Forecast, 2020–2033

- Global Silanes Market Outlook: Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Product Type , 2020 – 2025

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Market Attractiveness Analysis: Product Type

- Global Silanes Market Outlook Application

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Application, 2020 – 2025

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Market Attractiveness Analysis: Application

- Global Silanes Market Outlook End Use Industry

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By End Use Industry, 2020 – 2025

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis: End Use Industry

- Key Highlights

- Global Silanes Market Outlook Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Region, 2020 – 2025

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Region, 2026 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 – 2025

- By Country

- By Product Type

- By Application

- By End Use Industry

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Country, 2026 – 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis

- Europe Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 – 2025

- By Country

- By Product Type

- By Application

- By End Use Industry

- By Current Market Size (US$ Mn) and Volume (Tons)Forecast By Country, 2026 – 2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis

- East Asia Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 – 2025

- By Country

- By Product Type

- By Application

- By End Use Industry

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Country, 2026 – 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis

- South Asia & Oceania Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 – 2025

- By Country

- By Product Type

- By Application

- By End Use Industry

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis

- Latin America Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 – 2025

- By Country

- By Product Type

- By Application

- By End Use Industry

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Country, 2026 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis

- Middle East & Africa Silanes Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 – 2025

- By Country

- By Product Type

- By Application

- By End Use Industry

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Country, 2026 – 2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Product Type , 2026 – 2033

- Mono/Chloro Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Alkyl/Alkoxy Silanes

- Sulfur Silanes

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By Application, 2026 – 2033

- Adhesion Promoters

- Coupling Agents

- Crosslinking Agents

- Surface Modifiers

- Sealants & Binders

- Water Repellents

- Misc.

- Current Market Size (US$ Mn) and Volume (Tons)Forecast By End Use Industry, 2026 – 2033

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Semiconductor

- Paints & Coatings

- Rubber & Plastics

- Energy & Renewables

- Chemicals & Pharmaceuticals

- Misc.

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Wacker Chemie AG

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- KCC Corporation

- OCI Company Ltd

- Dow Inc.

- Momentive Performance Materials Inc.

- Evonik Industries AG

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd

- China Bluestar International Chemical Co. Ltd

- Dalian Onichem Co. Ltd

- Tokuyama Corporation

- Power Chemical Corporation

- Nanjing Shuguang Silane Chemical Co. Ltd.

- BRB International B.V.

- Nanjing Union Silicon Chemical Co. Ltd.

- Nanjing Wanda Chemicals Co. Ltd.

- Miliken Chemical

- Wacker Chemie AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Silanes Market

Silanes Market Size, Share, and Growth Forecast, 2026 - 2033

Silanes Market by Product Type (Mono/Chloro Silanes, Amino Silanes, Vinyl Silanes, Epoxy Silanes, Methacryloxy Silanes, Alkyl/Alkoxy Silanes, Sulfur Silanes, and Miscellaneous Silanes), Application (Adhesion Promoters, Coupling Agents, Crosslinking Agents, Surface Modifiers, Sealants & Binders, Water Repellents, and Misc.), Industry (Automotive & Transportation, Construction & Infrastructure, Electronics & Semiconductor) and Regional Analysis for 2026-2033

Silanes Market Size and Trends Analysis

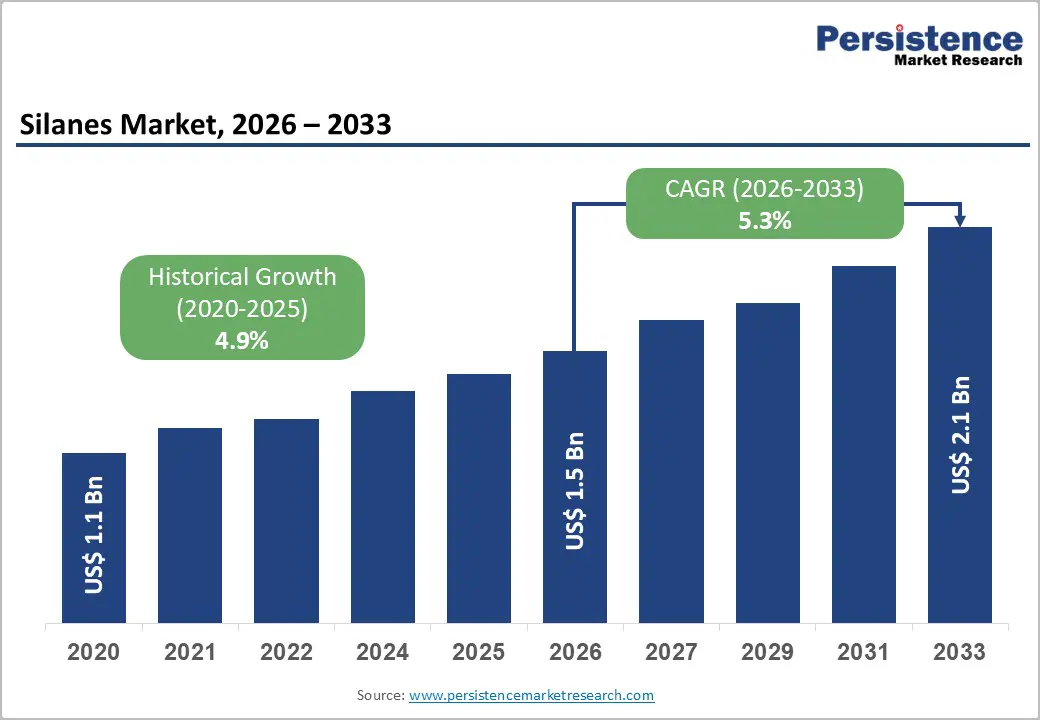

The global silanes market size is likely to be valued at US$ 1.5 billion in 2026 and is projected to reach US$ 2.2 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. This expansion reflects fundamental structural shifts in advanced manufacturing, electronics, semiconductor fabrication, sustainable construction materials, and polymer-composite engineering across global industries. The market's acceleration from a historical CAGR of 4.9% to 5.3% signals intensifying demand for organofunctional silanes that serve as molecular bridges between organic polymers and inorganic substrates, enabling enhanced adhesion, moisture resistance, and mechanical performance.

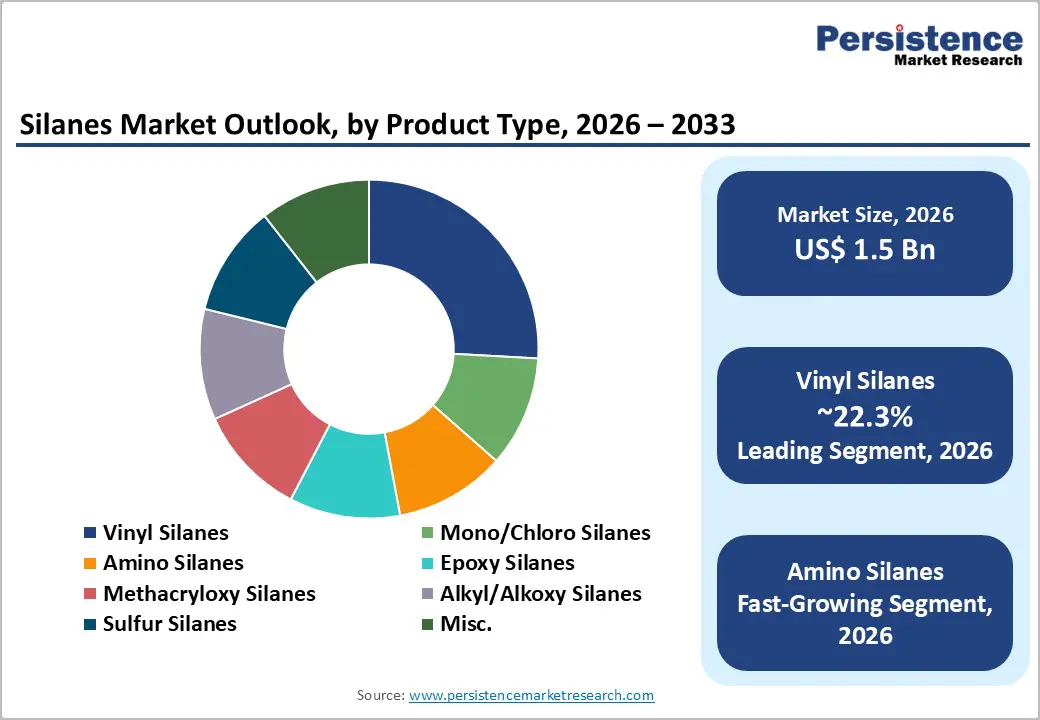

Vinyl silanes maintain foundational market dominance, while amino silanes and specialty epoxy formulations capture disproportionate growth reflecting semiconductor fabrication intensity, EV battery material innovation, and next-generation composite and coating applications.

Key Industry Highlights:

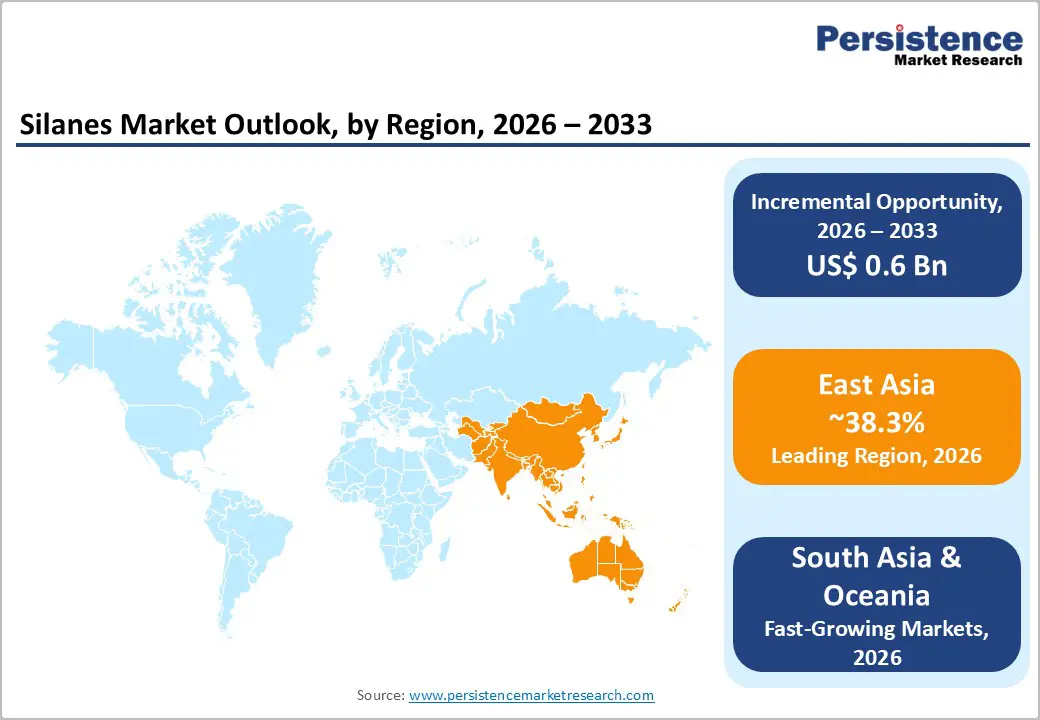

- Leading Regional Market: East Asia holds 38.3% of the Silanes market, driven by China’s semiconductor expansion, automotive growth, and large-scale infrastructure modernisation projects.

- High-Value Regional Contributor: Europe represents 22% of global market value, supported by stringent environmental regulations, sustainable building material adoption, and advanced manufacturing standards.

- Dominant Product Segment: Vinyl silanes lead with 22.3% market share, reflecting their extensive use in silica-reinforced tires, glass-fiber composites, and crosslinking processes.

- Fastest-Growing Product Segment: Amino silanes are the fastest-growing category, driven by pharmaceutical adhesives, semiconductor packaging, advanced coatings, and moisture-resistant automotive applications.

- Regulatory Growth: Low-VOC formulation mandates, green building regulations, and semiconductor fabrication standards across North America, Europe, and Asia Pacific accelerate organofunctional silane adoption.

- Industrial End-user Opportunity: Construction and infrastructure applications dominate with 28.9% share, while electronics and semiconductor applications demonstrate the fastest growth due to advanced microchip fabrication and high-purity silane requirements.

| Report Attribute | Details |

|---|---|

|

Silanes Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 2.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Dynamics

Drivers - Semiconductor Advanced Manufacturing and High-Purity Electronic-Grade Silane Deployment

Semiconductor industry expansion and advanced chip fabrication requirements represent a transformative structural force reshaping the Silanes Market globally, requiring specialised high-purity silane precursors for chemical vapour deposition, thin-film passivation, and next-generation microelectronic manufacturing. China's semiconductor industry has accelerated strategic government support, committing over US$ 150 billion between 2014 and 2030 to strengthen domestic chip capabilities and foster indigenous semiconductor innovation.

China's semiconductor achievements include astronauts launched to a new space station and rovers landed on Mars, both powered entirely by domestically designed and produced semiconductors, demonstrating advanced chip technology sophistication. Despite these successes, China maintains significant technological gaps in leading-edge logic and high-performance memory compared with global leaders, creating sustained demand for advanced silane precursor integration. The global semiconductor industry continues leveraging tetraethyl orthosilicate (TEOS), trichlorosilane, and dichlorosilane as critical precursors for thin-film deposition processes, microelectronic circuit passivation layers, and solar-grade polysilicon production. Emerging AI and cloud computing chip architectures demand increasingly sophisticated passivation and insulation layers, requiring high-purity amino and epoxy silanes for advanced packaging processes.

The silanes market responds through the development of ultra-pure, custom-specification silane formulations compatible with cleanroom and ultra-low defect semiconductor processes. Research indicates organofunctional silanes reflect semiconductor industry intensity and advanced packaging applications.

Construction Infrastructure Modernization and Sustainable Building Materials Integration

Construction and infrastructure sectors represent critical growth vectors for the Silanes Market, driven by regulatory mandates for sustainable building materials, energy-efficient design requirements, and global infrastructure investment cycles. India's construction sector presents particularly strong growth momentum, with government capital expenditure increased by 11.1% to US$ 133 billion in FY 2024-25, equivalent to 3.4 percent of GDP.

The real estate market is projected to reach US$ 5.8 trillion by 2047, contributing 15.5 percent of total GDP, with PM GatiShakti infrastructure initiatives supporting nationwide transportation, housing, and logistics infrastructure. Warehousing infrastructure demand is forecasted to reach 159 million sq. ft. by 2047 at 4% CAGR, creating sustained silane material demand for durable adhesives, sealants, and waterproof coatings. The U.S. construction sector generated US$ 2.2 trillion in annual spending in 2024 with employment of 8.2 million workers.

Europe's construction activity demonstrates regional variation, with strong performance in Poland (+5.7 percent) , Czechia (+4.6 percent), and Portugal (+3.6 percent), reflecting infrastructure modernisation and EU investment cycles. Silanes serve critical roles in sustainable building applications through silane-modified adhesives for green composites, moisture-resistant sealants for energy-efficient window systems, and low-VOC coatings supporting environmental compliance mandates. The Silanes Market benefits from sustained construction demand for organofunctional silanes that improve adhesion of high-performance coatings to diverse substrates, enhance durability and weather resistance of building materials, and support eco-friendly, low-VOC formulations addressing regulatory stringency and customer sustainability preferences.

Restraints - Moisture Sensitivity and Specialised Handling Requirements Increasing Operational Complexity

Silane compounds exhibit inherent moisture sensitivity, requiring specialised storage protocols, strict handling procedures, and stringent environmental controls, thereby increasing operational complexity and cost. Moisture-induced silane hydrolysis and condensation create storage constraints requiring inert atmosphere protection (nitrogen or argon), anhydrous containers, and controlled temperature environments.

Companies face elevated logistics costs, safety compliance investments, and regulatory adherence expenses to meet OSHA and REACH standards. Supply chain disruptions for key silicon-based feedstocks create procurement volatility and cost unpredictability, affecting silane manufacturers' ability to maintain consistent pricing and delivery timelines. These structural constraints disproportionately impact smaller manufacturers lacking specialised infrastructure and create competitive advantages for larger, integrated producers capable of absorbing specialised logistics costs.

Opportunities - Next-Generation AI-Optimised Organofunctional Silanes and Advanced Coating Formulations

The Silanes Market faces a transformative opportunity through the development of AI-augmented material optimisation and machine learning-enhanced silane formulation design, addressing emerging application requirements and performance specifications. AI and machine learning technologies enable novel silane generation through predictive material modelling, computational chemistry optimisation, and high-throughput screening, identifying silane compositions delivering superior adhesion, moisture resistance, thermal stability, and processability characteristics. Advanced silane formulations address emerging application demands in OLED (Organic Light-Emitting Diode) displays, optical fibre coatings, semiconductor advanced packaging, and green tire manufacturing, requiring specialised functional groups enabling precise polymer-inorganic interface engineering.

For semiconductor applications, AI-optimised silanes facilitate precision thin-film deposition, enhanced passivation layer uniformity, and reduced process defectivity, supporting advanced microchip fabrication for AI and cloud computing infrastructure. For construction and coatings, next-generation formulations enable environmentally sustainable, low-VOC coating systems with enhanced durability, weatherability, and aesthetic properties meeting regulatory compliance and customer sustainability preferences.

Machine learning-augmented silane development accelerates innovation cycles and reduces time-to-market for specialised formulations, enabling manufacturers to establish first-mover advantages in emerging application segments. Wacker Chemie AG's expanded GENIOSIL® organofunctional silanes portfolio demonstrates market innovation momentum, with enhanced formulations for adhesives, sealants, coatings, composites, and crosslinked polyethene/polypropylene applications, optimising polymer-filler compatibility and mechanical performance.

Asia Pacific Regional Manufacturing Capacity Expansion and Localized Customer Application Support

The Silanes Market faces substantial opportunity through manufacturing infrastructure establishment in high-growth emerging markets and localised application development center deployment supporting customer innovation and regional market penetration. WACKER's strategic partnership with Chinese specialty silane producer SICO Performance Material culminated in the Application Development Centre in Jining, China, featuring a 2,300 m² facility with multiple labs dedicated to developing high-performance additives for plastics, coatings, and adhesives. This facility integrates research, technical support, and production scale-up capabilities, accelerating market launch cycles and reinforcing speciality silane demand growth in the Asia Pacific region. The center demonstrates manufacturers' recognition of Asia Pacific growth potential and commitment to regional customer support and innovation infrastructure.

Evonik's rubber silanes production facility expansion at Evonik Lanxing (Rizhao) Chemical Industrial Co., Ltd. in Shandong, China, demonstrates strategic capacity establishment addressing regional tire and rubber industry growth. The upgraded facility introduces advanced manufacturing technologies, boosting efficiency, reducing waste, lowering CO2 emissions, and improving product purity, while expanding regional production footprint to include grades previously manufactured exclusively in Europe.

India's construction sector expansion capital expenditure US$ 133 billion in FY 2024-25, real estate projection US$ 5.8 trillion by 2047mand building materials demand creates proportional silane infrastructure requirements. Regional manufacturers establishing production capacity, engineering centres, and customer application laboratories will capture emerging market demand for cost-effective, locally supported silane solutions.

Category-wise Analysis

Product Type Insights

Vinyl silane compounds maintain the dominant market position, representing 22.3% of global market share in 2026, reflecting foundational applicability in silica-reinforced tire manufacturing, glass-fibre composite production, and crosslinking processes. Vinyl silanes' dual reactivity, enabling both filler surface grafting and polymer matrix polymerization, delivers direct performance benefits including reduced tire rolling resistance, enhanced wet-grip performance, and improved mechanical strength in fibre-reinforced composites. Established tire manufacturers prioritise silica-reinforced tread formulations where vinyl silanes optimise filler-rubber interfacial bonding, supporting sustainable tire development aligned with environmental efficiency mandates.

Amino silane compounds represent the fastest-growing product category, driven by pharmaceutical adhesive development, semiconductor packaging integration, and advanced coating applications requiring enhanced adhesion promotion and moisture-resistant surface modification capabilities. Amino silanes' bifunctional reactivity, delivering reactive amino groups and hydrolyzable inorganic alkoxysilyl groups, enables multifunctional applications spanning adhesion promotion, silane surface modification, and product formulation enhancement. SiSiB's comprehensive amino silane portfolio, including mono-amino silanes, di-amino silanes, tri-amino silanes, piperazinyl silanes, and cyclohexyamino variants demonstrates market sophistication and application specialisation intensity. Automotive industry adoption of amino silane-enhanced adhesives improves durability and performance, supporting vehicle safety and reliability.

Industry Insights

Construction and infrastructure represents the dominant end-user category, with a 28.9% share in 2026, reflecting universal applications across waterproof coatings, durable adhesives, high-performance sealants, and sustainable building-material integration. Construction sector expansion across regions, including India's government capital expenditure at 11.1 percent increase to US$ 133 billion (FY 2024-25), U.S. annual spending of US$ 2.2 trillion, and EU regional variation with Poland +5.7%, Czechia +4.6 percent, Portugal +3.6%, directly support sustained silane material demand.

The segment's market dominance reflects established silane integration across construction supply chains, where organofunctional silanes enable enhanced adhesion of protective coatings, moisture resistance of sealants, and durability of composite building materials. Construction industry preference for established silane manufacturers with proven compliance certifications, regional support infrastructure, and documented performance histories supports competitive consolidation favouring major integrated producers.

Electronics and semiconductor applications represent the fastest-growing end-use segment, driven by advanced chip fabrication expansion, high-purity silane precursor deployment, and semiconductor advanced packaging requirements. Global semiconductor fabrication expansion supported by China's US$ 150 billion investment commitment and international fab establishment in Asia Pacific, the U.S., and Europe creates sustained demand for tetraethyl orthosilicate (TEOS), trichlorosilane, and dichlorosilane, supporting thin-film deposition, passivation layer formation, and advanced microelectronic manufacturing.

Electronics industry growth, including India's domestic production expanding from US$ 29 billion to US$ 101 billion, with mobile phone manufacturing surging 21-fold to US$ 49.3 billion over the past decade, creates proportional silane demand across semiconductor packaging and consumer electronics manufacturing.

Regional Insights and Trends

North America Silanes Market Trends

North America represents a mature, technologically advanced market commanding approximately 20% of the global Silanes Market share in 2026, characterised by established OEM supply chain networks, regulatory compliance intensity, and substantial investment in semiconductor fabrication and advanced manufacturing infrastructure. The U.S. construction sector's annual spending of US$ 2.2 trillion with employment of 8.2 million workers provides substantial silane demand for protective coatings, durable adhesives, and sustainable building materials. Semiconductor fabrication expansion across Arizona, Texas, and other regions supported by the CHIPS and Science Act funding drives demand for high-purity electronic-grade silanes supporting advanced chip manufacturing and semiconductor packaging.

Sila Nanotechnologies' Moses Lake silicon anode manufacturing plant represents a major silane demand driver, with a facility designed for expansion to over 200–250 GWh capacity requiring substantial, sustained silane supply from domestic producers, including REC Silicon. North American regulatory environment emphasises VOC compliance, REACH chemical restrictions, and environmental sustainability standards, creating market preference for organofunctional silanes, enabling low-VOC formulations and sustainable coating solutions. Regional market growth projections range from 4.5–5.5% annually, reflecting market maturity balanced against semiconductor fabrication intensity and advanced manufacturing modernisation investments.

East Asia Silanes Market Trends

East Asia is likely to account as the fastest-growing region, commanding approximately 38.3% regional market share in 2026 and demonstrating exceptional growth momentum driven by semiconductor fabrication dominance, construction infrastructure expansion, and automotive manufacturing intensity. China's semiconductor industry commitment of over US$ 150 billion for domestic chip capability development drives substantial demand for high-purity silane precursors supporting chemical vapor deposition, thin-film formation, and advanced microelectronic manufacturing. WACKER's strategic partnership with SICO Performance Material and Application Development Centre inauguration in Jining, China, demonstrates a major manufacturer's commitment to regional market penetration and customer application support infrastructure. Evonik's rubber silanes facility expansion at Rizhao, China, supports regional tire and rubber industry demand for organofunctional silanes, enabling enhanced elastomer performance and sustainable tire formulation.

East Asia's estimated annual growth rates range from 7 to 10 percent, substantially exceeding global averages, reflecting structural manufacturing expansion, semiconductor fabrication intensity, and emerging market infrastructure investment cycles.

Europe Silanes Market Trend

Europe represents a mature, technologically sophisticated market commanding approximately 22% of the global Silanes Market share in 2026, characterised by stringent environmental regulations, advanced manufacturing standards, and substantial investment in sustainable building materials and circular economy initiatives.

The EU semiconductor industry's contribution of approximately €51 billion in 2022, with double-digit growth of 12.3 percent, drives demand for high-purity silane precursors supporting advanced chip fabrication and semiconductor packaging. European regulatory frameworks, including REACH chemical restrictions, VOC compliance standards, and circular economy mandates, create market preference for organofunctional silanes, enabling sustainable, low-VOC coating formulations and environmentally compliant adhesives and sealants.

Evonik's Smart Effects division, merging Silica and Silanes business lines, demonstrates market leader commitment to tailored, high-value solutions supporting green tire manufacturing, advanced composites, and sustainable material applications aligned with EU environmental objectives. Regional market growth projections range from 4.8 to 5.8 percent annually, reflecting market maturity balanced against semiconductor innovation momentum and environmental compliance intensity driving sustainable material adoption.

Competitive Landscape

The global silanes market is moderately consolidated, dominated by a few key players who control the majority of high-performance and speciality silane production, while smaller regional manufacturers serve niche applications. Leading companies such as WACKER Chemie AG, Evonik Industries AG, OCI, Sila Nanotechnologies, Dow Inc., and Momentive Performance Materials leverage advanced R&D, strategic partnerships, and regional capacity expansions to maintain technological leadership.

WACKER and Evonik have strengthened their presence in Asia through joint ventures and facility expansions, while OCI and Sila focus on supplying high-purity silanes for next-generation lithium-ion battery anodes. Dow and Momentive maintain dominance in coatings, adhesives, sealants, and composites applications. High entry barriers, including complex manufacturing, stringent quality standards, and large capital investment, restrict new players and reinforce the influence of established firms.

Key Industry Developments

- On Jan 22, 2025, Evonik launched its Smart Effects division, merging its Silica and Silanes business lines under the Advanced Technologies unit with 3,500 employees worldwide. This strategic move strengthens Evonik’s silane and silica technology platforms, enhances operational efficiency, and enables tailored, high-value solutions for automotive tires, electronics, lithium-ion batteries, and building protection markets. The merger also emphasises sustainability and circular innovation, reinforcing Evonik’s position as a global leader in speciality silanes.

- On Sept 24, 2024, Sila Nanotechnologies signed a long-term silane supply agreement with REC Silicon to secure high-purity, US-produced silane for its Titan Silicon anode material used in EV batteries. This was followed by the opening of Sila’s silicon anode plant in Moses Lake (2025), designed to scale from 2 to 5 GWh to over 200 to 250 GWh. These developments highlight the growing strategic importance of silane supply for next-generation lithium-ion batteries and position silane as a critical feedstock for the fast-growing EV and clean energy sector.

Companies Covered in Silanes Market

- Alcatel Submarine Networks

- KCC Corporation

- OCI Company Ltd

- Dow Inc.

- Momentive Performance Materials Inc.

- Evonik Industries AG

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd

- China Bluestar International Chemical Co. Ltd

- Dalian Onichem Co. Ltd

- Tokuyama Corporation

- Power Chemical Corporation

- Nanjing Shuguang Silane Chemical Co. Ltd.

Frequently Asked Questions

The global silanes market is projected to be valued at US$ 1.5 Bn in 2026.

The Vinyl Silanes segment is expected to account for approximately 22.4% of the global silanes market by Processing Treatment in 2026.

The silanes market is expected to witness a CAGR of 5.3% from 2026 to 2033.

The silanes market growth is driven by rising demand for high-purity silanes in advanced semiconductor manufacturing and expanding applications in sustainable construction and infrastructure materials.

Key market opportunities in the Silanes Maket lie in AI-optimized organofunctional silane development for advanced electronics, coatings, and green tires, along with expanding regional manufacturing and application support in high-growth Asia Pacific markets.

Key players in the Silanes Market include WACKER Chemie AG, Evonik Industries AG, OCI, Sila Nanotechnologies, Dow Inc., and Momentive Performance Materials.